demaerre

Molina Healthcare, Inc. (NYSE:MOH) achieved a 12% gain in its stock price while the S&P 500 (SPY) declined 12% since August 30, 2021. The company’s outperformance was a result of Molina’s reasonable valuation and above-average growth. Molina is set up similarly to how it was last year. The valuation is still reasonable, and the expected earnings growth of 28% for 2022 and 13% for 2023 is likely to drive the stock to continue its outperformance. The stock’s positive potential is in the midst of a possible recession within the next year.

As of March 31, 2022, Molina served 5.1 million members eligible for Medicaid, Medicare, and other healthcare programs. Molina operates in 19 states.

Recession-Proof Business

Molina is benefitting as a business because of its lack of economic sensitivity. Molina provides managed health care services to low-income individuals and families.

The company derived 80% of revenue from Medicaid, 12% from Medicare, and 8% from the healthcare marketplace in Q1 2022. Molina’s outlook looks good going forward as the U.S. managed care market (which includes Medicaid, Medicare, and private health insurance) is expected to grow by 5.6% annually to 2026. This growth is expected to bring the total market size up to $5.8 trillion in 2026.

Changing demographics are helping to drive this growth trend. The amount of people aged 65 or older in the U.S. is expected to almost double from 52 million to 95 million by 2060. This growth is expected to bring this age group from 16% of the population to 23%. This growing age group can help increase the amount of Medicaid and Medicare enrollees.

The bottom line regarding Molina’s business is that it is likely to experience growth while many parts of the economy are likely to decline due to rising interest rates leading to a possible recession. Medicaid enrollments actually increased during the financial crisis in 2008 and during the COVID recession in 2020. This makes sense, as the loss of jobs led to lower income for many households.

Acquisitions Boost Growth

Molina’s recent acquisitions provides add-on growth for the company. Molina completed its acquisition of Affinity Health Plan in October 2021. The company paid $380 million for Affinity Health, which gives Molina 284,000 Medicaid members for annual revenue of about $1.2 billion.

Molina completed its acquisition of Cigna’s (CI) Medicaid contracts in Texas in January 2022. Molina paid $60 million for about 50,000 Medicaid beneficiaries, providing approximately $1 billion in annual revenue.

In October 2021, Molina announced that it wishes to acquire the Medicaid Managed Long-term Care business from AgeWell New York for about $110 million. The deal would provide Molina with 13,000 members and about $700 million in annual revenue. This acquisition is expected to close in Q3 2022.

The company recently announced in July 2022 that it will acquire My Choice Wisconsin for about $150 million. This deal would give Molina 44,000 Medicaid and managed long-term services members. My Choice Wisconsin would also give Molina another $1 billion in annual premium revenue. The deal is expected to close later this year and will be immediately accretive to EPS.

Overall, Molina has a nice recent track record of M&A activity. These acquisitions provide new revenue in addition to the organic growth from its existing regions. This puts the company in a good position to weather any storms from high inflation, rising interest rates, and a potential recession.

Valuation

Molina is trading with a reasonable valuation with a PEG ratio of 1.3. I like to use the PEG ratio for growth companies since it takes the 3 – 5 year projected earnings growth into account. Molina is expected to grow earnings at an annual pace of about 14% over the next 3 to 5 years. This is above-average growth as the S&P 500 is expected to grow earnings at about 11.6% over the same time period. Molina trades below the Healthcare Plan Industry, which is trading with a PEG of 1.8.

Molina’s expected 3 – 5 year annual EPS growth is slightly higher than its industry’s expected growth of 12.5% over the same period. Molina has a good combination of valuation and growth to hold up well over the next year. During the same time, many companies that are more economically sensitive are more likely to struggle if higher interest rates lead to a recession.

Technical Perspective

stockcharts.com

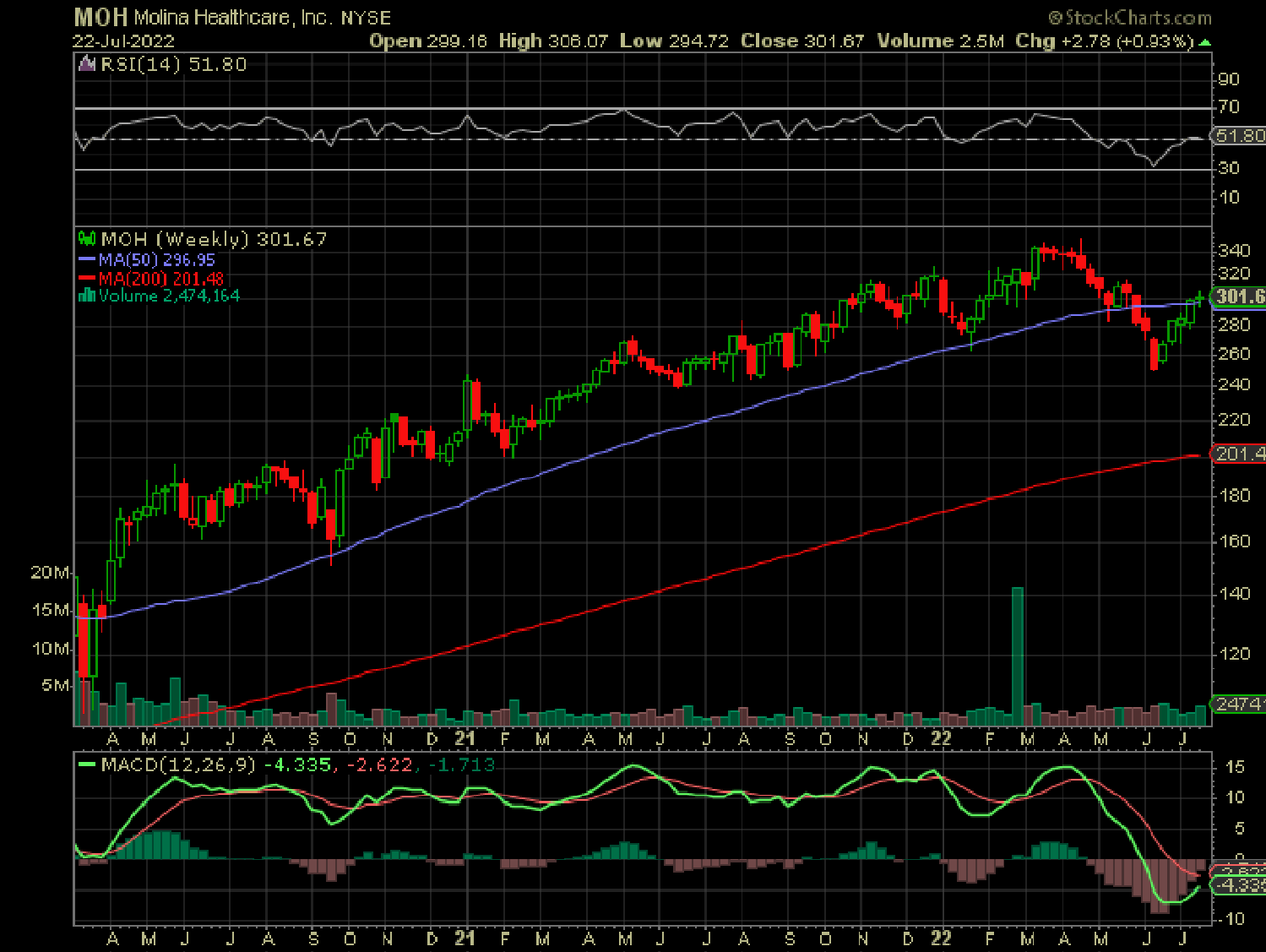

I zoomed out to the weekly chart where each candle stick represents an entire week to get a long-term perspective. With the exception of a few of dips, the stock price has been holding above the 50-day moving average. The RSI is showing strength as it increased from an oversold level to above 50. The green MACD line looks like it is about to rise above the red signal line, which would suggest a positive change in momentum.

I see this as a chance for investors to get in after the recent price pullback. The price might reach $340 as we head into the end of 2022 if everything goes well for the company. The next earnings report on 7/27/2022 could be a positive catalyst if earnings expectations are met or exceeded and the company gives positive future guidance.

Molina Healthcare’s Long-Term Outlook

Overall, Molina is in a good position to outperform the broader market over the next year and beyond. The company has a good combination of reasonable valuation and strong potential growth.

The company may not be totally immune from a strong bear market associated with an economic decline and recession. The stock could fall along with many others in such a scenario. However, the nature of Molina’s business as not as economically sensitive should allow the stock to hold up better than average. This is what has been happening over the past year as Molina’s stock increased while the broader market declined.

Watch for Molina to continue its M&A activity for add-on growth. The company is also likely to benefit from the long-term expected growth for Medicaid/Medicare enrollments. These factors can help drive strong above-average growth over the next 3 to 5 years for the company.

Analysts have a one-year price target of $340 for the stock which looks reasonable since the stock was trading there earlier this year before the recent pullback. Keep in mind there could be a lot of volatility in the stock due to the economic uncertainties in the current market.

Be the first to comment