Chesnot/Getty Images News

Introduction

Last week, I opined that going into its Q2 FY2023 report, Microsoft’s (NASDAQ:MSFT) stock was overloved and overvalued despite CEO Satya Nadella’s warning for a challenging couple of years for the tech sector. Based on our evaluation of Microsoft’s business fundamentals, valuation, technicals, and quant factor grades, we concluded that Microsoft is not a good buy at $240.

Here’s a link to the full report for your perusal:

- Microsoft Stock: You Have Been Warned By Satya Nadella

In the note tagged above, I wrote the following excerpt:

Microsoft is a fantastic business, but it is not immune to the broader economy. The tech giant is set to release its Q2 FY2023 quarterly report on 24th January 2023 and based on Nadella’s warning, I think this report could be a rude awakening for investors. Back in September, we discussed Microsoft’s Q2 FY2023 outlook and its management’s grim commentary on the economy in the following report:

Heading into next week’s earnings release, Microsoft’s stock looks primed for a significant move (up or down) based on its technical chart. While the macroeconomic environment remains uncertain, Microsoft may continue to retain its safe haven status by being more resilient than its peers – like a good house in a bad neighborhood. Past headwinds – high inflation, rising interest rates, and a strong US dollar – have all turned into tailwinds in recent weeks.

While some macro headwinds have turned into tailwinds, rising wages and flailing demand (due to a weaker IT spending environment) are set to result in further deceleration in growth rates at Microsoft whilst causing a margin contraction! As I see it, the recent warning from Satya Nadella should be taken seriously by all investors.

At ~25x P/E, Microsoft is looking expensive compared to peers and the market (S&P 500 P/E: ~18x). I continue to believe in Microsoft as a business; however, the stock is overloved and overvalued. The risk/reward is unfavorable for a near to medium-term investment, and so, I am happy to sit on the sidelines until Microsoft gets down to $200 or the valuation gets better with time.

While my initial plan was to sit on the sidelines and hold my shares through a potential downturn, Microsoft’s shocking guidance for Q3 FY2023 and a horrific outlook for the rest of this fiscal year has prompted me to downgrade the stock to a “Sell” rating.

In this note, we’ll analyze Microsoft’s Q2 results and forward guidance. Furthermore, I will share the rationale behind my decision to downgrade Microsoft in the aftermath of a mixed report. Without any further ado, let’s unpack Microsoft’s quarterly report.

Microsoft, Inc. Q2 FY2023 Earnings Review

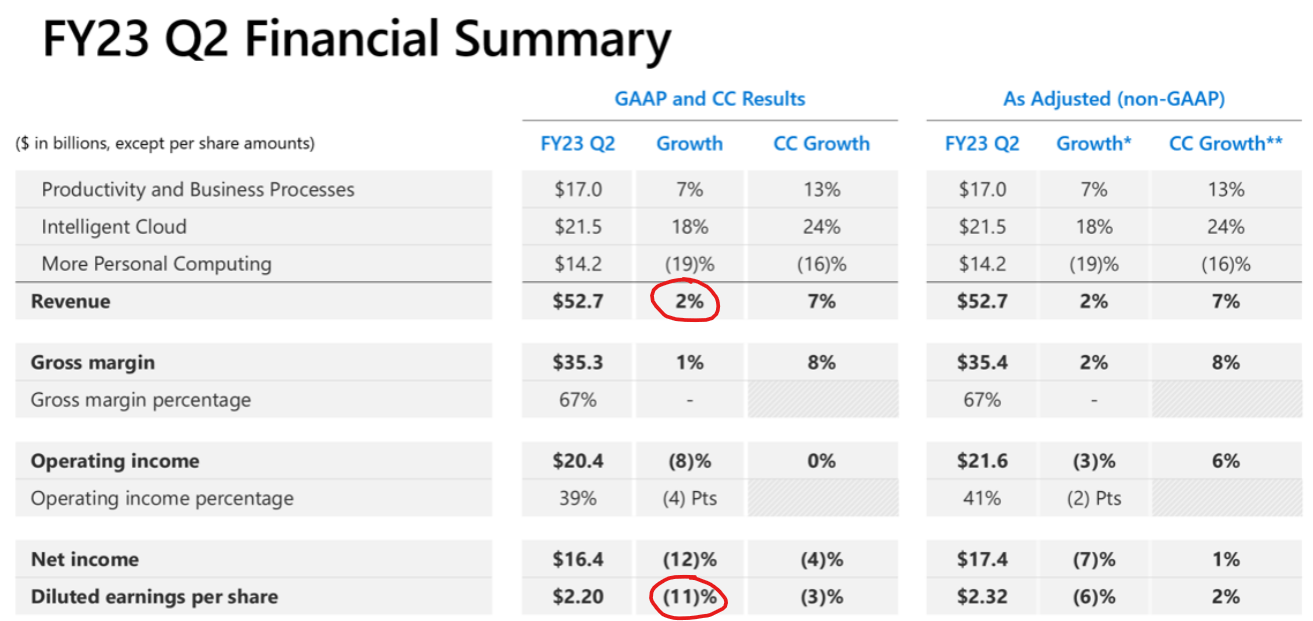

In Q2 FY2023, Microsoft recorded total revenues of $52.7B (up 2% y/y), missing Wall Street estimates of $53.2B by ~$450M. Despite a miss on the top line, Microsoft managed to deliver a slight beat on EPS, which came in at $2.32 (vs. est. of $2.31).

Microsoft Q2 FY2023 Earnings Presentation Microsoft Q2 FY2023 Earnings Presentation

While Q2 earnings have met management’s guidance, Microsoft may still need to tighten its belt even further as operating expenses are still outpacing revenues. Despite slashing 10,000 jobs last week, Microsoft’s employee count grew by +19% y/y at the end of Q2 FY2023.

Microsoft Q2 FY2023 Earnings Presentation

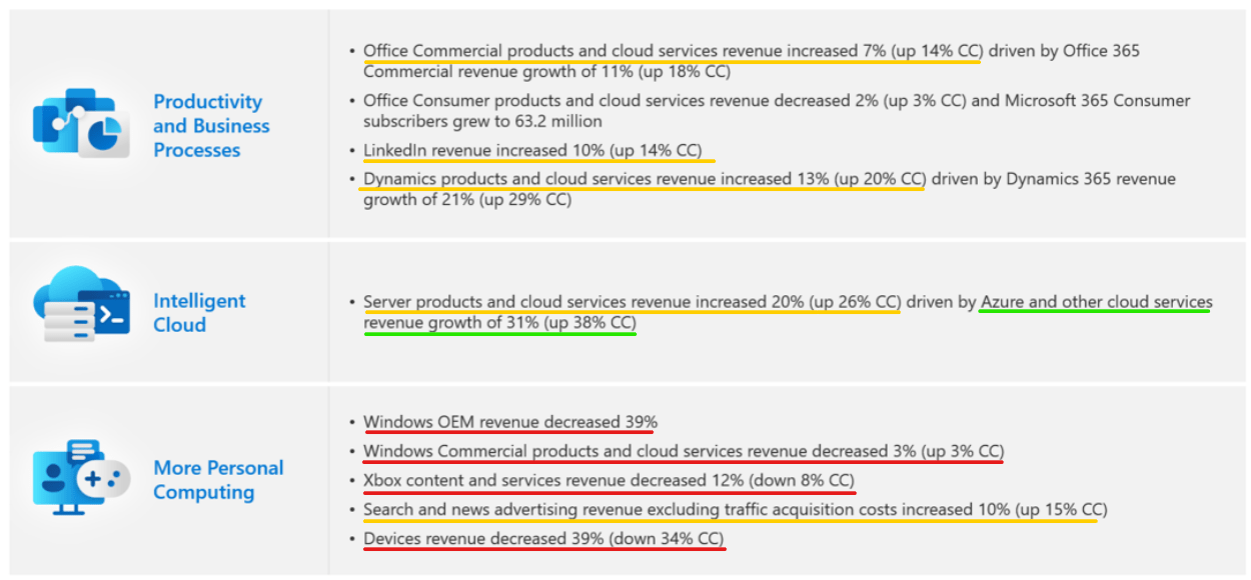

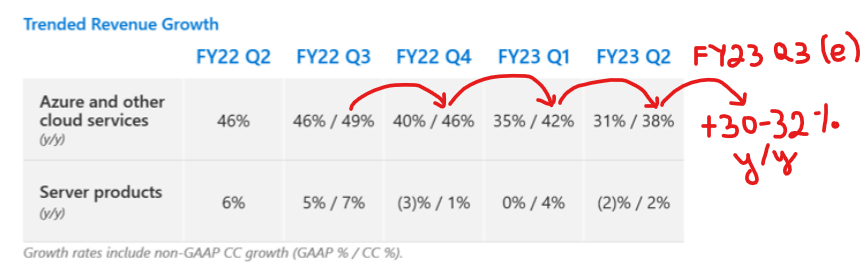

On a more granular level, Microsoft’s Azure Cloud business meeting revenue growth expectations of 31% y/y (+38% CC) was the highlight of this report. Furthermore, LinkedIn and Search & News advertising revenues were each up ~10% y/y, but Microsoft’s management highlighted that marketers are still being cautious.

Microsoft Q2 FY2023 Earnings Presentation

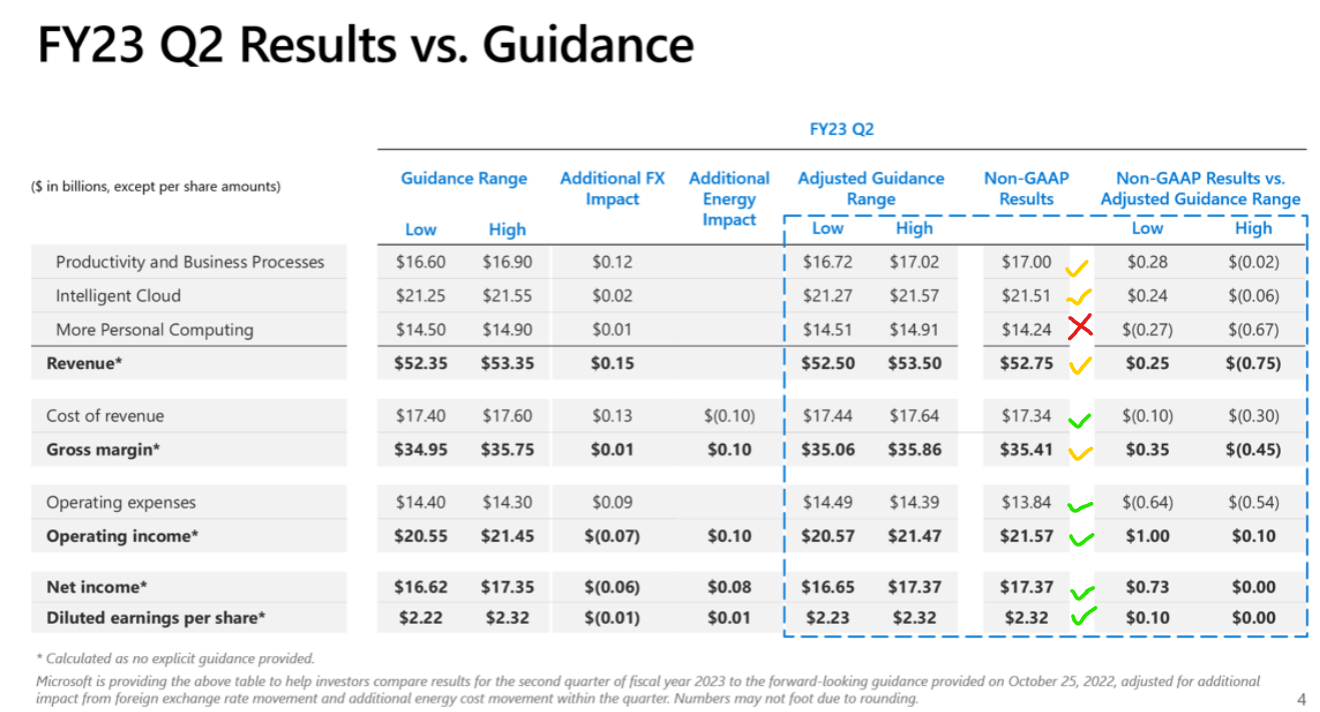

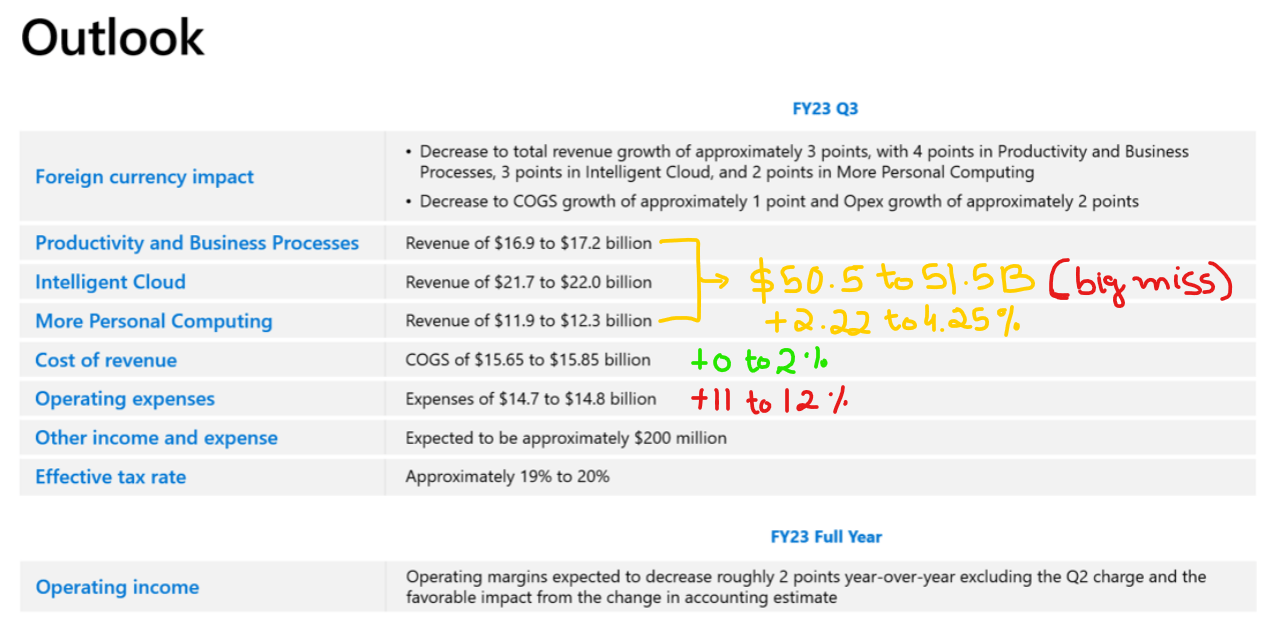

While Microsoft’s Productivity & Business Processes and Intelligent Cloud segment revenues for Q2 fell within management’s guidance range, the “More Personal Computing” segment revenue of $14.24B came in well below management’s guidance as Windows OEM and Devices revenue decreased by 39% y/y, amid a post-COVID normalization in PC demand. Xbox content and Services revenue also decreased by ~12%.

In a nutshell, Microsoft’s Q2 report was uninspiring, with a small EPS beat being offset by a miss on revenues. I am downgrading Microsoft on a mixed quarter; why you ask?

Rationale For Downgrading MSFT

In a challenging macroeconomic environment, Microsoft’s primary growth engine (Azure cloud) is hitting a snag, with management guiding for a sharp deceleration in Q3 to 30-32% y/y (from 38% y/y in Q2) based on weak trends seen in December.

I’d like to start by reiterating Satya’s thoughts on the changing environment and our priorities, which underpin the decisions communicated in last week’s announcement.

We exited Q2 with Azure growth in the mid 30s in constant currency and from that, we expect Q3 growth to decelerate roughly 4 to 5 points in constant currency.

Microsoft Q2 FY2023 Earnings Presentation

In Q2, Microsoft’s revenue growth slowed down to 2% y/y, and with Azure Cloud revenues decelerating rapidly, Microsoft’s business outlook appears to be grim. For Q3, Microsoft guided for revenues of $50.5 to $51.5B [well below Wall Street estimates of $52.5B].

On the earnings call, Microsoft’s executive leadership provided the following commentary:

As I meet with customers and partners, a few things are increasingly clear: Just as we saw customers accelerate their digital spend during the pandemic, we’re now seeing them optimize that spend. Also, organizations are exercising caution given the macroeconomic uncertainty. We are focused on helping customers do more with less.

– Satya Nadella, CEO

Customers optimizing their digital spend and trying to do more with less are just codewords for saying that demand is faltering. While Nadella spent a good bit of time talking up the next wave of computing platforms, this AI-driven growth wave is unlikely to materialize for another couple of years, by his own admission, in early January. Hence, we could be looking at a couple of years of low to no growth at Microsoft!

Microsoft Q2 FY2023 Earnings Presentation

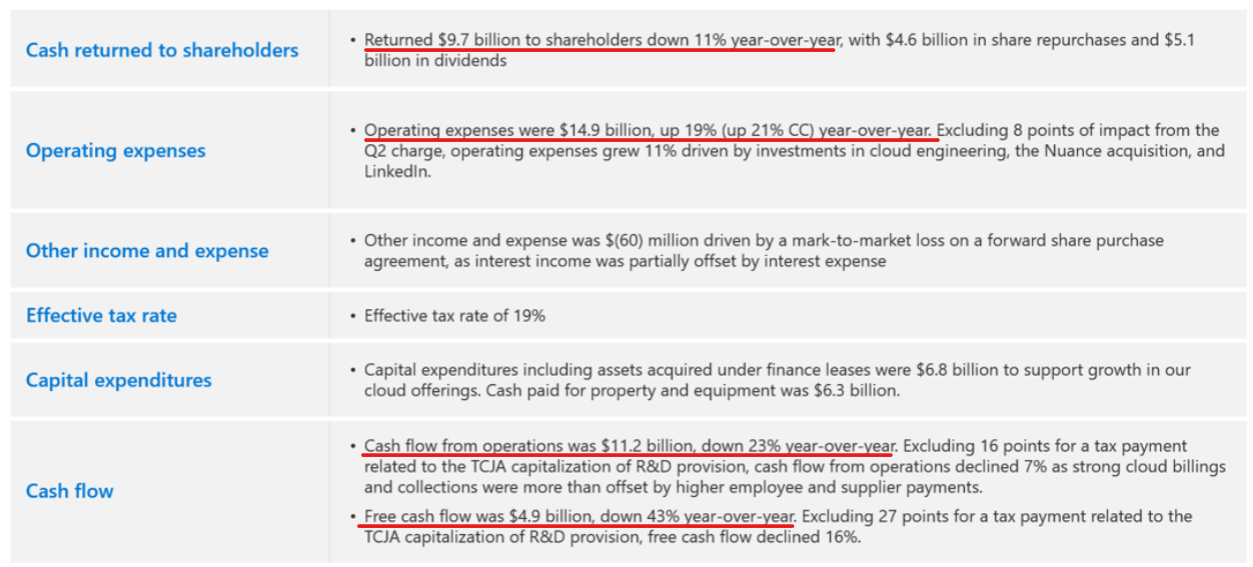

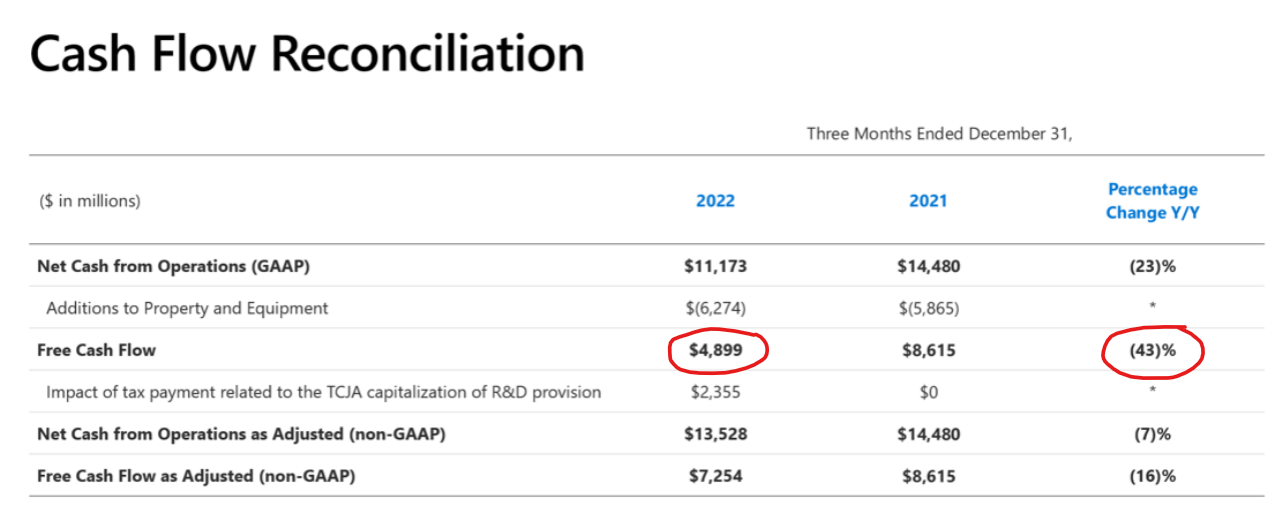

As operating expenses continue to outgrow revenues, Microsoft faces a painful earnings contraction in upcoming quarters. In Q2, Microsoft’s operating margin went down from 43.5% last year to 38.7%. Due to significant margin pressures, Microsoft’s cash flow from operations sank by -23% y/y in Q2, with free cash flows dropping like a rock (down -43% y/y).

Microsoft Q2 FY2023 Earnings Presentation

While Microsoft continues to boast a strong balance sheet, the fact that its Q2 free cash flows failed to cover its dividend expenses ($5.1B) is ample reason for investors to rethink their long positions in this counter.

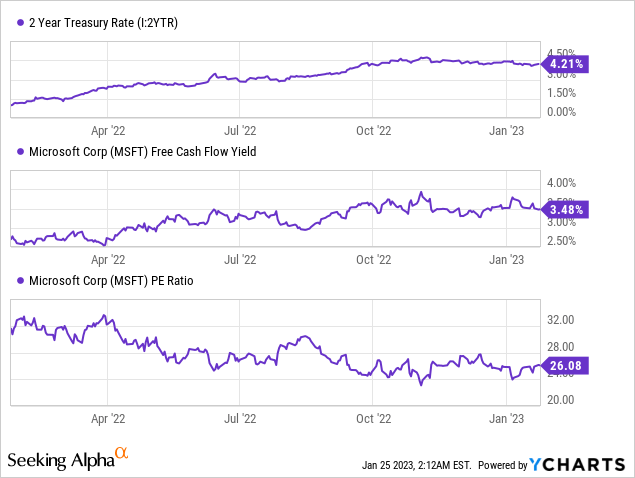

For FY2023, Microsoft is expected to grow revenue and earnings at low to mid-single-digit rates. With this drastic growth deceleration, Microsoft (at 26x P/E) is very expensive relative to the market (S&P-500 is trading at ~18x P/E). Furthermore, Microsoft’s free cash flow yield of ~3.5% is lower than most (risk-free) treasury bonds at this moment in time. The sheer lack of equity risk premium means Microsoft is priced for perfection, and there is absolutely no room for error.

Microsoft’s robust growth and free cash flow generation led to spectacular returns in the 2010s; however, as we learned today, revenue growth has slowed down to low single-digits, and free cash flows are collapsing.

The Q2 FY2023 report showed that Microsoft is not the “safe haven” everybody has fallen in love with over the years. And in my view, Microsoft will lose its valuation premium (sooner or later) to trade in line with the market (S&P500) multiple, which currently stands at ~18x P/E (higher than the long-term average of ~15-16x). With a TTM EPS of $9.12, Microsoft’s stock looks ripe for a reset to $164.16 per share (~30-35% down from here).

Interestingly, this price is pretty close to my fair value estimate of $161.26 per share. If you missed it, my updated valuation for Microsoft is available here.

With the FED still tightening its monetary policy, the odds of an economic recession remain elevated. And in the event of a recession, we could easily see Microsoft re-tracing to its fair value (and who knows, it could probably overshoot to the downside).

Final Thoughts

Overall, Microsoft’s Q2 FY2023 was not a good quarter for the Redmond-based tech giant, and the guidance for Q3 is simply horrifying (especially Azure growth deceleration). If a perceived safe haven company like Microsoft is experiencing a double-digit earnings contraction in this environment, I wonder how other S&P-500 companies will fare in this ongoing earnings season.

Anyways, the rapid deceleration in Microsoft’s cloud business looks primed to act as the trigger for a valuation reset (removal of valuation premium) in this counter. Given the trends in Microsoft’s business, I now believe we are very likely to experience a 30-35%+ plunge in MSFT stock in the near to medium term. Hence, I am downgrading Microsoft from “Hold” to “Sell”.

Key Takeaway: I rate Microsoft a “Sell” at $240.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Be the first to comment