jetcityimage

Mondelez International (NASDAQ:MDLZ) has performed exceedingly well in the face of numerous global challenges. The company has defied lower volume trends across consumer staples and has grown volumes and prices. The company also offers a good dividend yield for income seekers. But the stock is overvalued based on valuation metrics and a discounted cash flow model. Investors should wait for a pullback.

Stellar revenue growth

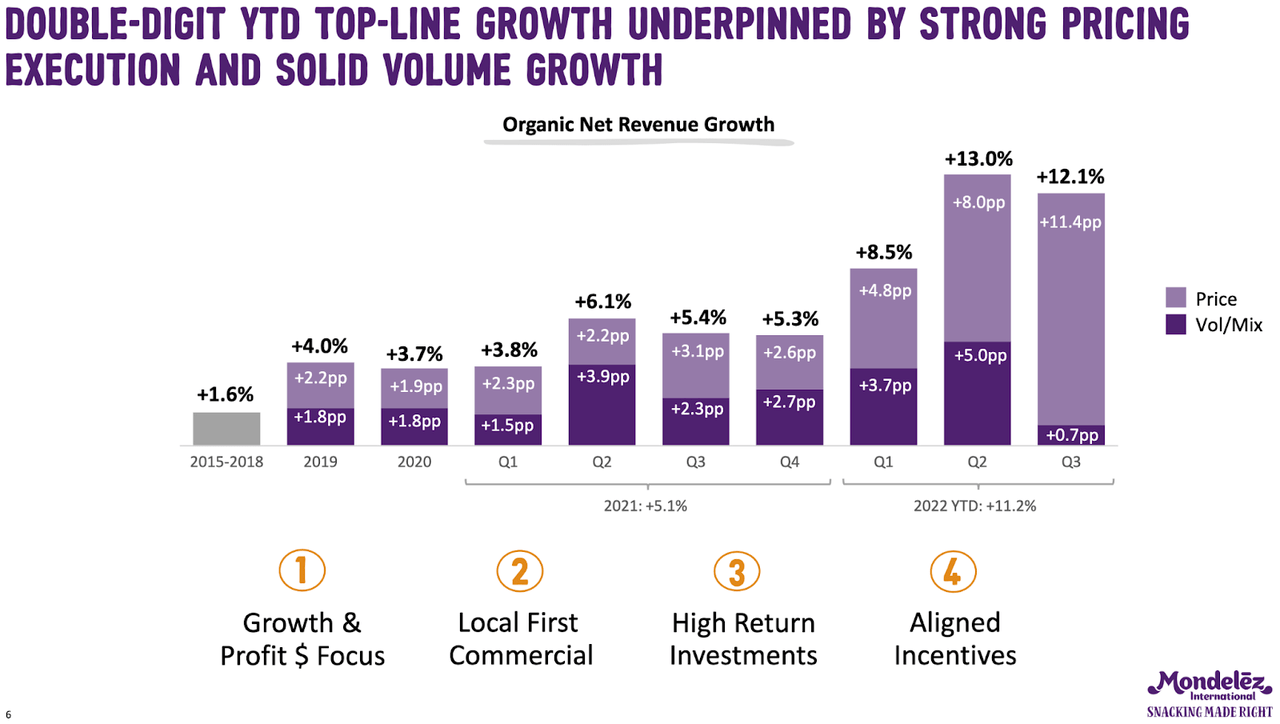

Mondelez continues to deliver stellar revenue growth globally in the face of high inflation. Revenue increased by 12% in Q3 2022, with every region showing positive growth. Volumes surprised on the upside on top of price increases (Exhibit 1).

Exhibit 1:

Mondelez Q3 2022 Revenue Growth from Volume and Price (Mondelez Investor Presentation)

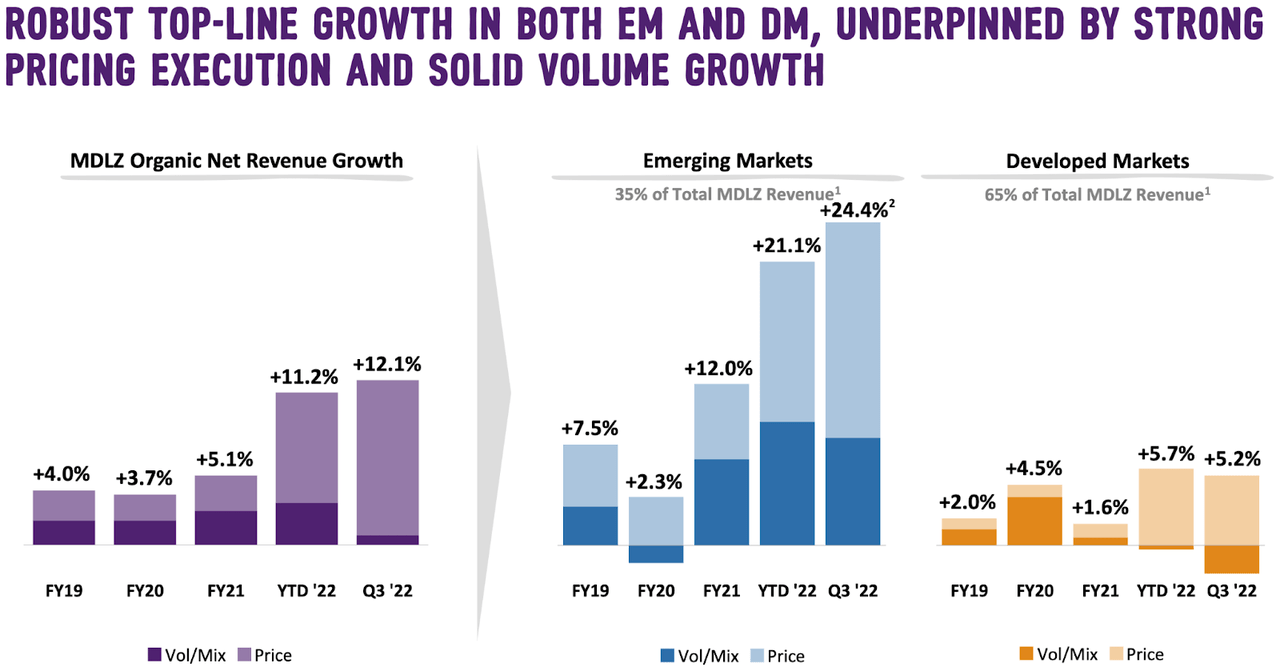

Across the consumer staples sector, volumes have declined by low-to-mid single digits compared to double-digit price increases. But, Mondelez may be a rare company where volumes have increased in the face of price increases. The company pointed out that the developed markets of Europe and the U.S. are struggling with inflation, but emerging markets are more used to high inflation rates and have weathered the price increases well (Exhibit 2).

Although overall price increases in Q3 2022 were 12%, developed markets saw price increases of 5.1%, while emerging markets saw increases of 24.4% (Exhibit 2). Even as total volumes saw a positive gain, the developed markets saw a decline in the volume of 3% due to disruptions in Europe. Since Mondelez’s products, geared toward snacks and comfort foods, may have offered some protection against volume declines. Q3 2022 saw the lowest volume increase the company has faced in a while.

Exhibit 2:

Mondelez Q3 2022 Developed vs. Emerging Market Comparison (Mondelez International Investor Presentation)

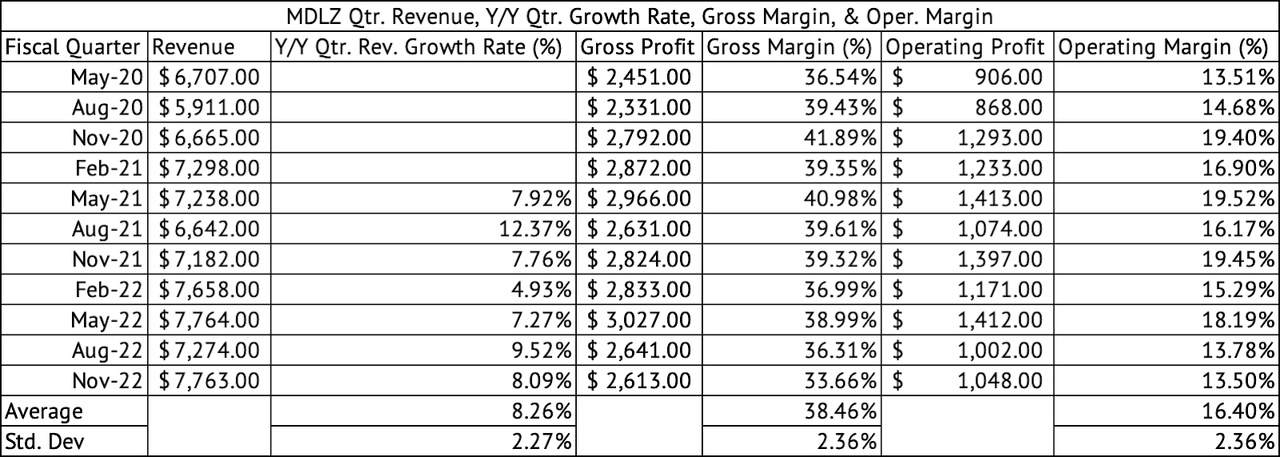

The company has not been immune to gross margin erosion due to derivatives costs, step-up costs of inventory, and acquisition-related costs. The company’s GAAP gross margins have dropped to 33.6% in November 2022 compared to its average of 38.4% since May 2020 quarter (Exhibit 3). Its operating margins have declined to 13.5% compared to its quarterly average of 16.4%.

Exhibit 3:

Mondelez International Quarterly Revenue, Y/Y Growth Rate, Gross, and Operating Margins (Seeking Alpha, Author Compilation)

Given the enormous price increases, it may be challenging to push through further increases, especially if inflation remains sticky. Consumers may bucket Mondelez’s snacks and comfort foods in their discretionary spending budget and reduce consumption. Mondelez has avoided volume declines, but the company is not immune to them.

Manageable inventory levels

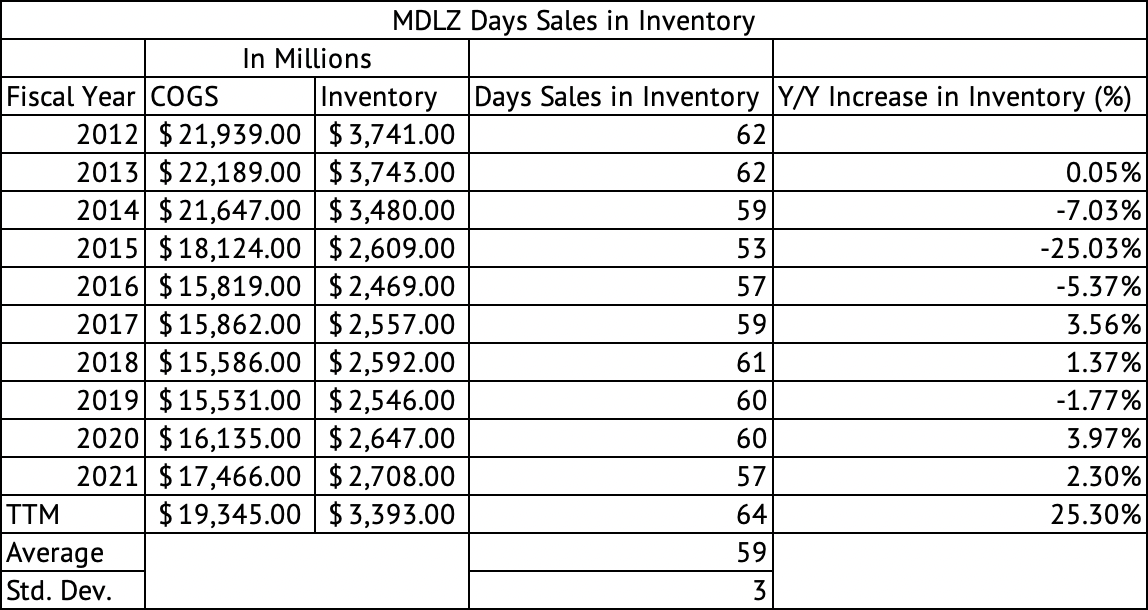

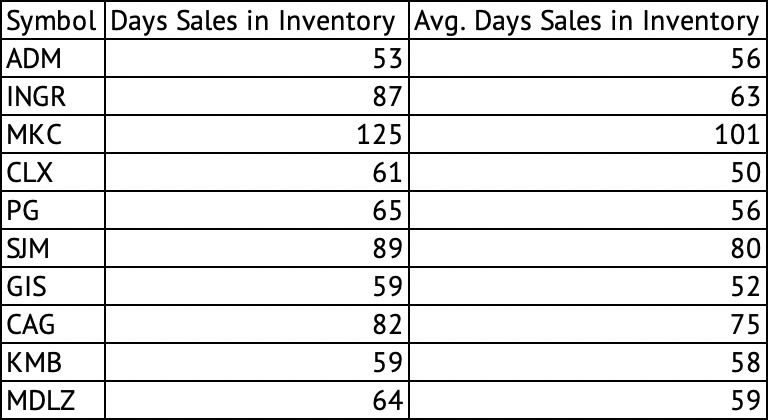

Mondelez experienced inelastic demand for its products which may be the reason behind its manageable inventory levels. The company has proven deft in managing its inventory costs in the face of high inflation and price increases. For the trailing twelve months, the company recorded a carrying cost of inventory of $3.3 billion, which amounted to 64 days’ worth of sales, compared to its average of 59 over the past decade (Exhibit 4). Since the standard deviation is 3, the 64 days of stock is slightly above one standard deviation from the mean, indicating it may be a bit on the excess side.

Exhibit 4:

Mondelez International Days’ Sales in Inventory (Seeking Alpha, Author Calculations)

As long as the company does not see a steep fall in volumes, these inventory levels should not further impact margins. But, if volumes decline, the company’s margins may be under further pressure. Many other companies in the consumer staples sector have seen a substantial increase in inventory due to a combination of cost increases and a decline in volumes (Exhibit 5).

Exhibit 5:

Days’ Sales in Inventory for Consumer Staples Companies – ADM, INGR, MKC, CLX, PG, SJM, GIS, CAG, KMB, MDLZ (Seeking Alpha, Author Calculations)

Dividend yield, debt, and share repurchases

The company offers a 2.3% dividend yield, which is low compared to the 2-year U.S. Treasury Yield of 4.2%. The company has consecutively increased its dividend over the past nine years and has paid a dividend for 21 years. The company’s GAAP dividend payout ratio is a tad high at 65% compared to its five-year average of 45%.

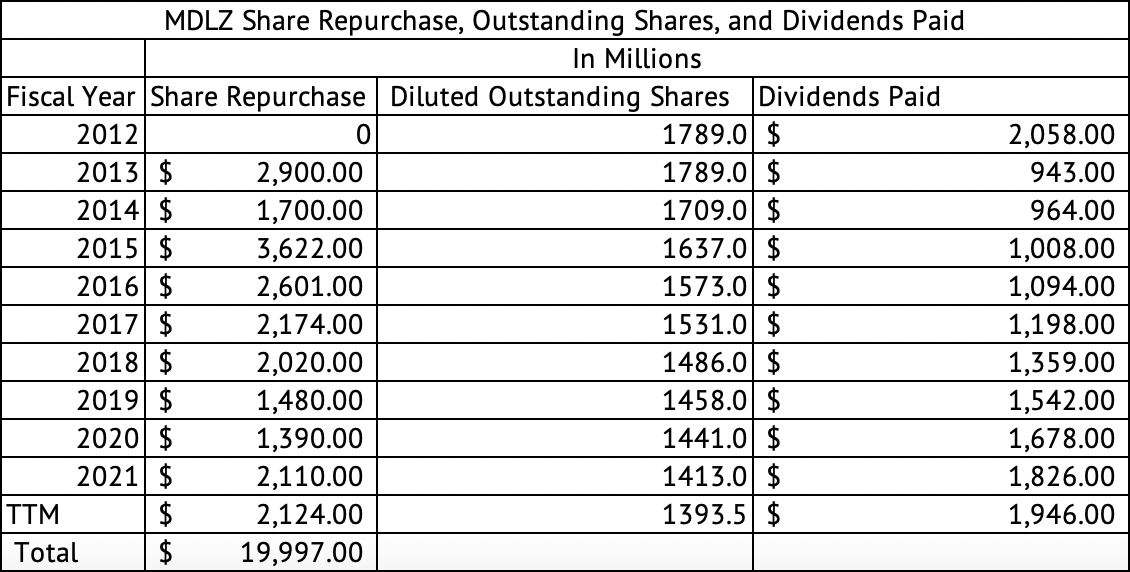

The company has spent nearly $20 billion in share repurchases over the past decade (Exhibit 6), which has reduced the share count from 1.78 billion to 1.39 billion, a reduction of 395.5 million shares. The average price paid for the share repurchase works out to $50.5. The shares are currently trading at $63.88. The company’s dividend costs may have been reduced marginally due to the buybacks, with the company paying $1.9 billion in dividends [TTM] compared to $2.05 billion in 2012. I have long argued that buybacks benefit management more than shareholders.

Exhibit 6:

Mondelez International Share Repurchase, Diluted Outstanding Shares, and Dividends Paid (Seeking Alpha)

Buybacks can help show good growth in earnings per share, but the valuation metrics derived from EPS, such as the P.E. ratio, may not be perfect tools to compare valuations across an industry. The long-term free cash flow generation by the company ultimately decides the valuation and growth of P.E. via arguably artificial ways such as share buybacks that do not accurately reflect the cash generation powers of a business.

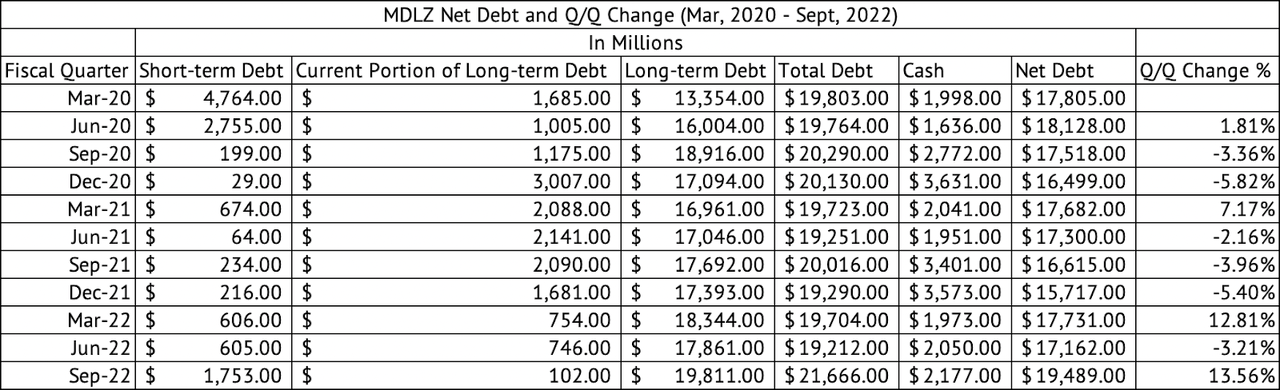

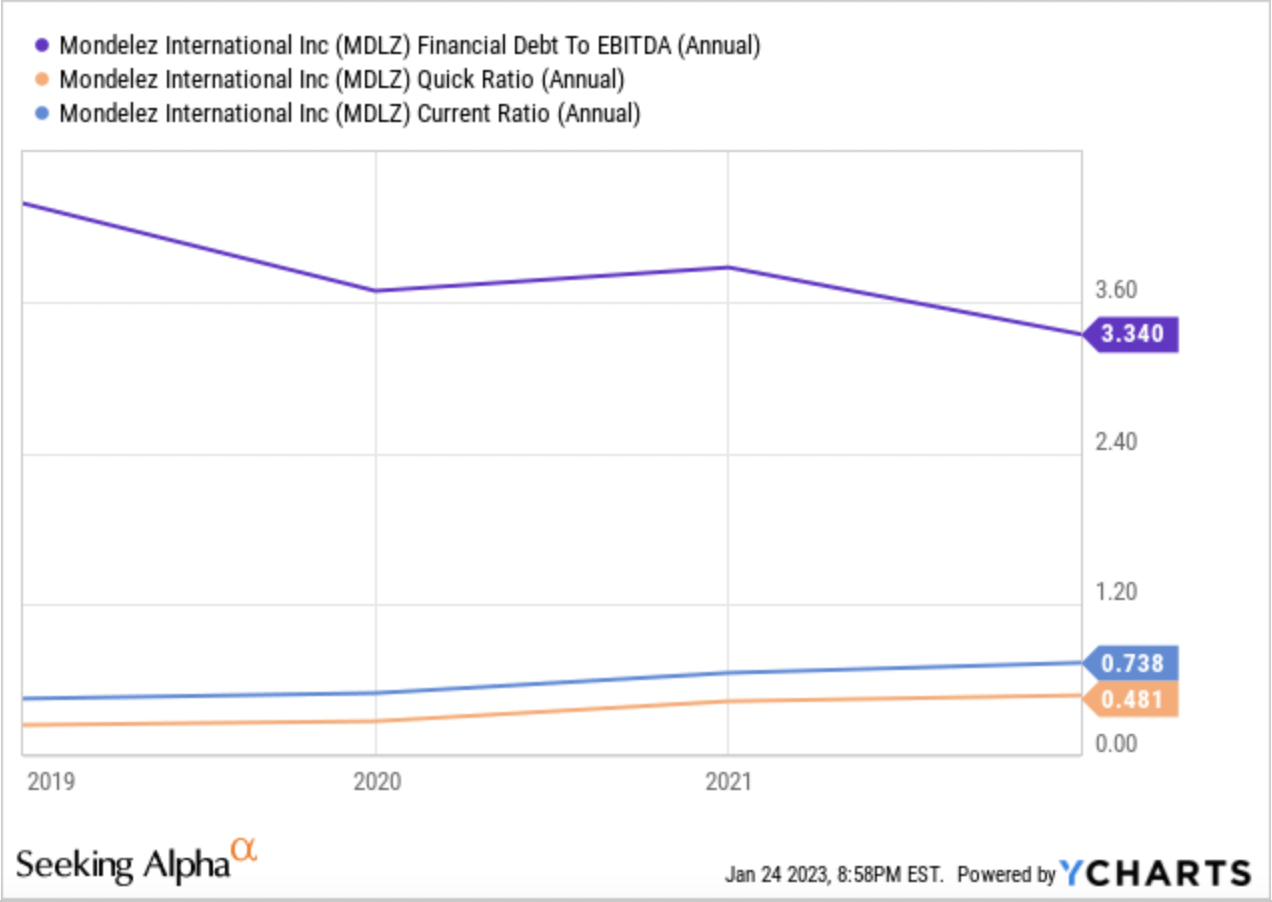

The company has a high debt level with a debt-to-EBITDA ratio of 3.3x and has poor short-term liquidity as measured by current and quick ratios (Exhibit 8). The company had $17.5 billion in long-term debt at the end of 2021. The company’s net debt [long-term + short-term – cash] stood at $19.4 billion at the end of the September 2022 quarter (Exhibit 7). The company has about $1.5 billion in long-term debt and finance lease payments coming due in 2025. Since most of the debt is due decades from now, the company may have the flexibility to pay down the debt over time.

Exhibit 7:

Mondelez Net Debt and Q/Q Change (Mar 2020 – Sept 2022) (Seeking Alpha, Author Compilation)

Exhibit 8:

Mondelez International Debt-to-EBITDA Ratio, Current, and Quick Ratios (Seeking Alpha)

Valuation

Mondelez has performed exceedingly well under challenging circumstances over the past year. Its performance is laudable, given that other companies in the sector are facing some volume declines in the face of double-digit price increases. But, the company is overvalued at this time. The company is trading at a massive premium with a forward GAAP PE of 26x, compared to its five-year average of 21.9x, and a trailing GAAP PE of 28x, compared to its five-year average of 22x. The low volatility of consumer staples stocks helps protect a portfolio from a bear market. The sector’s predictable dividends provide a good yield for income seekers. So, it may be a good idea to own the sector and companies like Mondelez for the long term. But, an investor looking to add to their existing holding or a new investor to Mondelez may be better off waiting for a pullback in the stock.

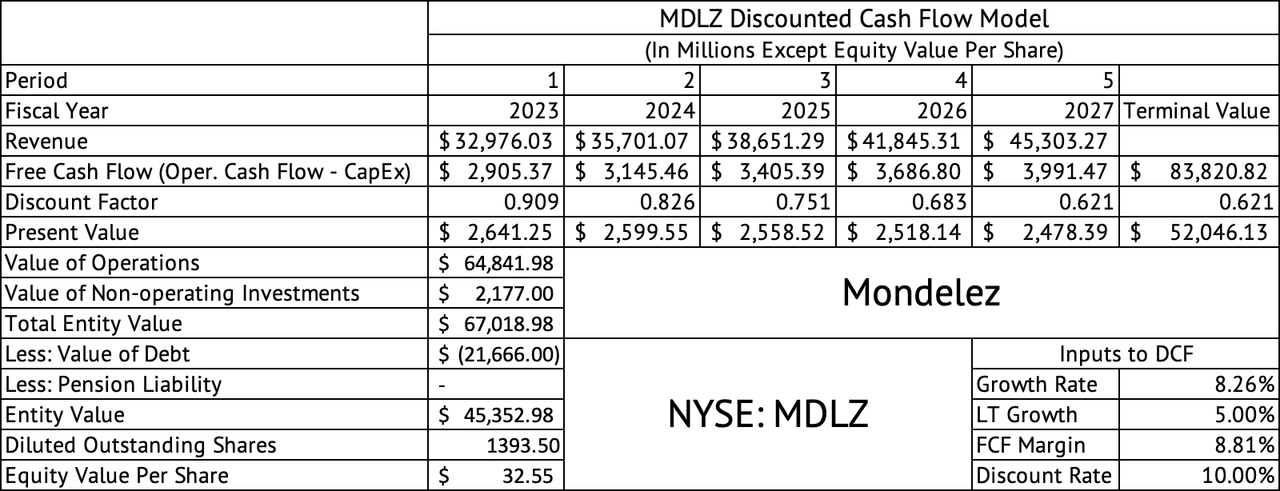

A discounted cash flow model estimates that the stock is overvalued at current prices (Exhibit 9). The high debt load takes a big chunk of the entity’s value, thus reducing the value available to equity owners. This model assumes a weighted average cost of capital of 10%, a reasonable assumption given the rise in interest rates, an optimistic growth rate of 8.2% until 2027 (the company’s average revenue growth rate since May 2020), and a long-term growth rate of 5%. Mondelez looks overvalued, trading at $65, with these optimistic growth assumptions. The free cash flow margin of 8.8% is the company’s average over the past decade.

Exhibit 9:

Mondelez International Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

Price return and momentum

The stock has dropped 3% over the past year, while the Vanguard S&P 500 Index ETF (VOO) has fallen 7.9%. Mondelez has performed well over the past three months returning 12%, but the momentum is fading, with RSI and MFI technical indicators showing weakness. Analysts have made upward revisions to the company’s earnings for the fourth quarter ending in December. The company is set to release its earnings report on January 31. Investors should watch for any weakness in volume growth and listen to any commentary on weakness in its North American and Asian markets. Surprisingly, Europe may fare well in the coming months due to the vanishing threat of energy shortages.

Mondelez has bucked the trend of declining volumes in the face of double-digit price increases. The upcoming earnings release may shed light on the strength of the consumer and set the stage for the outlook for revenue and profitability growth for 2023. Investors may be better off waiting for a lower valuation before buying Mondelez.

Be the first to comment