Eoneren

Analyzing MicroStrategy Incorporated (NASDAQ:MSTR) using a sum of parts valuation, I think the company is overvalued by over 60%. Even if one is bullish on Bitcoin (BTC-USD), there are a multitude of ways to gain exposure without having to pay the exorbitant premium to NAV on MSTR shares. Bitcoin is unlikely to rally sustainably until macro risk appetites improve. Investors can monitor this by looking at the ratio of Invesco S&P 500 High Beta ETF (SPHB) to the Invesco S&P 500 Low Volatility ETF (SPLV) ETF.

Brief Company Overview

MicroStrategy Incorporated, led by its mercurial Chairman Michael Saylor (formerly the CEO), is a business intelligence software company that also happens to own ~130k Bitcoins.

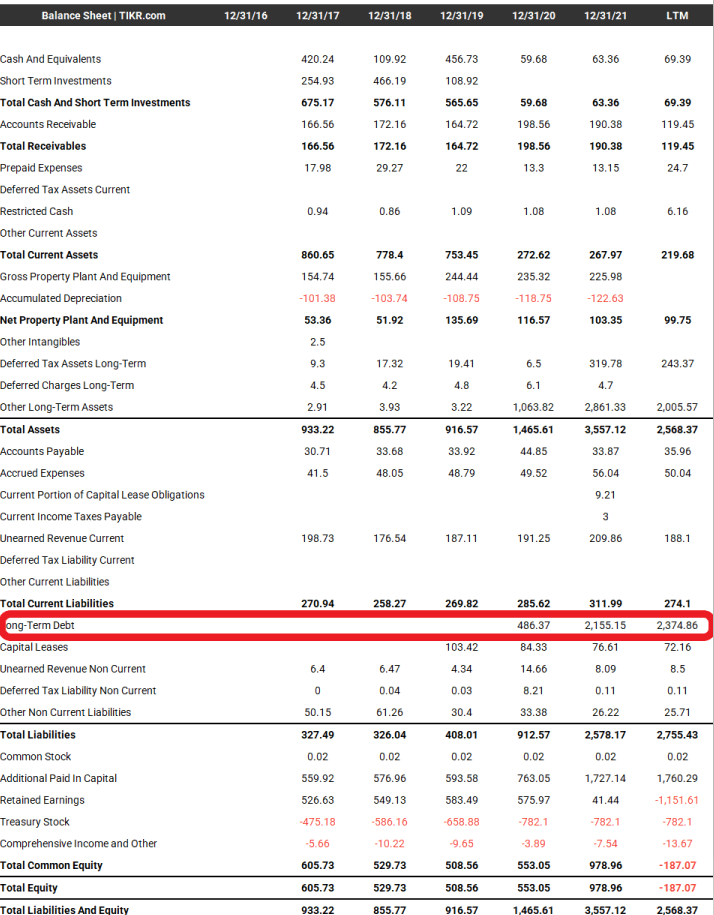

MSTR, once a sleepy small-cap survivor of the dot-com bust, famously adopted its Bitcoin strategy shortly after the COVID pandemic. First, it spent a portion of its cash reserves to acquire ~21k Bitcoins in August 2020 at ~$11,600 / Bitcoin. After exhausting its cash reserves, MSTR went even further, issuing more than $2 billion in debt to acquire even more Bitcoins (Figure 1).

Figure 1 – MSTR Balance Sheet (tikr.com)

Ultimately, the company has acquired approximately 130k Bitcoins for $4 billion in consideration, financed through multiple debt issuances.

Share Price Rode The Bitcoin Rocket

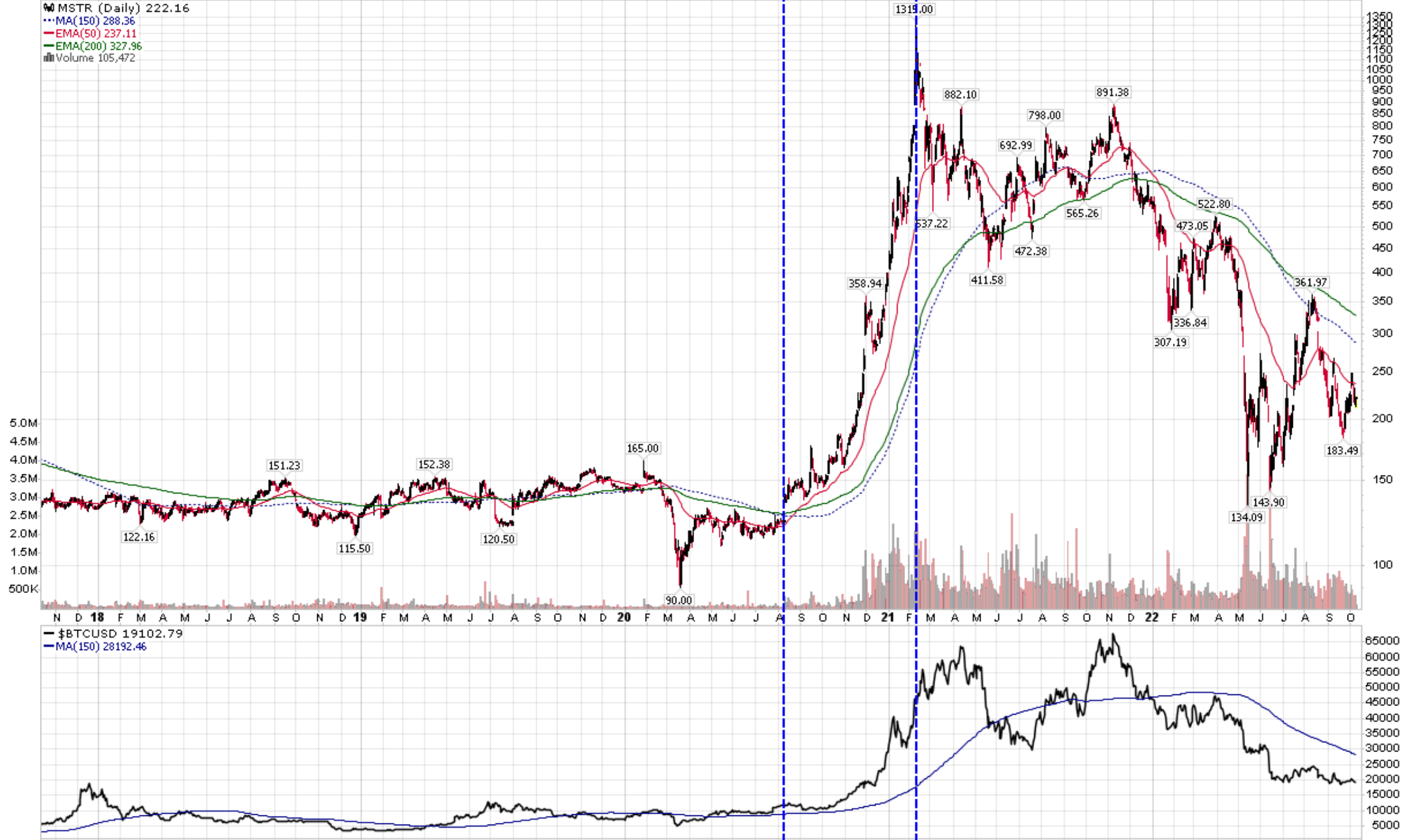

MSTR stock price rode the Bitcoin rocket, reaching a peak of $1,315 by early 2021, almost 10x its pre-pandemic range of $115 to $165 (Figure 2).

Figure 2 – MSTR benefitted tremendous from bitcoin price rise (Author created with price chart from stockcharts.com)

MSTR’s rise was even more remarkable, given that Bitcoin price only rose from ~$11,000 when MSTR first purchased them, to $45,000 when MSTR peaked at $1,315.

Part of the reason for MSTR’s meteoric rise was scarcity. At the time, MSTR was one of the few vehicles that investors could use to speculate in the price of Bitcoin. In effect, MSTR traded like a Bitcoin ETF, with a significant premium to its “Net Asset Value”.

However, as 2021 rolled on, crypto investors started having more investment options. First, ETFs like the Purpose Bitcoin ETF (BTCC:CA) that hold Bitcoins began to trade on Canadian exchanges. Furthermore, crypto exchanges such as Coinbase (COIN) became popular, giving investors direct access to crypto assets. Finally, ETFs like the ProShares Bitcoin Strategy ETF (BITO) were launched on U.S. exchanges that gave investors exposure to Bitcoin through futures contracts.

With so many ways to gain crypto and Bitcoin exposure, why would anyone need to buy MicroStrategy stock?

Sum Of Parts Valuation Suggests Stock Is 60% Overvalued

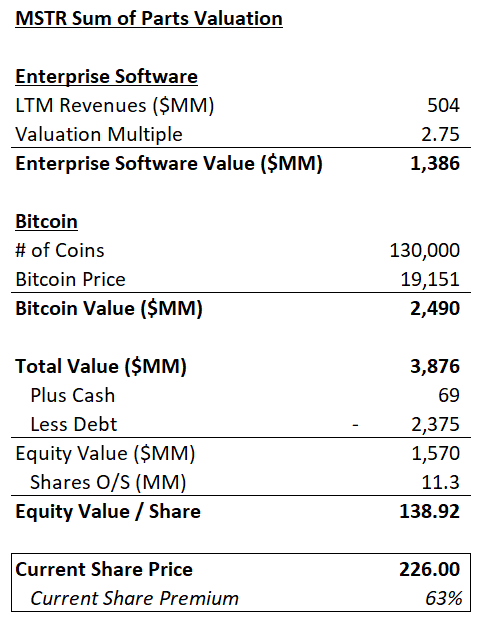

Valuing MicroStrategy using a sum-of-parts analysis, assuming the Enterprise Software business trades for 2.75x Price/Sales (the business traded between 2.5 – 3.0x Price/Sales prior to the adoption of the Bitcoin strategy) I come up with an equity value of $139 / share. With the shares currently trading at $226 / share, I think they are overvalued by over 60%.

Figure 3 – MSTR Sum of Parts Valuation (Author Created)

Bitcoin Highly Correlated With Risk Appetite

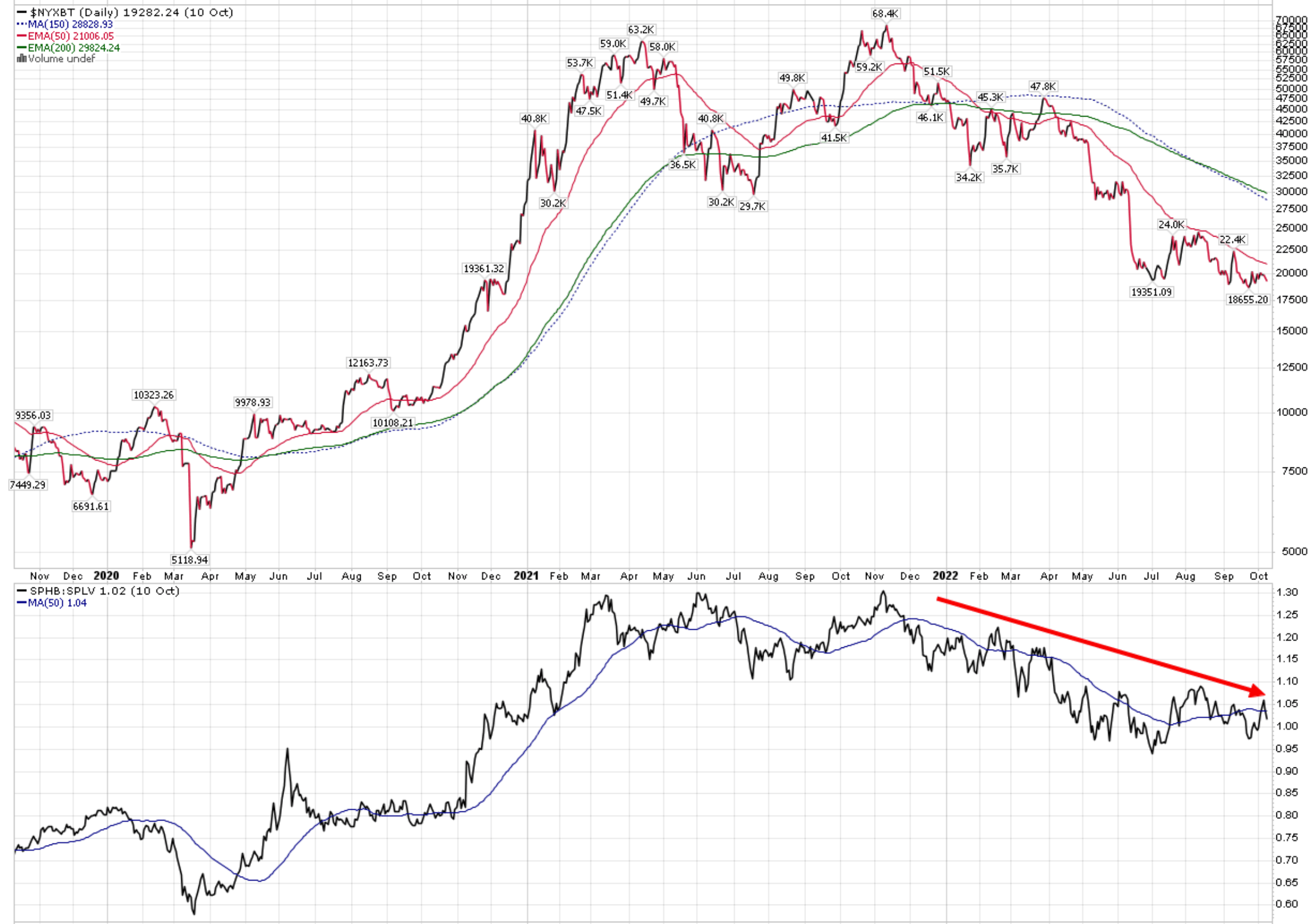

Putting aside the bull case for Bitcoin, since one either believes it or one doesn’t, we can see from factual evidence that Bitcoin prices are highly correlated to risk appetite, as measured by the ratio of the Invesco S&P 500 High Beta ETF to the Invesco S&P 500 Low Volatility ETF. Figure 4 shows the price of Bitcoin ebbs and flows as the SPHB/SPLV ratio rises and falls.

Figure 4 – Risk Appetite As Measured By SPHB/SPLV (Author created with price chart from stockcharts.com)

Currently, risk appetites are still in a downtrend, hampered by the Fed’s interest rate increases and tightening financial conditions. Until the macro situation changes, Bitcoin is unlikely to experience a sustainable rally.

Risk To My Call

The risk to my cautious call is obviously if the Bitcoin price rallies sustainably, then my bearish view on MicroStrategy will turn out to be incorrect. I believe investors can protect themselves from this risk by pair trading MSTR against an asset that has positive leverage to Bitcoin prices. For example, if we go long the BITO ETF (BITO trades near its NAV) and short MSTR, we can hedge away most of the Bitcoin risk and only bet on MSTR’s premium to NAV declining over time.

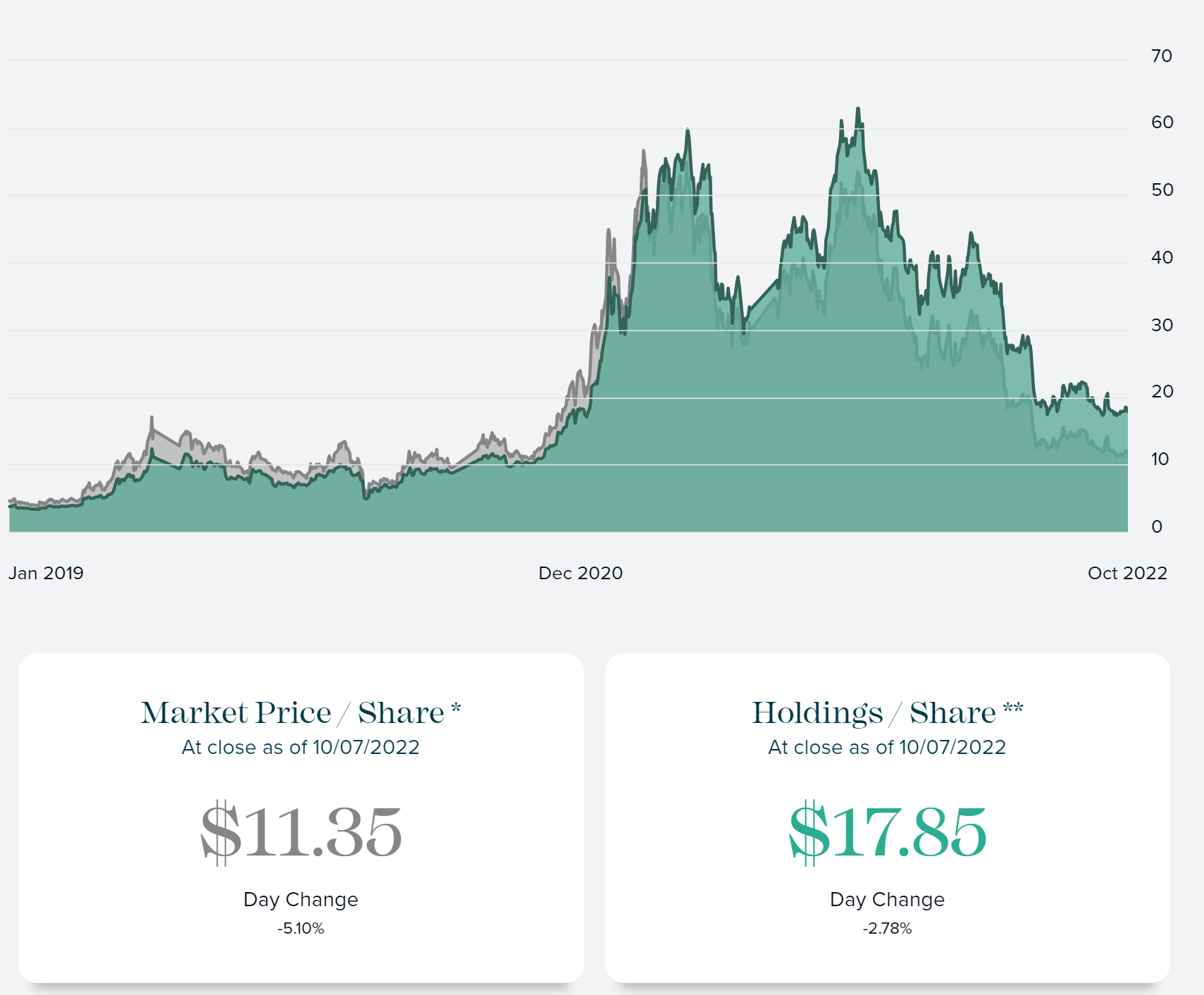

Investors who are bullish on Bitcoin may even wish to bet on the Grayscale Bitcoin Trust (OTC:GBTC), as it is currently trading at a 37% discount to NAV (Figure 5). Historically, when Bitcoin was in a bull phase, GBTC had traded at a premium to NAV as high as 30% (January 2021). However, GBTC does have an issue in that the trust currently does not have a built-in mechanism to close its discount to NAV. There was hope that GBTC’s proposed conversion to be an ETF would close the discount, however, to date, the SEC has denied GBTC conversion proposal.

Figure 5 – GBTC Discount To NAV (grayscale.com)

Investors should note that any pair trade strategy will involve shorting MSTR, which may introduce idiosyncratic risks associated with shorting meme-like stocks such as MSTR.

Conclusion

I think MSTR is overvalued by over 60% if we analyze the company using a sum of parts valuation. Even if one is bullish on Bitcoin prices, there are a multitude of ways to gain exposure without having to pay the exorbitant premium to NAV on MSTR shares. For example, investors can choose the BITO ETF which trades at NAV, or the GBTC trust which trades at a 37% discount to NAV.

In my opinion, Bitcoin is unlikely to rally sustainably until macro risk appetites improve. Investors can monitor this by looking at the ratio of SPHB to SPLV ETF.

Be the first to comment