sanjeri

Thesis

Macquarie Global Infrastructure Total Return Fund (NYSE:MGU) announced on August 11 that its board of directors approved the reorganization of the fund into Aberdeen Global Infrastructure Income Fund (NYSE:ASGI). MGU belongs to the Macquarie/Delaware Management Company CEF family and it seems that Macquarie is liquidating that business with all the CEFs being merged into Aberdeen funds. What is interesting about MGU is the fact that the fund with an AUM of $315 mm is significantly larger than the fund it is being merged into. ASGI only has $168 mm in assets:

Comparison of Funds (Author)

Both funds trade at significant discounts to NAV currently. Let us have a closer look at the analytics and composition for the two funds so that we can try to understand how the combined entity will look going forward and whether this is a positive for MGU shareholders:

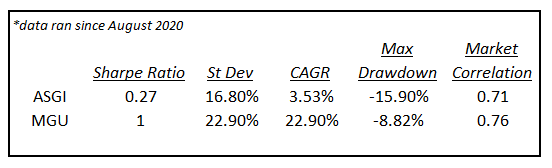

Analytics (Author)

MGU has better analytics across the board – a much higher Sharpe ratio, higher CAGR and a lower drawdown. The only negative for MGU in comparison to ASGI is the fact that it has a higher volatility. We are a bit surprised to see the weak metrics for ASGI given that it is a new fund established in July 2020. This is right as the Covid crisis was happening, resulting in substantially discounted valuations for infrastructure assets. Please remind yourself that in 2020 Heathrow Airport for example saw 73% less passengers than the year before. Now it is in crisis again with more passengers than it can handle! You would think that an infrastructure fund set up in July 2020 would have made a killing, wouldn’t you?

From a holdings perspective MGU is overweight Utilities and Energy Infrastructure while ASGI has a bit of a different focus, with overweight positions in Industrials and Utilities. MGU is up almost +9% year to date versus a small negative performance for ASGI.

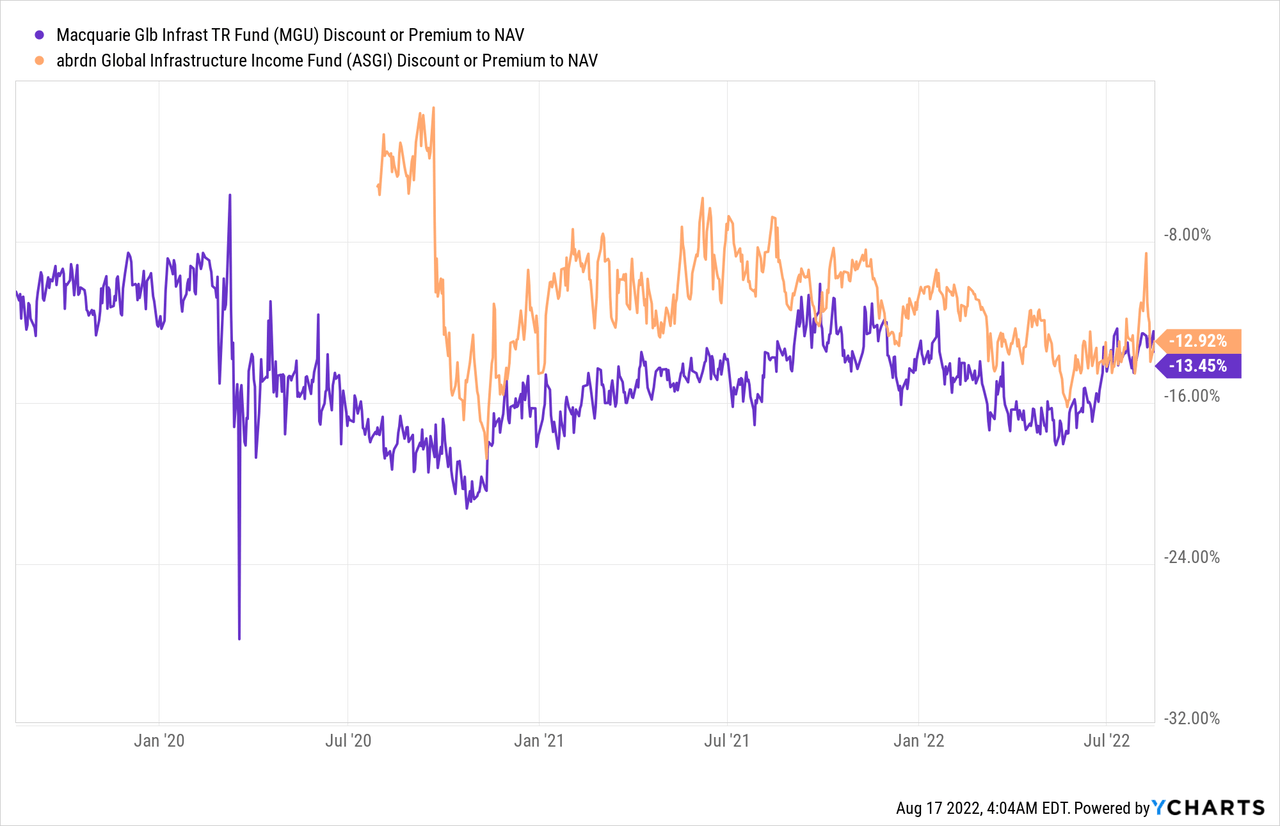

We like the MGU portfolio, track record and analytics better. It seems that ASGI shareholders are getting the better deal here in terms of acquiring a fund that has produced superior results. Both CEFs however trade at similar discounts to NAV:

The only positive we can see for MGU shareholders here is the value obtained from being merged into a platform with a better name. We can see the discount to NAV tightened for MGU from -16.5% levels to the current -13.5%. We would expect the combined platform to tighten further if the performance is commensurate.

Holdings

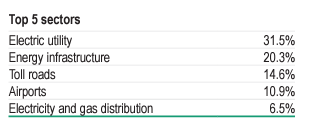

MGU is overweight Utilities and Energy Infrastructure:

MGU Top Sectors (Fund Fact Sheet)

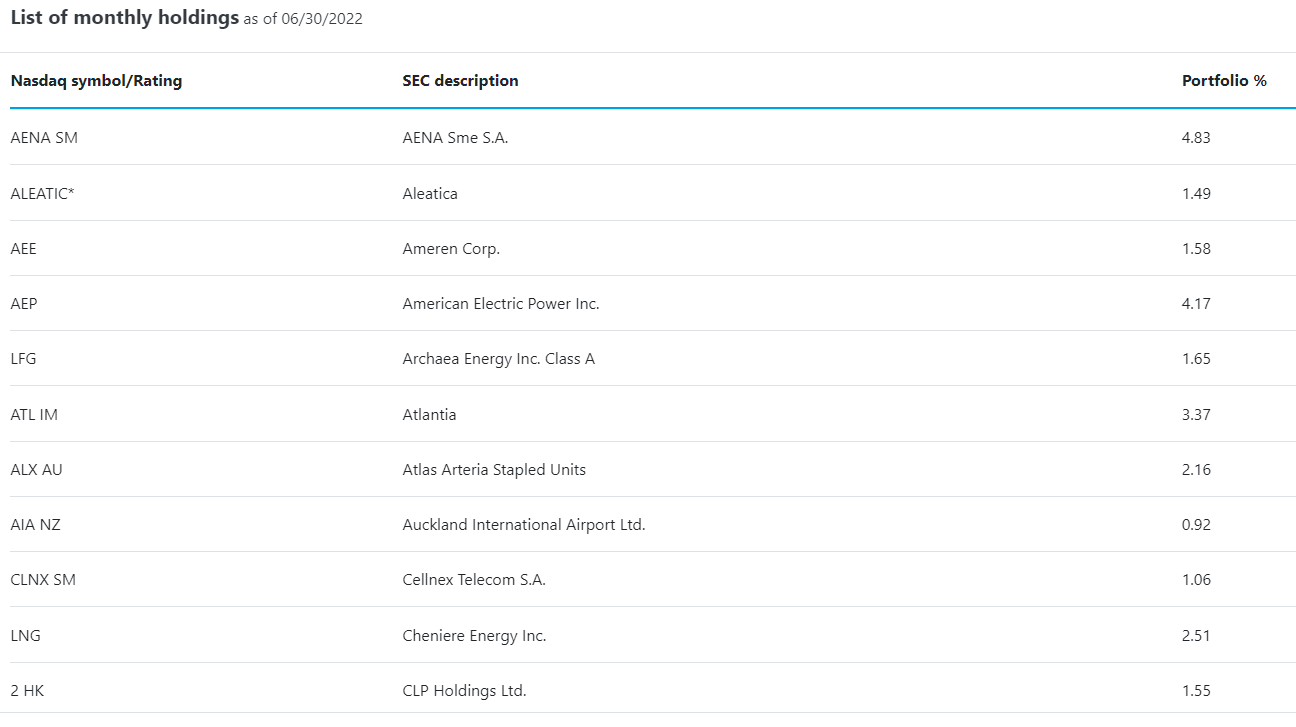

If we take a look at the top MGU holdings we can find the following:

MGU Holdings (Fund Website)

AENA Sme is a Spanish airport management company, Aleatica is a Mexican infrastructure company with a Latam and Europe presence. Per its description Aleatica:

We are focused exclusively on the design and operation of highways and other transportation assets that meet the needs of our customers and improve the quality of life of the communities where we have a presence.

Down the holdings chain we have the likes of Cheniere (LNG), which has seen an explosive stock price growth this year on the back of the European gas crisis and preeminence of LNG as a solution for the shortfalls in natural gas on the old continent.

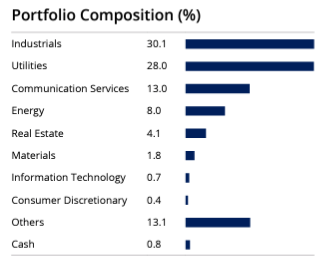

ASGI on the other hand has a bit of a different focus, with overweight positions in Industrials and Utilities:

ASGI Portfolio (Fact Sheet)

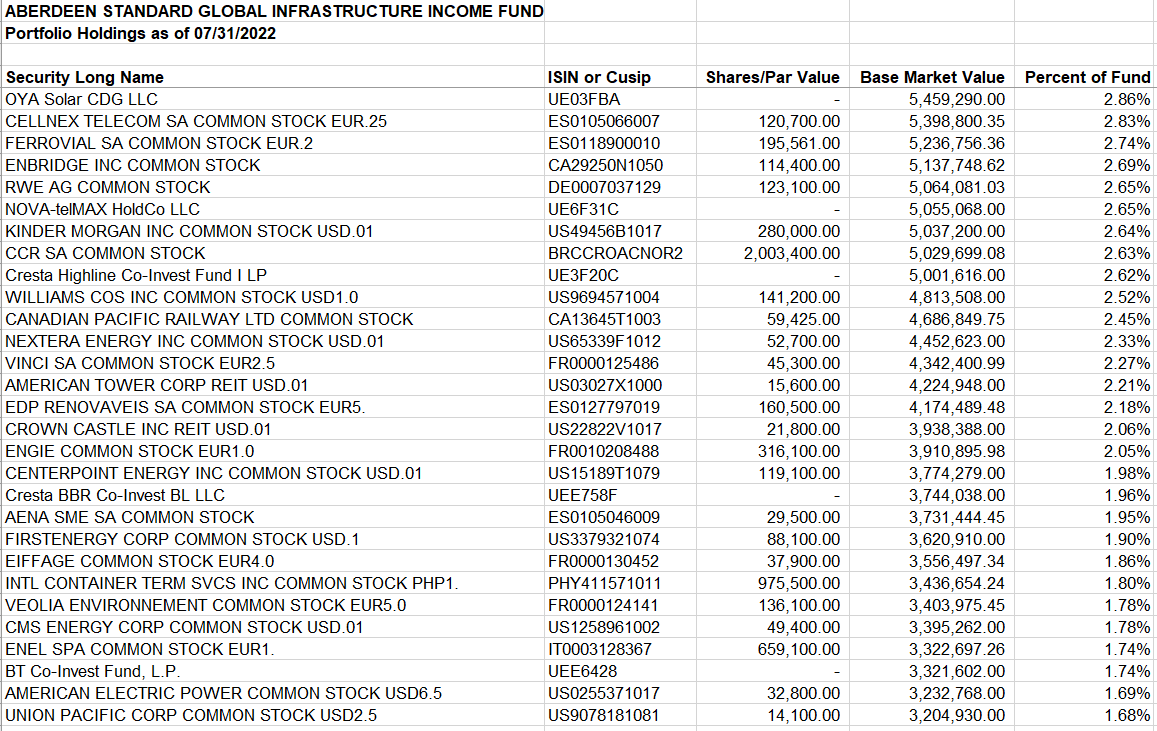

The top holdings for ASGI are as follows:

ASGI Top Holdings (Fund Website)

OYA Solar is a North American renewables company that sits on the private side, Cellnex (OTCPK:CLNXF) is a Spanish wireless telecommunications infrastructure and services company while Enbridge (ENB) is a well known Oil & Gas pipeline company.

Performance

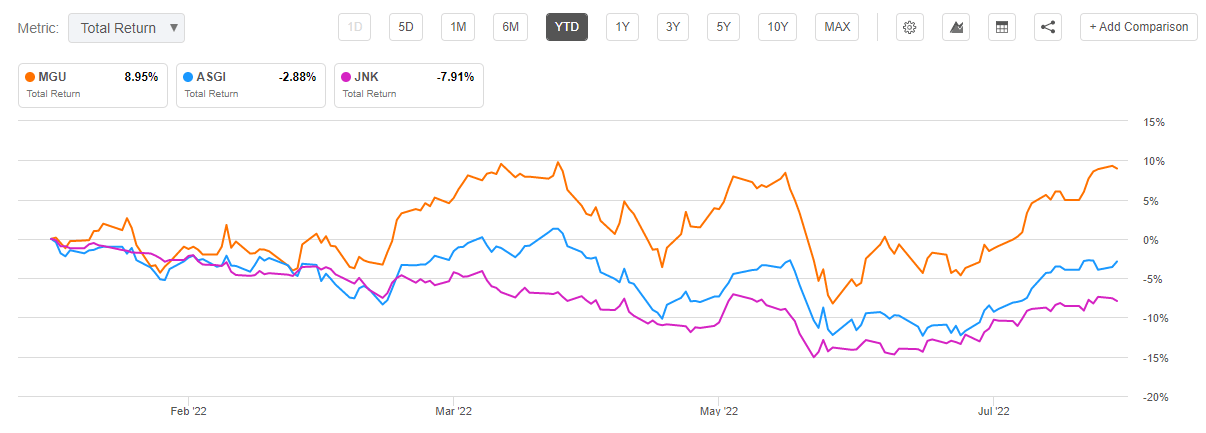

MGU is up almost +9% year to date versus a negative performance for ASGI and JNK:

YTD Performance (YTD)

This performance is due to MGU being overweight Utilities and Energy Infrastructure, sectors which have seen a very strong performance in 2022.

The performance is similar when looking on a 3-year basis as well:

3-Year Performance (Seeking Alpha)

Please note that ASGI is a new fund, having been established in July 2020.

Conclusion

The Macquarie/Delaware Management Company is liquidating its CEF management business. The Macquarie Global Infrastructure Total Return Fund Inc announced on August 11 that its board of directors approved the reorganization of the fund into Aberdeen Global Infrastructure Income Fund. Both are infrastructure funds, but with different focuses. MGU is overweight Utilities and Energy Infrastructure while ASGI has overweight positions in Industrials and Utilities. MGU is the fund with the much better track record and analytics. Overall ASGI seems to get the better deal here by absorbing a bigger fund with a better historical performance. MGU shareholders have benefited only marginally from the merger (still to be approved by shareholders) by being absorbed into a better name platform. The announcement resulted in a slight 3% narrowing of the discount to NAV for MGU.

Be the first to comment