izusek

Investment thesis

MP Materials (NYSE:MP) delivered another stellar earnings report. Besides the explosive growth, the company managed to turn most of its revenue into free cash flow. However, since the market looks ahead, we need to be careful about the prospects for the global NdPr price.

Market overview – How’s the demand for NdPr magnets?

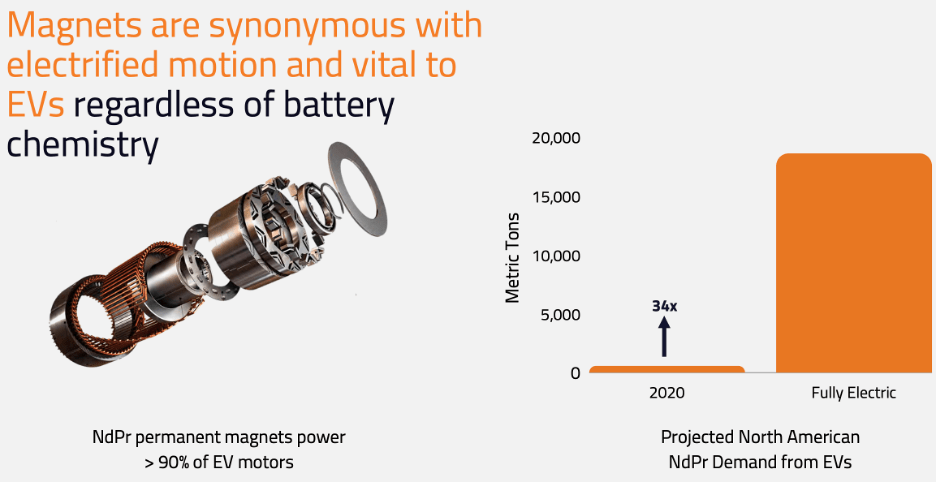

Although NdPr permanent magnets can be used for a wide variety of products (consumer electronics, wind turbines, robotics, etc.), the fastest growth is still expected within the electric vehicles (EVs) space. EVs are expected to account for 16% of the total number of cars sold in 2025 and for ~70% of all the cars sold in 2030, according to IEA and BloombergNEF, cited in The BMO Rare Earth Supply Chain Conference. As a result, it is expected that the demand for NdPr in the US will skyrocket:

The BMO Rare Earth Supply Chain Conference

MP Materials seems to be in a great position to capitalize on the environment envisioned here. The company is the biggest producer of rare earth oxides (REO) outside of China and it had a market share of 15% of global REO produced in 2021. Let’s look at how well MP Materials executes:

Financials

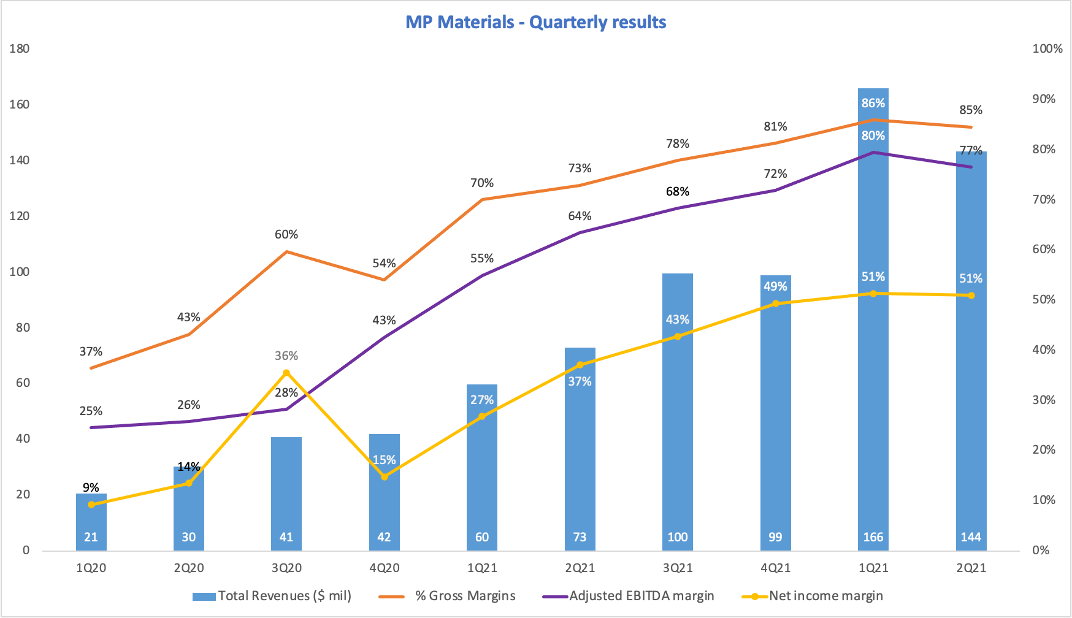

MP Materials grew its revenue 97% YoY while gross margin stabilized around 85%, only 100 bps lower than 1Q22. Moreover, even if adjusted EBITDA margin slightly decreased, the net margin remained above 50% for Q2, which is a phenomenal result.

MP Materials 10-Q 2Q22

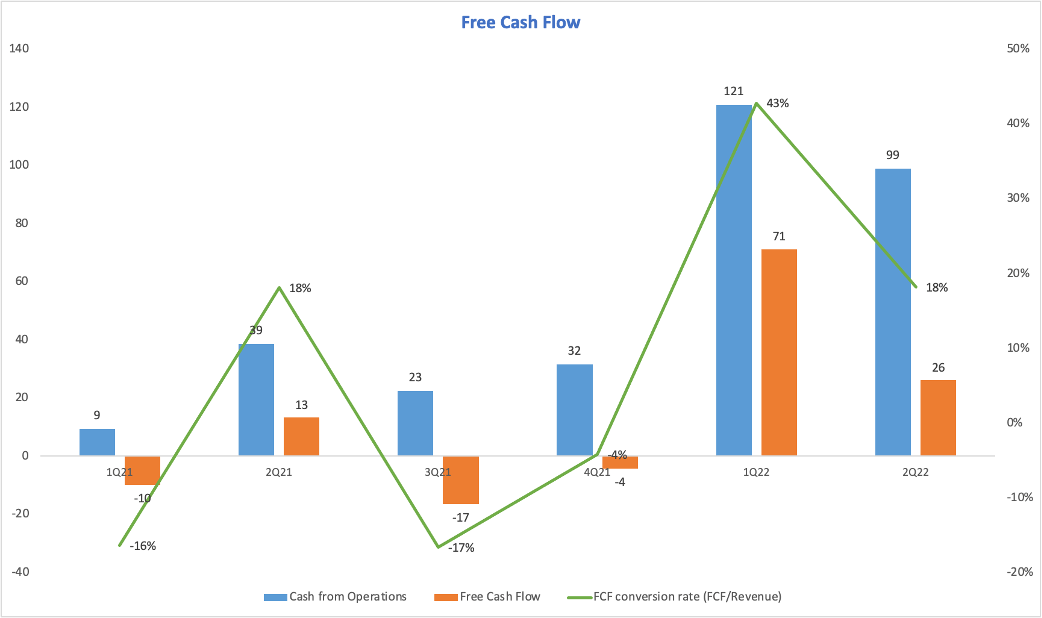

Although the operational metrics remained solid, another crucial aspect that makes this quarter a success is the cash flow statement. In Q2 the company had around $26 million in FCF, growing 100% from 2Q21 and represents around 18% FCF conversion rate:

MP Materials 10-Q 2Q22

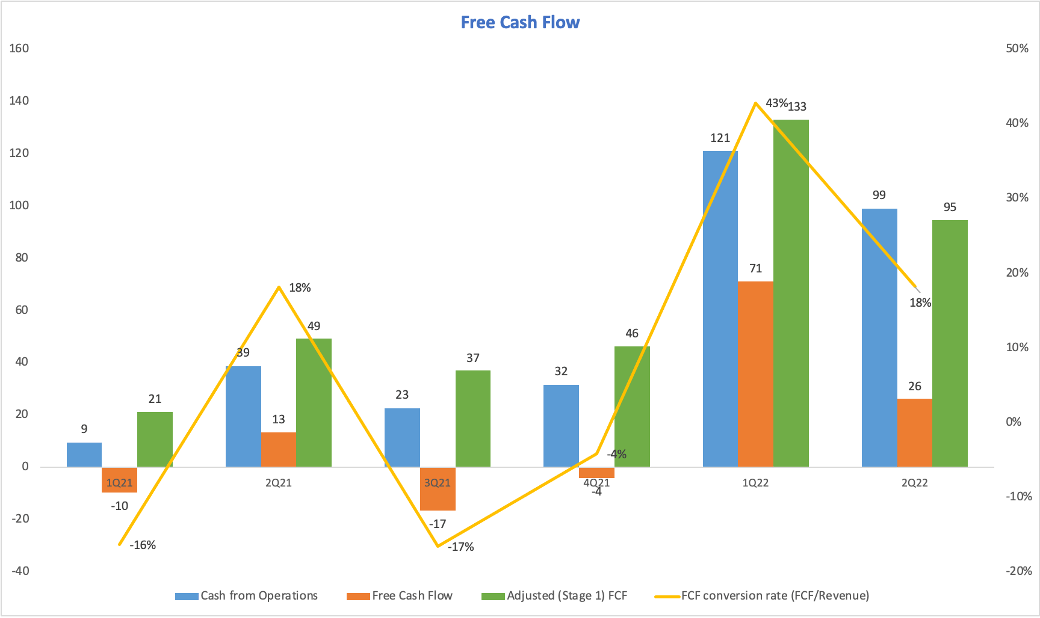

Still, keep in mind that this is the FCF defined as Operating CF – CAPEX. Since MP operates in an asset-heavy industry, it is forced to spend considerable amounts on capital investments that will fuel future growth from phases II and III of MP’s long-term plans. As a result, this is a situation where it’s also useful to look at the adjusted free cash flow, since that is the FCF that stage 1 generates. As we can observe below, MP Materials has generated more FCF from stage 1 in the first six months of 2022 ($228 million) than it has for the entirety of 2021 ($154 million):

MP Materials 10-Q 2Q22

This proves that the current activity is generating a lot of free cash flow for MP Materials and gives the company strength to undertake its investments in stages II and III. Next up, to see why MP Materials’ results were so good, let’s look at the company’s KPIs.

Key Performance Indicators

MP Materials 10-Q 2Q22

Firstly, the most significant factor is the NdPr selling price. This remained constant as compared to 1Q22 and grew ~90% YoY. This led to a consolidation of the gross margin per MT as the production cost increased only 10% Q/Q and 13% YoY. This proves that in spite of the massive growth in NdPr price, MP Materials is able to keep the extraction costs in check, which creates significant operating leverage.

Checking on the current price for NdPr, it looks like it slightly decreased since May, when I first wrote about MP Materials, with NdPr sitting around $110/kg as compared to $140/kg. This is the biggest decrease for NdPr price in the last 18 months, when this parabolic move began. It will be interesting to see if and how much will MP’s KPIs decrease in the subsequent quarters:

Metal.com

Management

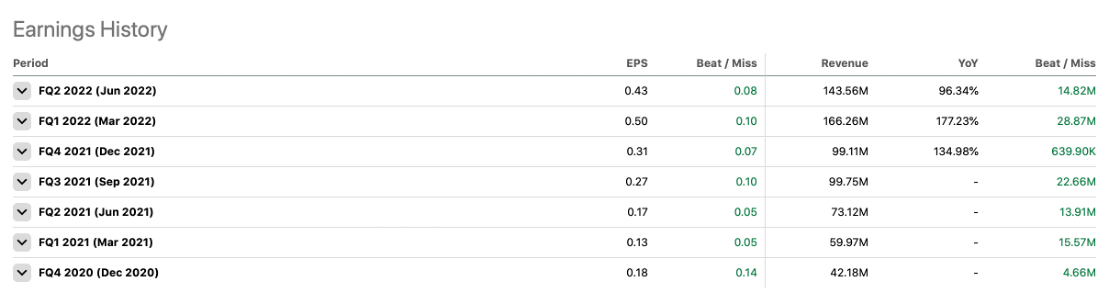

I believe that MP’s management has navigated the current market environment very well, and I think that for the moment there are no signs of slowing down. Even if the NdPr price might decrease below $100/kg, as long as MP Materials keeps its operating costs low, their margins will remain strong. The reason why I trust the management is because they were able to deliver on every quarter since the company got listed (seven in a row) as the company beat both earnings and revenue estimates with ease:

Seeking Alpha

Risks

Since, in this case, the risk related to investing in MP Materials are quite distinctive, I believe there are two main unique risks regarding the company: firstly, evident by now, a sudden drop in the global NdPr price that might put downward pressure on MP’s margins. Second, the company is investing really high amounts of capital in long-term assets. Aswath Damodaran argues that this is especially risky in periods of high inflation. MP Materials has laid down its long-term plan since 2020, but now with inflation at an all-time high, there’s a high chance that its initial cost estimates are outdated. Although the company didn’t provide an update on the cost side in 2Q22, it has stated that hiring is accelerating for stages II and III.

What the company did reveal are the capitalized expenditures for H122. These are related to assets under construction to support MP’s Stage II optimization project and magnet manufacturing facility as a part of Stage III. Still, the $1.2 billion that MP Materials has on its balance sheet as cash & equivalents gives me confidence that the company has plenty of room for maneuver:

MP Materials 10-Q 2Q22

Valuation

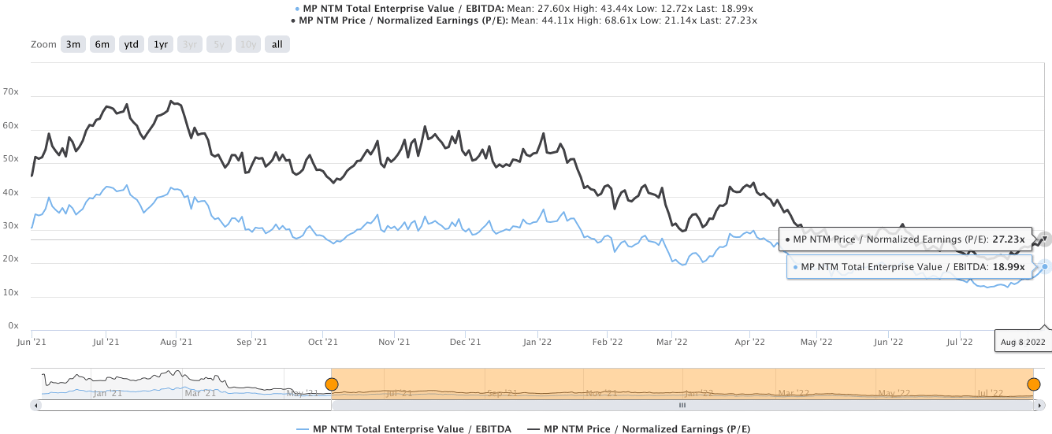

MP Materials remains one of the more expensive mining companies. Although it seems richly valued with a P/S around 12X, when looking at Enterprise Value/EBITDA multiple, MP trades around 19X. In terms of EV/Normalized Earnings, MP trades around 27X, which is slightly higher than the lowest 21X normalized earnings registered in July 2022.

TIKR.com

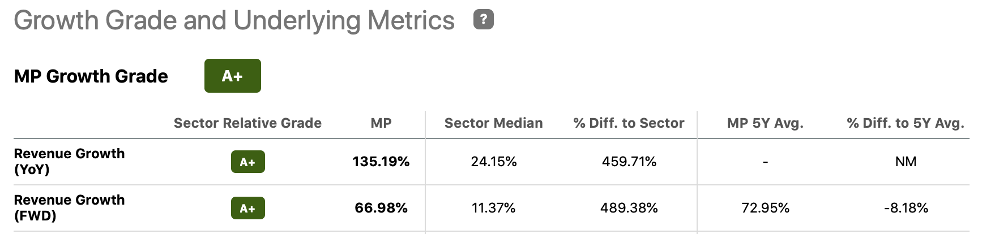

Even if the Seeking Alpha valuation gives the company a very low rating because of its much higher multiples compared to its peers, I believe that the 67% forward revenue growth is totally deserving of a premium, as compared to the 11% sector median:

SeekingAlpha.com

Where to buy – Technical analysis

Obviously, the stock will probably do what the broad market will. Even with great execution from MP, if the whole market drops, MP’s stock will probably do the same. After a recent 30% increase from the lows, the stock found resistance around the 100 and 200 SMA (blue and red lines) and seems to be forming a bearish short-term pattern known as an evening star reversal:

TradingView.com

Without going too deep into the technical analysis, I believe that the stock will have a small retracement following the 30%+ run that it had during the last two weeks. I hold my view that the stock is a buy at these levels, just don’t open a full position all at once. Always leave some room for adding on the retracement. Another strong area of support is the $30 price, so if the price gets that low, buying there would be an excellent opportunity.

Final thoughts

Given the huge gap between the demand and supply for NdPr and permanent magnets, I believe that MP Materials has a unique position within the western hemisphere. The biggest challenge for the management will be keeping margins high and maintaining the same free cash flow conversion rate in a period of decreasing NdPr price. Still, with the evidence that we have so far, it seems like management is well-prepared and will continue to execute, so I maintain my Buy rating for MP Materials’ stock.

Be the first to comment