Orla/iStock via Getty Images

A Different Approach to Valuation:

Cathie Wood, portfolio manager for the ARK Innovation Fund (NYSEARCA:ARKK) offered a rebuttal to her many critics earlier this month. She laid out her doubters’ views fairly succinctly with:

“For years, market pundits have been warning investors about “profitless tech”––companies ostensibly incapable of turning a profit. They describe stocks in ARK’s strategies as “concept capital” and suggest that our investment team either cannot distinguish profitable companies from unprofitable ones or seeks to invest in unprofitable companies.”

For anyone who has read my first write up or more recent piece on ARKK, that quote about sums up what I believe appears to be the investment style of the fund’s management.

Wood follows that up with her standard defense: that the ARKK team is investing for the long term.

“In our view, the companies in which we invest are sacrificing short-term profits to capitalize on the exponential growth and highly profitable opportunities that a number of innovation platforms are creating.”

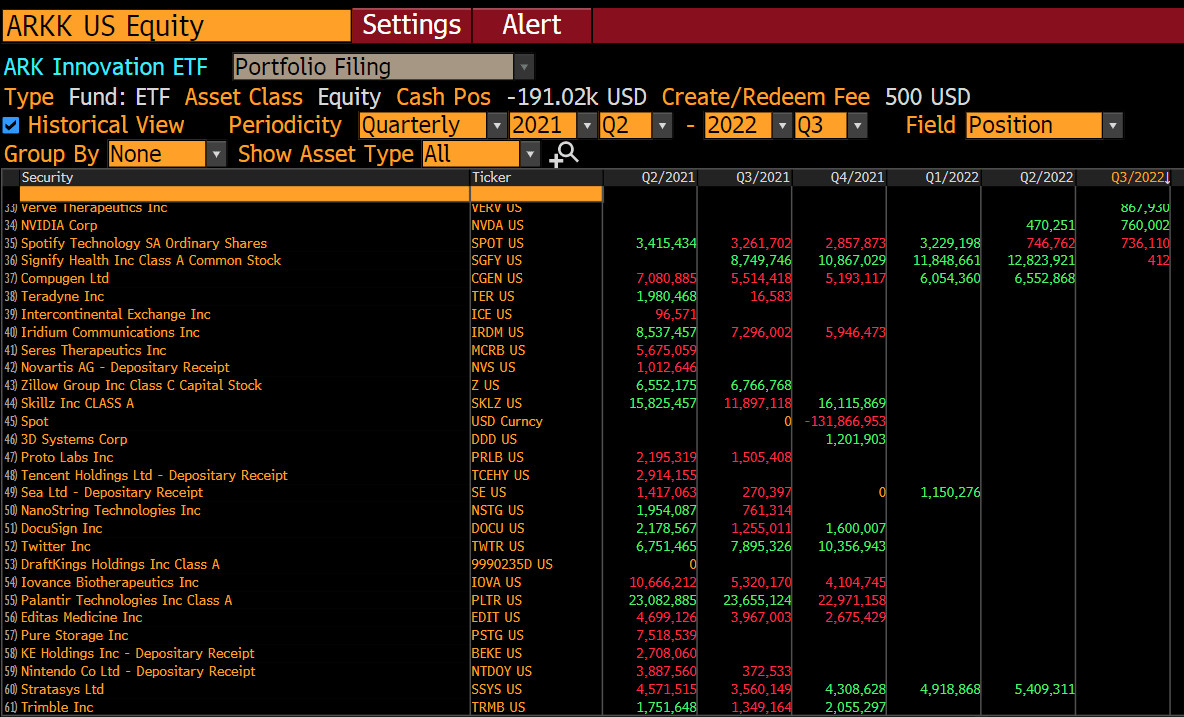

As I have written previously, while that argument might sound good as a marketing piece, it is not supported by the holdings of the fund. From the end of the second quarter 2021 to the end of the third quarter 2022, ARKK exited 25 investments versus the 36 it currently holds.

ARKK Exited Positions over the Past Five Quarters (Bloomberg)

Such turnover is not indicative of a five-year horizon.

I think the ARKK team might have been okay if the counterargument had just ended there. Instead, they offered their differentiated (being kind) view of how to measure a company’s profitability.

“We adjust EBITDA to normalize expenses that are investments and should be capitalized. In a company’s early days, a significant amount of research and development, stock-based compensation, and even sales and marketing are investments in platforms that ultimately will yield significant cash flow.”

In other words, nearly every cost for a young growth company is an investment in the future that shouldn’t be counted towards current losses. I assume that means that we should also ignore the ongoing funding requirements such losses generally necessitate, or the future dilution to earnings (should they ever materialize) created by that SBC (stock-based compensation). In my opinion, this thinking is akin to forgetting about every tee shot I hit into the woods, necessitating another tee shot. That first tee shot was just practice for my better (hopefully but not always) second shot.

The ARKK paper claims that if one were to make those cost adjustments, 84.9% of ARKK’s holdings would be “profitable” instead of the current 27.8%. Quite the trick. What I find truly astonishing is that even by eliminating R&D, sales and marketing and SBC, over 15% of the ARKK portfolio still would not be profitable! How much leeway can one give an enterprise?

Disdain for Fundamentals:

Cathie Wood does not hide her disdain for “companies that have catered to short-term oriented shareholders with share repurchases and dividends, at the expense of investing in the future.”

Yes, isn’t it terrible when profitable, cash-generative franchises return excess capital to shareholders? Moreover, apparently, the ARKK team is so accustomed to looking at companies that are cash-burning furnaces, that they posit that a company cannot have the means to reinvest in its business responsibly while simultaneously returning excess cash to shareholders. Meanwhile, I believe most classically trained value investors search for just such opportunities and are often successful at it.

Last Line of Defense:

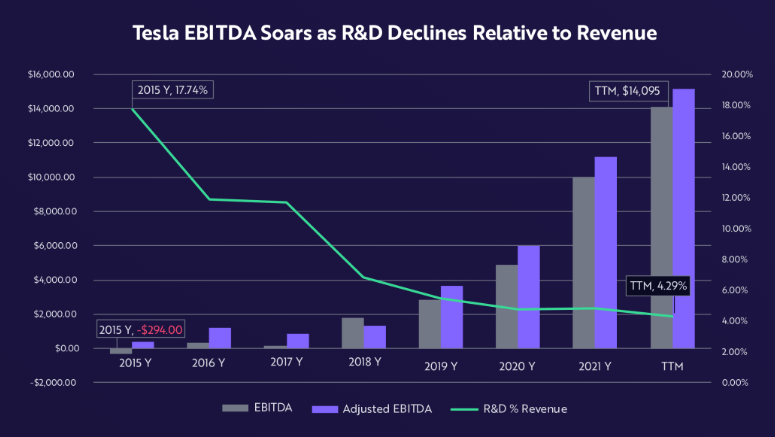

A portion of the ARKK letter is dedicated to describing Tesla (TSLA) as a model for this theory of treating all of those operating costs as investments. They point out that higher revenue grows, the lower a percentage R&D becomes.

Tesla R&D vs Revenue 2015-Present (ARKK memo)

I don’t blame the ARKK team for throwing TSLA in its doubters’ faces. After all, that stock’s remarkable run drove a good deal (I don’t have the exact amount) of ARKK’s own returns in 2020.

TSLA is an incredible company. It is the only example I know of a car company starting essentially from scratch and making it into the mainstream and relatively large production over the past seventy or so years.

However, ignoring all of the costs TSLA incurred getting to its elevated state was not without considerable risk. Elon Musk has admitted that as recently as 2019, TSLA was “30 days from bankruptcy” while it was ramping up production of the model 3. Maybe Cathie Wood and her team consider investments for the future in purely virtuous terms, but the world ultimately revolves around cash flow. Run out of cash and you run the risk of bankruptcy. In periods like now when funding for higher risk/VC-like investments becomes harder to come by, companies that burn cash risk running out of it.

Rebuke from Seasoned Investors:

The ARKK memo drew criticism from other wall street players. Dan Loeb of Third Point tweeted, “Anyone teaching a value investing class or one on investment psychology should use this memo as a treatise to study the mindset of stonk hodlers.”

Cliff Asness of AQR responded with, “Value investors who have to ride out manias driven by people like her are the “short-term” investors. So wrong. But her forecasting a bazillion percent GDP growth and forecasted returns of a bazillion were a hint.

Rich Handler of Jefferies added, “I can think of a lot of ways to use up all of our cash flow for rapid revenue growth that will last awhile, until it doesn’t. Then we’re dependent on someone else to believe even more than we do and supply the capital to keep going. Hope they believe at a higher valuation.”

I believe this last comment from Handlers sums up the crux of the difference between Cathie Wood et al and more traditional investors like myself who focus on cash flow and asset values. In my opinion, her style of investing without regard to cash generation or valuation relies on the greater fool theory. To make money, one must have others who believe that a continuous supply of capital will seek assets at continually higher prices, unanchored from any reasonable measure of value.

Conclusion:

As I have said before in previous critical write ups, I am not attacking Cathie Wood or anyone at ARKK personally. I do not know anything about them. But I sincerely believe that investing exclusively in unprofitable business and/or without regard to valuation is a non-sensical approach that only works in the most maniacal of bubbly markets. One would think that losses approaching 80% from a high set less than two years ago would inspire at least some self-reflection from the ARKK crew that maybe they have been wrong. This memo indicates that they have learned nothing. I believe those who continue to entrust them with capital risk even further losses.

Be the first to comment