MiX Telematics (disclosure: long) is a founder-led business at somewhat of an inflection point.

The company has spent the past few years investing margins into growing the customer base while increasing their global presence and building their brand, and are now poised to experience operating leverage as they continue to scale their SaaS products and service offerings.

Despite having a diverse customer base and a large market share in fleet management services, the growth runway remains incredibly long with a huge TAM and overall under-penetration for telematics services industry wide. The company has a long history of profitability, accretive buybacks and returns of capital to shareholders, and can be purchased today for prices that materially undervalue the future prospects of the business and represent extreme discounts on an absolute and comparable M&A transaction basis.

Thanks to the recent market-wide selloff as well as a portion of the business being tied to the oil and gas industry, shares have dropped some 30% in the past few weeks while the business continues to execute and grow their customer base.

Source: Author Data

At a current share price of $8.37 (US ADS), MIXT can be purchased at around 4.0x TTM EBITDA, and less than 8.0x UFCF. Additional positive catalysts include U.S. listings and SEC filings. The above uses 2019 numbers, while TTM figures are even better. MIXT reports Q4 and FY2020 results sometime in late April.

Business Overview

MIXT is a global technology company that provides driver safety, vehicle tracking and fleet management services to consumers and fleet operators. The company helps individuals and businesses manage their mobile assets through SaaS products and services, with an emphasis on efficiency, safety, compliance and security.

MiX was founded in 1996 in South Africa by CEO Stefan Joselowitz as Matrix Vehicle Tracking Proprietary Limited, and over the next two decades made six key acquisitions in the areas of fleet management, safe driving technology, software development and drive training technology. One of the most important acquisitions was that of a competitor, OmniBridge, in 2007. MiX inherited a team with more than 20 years in the logistics sector as well as its current COO Charles Tasker (at the time Managing Director of OmniBridge). Shares were listed on the JSE in 2007 followed by a US IPO in 2013, and ADSs are now listed on the NYSE. Mix currently operates in North America, Europe, the Middle East, Australia, Asia and they have a position in Brazil growing at a spectacular rate.

Today, MIXT helps their customers reduce costs, improve safety, lessen their environmental impact and manage large amounts of historical and real-time data. MiX solutions help solve a variety of challenges faced by fleet operators, including high operating costs, insufficient data management, poor visibility into operations and compliance challenges. The company’s customer base falls into three primary categories; Premium Fleet, Light Fleet and Asset tracking. In all three verticals, MiX aims to save their customer’s money and make their lives easier. Legacy fleet management solutions are made up of spreadsheet and paper-based systems which are labor intensive, prone to error and can’t provide reliable, timely data. In order to fully benefit from cost savings and efficiency improvements, full functionality products need to be purchased. MiX’s ability to address customer needs is part of the reason why retention is so high (try it, you buy it). As of today, MIXT has a wide base of customers, over 800,000 vehicle subscribers, and a presence in 120 countries across the world.

A brief real life example helps illustrate the power of telematics solutions as a whole:

A truckload carrier used its telematics program as the basis of a comprehensive effort to optimize total cost of ownership across its geographically dispersed fleet comprising thousands of tractors and trailers. The company built a financial model that combined data on maintenance costs, fuel consumption, depreciation and other per-mile costs for its entire tractor fleet. Within four weeks the new model, which unlocked previously inaccessible asset-level cost data, revealed that maintenance costs for older vehicles in the fleet were much higher than the company had expected. That insight drove a change in policy, with vehicles retired earlier to cut the average age of the fleet in half. The reduction in operating and maintenance costs that resulted from this change more than compensated for the increased capital expenditure required to achieve it.

I’d encourage investors to check out their website and YouTube channel for overviews and summaries of all relevant products.

A look at historical numbers reveals that MIXT has done a phenomenal job of balancing growth and profitability over the past decade, with zero unprofitable years since 2010.

Source: Seeking Alpha

MiX derives the majority of revenues (88%) from recurring subscription revenues charged to customers for collecting, processing and delivering information. Customers subscribe to the service monthly on a per-vehicle-installed basis. The remaining revenue percentages consist of hardware sales, vehicle recovery services, and driver training and consulting.

The company has an incredibly diverse customer base of 6,300 fleet operators (representing 73% of 2019 subscription revenue) and target sales toward customer’s with large fleets (50 or more vehicles). The large fleet customer base accounts for nearly 90% of fleet subscriptions as of 2019 with a customer retention rate of 92% (the company unfortunately doesn’t report churn). The retention rate for fleets with greater than 500 vehicles is 100%, which speaks to the stickiness of the products and value proposition delivered to customers. MiX’s global presence and wide product offering allows them to service customers such as BP, Chevron, Nestle, PepsiCo, The Linde Group among others.

Unfortunately, this isn’t a great business, as telematics product and service offerings can basically be categorized as commodities (vehicle measurement device hooked up to software), and MIXT has lower EBITDA margins than competitors due to low barriers to entry and little pricing/negotiating power. Having said that, a fair business run the right way with a focus on capital allocation, cash flow conversion and growth can lead to decent returns, and in this case, size and scale matter, management matters, and customer relationships matter. MIXT’s long track record and outstanding reputation in addition to their focus on large fleet customers has differentiated them among competitors.

A few of MiX’s competitive advantages / entrenched positioning include:

- Large customer base with a long track record of success – referenceable clients and success stories matter in Telematics when everyone questions the ROI

- Diverse customer base – not subject to customer concentration, global supply chain whereas most competitors operate on a regional basis

- Enterprise fleet customers – stickier customer base, less price sensitive and less prone to switching solutions frequently compared to SMB customers (basic functionality)

- The ability to quickly enter a new market (and become profitable)

Over the past decade, MiX has grown their revenues and subscriber base organically at a mid-high single digit rates while making complementary acquisitions to improve product and service offerings.

Moving forward, the company’s strategy will be to lower hardware sales as a percentage of overall revenues, increase margins as the company scales, and transition customers from unbundled service packages to bundled service packages. Hardware revenue has been trending downward over the past three years and now sits at 12.2% of revenues versus 14.4% in 2017. In addition, in 2016, management began talking about making investments in other regions of the world outside of Africa in order to scale. The CFO at the time commented that the business would expect other regions of the world to offer the same growth and adjusted EBITDA margins (40%) as they’ve experienced in Africa.

A quick look at operating margins over the past three years indicate a favorable trend:

2017: 9.0%

2018: 12.6%

2019: 17.2%

2020E: 18%+

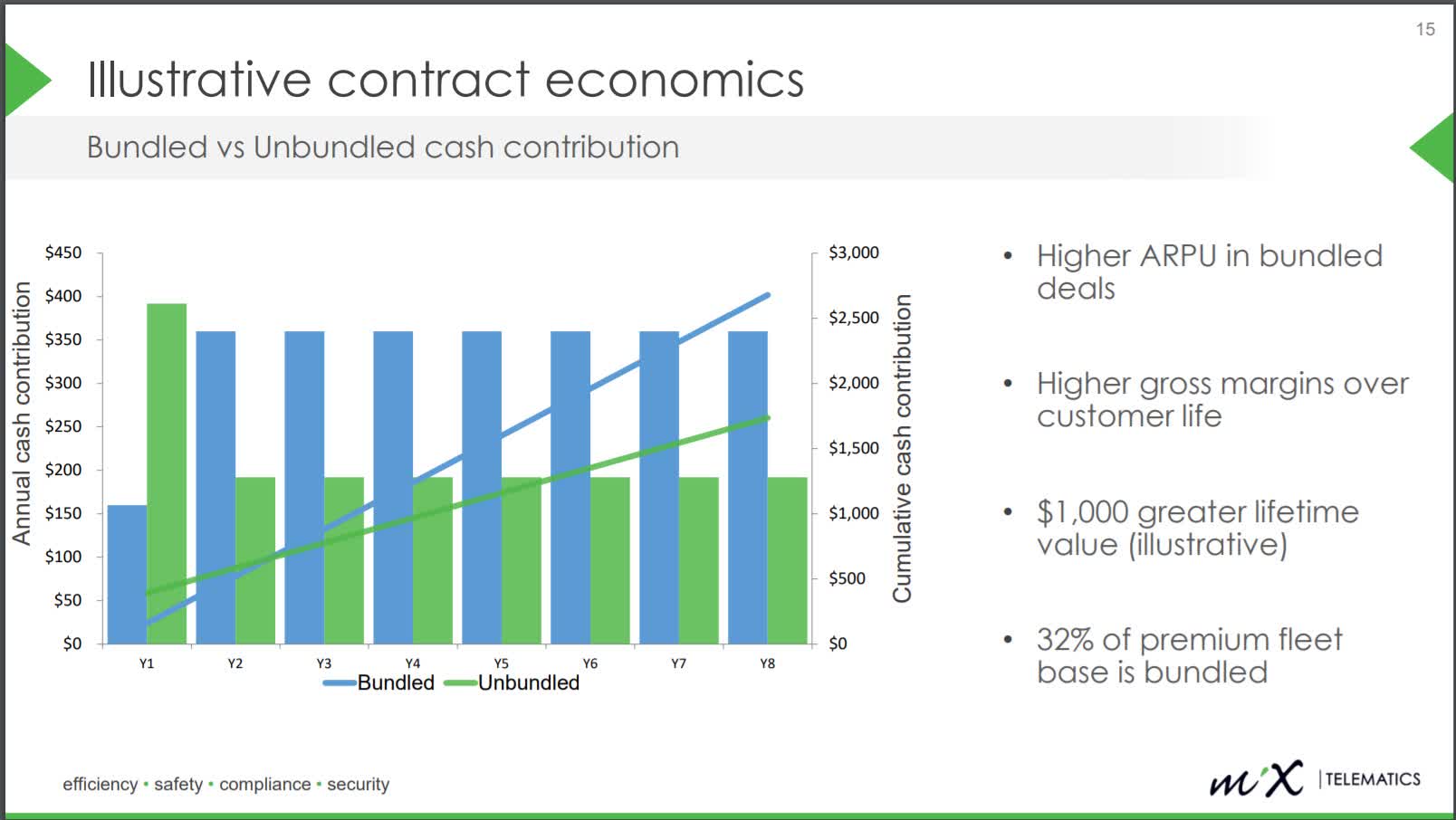

Despite the above, MIXT is potentially at an inflection point as a business, having spent the past decade making significant investments in R&D, sales and marketing in order to increase subscriber growth and increase the number of bundled solutions sold to customers. Where the opportunity gets interesting is that this focus on selling bundled solutions has a short term muting effect on revenues and operating earnings due to the upfront hardware revenue forfeited using this sales approach. However, the company believes the shift to bundled contracts will lead to increased long-term value as contracts go through the renewal cycle.

A look at the unit economics of the company’s subscription products reveal some insight into how future value is created. MIXT business strategy is to take a hit in the initial years of signing up a new fleet/customer, to generate higher LTV on the backend of customer subscriptions. The company offers two product choices, bundled and unbundled. Unbundled customers pay lower amounts upfront, while bundled customers pay less upfront and receive hardware for free, while paying more in the latter years of the contract. Currently, 80% of new contracts are bundled, requiring higher capex and lower initial free cash flow in the short term, with higher gross margins, higher FCF and higher LTV in the long term.

So here you have a management team that saw an opportunity to bundle their service offerings at a greater value to both the customer and the business, but knew that in the short term the efforts would cause short term hits to both revenues and earnings, and decided to engage in the strategy anyway. Management has long spoken about thinking long-term and not focusing on quarter to quarter results (something I always love to hear) and the business strategy and capital allocation back up their words.

Q3 2016 call: The demand has exceeded our expectations. We are happy to absorb the near-term P&L effects and we believe funding the upfront cost is an excellent uses of cash as the returns are very attractive.

As mentioned above, 80% of new contracts are now bundled contracts. Why is this important? Basically, MIXT is gaining additional subscribers to their service who are paying higher rates, in exchange for an upfront cost at the beginning of the contracts. Given the high retention rate, when contracts expire (maturity 3-4 years) and begin to renew, MIXT doesn’t have to spend any more on additional hardware or CAC, but instead get to keep the high margin cash flows. In this model, the customer is happy to not have to pay the hardware expense upfront, and places less weighting on renewal subscription prices.

Source: Company Investor Presentation

So earn less money in year one, but drive higher returns by collecting more subscription revenues in later years at lower costs. It’s been working really well.

Industry Info

I would say that MiX Telematics was early to the fleet management industry, and especially as it relates to selling software products. Even if there was a need to digitize vehicle tracking and fleet management in 1996-2007, the capabilities to do it well didn’t exist. The advancement and reliability of wireless networks, satellite technology and data storage have now supported the rise of cloud computing which makes the delivery of these SaaS technologies possible (and beneficial). These improvements in technology and secular demand have helped spur the adoption of MiX products and services, yet penetration rates remain low.

According to a report by ABI Research, there were more than 206 million commercial vehicles registered globally by the end of December 2018. Global fleet management penetration was estimated to be approximately 19%. ABI forecasts that by 2023, the number of registered commercial vehicles will be approximately 260 million.

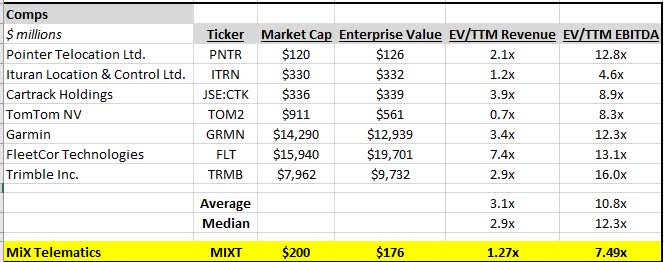

While Verizon and Geotab are some of the leaders in the telematics space (by subscriber numbers), it’s tough to find direct comps (large, diverse telematics businesses with focuses on large fleets). However a brief depiction of MIXT competitors below helps illustrate the valuation discount.

Competitors

Source: Author Data

Management

Stefan Joselowitz is the founder/CEO who has been with the company since 1996 and has strategically navigated the business through multiple cycles. He is a cut above most microcap CEOs, and has a unique combination of operational expertise and capital allocation skills. Joselowitz owns 3.2% of the company, with total insider ownership at 23%.

Of note, 15% of the business is owned by Ian Jacobs, an independent board member. Jacobs graduated from Columbia Business School in 2003 and worked as a special projects research analyst for Warren Buffett for six years. In 2009, Jacobs left Berkshire Hathaway Inc. to form 402 Capital LLC, a concentrated value focused manager that invests in businesses with structural competitive advantage. Jeff Gramm through Bandera Partners also owns a small chunk.

Management pay seems very reasonable, with the CEO taking home a little over $500k in salary with reasonable performance bonuses, with performance targets for options and stock comp bonuses based on important metrics such as subscription revenue growth, operating profit and cash generated by operations. Option awards are tied to total shareholder return targets (minimum 10%) and revenue/EBITDA growth targets.

There is currently around a $20mm share repurchase program in place from 2017, through which MiX has repurchased over $6mm in shares over the past two years. At times, management has shown a willingness to use their balance sheet to fund accretive share repurchases and my guess is that they will be initiating more buybacks soon given the stock’s recent decline. This can be seen especially during cyclical downturns and share price volatility such as in 2016 when MIXT repurchased 25% of shares outstanding in Q4.

Before diving into valuation, I want to comment on MiX’s exposure to the oil and gas industry. MiX derived 26% of their revenues from oil and gas customers in 2019 (historically has been in the low to mid-20% range). Declines in the price of oil will no doubt have an adverse effect on some of MiX’s customers and impact revenues for MiX. This was the case in 2015-2016 as some of these businesses reduced their fleet sizes during rough periods in the industry. While MiX will always have some exposure to oil and gas, it’s worth noting that the last time the price of oil took a plunge this large was in 2015, and MiX lost zero customers. Zero. In addition, MIXT solutions are designed to help customer’s reduce costs and increase efficiency, so customers may even choose to invest in these solutions even during tough times. MIXT still generated $23mm in combined operating income in 2015-16 on the back of a 12% decline in revenues. In addition, the balance sheet with 13% of the market cap in net cash provides comfort and flexibility.

From the Q2 2016 conference call:

Despite this energy crisis, every single key customer in this sector who has come up for renewal with us has re-signed for terms between three and five years and some with even higher options (phonetic).

Yes, I could probably add this because I remember the time when we first signed these guys and when the sector was flying so to speak with a very profitable oil price from their perspective there was definitively much more appetite to do upfront deals and even I recall we did a few cash up front deals because of the cash flushness and etc, but in the current cycle it’s really been the reverse experience where they are very happy to conserve cash from their side and engage with a bundle deal on a monthly payment scheme.

Q3 2016 w/ only 9,000 subscriber additions:

…I will answer your second question first. It was below our expectations. Churn is probably in the current situation that we are in probably not the right descriptive width, but the net effect of the same. We are seeing contraction in some of our large premium fleet customers, where we are seeing the fleet sizes coming down. We are not losing the customer. Customer is happy with us as I highlighted and I will repeat again. We renewed every single energy sector customer. We were in a time when you would have thought we were most vulnerable in the midst of this oil crisis, where undoubtedly they all have directed from the boardroom to cut cost to the bone wherever possible. They opted not to terminate our services, but in fact to renew them for extended periods of time.

Q4 2016:

The advantage of that focus on huge fleets don’t insulate us somewhat from losing customers to bankruptcy, so we don’t deal with a lot of the small players in that space and a lot of those small players have gone, potentially they have gone out of business. So we’re not exposed to that which is a good thing, most of our customers are blue chip – a definition of the word and we have certainly survived the cycle and we will be around for many decades to come.

Valuation

MiX is cheap on both an absolute and M&A comp basis. Of note, the below numbers don’t include any potential future sources of value including consumer verticals in safety and security, or asset tracking solutions (MiX Tabs) for businesses to keep track of non-vehicle assets (generators, HVAC systems, lighting, storage tanks etc).

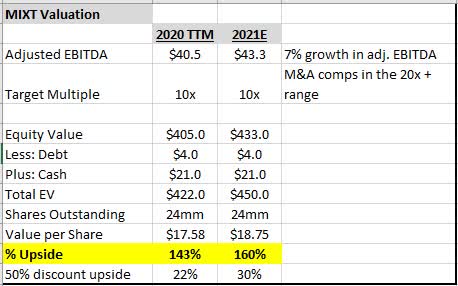

Back of the napkin valuations for YE 2020 and 2021 assuming 7% growth in adjusted EBITDA (expectations are low double-digit to mid-teens growth) and using a 10x EBITDA multiple (M&A comps have been in the 20x+ range) results in significant upside from today’s share price of $8.37.

Source: Author Data

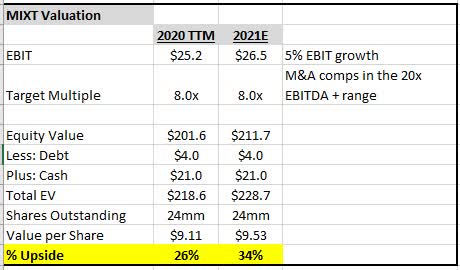

An even more conservative valuation measure using EBIT over the next year or so, in what I deem to be an overly draconian scenario where the company only grows operating income by 5%, and using an 8x multiple of EBIT still results in greater than 25% upside from today’s share price, providing what appears to be a decent margin of safety at today’s levels.

Source: Author Data

Of note, these valuations do not include recent impacts on Q4 and Q1 2021 from a large drop in oil prices, nor do they factor in potential significant buybacks over the next year or two.

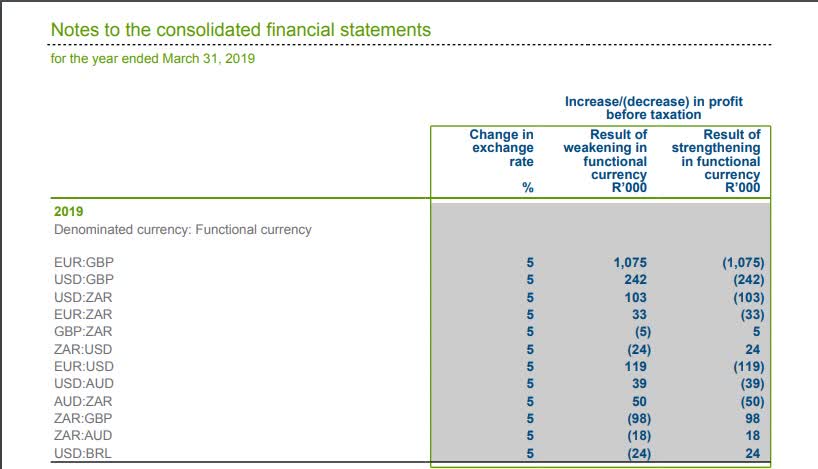

**A note on currency risk impacting valuation:

MIXT has a reporting currency of the South African Rand (ZAR). The ZAR has depreciated over 20% against the USD in the last month alone. While there are ADSs available to US investors (quoted in USD share price), the company’s financials will without a doubt be impacted by the foreign currency translation as it relates to top and bottom line growth. For example, my projections can be interpreted on a constant currency basis – 5% EBIT growth from 2020-2021 using an exchange rate of $14.0 ZAR/USD – but if the local currency declines 20% or more, or less, results will be impacted further on a realized exchange rate basis (5% growth in EBIT and -20% in currency depreciation would equal -15% realized growth).

In their Annual Report, MIXT outlines briefly the impact a 5% move in exchange rates would have on operating profit, with a 5% move in either direction contributing to a gain or loss of $24,000 ZAR. A 5% move in exchange rates in the other direction would result in a gain or loss of $103,000 ZAR. A 20% move would multiple that number by 4x, resulting in a gain or loss of $412,000 ZAR or $22,000 USD.

Source: MIXT Annual Report

While all foreign currencies introduce currency risk, especially during uncertain times like these, I would view the recent large depreciation of the ZAR against the USD to be temporary. The current exchange rate of $18-19 ZAR/USD is a greater than 10-year low for the currency, measured against the historical average of $15 ZAR/USD (MIXT uses an exchange rate of $14.0 ZAR/USD. Factors impacting the currency the most include COVID-19, low commodity prices, exposure to China and overall economic shutdowns.

So while results may be impacted more in the short term due to currency exchange rates and the depreciation of the ZAR, long-term MIXT should continue to drive it’s business forward in a meaningful way.

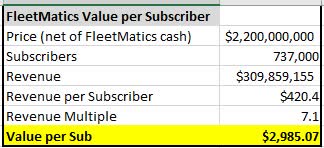

Switching over to comps and M&A deals, Verizon acquired FleetMatics in 2016 for $2.4 billion, representing a 7.1x REVENUE multiple. At the time of the acquisition, FleetMatics had 737,000 subscribers. MIXT currently has 812,000. Prior to the acquisition, FleetMatics was trading at a 5.2x revenue multiple and 22x EBITDA. While MIXT most likely wouldn’t fetch the same sales multiples (currency risk, less US sales, lower contract values), the multiple discount seems egregious. The discount persists when looking at per-subscriber values.

A quick back of the napkin analysis for FleetMatics value per subscriber comes out to a shade below $3,000 per sub.

Source: Author Data

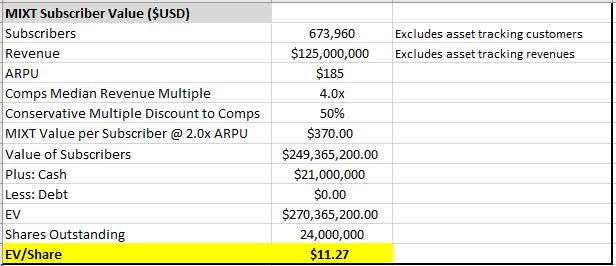

When valuing MIXT on a per-subscriber basis using a discount multiple, you can see the market is still assigning a value to MIXT subscribers that is way below competitors/peers. This is despite MIXT being one of the larger players in the space with a global presence and subscriber count of >800,000.

A peer median multiple discount should be applied to MIXT subscription revenues given that a portion of subscribers are made up of Light Fleet (20%) and Asset Tracking (17%) customers.

Source: Author Data

So excluding the entire revenue base from asset tracking customers, and applying an overly conservative 50% discount to the peer median EV/Revenue multiple of 4.0x, there still remains around a 35% discount to what I’d call starting fair value. A wide range of outcomes is possible here, but I like the operating history, the management team, the growth prospects and the price.

Risks/Mitigants

Exposure to oil and gas industry/a large chunk of revenues are correlated with oil prices – MIXT is not exposed to small businesses with bankruptcy risk in this segment, focus is on large fleets. 20+ years operating through cycles, commence large buybacks, still grow subscription revenues and subscribers, no contract terminations or customer losses, just downsizing

Currency risk – likely a reason for the discount. MIXT will be adopting US GAAP standards in 2020 as well as becoming a domestic filer in April of this year, hopefully providing a window for larger funds to take a look (many aren’t able to own ADRs)

Amazon/Google/OEMs develop their own cheaper fleet management technology – the company has historically commented on the potential of this happening, however most fleets utilize multiple OEMs, and most likely want a hardware agnostic solution. In addition, MiX is already giving their hardware away as part of the bundled offering

Low barriers to entry for simple functionality solutions – takes a lot of resources/knowledge/time to develop a sophisticated solution with multiple features needed for enterprise fleets

Lack of pricing power – large fleet customers don’t allow pricing flexibility and are quick to reduce fleet sizes during periods of reduced demand. However, product is very sticky, and MIXT has yet to lose a customer (just seeing reduced fleet sizes)

Growth and margin expansion can come from large deals only – particularly oil and gas related deals are driving a lot of large fleet expansion. Would like to see more customer diversity in the large fleet segment

End markets go out of business/decrease fleet sizes – despite fleet sizes decreasing across some of the oil and gas vertical, MIXT has not lost one customer. Retention rates for large fleets (>500 vehicles is 100%!)

Insurers no longer offer discounts for fleets that have installed MiX products – haven’t seen much of this

Products/services not required/low ROI/discretionary – MiX subscription costs make up a tiny portion of client’s expenses on a per-vehicle basis, and the ROI remains compelling

Once-in-a-100-year virus shuts down the economy for a period of weeks/months – unclear how this is affecting MiX at this stage, other than less driving hours on the road, longer sales cycles, no in-person demos/presentations of the product etc.

Industry consolidation could lead to increased competition that has better scale/leverage/pricing flexibility – consolidation would be a good thing for MIXT, they may lead some of the consolidation efforts. Management has long talked about doing an acquisition at the right price

Supplier risk as two key suppliers for GSM module components (extended lead times on orders) – hasn’t been an issue thus far

Disclosure: I am/we are long MIXT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment