Zach Gibson/Getty Images News

Thesis

I really envy Mark Zuckerberg’s job, at least before 2022. Meta Platforms (NASDAQ:META) enjoyed dominance in the social media and digital ad space, generating so much cash that the CEO’s capital allocation decisions, half of a CEO’s job, are made really simple. As recent as 2019-2020, META generated on average $38B of operating cash per year, was debt-free, and its maintenance CAPEX was only about $6.8B. And all of these left Zuckerberg a pool of disposable cash, more than $30B per year, to allocate.

The picture changed dramatically in 2022. Operating income fell sharply from a peak of $46.7B in 2021 to $39.8B (a 15% decline) TTM 2022. At the same time, both CAPEX and R&D expenses soared as the company aggressively bets on the metaverse future. CAPEX increased from $18.5B in 2021 to $22.6B TTM 2022, a hike of more than $4.1B. R&D expenses increased from $24.6B in 2021 to $29.8B TTM 2022, a hike of more than $4.2B. As a result, it has been burning cash from both ends. Its cash stockpile peaked at more than $60.6B by the end of 2020 and currently stands at $40.4B, a decline of more than $20 in about a year and a half.

Going forward, Zuckerberg’s capital allocation ability will be put to test. He obviously will have to work under less flexibility. At the same time, META will also have to work with the debt market and has just debuted its $10 billion bonds issuance recently. He will also have to strike a better balance between near-term issues and long-term high-risks bets.

Overall, I see Zuckerberg as an effective executive to lead META to navigate through these issues, as detailed next.

Zuckerberg’s scorecard

Despite all the issues META has been facing lately, Zuckerberg has been an extremely effective executive in my opinion, and has delivered extraordinary returns for shareholders over the long term. Putting subjective opinions aside, here let’s apply Buffett’s subjective $1 test on Zuckerberg. The $1 test was promoted by Buffett himself and the gist is summarized in his 1984 shareholder letter (the highlighted was added by me):

“Unrestricted earnings should be retained only when there is a reasonable prospect – backed preferably by historical evidence or, when appropriate, by a thoughtful analysis of the future – that for every dollar retained by the corporation, at least one dollar of market value will be created for owners. This will happen only if the capital retained produces incremental earnings equal to, or above, those generally available to investors.”

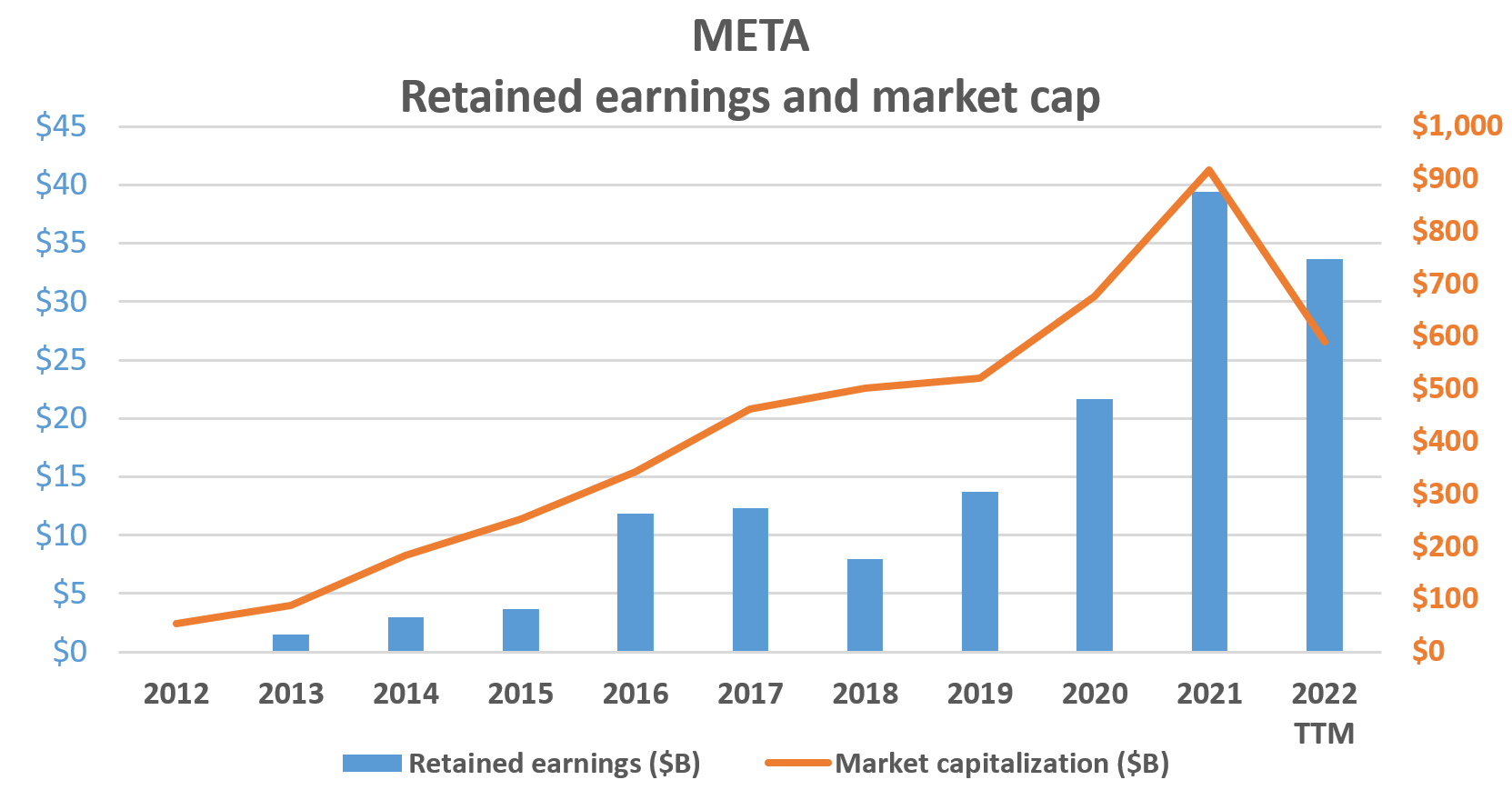

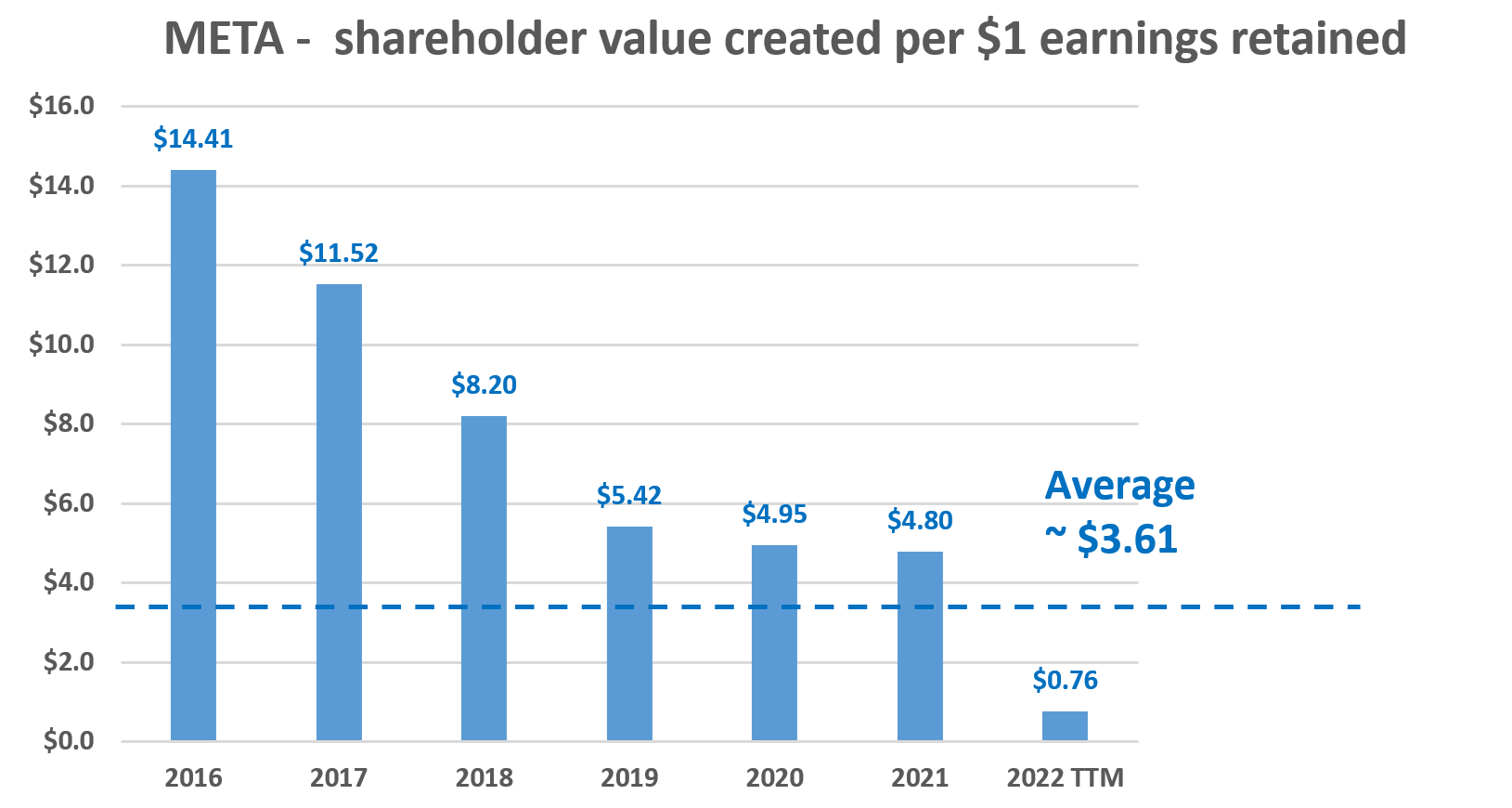

The first chart below shows the annual market cap (“MC”) of META and the amount of retained earnings since 2012. And the second chart shows the shareholder value created by every $1 of retained earnings. Note I applied a 5-year average in the second chart to even out YoY noises. As seen, Zuckerberg has passed the test with flying colors. The business has created an average of $3.6 of MC for every dollar retained. Even with its early explosive years (2016 to 2018) excluded, Zuckerberg managed to deliver more on average $5 of shareholder returns per dollar retained from 2019 to 2021.

Obviously, the concern came in 2022. As you can see, META’s market cap plummeted from over $900B in 2021 to about $600B in 2022 (note here I am using annual average share prices to filter out short-term volatilities). Such a plunge has also changed Zuckerberg’s score from A+ to failing. For every dollar of retained earnings, he only delivered $0.76 of shareholder return in 2022.

And next, we will see the challenges and opportunities for him to turn the score around.

Author Author

Debt issuance for first time

Firstly, META decided to work with the debt market. It decided to issue a $10B jumbo bond deal for the first time in its history, and the details are quoted below from a Bloomberg report (slightly edited by me):

- The social-media giant has been one of just 18 companies in the S&P 500 without debt.

- The deal comes in four parts, Bloomberg reports; a 40-year portion will yield 1.65 percentage points above Treasury’s, down from previous expectations for 1.75-1.8 points.

- Orders for the bonds hit more than $30B.

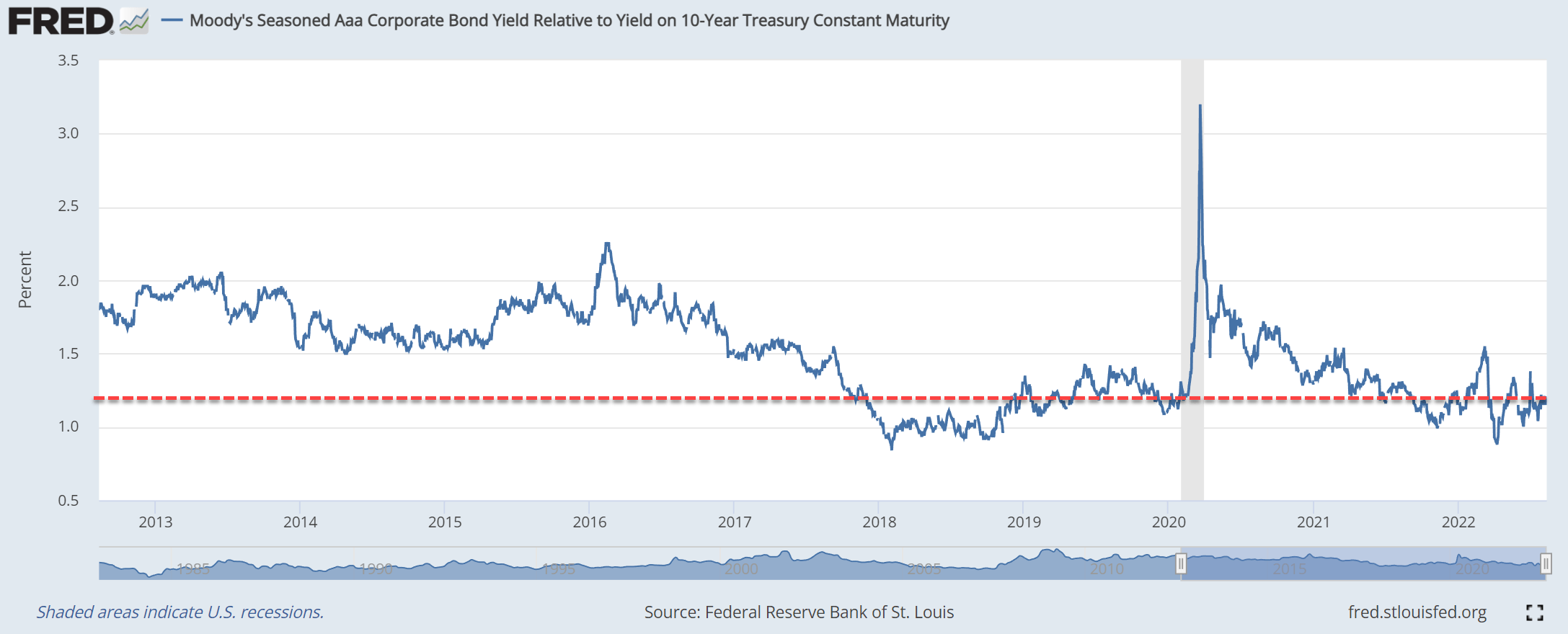

I am not against issuing debt in any way, and I see this decision from Zuckerberg as a very shrewd move at a well-chosen timing. The following chart shows Moody’s seasoned Aaa corporate bond yield relative to the 10-year treasury constant maturity yield. As you can see, right now, the yield spread is near a historical low, only at about 1.2% above 10-year treasury rates. Furthermore, the bond market’s overwhelming responses show investors’ confidence in the company’s profitability in the long term.

FRED

Zuckerberg’s R&D challenges ahead

Compared to debt issuance, Zuckerberg’s challenges to better balance long-term R&D needs and near-term profitability are more fundamental in my view. The next chart shows a variation of the above Buffett’s $1 test on R&D expenses.

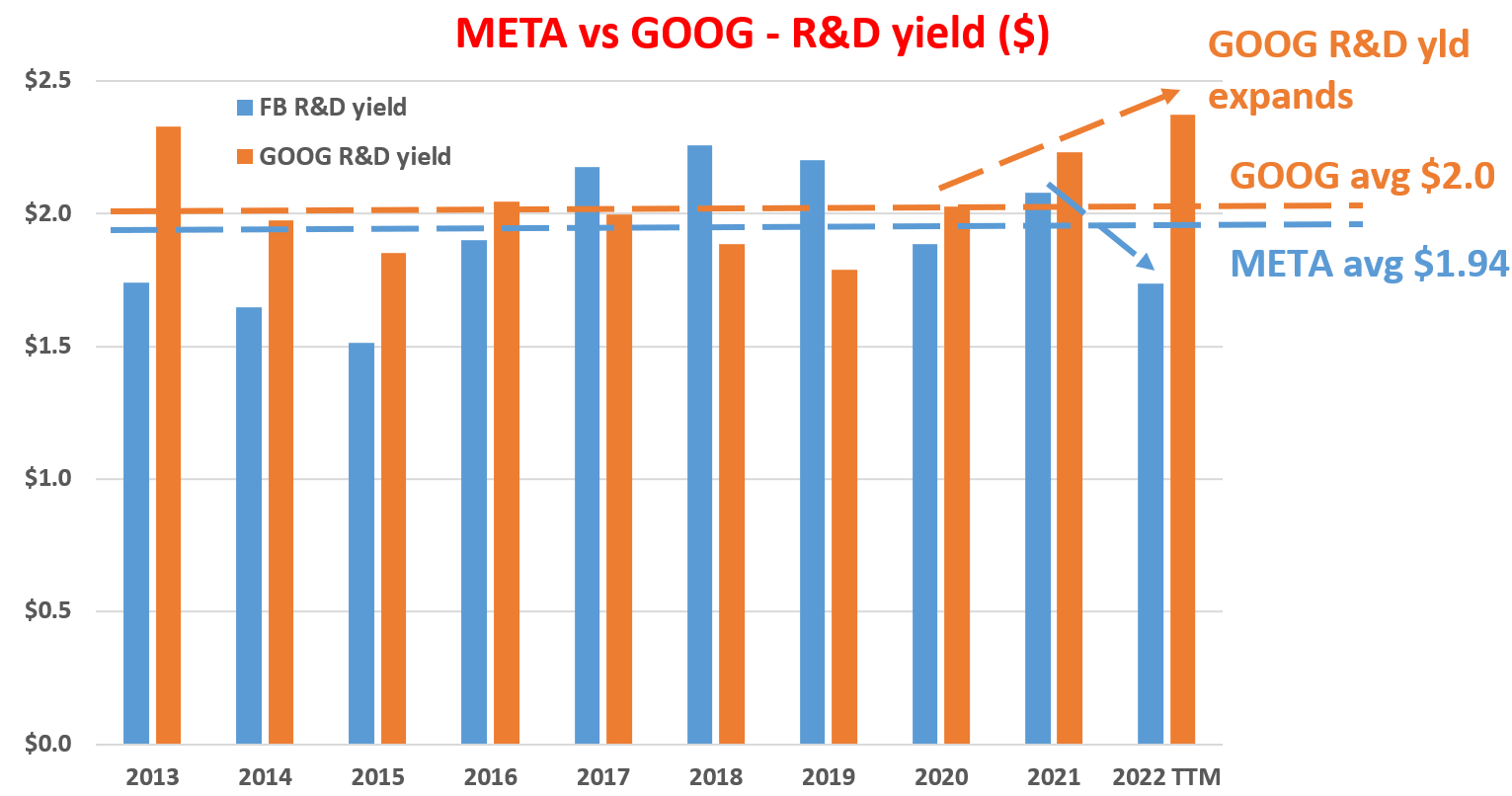

The chart measures the operating cash flow generated by every $1 of R&D expenses (just like the original Buffett’s test measured the MC created by every $1 of retained earnings). Furthermore, the chart compares META’s R&D yield against its closest peer in the digital ad space, Google (GOOG) (GOOGL). Note that I applied a 3-year moving average here to represent a typical 3-year R&D lifecycle.

As you can see, both META and GOOG have also passed this $1 test with flying colors. The R&D yields for both of them have been on average $2.0 in the long term ($2.0 for GOOG and $1.94 for META). However, the concern here is again the trend in recent years. GOOG’s R&D yield has been on an expanding trajectory since 2019, expanding from a lower-than-average level in 2019 to the current level of $2.4, 20% above its historical average. META, in contrast, has seen its R&D yield shrink from $2.1 in 2021 to $1.7 TTM 2022.

A primary reason behind such divergences involves META’s aggressive bets on futuristic metaverse technologies. Its Q2 R&D increased 43% YoY, mainly due to Reality Labs and its family of apps. Reality Lab currently suffers operation losses in the $2B to $3B range over the past few quarters. There is no clear sign for it to become profitable in the near future.

Author

Final thoughts and other risks

Going forward, I see plenty of short-term headwinds for Zuckerberg and META investors. Data privacy concerns (especially the privacy changes to Apple’s iOS system) and intensified competition will keep pressuring its margin. And its futuristic bets on metaverse won’t begin to contribute in any meaningful ways for years.

Expanding the horizon to the longer term, there are plenty of reasons to be optimistic too (as many other SA authors have already eloquently argued). In this article, I just wanted to add one more argument: Zuckerberg. I see Zuckerberg as an effective executive both based on his past scorecard and his ongoing capital allocation decisions.

Besides the specific risks META faces, there are also macroeconomic risks and geopolitical risks. There is a realistic chance for a recession or a major economic slowdown in the near future. Advertising budgets could suffer a dramatic tightening should this occur. At the same time, sadly, the Russian/Ukraine war continues and has no end date in sight, which further compounds the macroeconomic uncertainties.

Be the first to comment