Vertigo3d

At Investor Day 2022, MoneyLion (NYSE:ML) executives highlighted the big plans of the small fintech. The company continued forward with an intent to create a financial Super App with a robust business focused on investment content along with products to help consumers. My investment thesis remains ultra Bullish on the stock with the irrational dip below $1 making MoneyLion a top pick for 2023.

Booming Medium-Term Targets

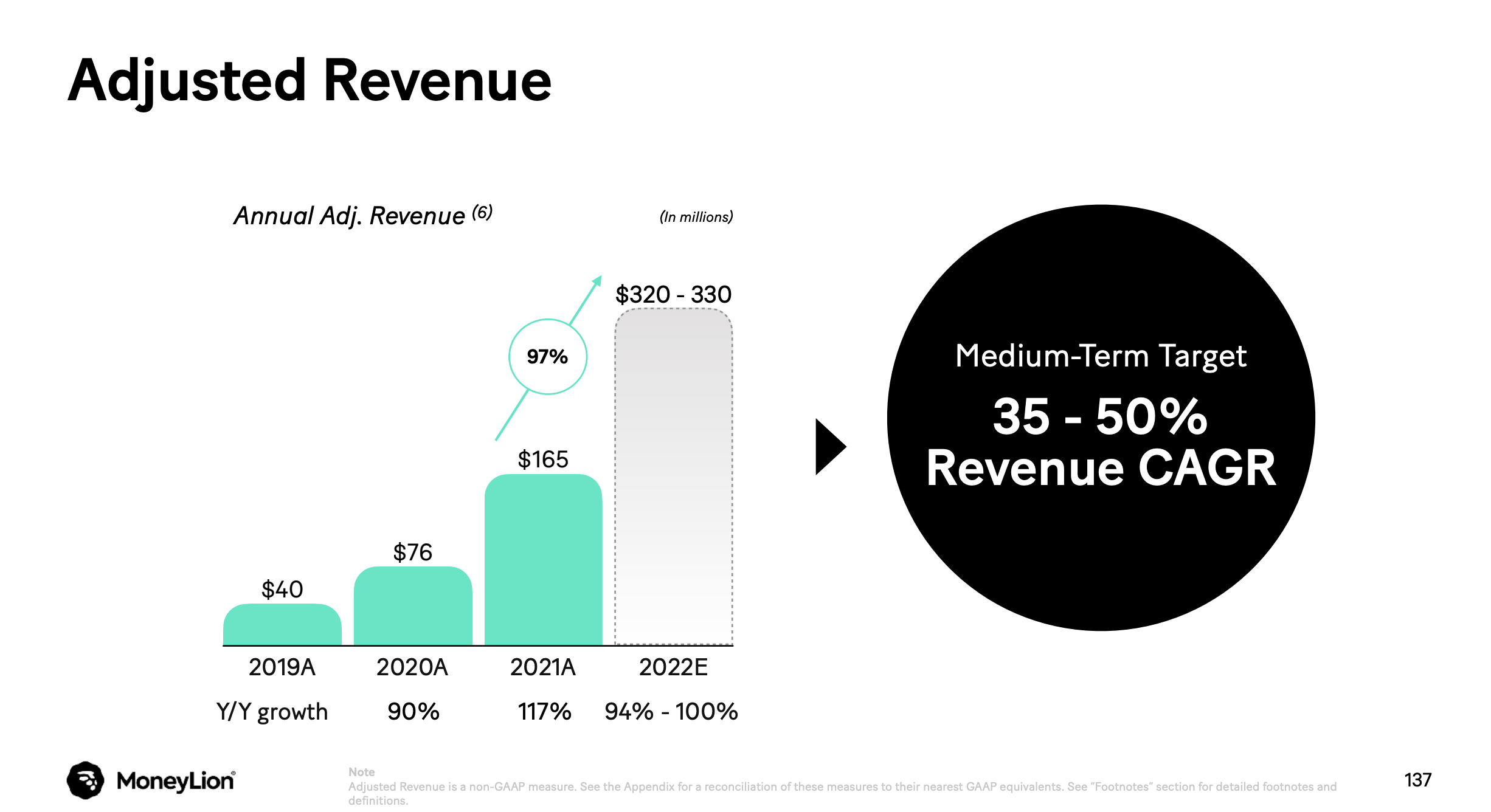

MoneyLion trading below $1 remains bizarre with the company growing revenues in the 100% range since the company came public via the SPAC deal back in 2021. The fintech did cut 2022 financial targets following a dip in enterprise revenue expectations as other fintechs pull back on marketing spend.

The market should’ve been relieved that MoneyLion maintained strong financial targets through the next couple of years. The fintech is now targeting revenue growth between 35% to 50% through the medium-term, which the CFO defined as the next 2 to 3 years at the Investor Day.

Source: MoneyLion Investor Day ’22 presentation

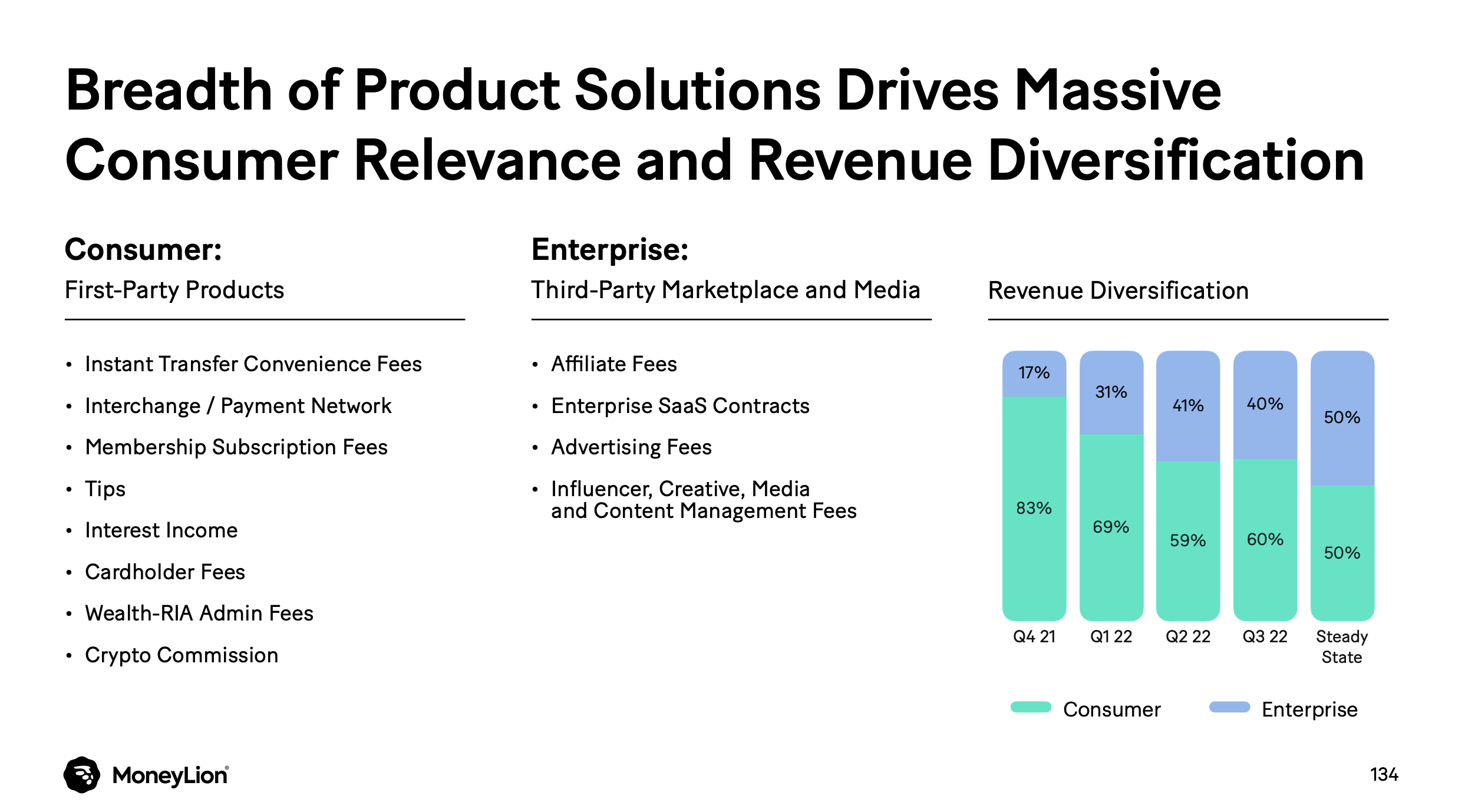

The company has a unique business model for fintechs with a focus on enterprise revenues from working with other fintech partners. MoneyLion provides investment content for users along with connecting those members to financial partners offering financial solutions, such as house or car loans.

In the future, the fintech plans to benefit as much from affiliate and advertising fees as instant transfer fee and interest income. MoneyLion plans for a 50/50 revenue diversification from consumer and enterprise revenues of their 5.4 million members at the end of Q3’22.

Source: Investor Day 2022 presentation

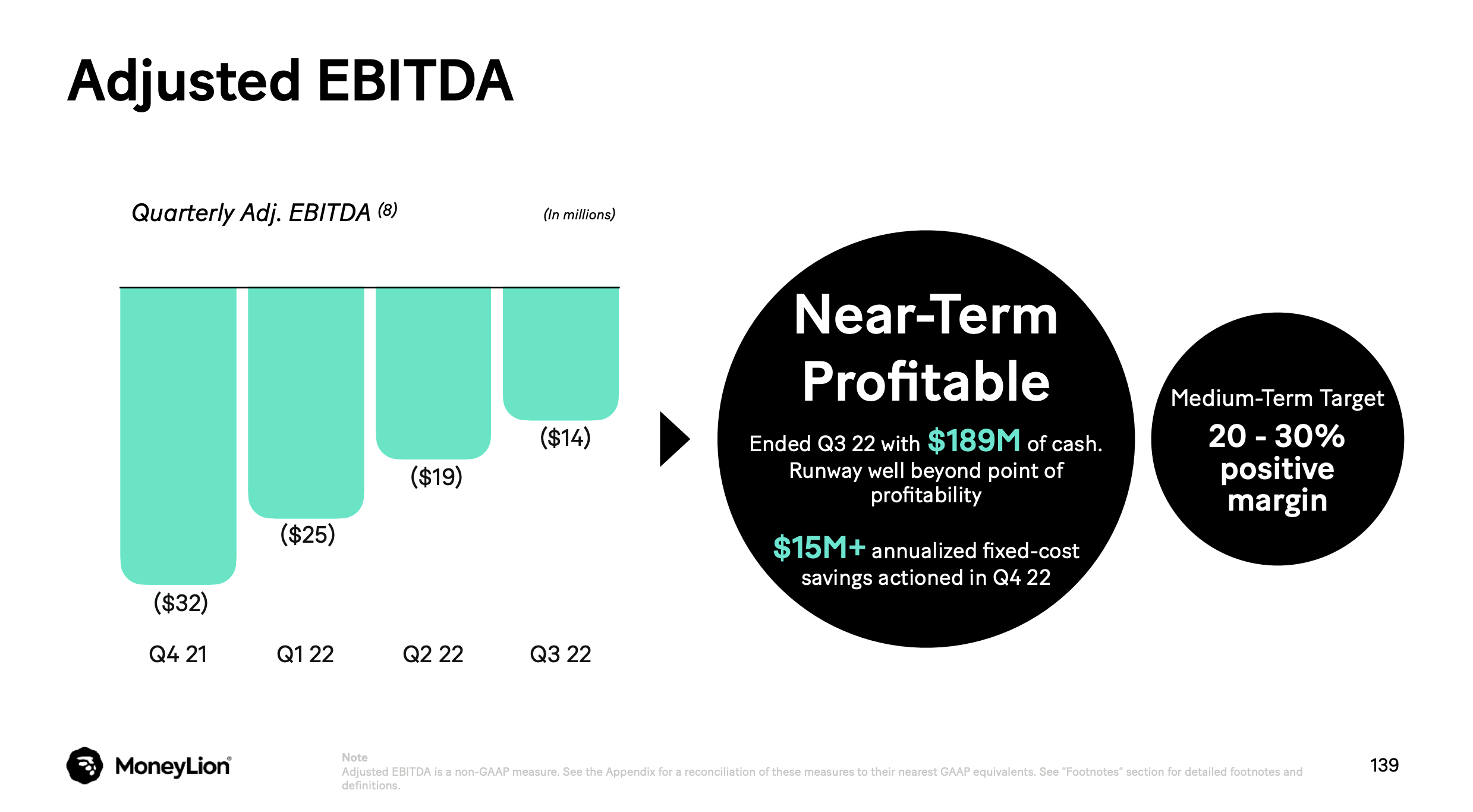

MoneyLion cut the Q4 and 2022 financial targets due to a decrease in enterprise partner spending with a looming recession. The fintech still forecasts a robust revenue target for the year at $325 million.

The market doesn’t like EBITDA losing companies in this current weak economic environment, but MoneyLion should’ve ended the year not too far from EBITDA profits. The company lost $14 million in Q3’22 and between cost initiatives and revenue growth, the amount should approach breakeven very quickly with the goal of reaching 20% adjusted EBITDA margins in the medium term.

Source: MoneyLion Investor Day ’22 presentation

Very important to note that MoneyLion isn’t targeting 20%+ adjusted EBITDA margins in the long term, the company is forecasting the positive margin in the next few years. The fintech could be talking about adjusted EBITDA topping $100 million by 2025.

MoneyLion has these key financial targets from the Investor Day for the medium-term targets:

- 35-50% revenue CAGR

- 55-65% adj. gross profit margin

- 20-30% positive adj. EBITDA margin

The company suggests the medium term means 2 to 3 years leading to the below financial targets for 2025:

- Revenue: $325M @ 42.5% growth = $940M

- Adj. EBITDA: $940M @ 25% margin = $235M

- 20x Adj. EBITDA multiple = $4.7B market cap

The stock only has a current market cap of ~$225 million providing substantial upside potential, if MoneyLion only hits the targets. Of course, the fintech hasn’t hit targets having just cut expectations for Q4.

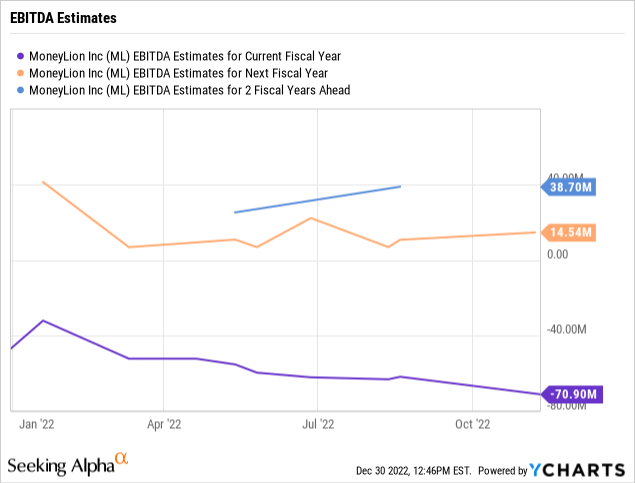

Analysts already forecast MoneyLion hitting nearly $15 million in positive EBITDA next year. The fintech reported an EBITDA loss of $14 million in the last quarter, so the team has a lot of work to close the gap.

The company stripped out $15 million in fixed costs starting in Q4 amounting to ~$3.5 million per quarter. Clearly, the next quarterly report must show material progressing in shifting from large EBITDA losses to at least breakeven for the stock to work here.

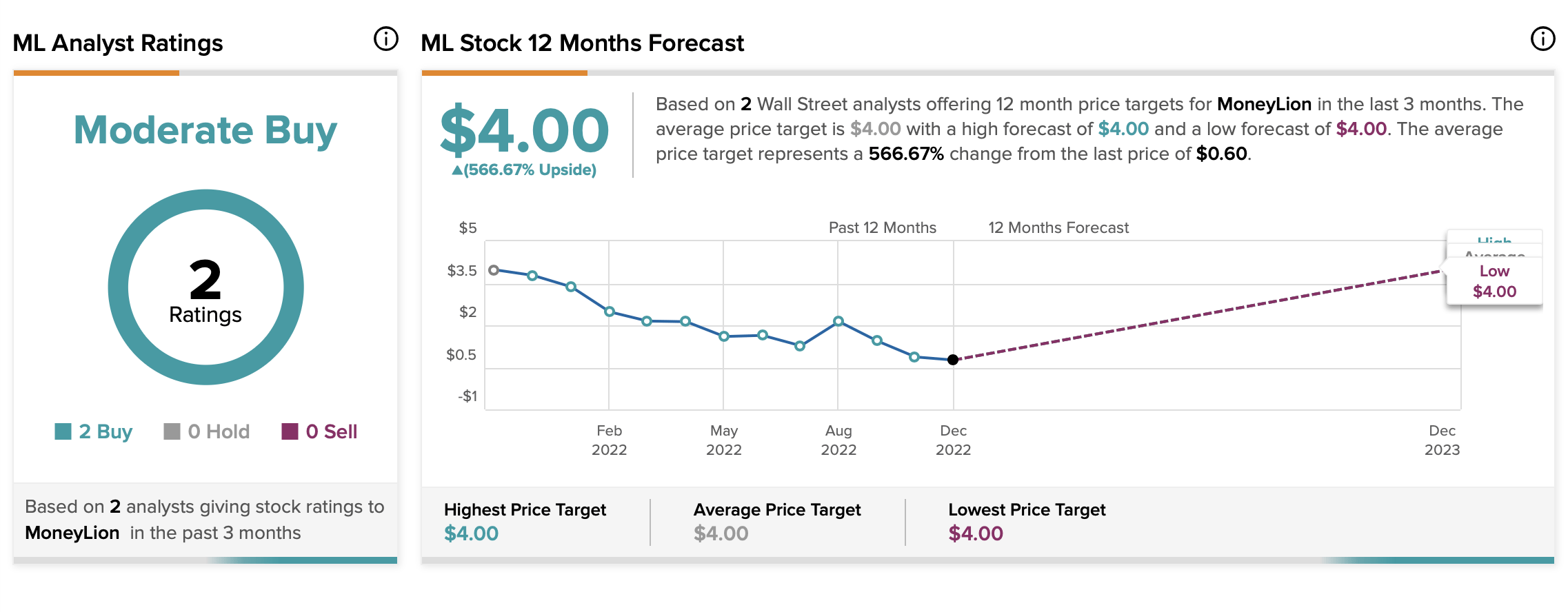

Limited Analyst Coverage

The biggest issue with MoneyLion appears related to the company coming public via a SPAC. The stock has no support from analysts despite an average price target of $4.

Source: TipRanks

At Investor Day 2022, the analysts didn’t ask any questions or provide any updated financial information. The stock should have far more analyst coverage with a revenue base of $320 million heading to nearly $500 million in 2023.

The lack of analyst coverage after going public as a SPAC hits investor confidence. MoneyLion only has a market cap of $225 million after the recent rally here suggesting the stock is only trading below $2 or $3 due to the lack of investor confidence primarily because the company has limited analyst coverage.

Cheap Penny Stock

MoneyLion trades below $1 despite last reporting a quarter where revenues grew 100% to reach $89 million. The company isn’t a traditional penny stock (trading below $5) with no growth prospects.

The fintech has a cash balance of $189 million, but MoneyLion has $173 million in convertible debt. The net cash balance is ~$16 million, but the company has the cash to fund the business with the quick path to adjusted EBITDA in 2023.

The stock shouldn’t trade far below 1x forward sales targets. Though, MoneyLion definitely has risks, or the stock wouldn’t trade below $1.

The fintech was recently sued by the CFPB over excessive charges to members. In addition, the stock trades below $1 possibly requiring a dreaded reverse split by MoneyLion. The recent 1-for-12 split by Paysafe (PSFE) should provide some investor confidence a dire outcome isn’t the necessary result of such a move.

The tough economic environment causing the original Q4’22 revenue cut hasn’t improved. Investors shouldn’t expect in bounce back in enterprise revenues in the current market.

Takeaway

The key investor takeaway is that MoneyLion is a top pick for 2023 with the stock valuation far below the actual prospects for the fintech Super App business. The stock faces some negative headlines this year, but the risks are vastly over played here. As always, investors shouldn’t invest capital into a stock trading in the penny stock area without understanding loss of capital is a real possibility.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment