Mario Tama

Morgan Stanley (NYSE:MS) is one of the largest financial services companies in the world and its dominance has grown in the last decade. CEO James Gorman has transformed the investment bank into a wealth management giant. Q4’22 and FY22 results shows the success of this transition. Morgan Stanley showed remarkable resilience amid an abundance of macro headwinds. The transformation is not yet complete. In its Strategic Update, Morgan Stanley shows it will double down on its expansion in Wealth Management. This will prove to be valuable as its resilience will only increase from here.

In addition, recent layoffs in the financial industry have shaken confidence on Wall Street, but Morgan Stanley’s headcount remains relatively stable proving its confidence in its business. However, I believe continued rate hikes and inflation will continue to cause Morgan Stanley to be defensive and succession could be a risk as James Gorman’s retirement could cause a change in strategy. Although Morgan Stanley has shown resilience, I believe its valuation is looking increasingly expensive. With high uncertainty in 2023, in my view, it is hard to justify the current valuation. Therefore, I believe Morgan Stanley is a hold, but would be a buy on any major pullback in 2023.

Q4 2022 and FY 2022 Earnings

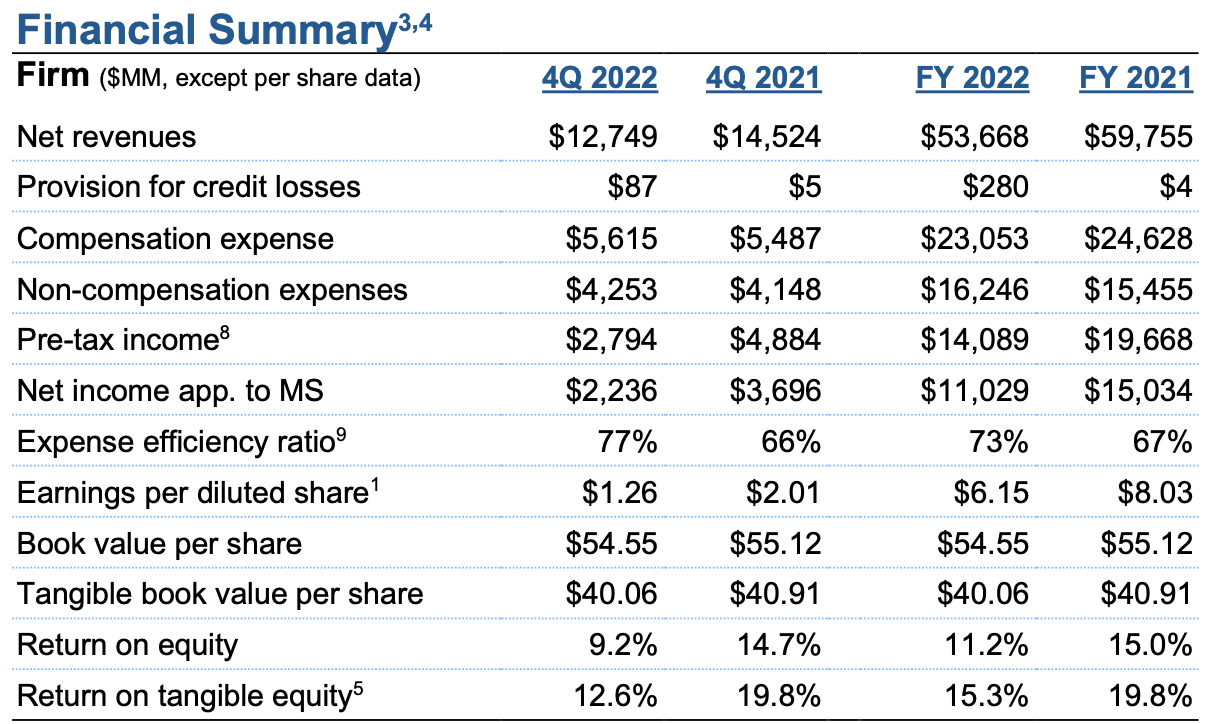

Morgan Stanley’s recent earnings showed resilience. For Q4, their net revenue was $12.7 billion, down from the prior year’s $14.5 billion. For FY, their net revenue was $53.7 billion, down from $59.8 billion in the prior year. Their EPS showed larger declines. Q4’22 EPS of $1.26 is significantly down from Q4’21 EPS of $2.01. FY22 EPS of $6.15 is also much less than FY21 EPS of $8.03. Note that FY comparisons may have been impacted by its Eaton Vance Corp. acquisition and Q4’22 results were affected by the high severance costs in December. Nonetheless, figures were better than many were expecting and the stock surged following this earnings release.

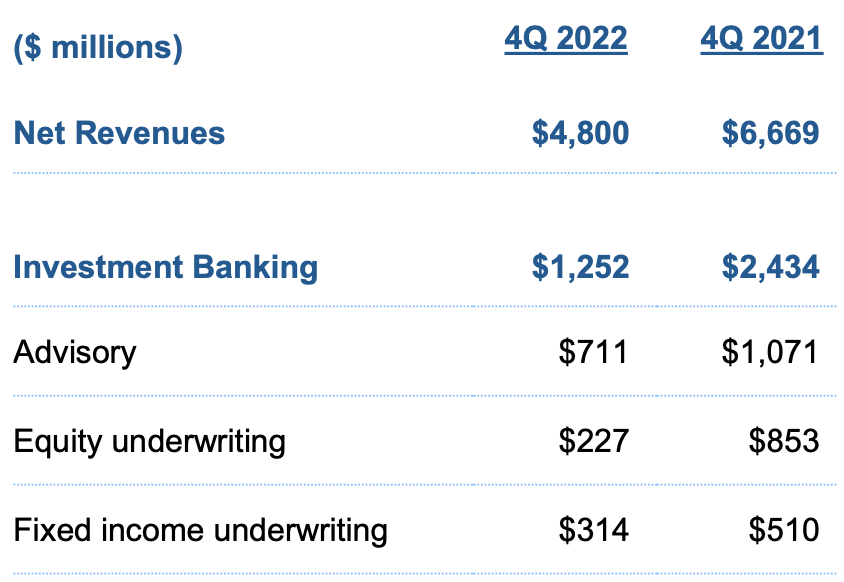

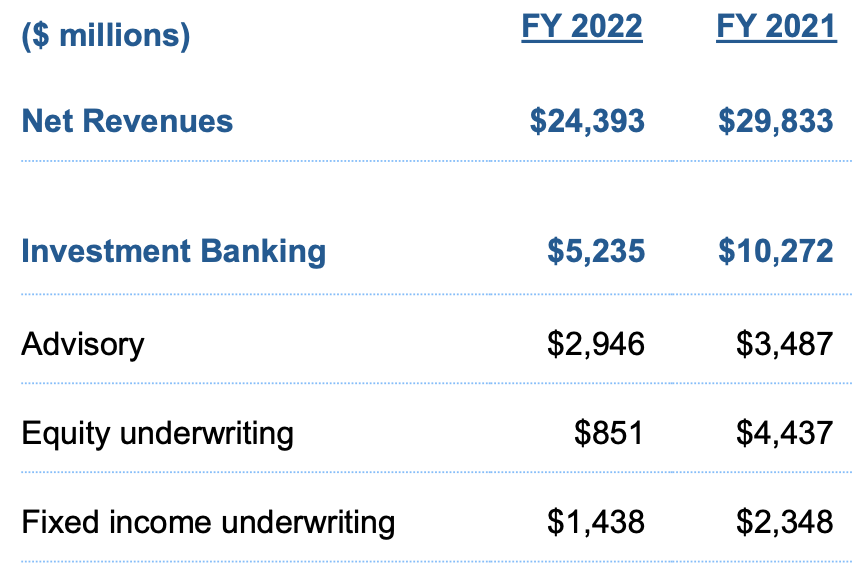

As an overview, Institutional Securities reported weak results as Investment Banking revenues were crushed by low investor sentiment.

MS Q4/FY 2022 Earnings

Wealth Management showed strong resilience to headwinds while Investment Management showed poor results. Provisions for Credit Losses also increased greatly in both Q4 YoY and FY terms, showing an increase in cautiousness. Overall expenses were also up with the only exception being FY compensation expense which was down from $24.628 billion to $23.053 billion, likely as a result of a decrease in performance-linked compensation.

In addition, the expense efficiency ratio also worsened in Q4 YoY and FY terms reflecting a difficult business environment in 2022. Lastly, ROTCE was also significantly down from the prior year’s 19.8%. Even though results were not great compared to the prior year, after accounting for the tough macro environment of 2022, I believe Morgan Stanley still had decent numbers.

Institutional Securities

Institutional Securities’ results were directly impacted by interest rates and macro environment. In both Q4 YoY and FY terms, they suffered large decreases in net revenues.

MS Q4/FY 2022 Earnings

Pre-tax income also showed steep drops. Its Q4 pre-tax income dropped to $748 million from Q4’21’s $3.0 billion. For the FY, this figure dropped to $6.7 billion from the prior year’s $11.8 billion. Within this unit, Investment Banking showed the worst performance as revenues were basically halved for both Q4 YoY and FY. In particular, equity underwriting performed the worst reflecting low global IPO activity. In addition, advisory revenues and Fixed Income underwriting both showed Q4 YOY and FY declines due to lower M&A activity and lower bond issuance, respectively.

MS Q4/FY 2022 Earnings

Their Equities trading also showed weakness with revenues down from 2021. This was a slight surprise for me given that Equity trading revenues usually increase when there is high volatility in the markets. Given 2022’s volatile environment, I expected stronger results from Equities. Their Fixed Income showed strength likely as a result of rate hikes with both Q4 YoY and FY gains versus the prior year. In their “Other” revenues, they had negative revenues as a result of mark-to-market losses on corporate loans.

As expected, their Institutional Securities unit showed weakness in a tough environment and reaffirms the fact that an over-reliance on revenues from this unit would cause volatility in company earnings. I believe it makes sense for Morgan Stanley to continue to move away from these traditional sources of income in its attempt to de-risk its business further.

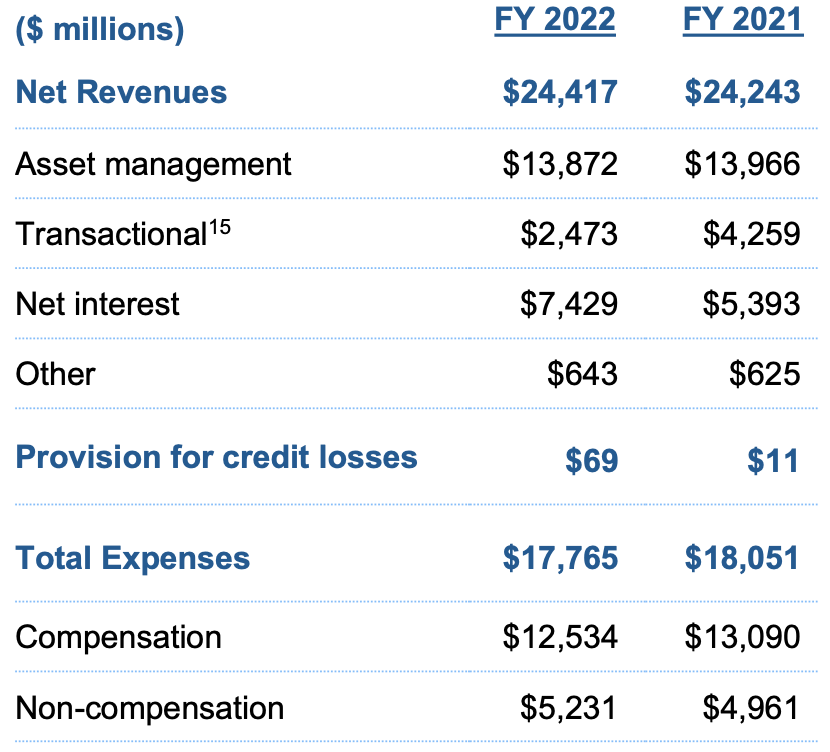

Wealth Management

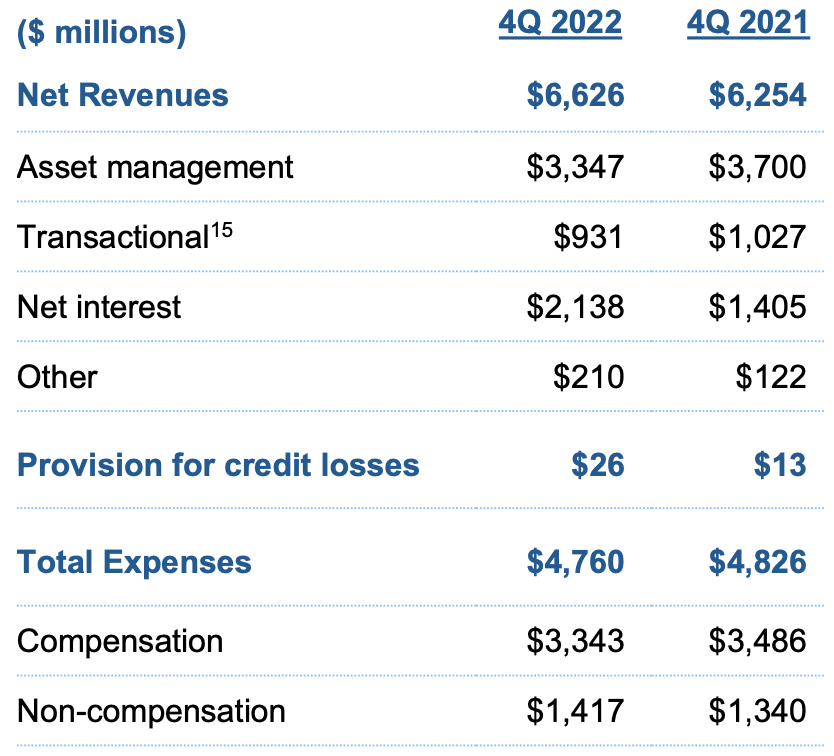

This unit was the main story of their earnings. Results were rock solid for both Q4 and FY. It had an increase in net revenues in both Q4 YoY and FY.

MS Q4/FY 2022 Earnings

They had a 27.8% pre-tax margin for the quarter. For FY, their revenues also showed increase from the prior year while showing a 27.0% pre-tax margin. Pre-tax income for both Q4 YoY and FY were also up from the previous year as they reported $6.6 billion in pre-tax income for FY22 vs. $6.2 billion in FY21. The only blemish in this unit’s results was a decrease in fee-based client assets. This figure declined from $1,839 billion in 2021 to $1,678 billion, reflecting market weakness. This is quickly forgiven as they had positive Fee-based asset flows of $20.4 billion in Q4 and $162.8 billion in the FY.

MS Q4/FY 2022 Earnings

They also had positive net new assets $51.6 billion in Q4 and $311.3 billion in the FY. Both Fee-based asset flows and net new assets were less than in the prior year, but nonetheless showed great strength in the attractiveness of Morgan Stanley’s Wealth Management to clients. Digging deeper, they had weaker asset management revenues in both Q4 YoY and FY. Transactional revenues also weakened in both Q4 YoY and FY terms. Net Interest revenue was the star of this unit’s results as it showed major increases as a result of higher rates and lending growth. Provisions for credit losses increased significantly, reflecting a conservative stance.

Although there were some areas of weakness within their Wealth Management unit, I believe the unit as whole showed resilience in a tough environment. This unit showed record net revenues in both quarterly and annual terms proving Wealth Management to be a very stable source of revenues and earnings.

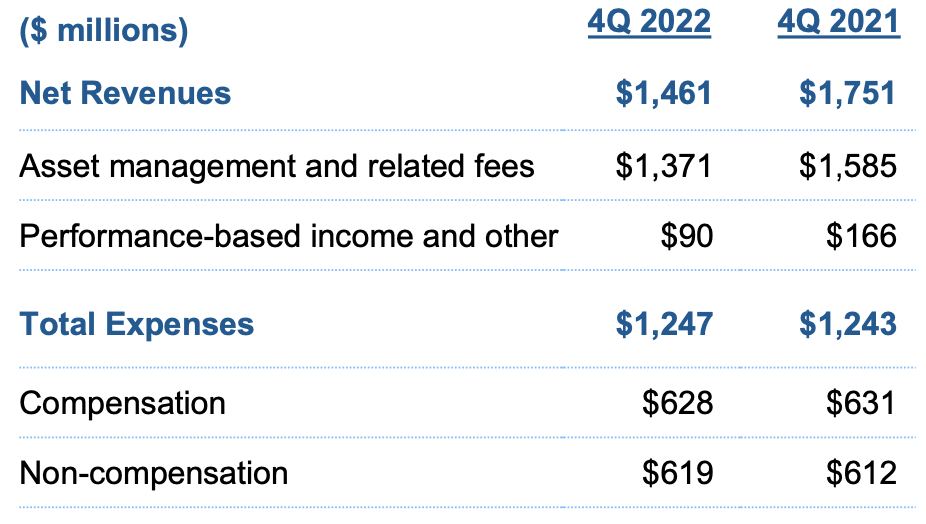

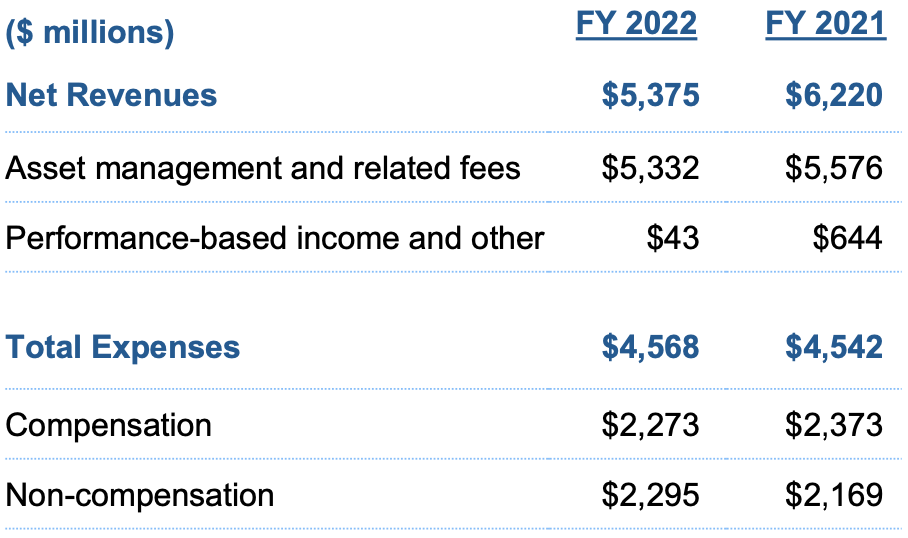

Investment Management

This unit showed poor performance in my view. Their results showed weakness in net revenues, AUM, and long-term net flows. Its net revenue decreased in both Q4 YOY and FY terms.

MS Q4/FY 2022 Earnings

Its pre-tax income was also crushed as it declined by over 50% for Q4 YoY and FY. AUM also shrunk from $1,565 billion in 2021 to $1,305 billion. Even more worrying would be long-term net flows showing negative flows. In Q4’22 there was a -$6.0 billion net flow and FY22 showed a -$25.8 billion net flow while in Q4’21 there was a -$1.1 billion net flow and a large positive $26.4 billion net flow for FY21. Digging deeper, their Asset Management and related fee revenues showed declines due to the weakness in equities and their performance-based income also showed declines.

MS Q4/FY 2022 Earnings

Overall, I believe even though market conditions were very tough, these results could be potentially concerning regarding the resilience of Investment Management amid headwinds. Investment Management revenues are showing too much correlation with institutional securities revenues in tough market conditions. From my analysis, further diversification will be required to build a more resilient Investment Management unit.

Earnings Were a Mixed Bag

As a whole, I believe earnings were a mixed bag. Traditional sources of income were crushed as interest rates rose. For me, equity trading and Investment Management revenues were disappointments. Amid volatility I would have expected somewhat better equity trading results and I would have also expected more resilience from Investment Management. Of course, the Wealth Management unit stole the show. It showed great resilience in a tough environment and it has succeeded in reducing the volatility in Morgan Stanley’s earnings. Looking forward to this year, I expect that this unit will continue to carry Morgan Stanley’s earnings as interest rates will likely continue to weigh on many of their other units. Their transformation into Wealth Management is paying off.

Strategic Update

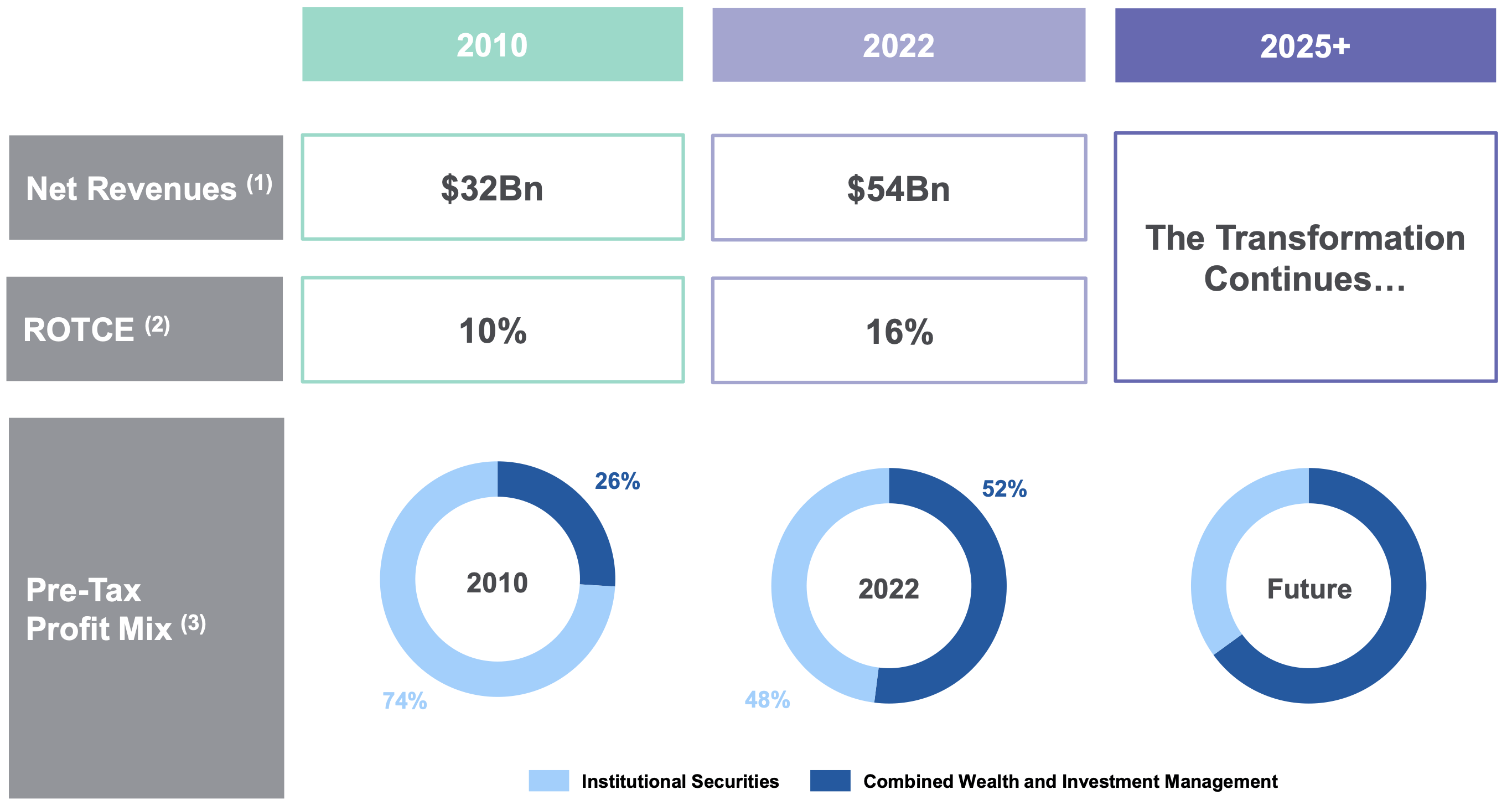

Along with its earnings release, Morgan Stanley presented an update for its strategy. In terms of their business mix, they showed their desire for a continued shift away from reliance on Institutional Securities to Wealth Management.

MS Strategic Update Presentation

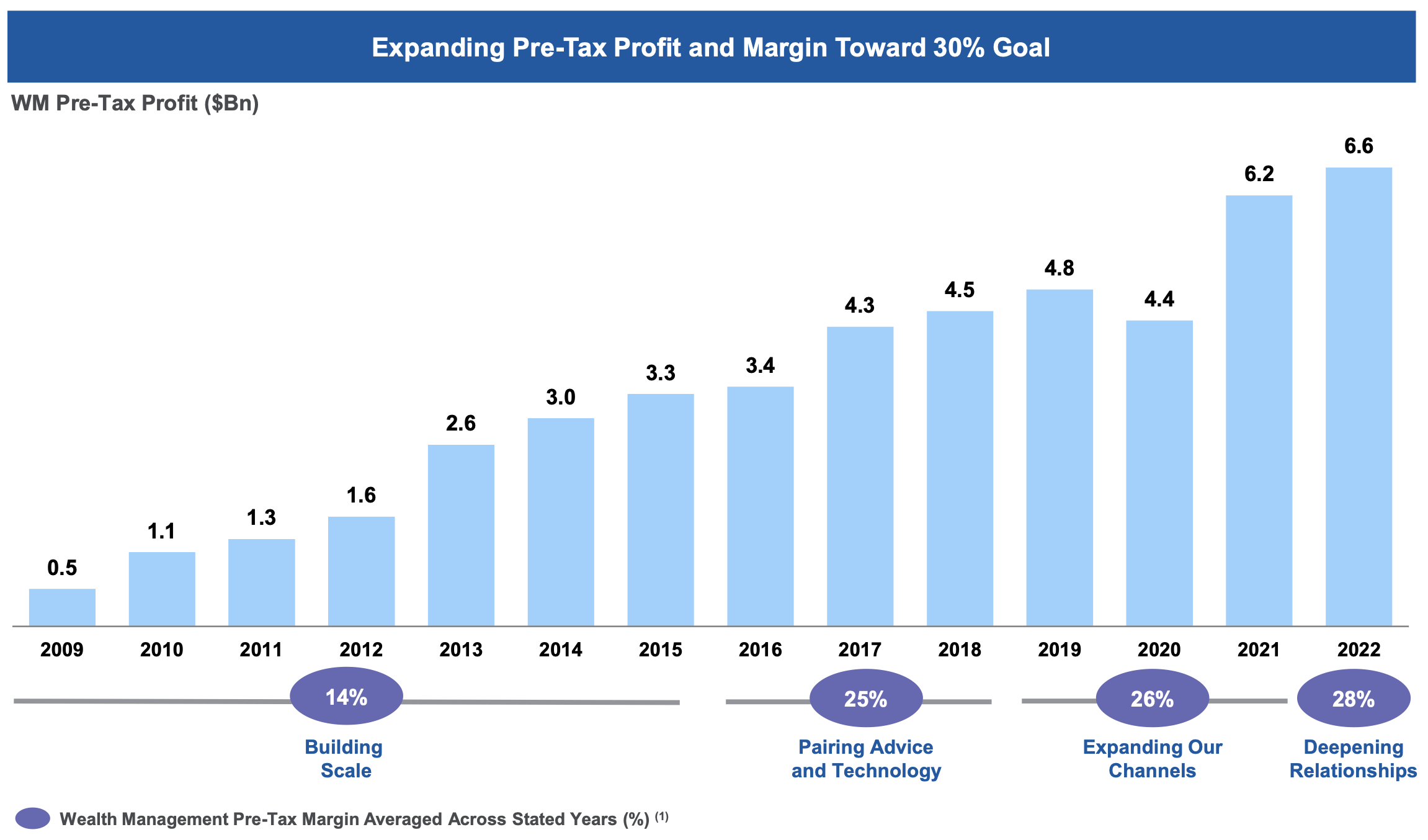

Morgan Stanley further highlighted their Wealth Management business by showing its stable revenues and surging margins. Pre-tax margins showed major increases in the last decade.

MS Strategic Update Presentation

Looking forward, Morgan Stanley is still setting ambitious goals to drive growth. They set a goal of adding $1 trillion in assets in Wealth Management every 3 years as well as eventually hitting $10 trillion in assets in Wealth and Investment Management combined. They are also aiming for an ROTCE above 20% while holding the expense efficiency ratio to less than 70%. Lastly, they aim to boost Wealth Management margins to above 30%. Overall, in my view Morgan Stanley’s strategy is on point. They are doubling down on efforts that have made the firm so successful over the past decade. Therefore, I believe Morgan Stanley will only become even more resilient as their transformation continues.

Layoffs

In December, Morgan Stanley cut 2% of their workforce. They had layoff approximately 1,600 of their 81,567 employees. Note that financial advisors were exempt from cuts. At first this might have seemed to be a weakening of Morgan Stanley’s confidence. Not long after, The Goldman Sachs Group, Inc. (GS) was reported to be laying off up to 3,200 employees, dwarfing Morgan Stanley’s layoff. The 3,200 employees would be 6.5% of Goldman’s 49,100 employees.

Morgan Stanley further showed its confidence when its CFO Sharon Yeshaya said “we’re comfortable with where we are” when asked about further job cuts. Amid layoffs in the financial industry, in my view Morgan Stanley has demonstrated that it has high confidence in its business as its layoffs were held to very modest figures compared to other firms.

Risks

The first risk would be the Fed. Recently, Fed Governor Waller expressed his support for a 25bps rate hike at the next Fed meeting but he also mentioned continued hawkishness. He said “we still have a considerable way to go toward our 2 percent inflation goal, and I expect to support continued tightening of monetary policy.” His overall stance was that rates may be kept higher for longer than market expectations as inflation may be more sticky than the market foresees.

From these remarks, in my view, rate cuts are not likely to occur later this year. With interest rates weighing on Morgan Stanley’s Institutional Securities and Investment Management units, if rates were to be kept higher for longer, Morgan Stanley will be kept on the defensive for longer. This is a short-term risk that might cause more pain for Morgan Stanley’s earnings.

The second risk would be James Gorman’s succession. In early January, it was reported that COO Jonathan Pruzan would be retiring on January 31st and that initiated talks of succession to CEO James Gorman. Days ago James Gorman directly addressed this by responding that “you plan a generation of people who can take over,” and that “ultimately the board will decide.” The contenders include Co-Presidents Ted Pick and Andy Saperstein, and Investment Management Chief Dan Simkowitz.

With succession, comes uncertainty. In my view, James Gorman has been one of the best CEOs on Wall Street in the past decade. His leadership at Morgan Stanley has transformed it into the wealth management giant it is today. I believe his retirement is a risk as a shift in strategy might occur as a result of a change in leadership. This could be potentially a longer-term risk as the direction of the firm is at stake.

Valuation

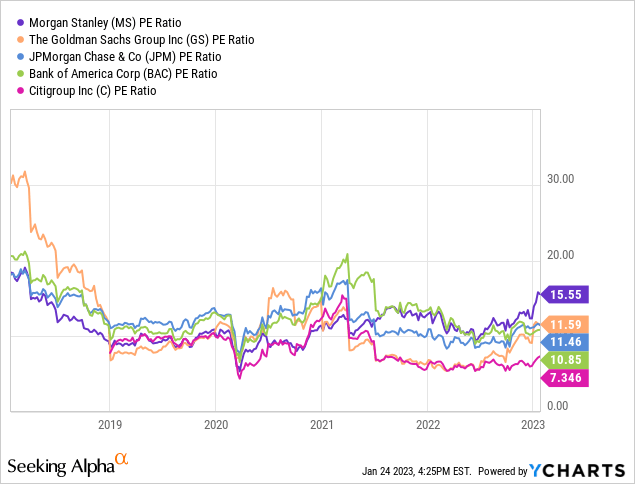

The P/E ratio of Morgan Stanley sits at around 15. It is at the highest level since 2018. As shown in the chart below, Morgan Stanley is significantly valued higher than its competitors Goldman Sachs, JPMorgan Chase & Co. (JPM), Bank of America Corp. (BAC), and Citigroup Inc. (C). It is valued nearly 50% higher than Goldman, JPMorgan, and Bank of America. In terms of P/E, I believe that Morgan Stanley is richly valued even after accounting for its Wealth Management stability. In my view, Morgan Stanley would be fairly valued at around an 11-12 P/E range with so many 2023 uncertainties and headwinds.

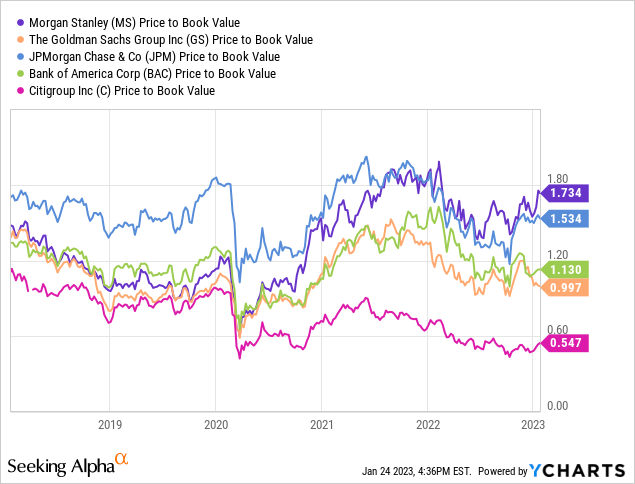

In terms of P/B ratio, it is a similar story. Morgan Stanley with a P/B of around 1.7 holds the highest P/B ratio among the big banks. Although down from the 2022 peak, the P/B ratio still remains quite high. It is significantly higher than pre-pandemic levels of around 1.2. With a potential 2023 recession coming, I believe it is hard to justify the current P/B ratio. Morgan Stanley is overvalued in terms of this measure. In my view, Morgan Stanley would fairly valued at a P/B ratio of around 1.3.

Conclusion

Morgan Stanley is a premium business trading at a premium valuation. Its recent earnings is a mixed bag but the highlight was its Wealth Management unit. It demonstrated its ability to withstand tough market conditions and showed that Morgan Stanley’s transition is paying off. Furthermore, in its Strategic Update, Morgan Stanley showed off its ambitious goals in its pursuit of growth in the next decade. Morgan Stanley will continue to be benefitting from stable revenues and high profit margins. Morgan Stanley’s headcount has also been relatively stable amid layoffs in financial services showing their confidence in their business.

However, the risk of continued higher rates and CEO James Gorman’s succession combined with a rich valuation will put pressure on their stock in the near term. In the long term, as Morgan Stanley becomes increasingly reliant on stable Wealth Management revenues, I expect its valuation metrics will continue to average higher as the firm becomes increasingly less risky. However, in the short term amid headwinds and uncertainty, in my view Morgan Stanley is overvalued. Therefore, I initiate coverage of Morgan Stanley with a hold rating. However, any major pullback to fair values would present a good opportunity for long-term investors to buy a premium business at a fair price.

Be the first to comment