David Ramos/Getty Images News![]()

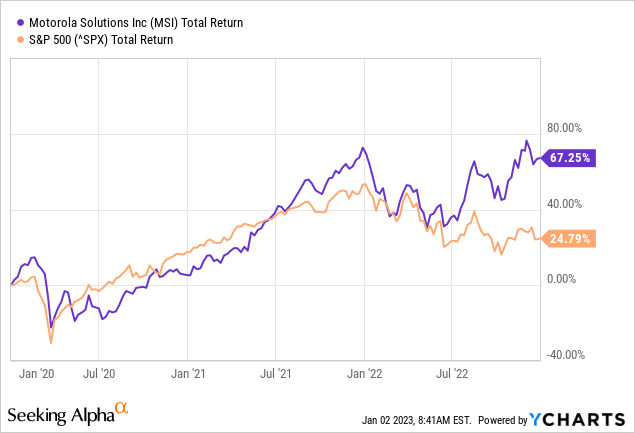

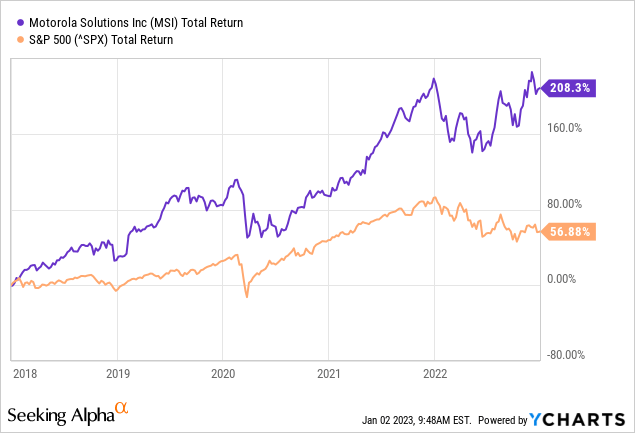

Motorola Solutions (NYSE:MSI) has been a strong stock during the last few years and has significantly outperformed the broad S&P 500 (see below). Much of that strength comes from a relatively entrenched and “sticky” mission critical LMR business that’s relatively recession resistant due to government sales. That being the case, MSI throws off strong free cash flow that management has been using to invest in relatively small strategic and accretive acquisitions that have opened up new market opportunities for growth. As a result, the company has delivered five straight years of double-digit dividend increase and the future looks bright going forward.

Investment Thesis

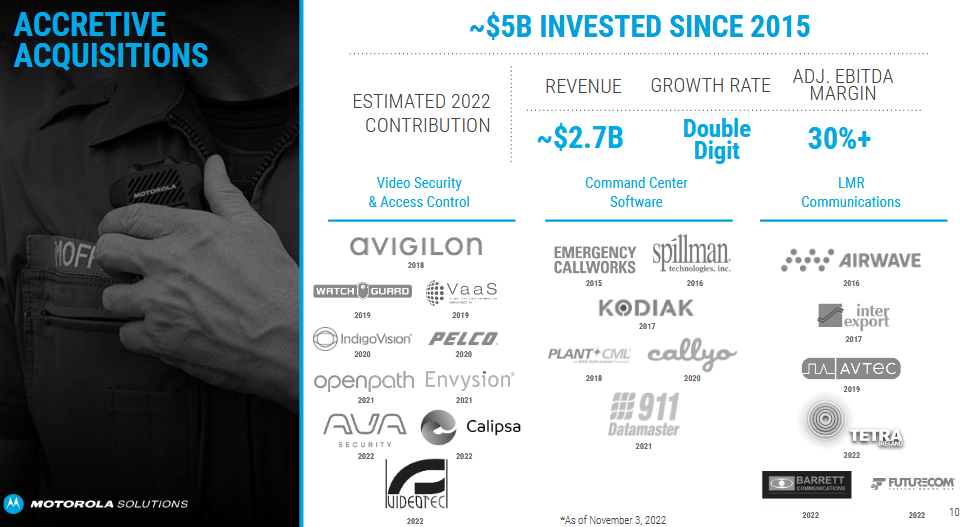

As I reported on Seeking Alpha back in February 2021, Motorola Solutions is the largest supplier of land-mobile-radio (“LMR”) in the U.S. and has a thriving mission critical communications business with state, local, and federal government agencies and globally as well. Meantime, the company has been using the free cash flow generated by its LMR business to invest in numerous strategic and accretive acquisitions (see below) to grow the company’s Software & Services Segment and to improve its already strong competitive profile. Margins are strong, annual recurring revenue (“ARR”) is growing, and new market opportunities have expanded the company’s TAM (see MSI: Record Backlog, Strong FCF, 11% Dividend Boost, Emerging ARR Story). These new ARR growth opportunities include Video Security & Access Control and Command Center Software:

Motorola Solutions

Earnings

In November, MSI released strong Q3 earnings. It was a beat on the top line (by $50 million) and also a bottom line (by $0.12) beat. Highlights included:

- Sales of $2.4 billion, were up 13% vs. a year ago

- GAAP EPS was $1.63, down 7% from a year ago, but that was inclusive of a $147 million fixed asset impairment charge for the expected exit from the Emergency Security Network (“ESN”) contract in the UK.

- Non-GAAP EPS of $3.00 was up 28% yoy.

- During the quarter, MSI generated $388 million of operating cash flow, up $12 million yoy.

- Free cash flow was $318 million, or an estimated $1.84/share based on 172 million fully-diluted shares.

- Margin was strong: non-GAAP earnings as a percentage of sales was 35.7%. Non-GAAP operating margin was up 220 basis points yoy.

During the quarter, Products & Systems Integration (the “PSI” Segment) sales were up 15% while Software & Services sales were up 8%. Video sales were up 33% and LMR sales were strong as well (+9% yoy).

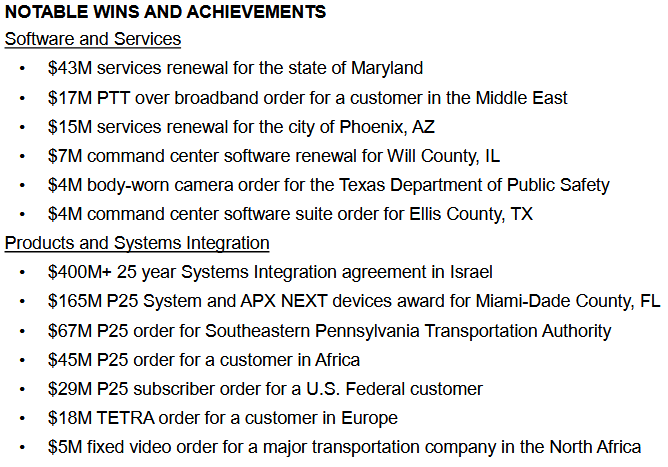

MSI continues to benefit from a pandemic related rebound in sales and the stream of new contract wins continued to be impressive in Q3:

MSI

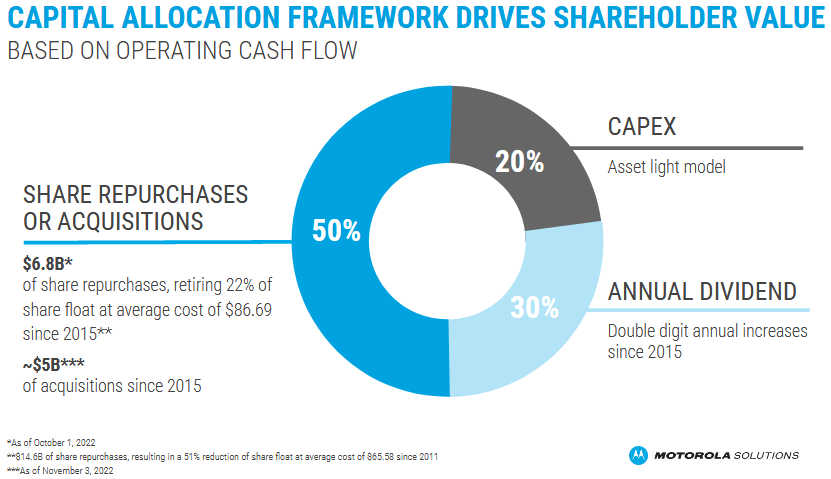

Capital allocation during the quarter was rather typical of what shareholders have come to expect from MSI:

- $132 million in cash dividends

- $94 million of share repurchases

- $70 million of capital expenditures

- The acquisition of Barrett Communications for $18 million (net of cash acquired)

Note the relatively small cap-ex allocation as compared to shareholder returns. This is an indication of MSI’s asset-light business strategy that has been so beneficial for shareholders.

Going Forward

As I have been pointing out in my Seeking Alpha articles, MSI continues to have a very strong backlog. Indeed, the Q3 ending backlog was a record $13.5 billion – up a very strong 19% yoy:

MSI

Motorola’s strong and record backlog – and its long-term track record of increasing that backlog – is a primary investment catalyst for the company going forward. I say that because the backlog gives a clear line-of-sight for growth and gives the management team the confidence to continue to reward investors with strong dividend growth.

For Q4, MSI expects revenue growth of ~9% yoy and non-GAAP EPS in the range of $3.40-$3.45 per share. The guidance assumes ~$90 million in foreign exchange headwinds due to the still strong U.S. dollar.

For full-year FY2022, MSI raised revenue growth guidance from ~8% growth to a range of 9.25%-9.5%. The midpoint of non-GAAP EPS was raised to $10.195/share from the previous $10.08/share. The company expects full-year foreign exchange headwinds of ~$220 million.

Going forward, investors can expect Motorola to continue the successful strategy it has used in the recent past. This includes exploiting a $50 billion TAM opportunity as well as continuing its successful track-record of making and integrating relatively small strategic acquisitions (typically accretive) to improve its competitive position in these markets:

MSI

Increasing video and software sales should continue to boost margin going forward.

Shareholder Returns

As mentioned previously, MSI strong free cash flow profile – along with its technology-based asset-light business model – has led to excellent returns for shareholders:

MSI

Note that since 2015, share buybacks have retired 22% of the outstanding float at an average cost of $86.69/share (the stock closed Friday at $257.71). Clearly, MSI’s stock buyback program has been a wise use of shareholder capital.

As for the dividend, on Nov. 17 MSI raised the quarterly dividend by 11.4% to $0.88/share. That is the fifth-straight year of double-digit dividend increases. On an annual basis, that equates to $3.52/share for a current yield of 1.37%. As compared to the new quarterly dividend of $0.88, and given the $1.84/share in FCF generated in Q3 mentioned earlier, it’s clear that MSI has significant room to expand the dividend going forward.

Risks

MSI’s forward P/E is currently 25.3x. That’s relatively rich and is an above market multiple. However, in my opinion the premium is rational given MSI’s strong backlog (an estimated 1.5x FY22 expected revenue), its strong free cash flow profile, and its relatively “sticky” governmental mission critical businesses.

However, as we saw from the company’s decision to back away from its UK ESN businesses due to the “future service potential of the assets is limited,” Motorola does face competition for is LMR-based Police and Emergency Services. That said, this is a relatively “sticky” business for Motorola given the proprietary Motorola designed networks that these services run on and the significant expense (and short-term risks) that would evolve in a customer attempting to switch to a new vendor.

LTE networks could prove to be strong competition to MSI’s LMR business. Specifically, the recently merged L3Harris (LHX) may present competent competition and erode MSI’s market share.

The $400 million contract with Israel could cause share divestment by institutions and individuals that do not agree with Israel’s policy with respect to the Palestinians and continued Israeli settlements in opposition to votes by members of the United Nations.

Foreign currency headwinds persists, but the U.S. appears to have peaked in September, so the worst may in the rear-view mirror. That said, the Federal Reserve is still in a quite hawkish stance, and future interest rate increases could result on downward pressure on MSI stock.

Summary and Conclusion

I reiterate my BUY rating on Motorola Solutions given its record backlog, its large TAM opportunity, its growing ARR, and its asset-light business model. The combination has enabled MSI to return significant cash to directly to shareholders in the form of a strong and growing dividend while at the same time significantly reducing the outstanding share count via share buybacks. I don’t see that changing anytime soon and this strategy will continue to benefit MSI shareholders in 2023 and beyond.

I’ll end with a five-year total returns comparison of MSI vs. the S&P 500:

Be the first to comment