How The Cloud Looks In Seattle Right Now Massimo Ravera/Moment via Getty Images

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Whither Bears?

The bears are, it seems, temporarily absent, to be found in bear caves gorging on the honey-spoils gathered through the course of 2022. Rather surprisingly they have yet to pounce on Microsoft (NASDAQ:MSFT) stock following a weak Q2 of FY6/23 earnings print yesterday after the close.

We have two simple things to say about Microsoft and its stock.

One, the quarter was dreadful, and no amount of window dressing would persuade us otherwise. That the stock isn’t down more than is the case tells us more about market appetite than it does about Microsoft fundamentals.

Two, the stock did in fact dump rather meaningfully in 2022, and at these prices we believe accumulating a long-term position is likely to work out if your approach is patient and slow, and your liquidity horizon long. It remains the case that Microsoft is likely to grow revenue at above-GDP rates, that its cash flow margins are likely to hold up well, its balance sheet remains a fortress, and we would not bet against CEO Satya Nadella placing winning bets in AI to drive unexpected upside.

So – the punchline here is, we rate at Accumulate, but by that we mean – picking up small allocations of the stock on red days when doom is in the air, with a view to holding for a retirement-account period of time. This is our approach in staff personal accounts. With that, let’s turn to the numbers, the valuation, and the chart.

Fundamentals

Headlines:

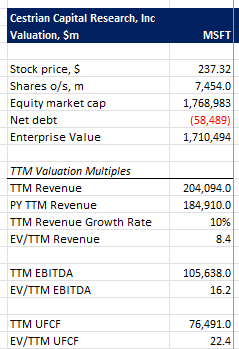

- Quarterly revenue growth slowed to 2% vs prior year, down from a peak of 22% as recently as September 2021.

- TTM revenue growth (the 12 months ending 31 Dec 2022 vs. the 12 months ending 31 Dec 2021) slowed to 10% from a peak of 21% this time last year.

- Gross margins held up at 68% on a TTM basis, nothing to worry about there.

- Unlevered pretax FCF margins fell to 37%, a level not seen since December 2019, a result of weak revenue and also of a large working capital outflow in the quarter. MSFT fiscal Q2 (the quarter just reported) is always weak on cashflow, a result of contract renewal timings, but this was a large outflow. We are looking for a substantial reversal in fiscal Q3 (ending 31 March 2023).

- Balance sheet remains unassailable with $53bn of net cash.

- The value of the order book – the “remaining performance obligation” – stands at around 95% and it’s growing at 27% year on year. This is a solid guide to a comfortable future and a core part of why we believe long-term accumulation is in order.

MSFT Fundamentals (Company SEC filings, YCharts.com, Cestrian Analysis)

The valuation – we’re using the 25 January pre-open price here – is as follows:

MSFT Valuation (Company SEC filings, YCharts.com, Cestrian Analysis)

The cash flow multiple looks a lot due to that working capital outflow, so, we’ll forgive that a little. 16x TTM EBITDA for a 10% TTM grower with that level of order book comfort doesn’t look so bad to us, again, with a long-term view in mind.

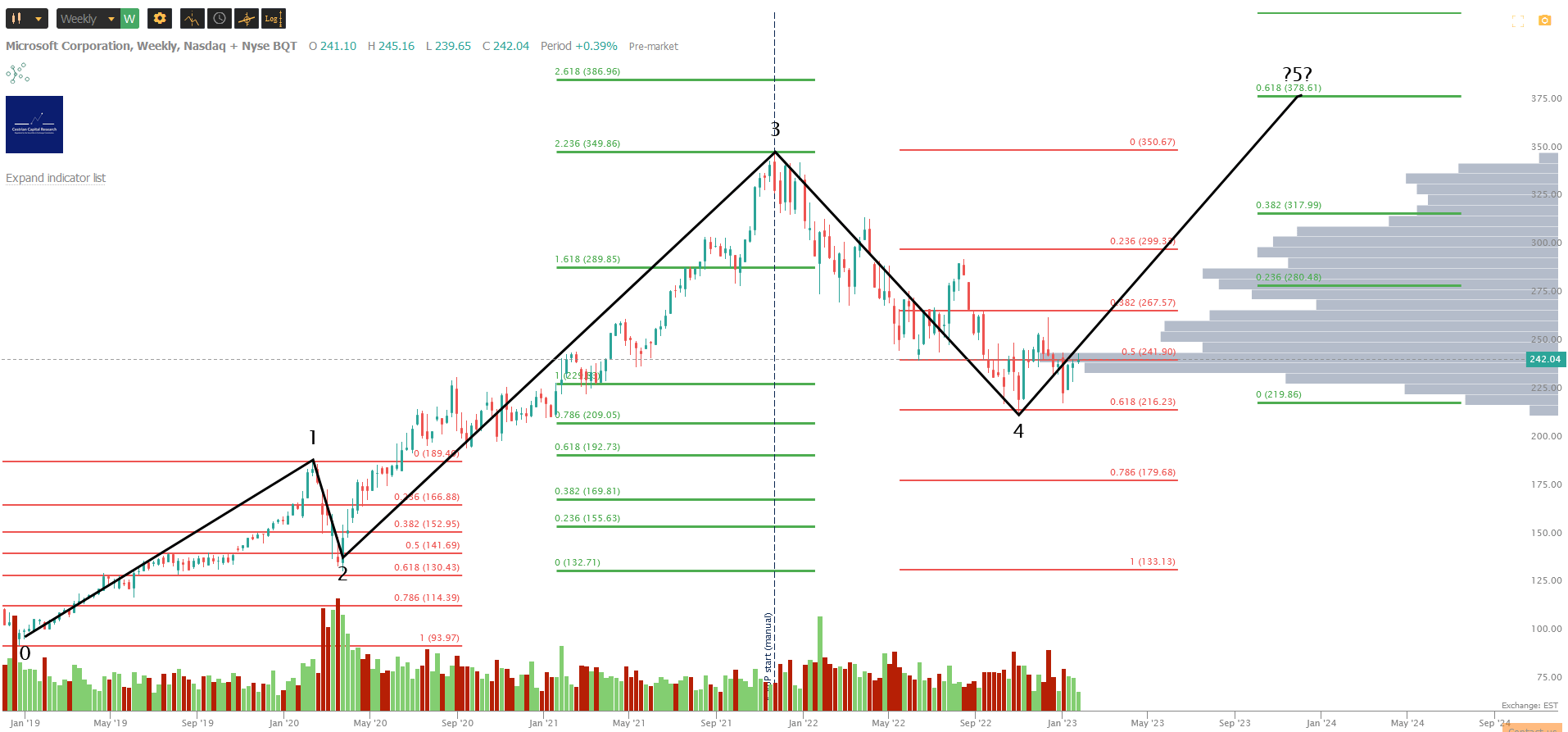

Now the chart – this is the larger degree outlook in our mind. You can open a full page version, here. Take a look at the volume profile on the right hand side – this shows volume traded by price level, and we’ve started the clock at the all-time high so the bars you see there are all since the peak. Look at the high volume nodes in the $236-245 range. That sure looks like institutional accumulation to us.

MSFT Chart (TrendSpider, Cestrian Analysis)

In the short term we anticipate a further selloff in the immediate period, particularly if other tech names report poor quarters. But if you’re adopting the Wyckoff Cycle motif, as we do in our retirement accounts, this is likely to present accumulation opportunities which are not to be feared. You will, as always, make your own decision.

Cestrian Capital Research, Inc – 25 January 2023.

Be the first to comment