Enes Evren/E+ via Getty Images

We have mixed feelings after reviewing MillerKnoll’s (NASDAQ:MLKN) Q2 results. While it beat expectations and guided in-line for next quarter, we are seeing clear signs that work-from-home is taking a toll on the business with the Americas Contract segment experiencing a 17% decrease in order levels in the second quarter. Fortunately, MillerKnoll’s diversified business model has helped mitigate some of these pressures. Internationally the work-from-home trend has been less strong, and has also seen a faster return to the office. It appears that the way people are working has not changed as much internationally. This is reflected in new orders for the International Contract & Specialty segment being essentially flat compared to last year organically. Meanwhile the Global Retail segment saw new orders down only 4% organically. This is much better than the Americas Contract segment, and impressively Global Retail is now a business with over $1 billion in annual revenue. This is despite orders having softened in the residential home furnishings market.

In general, the company is going to have to navigate softer order levels across its business segments. Particularly in the Americas segment, revenues have been running ahead of order levels, which means the company is working down its backlog.

In terms of profitability, it was nice to see that both the Americas Contract segment and the International Contract & Specialty segment experienced operating margin expansion. Price increases and cost synergies have helped improve profitability.

MillerKnoll is doubling down on the strength in the international segment. It on-boarded nearly 50 dealers in Europe and will emphasize Asia-Pacific and Middle East dealer onboarding during the next few quarters.

Q2 2023 Results

Consolidated net sales in the second quarter were just under $1.1 billion, an increase of 4% on a reported basis and 8% organically compared to the same quarter last year. Consolidated orders of $1 billion were 12.5% below prior year levels on a reported basis and 9% lower organically.

Gross margin in the quarter was 34.5%, which is 10 basis points higher than the same period last year. Adjusted gross margin declined 40 basis points compared to the comparable period last year. The decline in adjusted gross margin was primarily driven by inflationary pressures and the near-term elevated inventory-related costs for retail, partially offset by further realization of price increases and synergy capture.

Operating margin for the second quarter was 3.6% and on an adjusted basis came in at ~6%, which was 20 basis points lower than the prior year. Higher sales and well-managed operating expenses helped partially mitigate the near-term pressures on gross margin. MillerKnoll reported diluted earnings per share of $0.21 in the quarter and adjusted diluted earnings per share of $0.46, compared to $0.54 in the same period last year.

The company ended the second quarter with cash on hand and availability on its revolving credit facility totaling $428 million, and a net debt to EBITDA ratio of 2.8x.

Guidance

Guidance for next quarter was not particularly strong, although the company reminded investors that next quarter usually sees a relative seasonal slowdown in factory production around the holiday period and in the month of January. Guidance for the third quarter is for sales to range between ~$980 million and $1.01 billion, and adjusted earnings per share to be between $0.40 and $0.46. Given the number of headwinds the company is experiencing, and the slowdown in orders, we view this guidance as relatively attractive.

Valuation

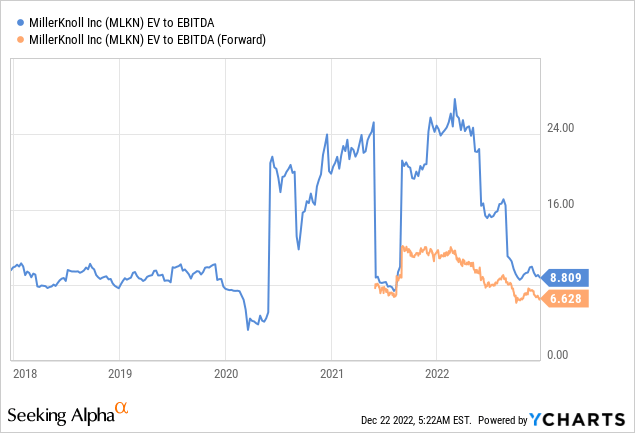

Despite some of the headwinds the company is experiencing, we continue to believe shares are significantly undervalued. Historically it has traded with an average EV/Revenues multiple close to 1x. This valuation multiple is currently ~0.65x, which is very low for the company and other than during the worst of the Covid crisis, it traded above this level in general during the past ten years.

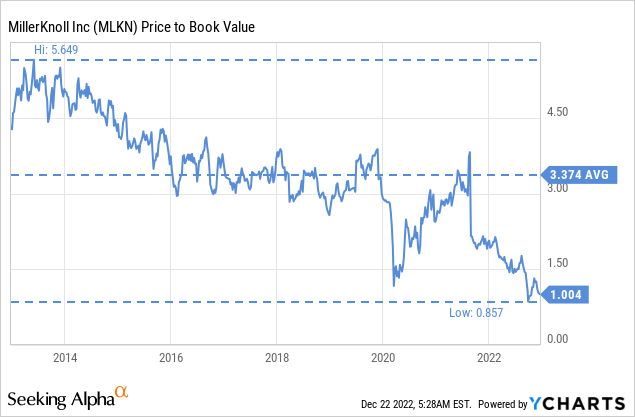

Shares also look cheap on an EV/EBITDA basis, especially the forward multiple which is currently an undemanding ~6.6x.

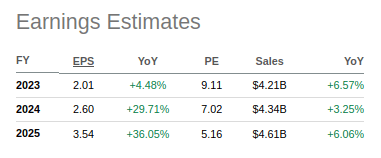

Perhaps the indicator that screams “cheap” the loudest is the price/book multiple. While we tend to give this valuation multiple less importance, it is still surprising to see that the company is trading at a cheaper multiple to book value than during the worst of the Covid crisis.

A more practical indicator, especially for income investors, is the dividend yield. Shares are currently yielding over 4%, which is very high for the company. Historically it has tended to yield closer to 2%. If the headwinds we have discussed get much worse, we would not be surprised to see the dividend cut or temporarily suspended, but so far the company is maintaining the dividend.

Seeking Alpha

If analysts are correct, the company should see much higher earnings in a couple of years. On average analysts estimate EPS of $3.54 by fiscal 2025. That means shares are trading at only ~5x what analysts expect the company to be earning in two years.

Seeking Alpha

Risks

There are two very important risks that investors should consider with MillerKnoll. One is the balance sheet, which despite having high liquidity is more leveraged than we believe to be prudent. This is reflected in a low Altman Z-score below the critical 3.0 threshold. The other big risk we see is that of a potential recession in 2023 which could add to the current headwinds the company is already experiencing, including the work-from-home trend and inflationary pressures.

Conclusion

We believe things would be looking a lot worse for MillerKnoll were it not for its diversified business model. The Americas Contract segment experienced a huge drop in orders, but this was mitigated by more stable orders from the Global Retail and International Contract & Specialty segments. Despite the headwinds and numerous risks, we still believe shares to be significantly undervalued. Hopefully the company will be able to navigate through this difficult period, and it should be able to earn much higher profits in the future.

Be the first to comment