ryasick

Article Thesis

Blackstone Mortgage Trust, Inc. (NYSE:BXMT) is a leading mortgage trust that offers a compelling dividend yield of 11% and that trades at a very reasonable valuation. Compared to many other real estate financing companies, it has outperformed in the recent past and could continue to do so.

Blackstone Mortgage Trust: Attractive Business

Blackstone Mortgage Trust is a mortgage real estate investment trust that has outperformed many other major mREITs due to being active in a more attractive niche and utilizing a more resilient business model:

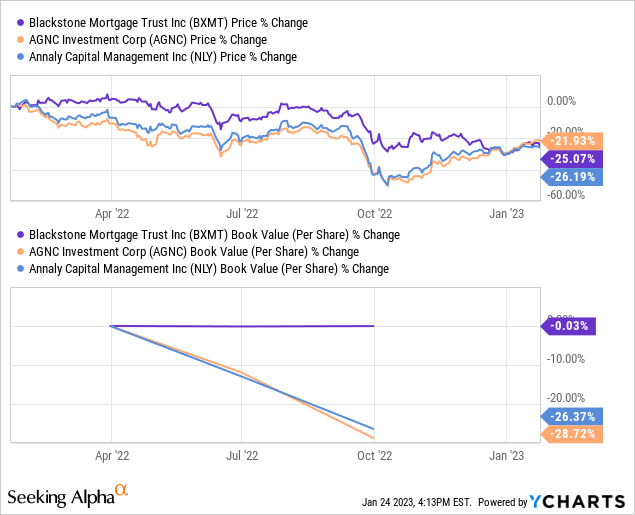

Over the last year, Blackstone Mortgage Trust’s book value per share is essentially flat. Meanwhile, mREITs such as AGNC Investment (AGNC) and Annaly Capital Management (NLY) have seen their book value per share drop by more than 25%. Somewhat surprisingly, Blackstone Mortgage Trust nevertheless saw its share price decline about as much as what AGNC and NLY experienced. I believe this provides a buying opportunity, as BXMT was sold off along with most other mREITs even though its business fundamentals outperformed versus its peers.

Blackstone Mortgage Trust’s book value outperformance versus the majority of mREITs can be explained by the fact that BXMT does not have to mark-to-market its assets, which was a key factor for the book value hits that many of BXMT’s peers experienced. This is due to the nature of BXMT’s assets — the company does not invest in publicly traded debt such as mortgage backed securities but originates loans itself, mostly ones that are backed by commercial properties in North America, but the mREIT also has some exposure to Europe and Australia.

While some deem commercial properties risky, Blackstone Mortgage Trust’s portfolio performance has been strong so far, despite a rise in interest rates. That can be explained by the fact that Blackstone Mortgage Trust primarily owns senior loans. The average loan to value at origination is just 64% — that means that even if commercial properties took a 30% hit across the board, the average BXMT loan would still be fully backed by the value of the underlying property. Even a major market decline in commercial properties would thus not necessarily impact BXMT meaningfully. The loan to value ratio of BXMT’s more recent originations is even better than the average across its portfolio, as the ratio stood at just 58% for the loans Blackstone Mortgage Trust made during the most recent quarter — a massive 40% price decline for these properties would still result in the loan being fully backed by the value of the property.

Blackstone Mortgage Trust has also chosen to increase its investments in one of the most attractive segments of the commercial property portfolio, industrial properties — these made up almost 80% of the loans that Blackstone Mortgage Trust originated during the most recent quarter. This includes assets such as warehouses that are used by logistics companies and online retailers such as Amazon (AMZN). Not only are these assets in high demand due to macro growth tailwinds, but they are also not very vulnerable versus recessions or economic downturns, unlike more cyclical assets such as hotels or shopping malls. All in all, this has resulted in a very compelling 100% interest collection rate in the recent past, including the most recent quarter, showcasing that BXMT’s risk management is strong and works well, even in the current uncertain environment.

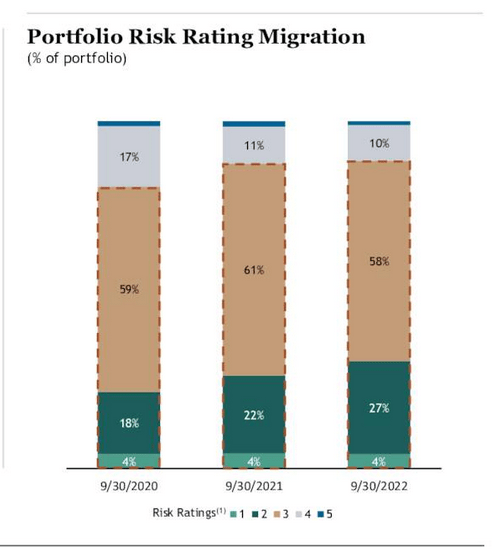

Looking at the loan quality of the loans BXMT has on its books today, we see the following:

BXMT presentation

Most of Blackstone Mortgage Trust’s loans are rated “3”, which indicates average risk. The second largest portion of BXMT’s loans are those rated “2”, which indicates below-average risk. As we see in the above chart, the trend has been very positive — the ratio of loans with below-average risk has risen, while the ratio of loans with above-average risk has declined over the last two years.

Blackstone Mortgage Trust Is A Winner In This Environment

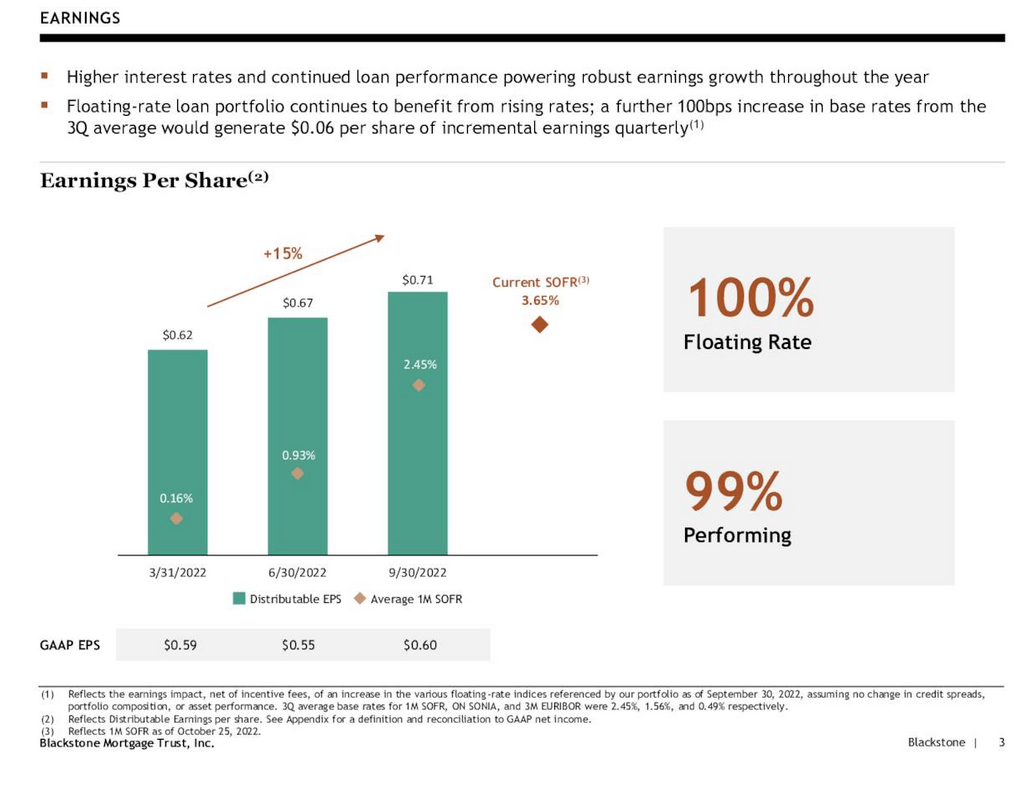

Blackstone Mortgage Trust is not only outperforming most of its mREIT peers when it comes to book value per share growth, but the company is also seeing its profits improve thanks to rising interest rates:

BXMT presentation

Earnings per share have risen by 15% between Q1 2022 and Q3 2022 (Q4 results are not out yet), driven by tailwinds from rising interest rates and, to a lesser degree, by new loan originations. All of the loans BXMT has originated have a floating interest rate — when interest rates climb, which has been the case in 2022, these loans generate more interest income, which drives Blackstone Mortgage Trust’s profits upwards. At the same time, Blackstone Mortgage Trust has locked in interest expenses on the financing side, which is why its financing costs are not rising as much as its interest income — rising interest rates thus make for a beneficial macro environment where BXMT is seeing considerable profit expansion as showcased by the above numbers. Blackstone does not have any short-term debt, thus refinancing in a rising rates environment will not be an issue in the foreseeable future — which indicates that management has been wise in locking in interest rates at an opportune time.

The Q3 earnings run rate is north of $2.80 per share per year, which is highly compelling for a company that is trading at less than $23 per share today.

Blackstone Mortgage Trust Offers A High Yield And Is Inexpensive

Blackstone Mortgage Trust has lifted its dividend to $0.62 per share per quarter years ago and has maintained the dividend at that level in recent years. The payout of $2.48 per year makes for a dividend yield of 10.8% at current prices, or almost 11%. A dividend yield this high is so attractive that no dividend growth is needed to make BXMT a compelling income investment.

Of course, when shares trade with a dividend yield this high, one should not blindly buy into a company before evaluating the safety of the dividend. But since Blackstone Mortgage Trust has kept the dividend stable for years, even during the COVID panic when other mREITs were hit hard, I do not see a dividend cut as likely. The company also covers the payout easily with its profits — based on expected earnings per share of $2.72 for 2022 and $2.91 for 2023, the payout ratio for those two years is 91% and 85%, respectively. While that would make for a pretty high payout ratio for an average company, mREITs tend to have high payout ratios. The fact that the payout ratio should improve going forward, thanks to the positive impact of rising interest rates on BXMT’s profitability, results in an improving dividend safety. Of course, a dividend cut can’t be ruled out, but I do not see a good reason why BXMT would cut its dividend in the foreseeable future.

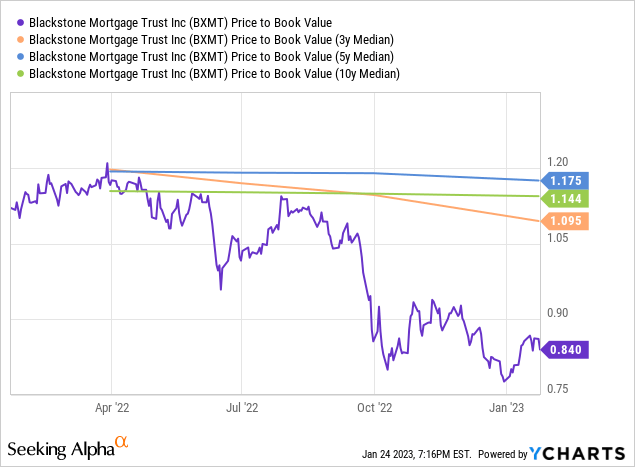

Blackstone Mortgage Trust’s dividend yield is pretty high due to the hit BXMT’s shares have taken over the last year, as they have declined by a pretty sizeable 25% — despite book value being resilient and profits actually growing in recent quarters. The share price decline that has caused BXMT’s yield to spike has also made its valuation decline, thus shares look attractively valued today:

Today, Blackstone Mortgage Trust trades at 0.84x book value. That’s lower than a year ago, and this also represents a major discount compared to how Blackstone Mortgage Trust was valued in the past. The median book value multiples over the last 3, 5, and 10 years are in the 1.1 to 1.2 range. This implies that BXMT trades at a discount of around 27% versus its historical valuation today. In other words, if BXMT saw its book value drop by close to 30%, it would be fairly valued. But a book value hit this hard seems unlikely to me, thus shares should have upside potential from the currently depressed level. Over a multi-year time frame, substantial share price gains in addition to the high dividend yield are thus not unrealistic, I believe.

Takeaway

I am a fan of Blackstone (BX) and of Blackstone Secured Lending (BXSL), and BXMT is the third Blackstone entity I’m a fan and shareholder of. At current prices, BXMT is trading inexpensively while offering a huge dividend yield. The company’s credit quality is solid and its floating rate investments provide considerable profit growth tailwinds in the current rates environment. I think BXMT is an attractive investment right here.

Be the first to comment