As we have discussed in the past, Meta Platforms, Inc. (NASDAQ:META) is experiencing heightened business volatility due to a challenging macro environment, Apple’s (AAPL) platform policy changes, Mark Zuckerberg’s metaverse ambitions, and a massive executive leadership turnover. These factors are hurting both the top and bottom lines of the social media/digital advertising giant, as evidenced by recently released Q2 numbers.

In today’s note, we will briefly discuss Meta’s Q2 report (focus will be on positives) and study its technical chart once again. For the purpose of brevity, I will skip the valuation bit; however, if you are interested in my valuation for Meta and my detailed investment thesis for the company, I urge you to read the following note before moving forward in this article:

Alright, let’s dive straight into Meta’s Q2 numbers now.

Meta’s Q2 Earnings Review

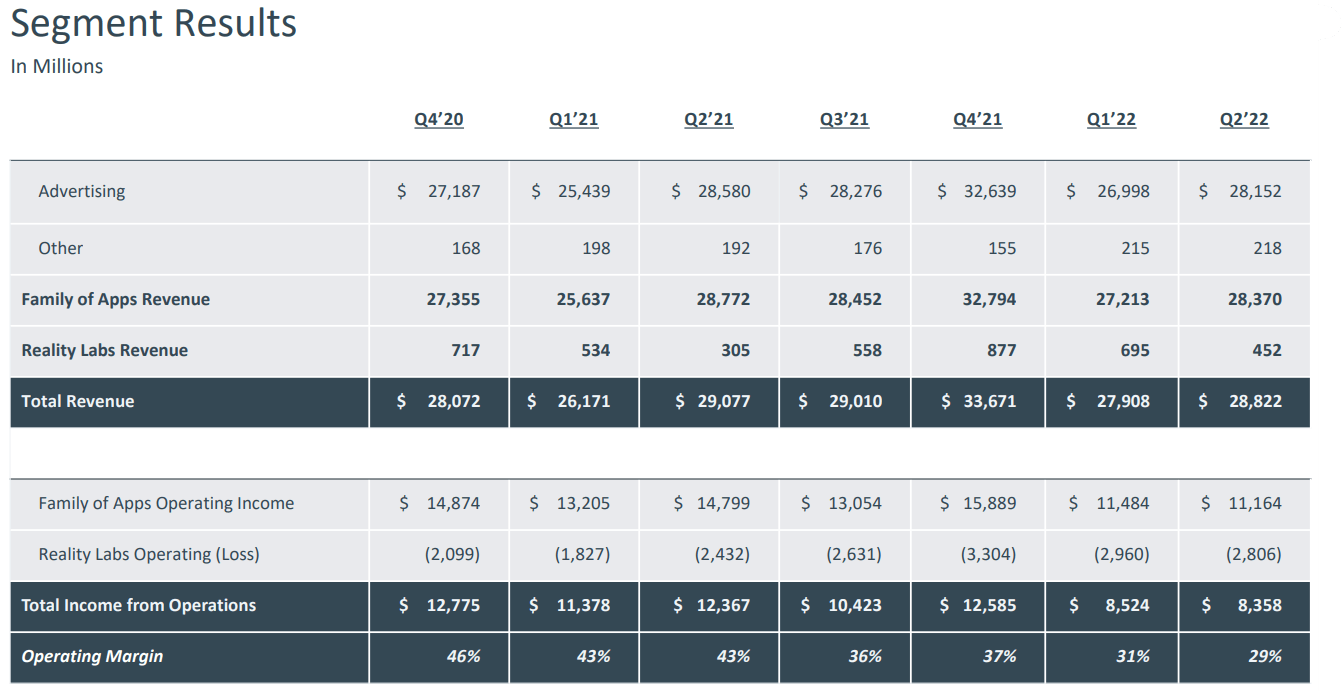

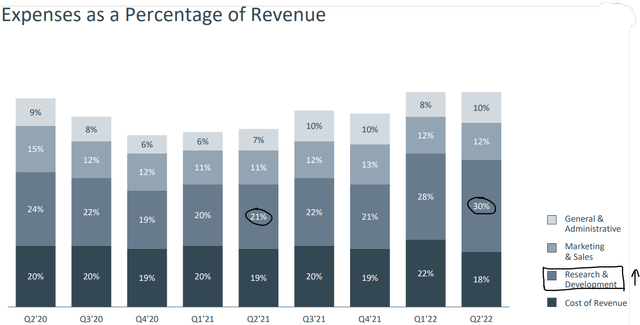

In Q2 2022, Meta’s revenue decreased (-1% y/y) for the first time in its history as a public company, whilst operating income fell by -32% y/y. As you can observe from its financial data, Meta’s operating margins are getting squeezed (down from 43% in Q2 2021 to 29% in Q2 2022) due to heightened R&D spending in the Family of Apps and Reality Labs divisions.

Meta Q2 Earnings Presentation

Meta Q2 Earnings Presentation

Macro headwinds coupled with Apple’s IDFA changes are driving a decline in Meta’s ad prices; however, this decline was somewhat offset by higher engagement (ad impressions) in Q2. As you may know, Reels’ growth is cannibalizing other ad surfaces across Facebook and Instagram; however, management’s positive commentary on Reels’ net impact on user engagement and long-term monetization potential was heartening.

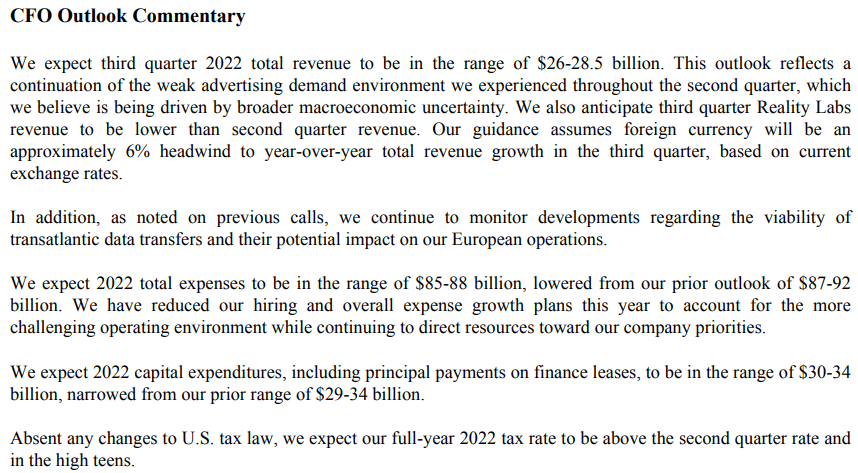

With that said, management’s sales guidance for Q3 ($26-$28.5B) came in ~10% below Street estimates, and this tells me that the worst may not be over yet. Here’s what Meta’s outgoing CFO had for us:

Meta Q2 Earnings release

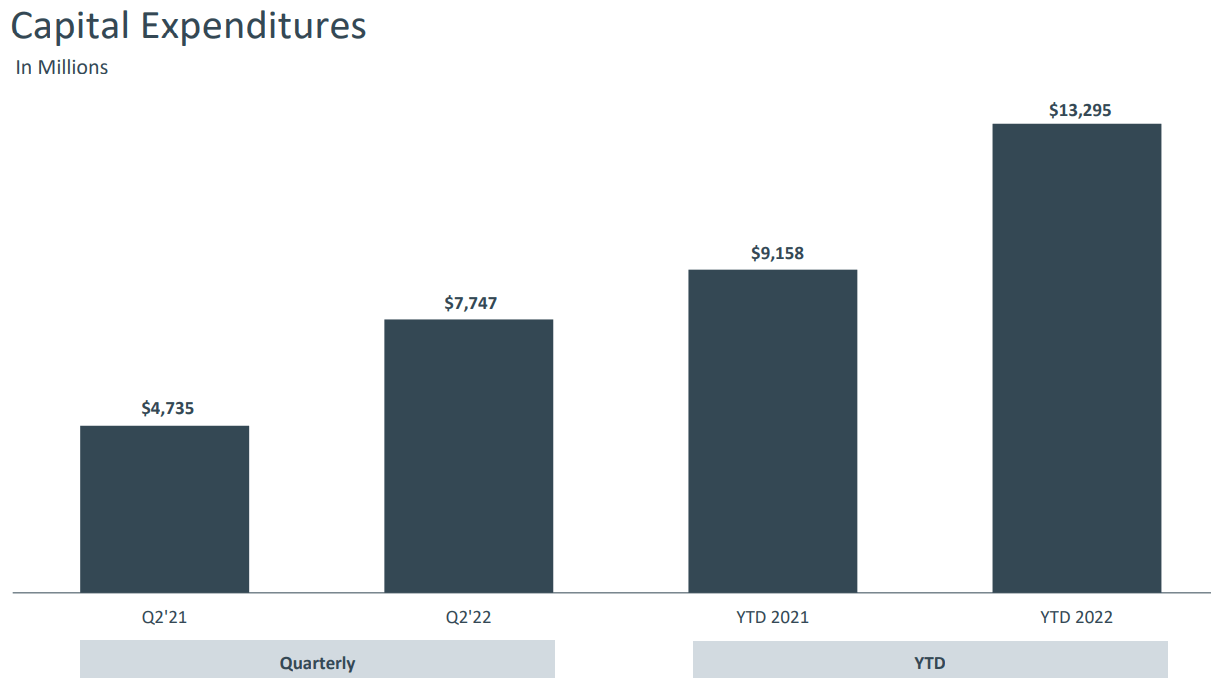

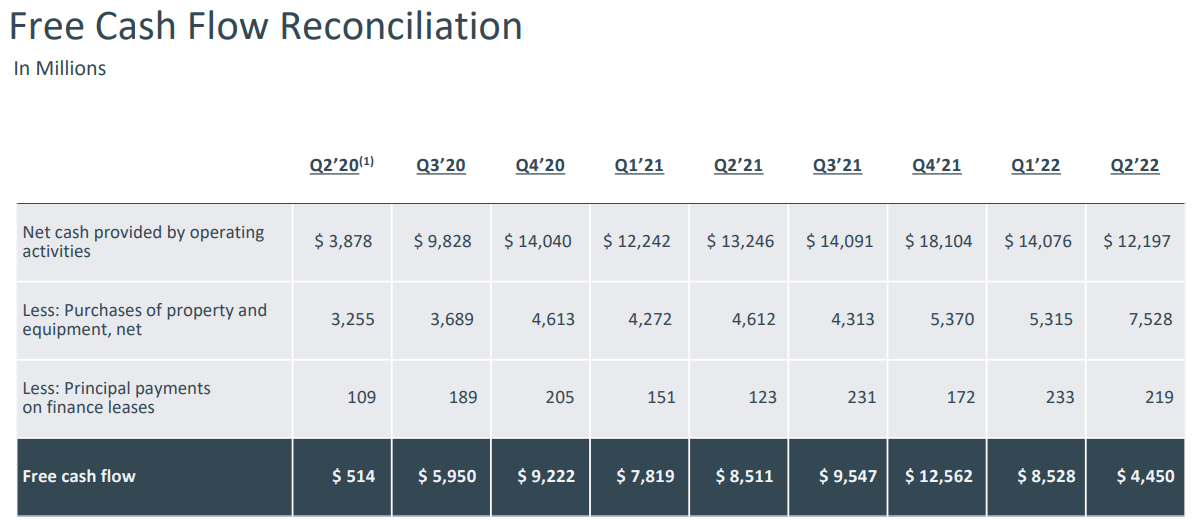

Increased AI compute CAPEX spending is causing a dent in Meta’s free cash flow generation (along with a massive slow-down in revenue growth). Meta’s management is cutting some expenses; however, free cash flows may remain under pressure over the next few quarters.

Meta Q2 Earnings Presentation

Meta Q2 Earnings Presentation

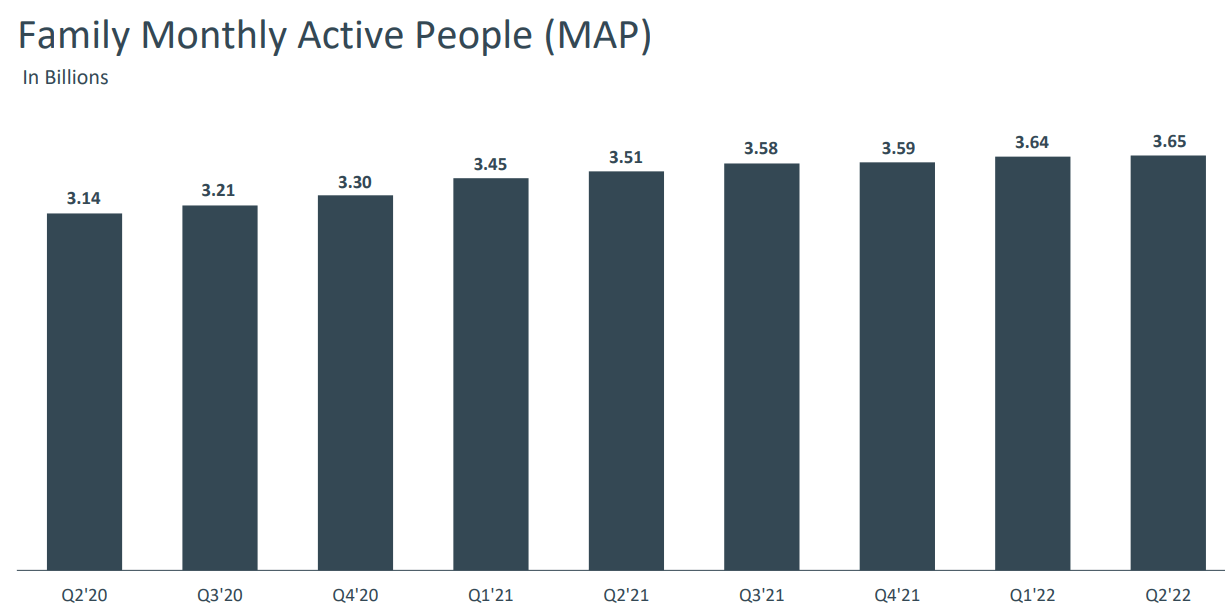

While I think it is fair to assume that Meta’s financial performance will worsen in the coming quarters, comments like “Meta is the next General Electric (GE)” are simply premature. Despite all the headwinds in 2022, Meta’s user base (3.65B MAUs across Family-of-Apps) is still growing, and so is user engagement across its platforms. Furthermore, the potential monetization of WhatsApp leaves tons of revenue upside. And we are not even considering the potential of Metaverse, which Mark Zuckerberg believes could be worth billions (or even trillions) of dollars.

Meta Q2 Earnings Presentation

On the other side of these turbulent economic times, the digital ad spending market should continue to grow, and Meta’s position in this market is still dominant. In the past, Meta has endured such recessionary environments with aplomb (re-built their advertising platform in 2008-09), coming out a stronger company on the other side. Mark Zuckerberg expressed a similar view on this crisis during the Q2 earnings call, and given his past performance record, I am happy to bet on Mr. Zuckerberg to get Meta through to the other side of this cycle, a stronger company. FYI, Zuckerberg sounded bullish on Meta’s business for the first time in several quarters. In my view, Reels’ engagement data, coupled with Meta’s progress on an AI-based discovery engine, is driving this bullishness. Little to no mention of TikTok was another positive change from Meta’s previous call, and I believe that Meta’s management is now confident in their product roadmap to compete with TikTok (and other competitors).

Meta’s financial performance may get worse before it gets better, and investors will need to stay patient in this counter. However, a low starting valuation coupled with Meta’s robust share buyback program puts a high floor on the stock, creating a setup similar to Apple of 2012-13. I have a kitchen sink feel regarding Meta’s Q3 guidance, which makes me wonder if the stock has already bottomed out. However, let’s take a look at Meta’s technical charts for some guidance.

Technicals Support A Long-Term Buy

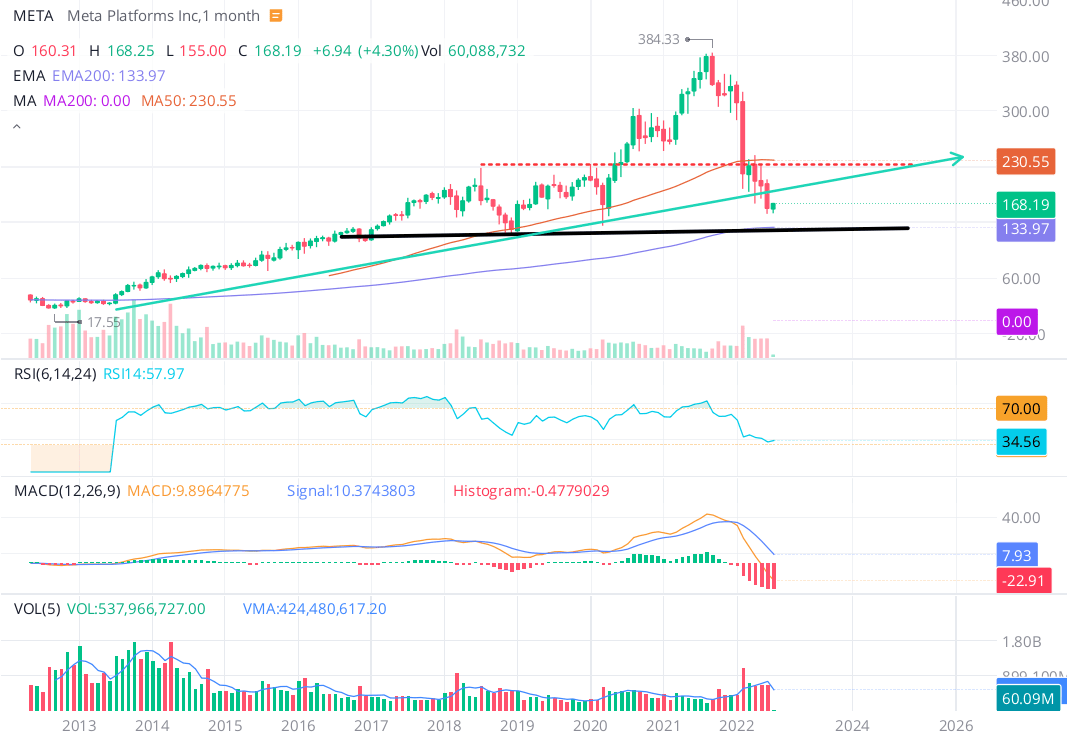

Back in early July, I made the following comments about META’s technical setup:

There is no space for indecision at TQI; however, Meta’s technical charts tell me that the stock is currently trading in no-man’s land. After sliding through its long-term bullish trendline (marked in a green arrow on the chart), Meta’s stock is trying to bounce back up.

WeBull Desktop

With this being said, Meta’s technical chart is broken (the business is not), and it could easily test the $133 support zone, which also happens to be Meta’s 200-EMA level. Hence, if you are looking for a near-term play, skip Meta. However, if you are looking for a long-term play, Meta is a fantastic buy.

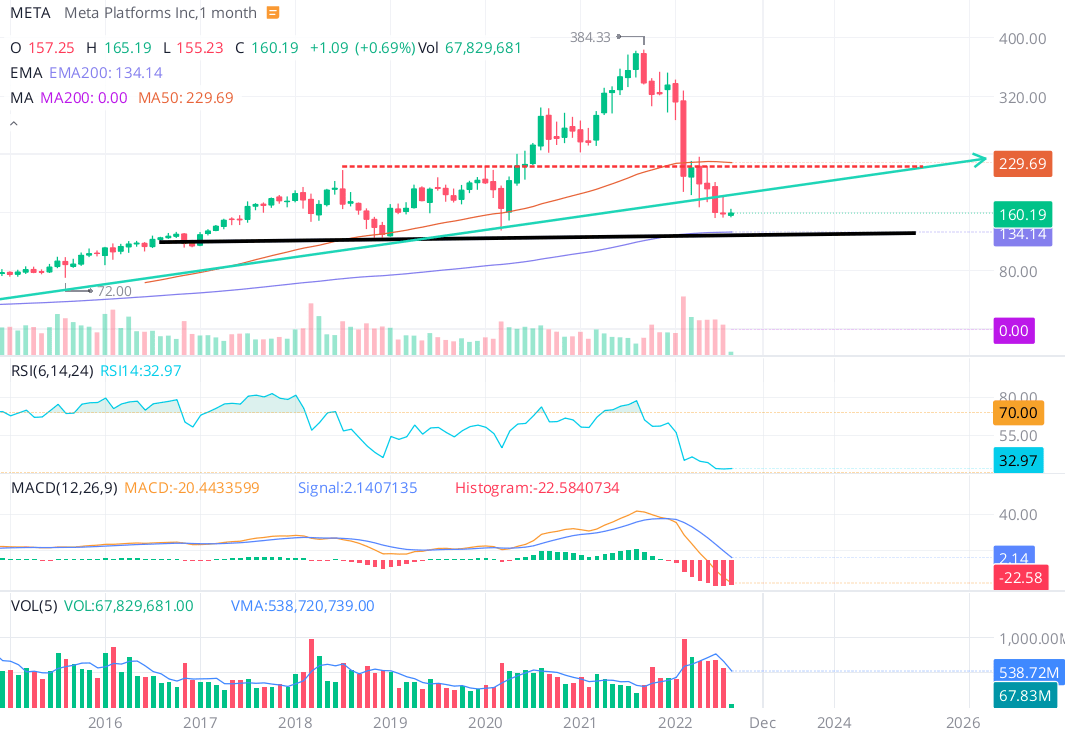

Let’s see how the chart has evolved over the last three weeks:

WeBull Desktop

After the rejection of a bounce to ~$185 (the long-term bullish trendline marked in green), Meta’s stock is once again trading right above the $155-$160 support level. The Q2 earnings report, combined with a weak outlook for Q3, could leave Meta in the penalty box in the near term. Technically, a swing down to the multi-year support zone in the $130-$135 range is still on the table; however, I think this would only happen if we were to suffer a deep recession. As a short-term play, I would still avoid Meta.

YCharts

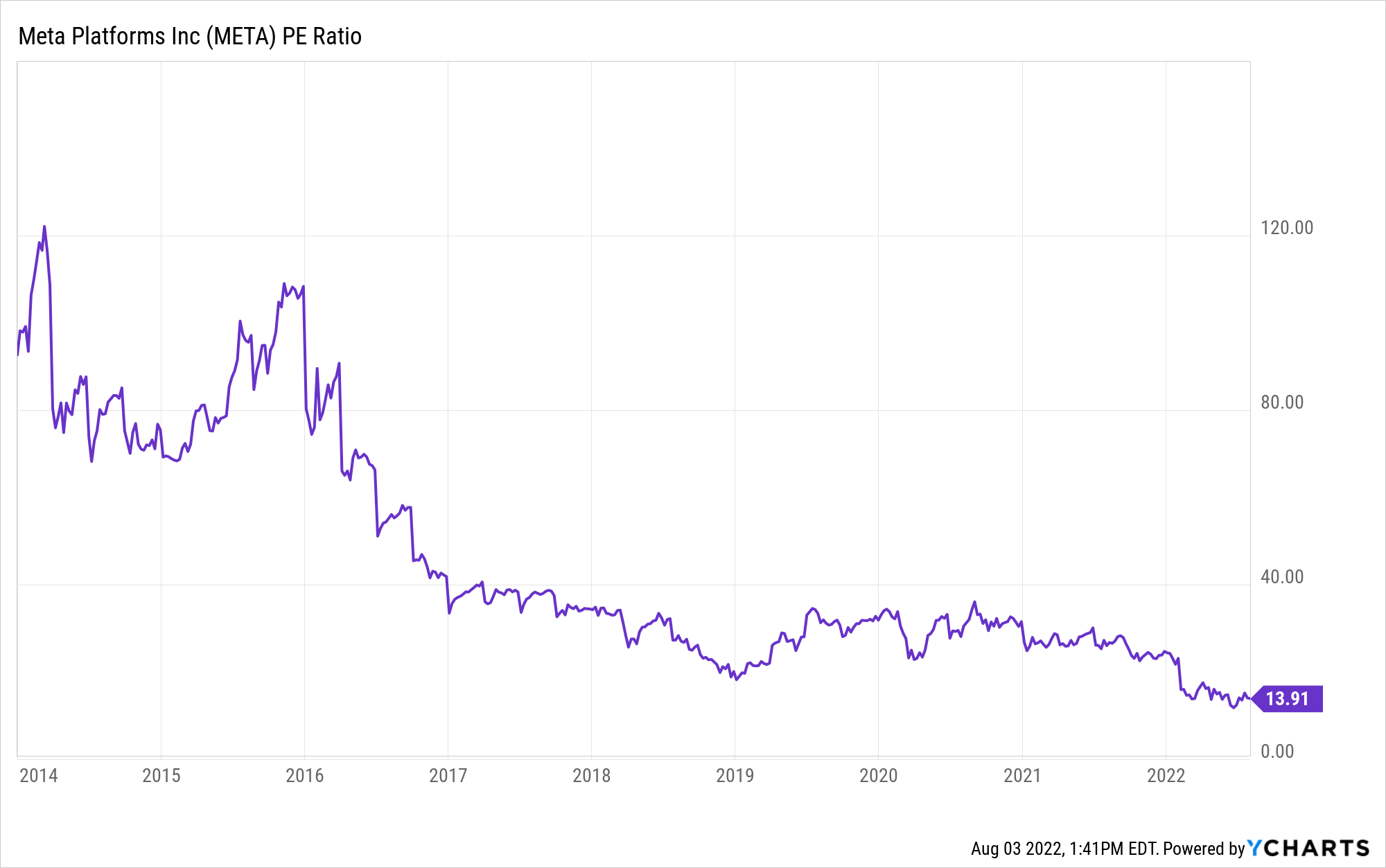

From a long-term investors’ perspective, Meta is offering a fantastic entry point (the stock has never been cheaper based on trading multiples). According to my model, Meta’s fair value is ~$260 per share, and an investor buying in at these levels could expect to generate 25%+ CAGR returns until the end of 2026.

Concluding Thoughts

Meta’s Q2 earnings report was disappointing, but not all that surprising. As I see it, the weakness in Meta’s financial performance is temporary, and even during this challenging period, it remains a cash cow. While near-term headwinds may persist for the next two to four quarters, Meta’s stock seems to have priced in this weakness (and a bit more). Considering Meta’s business performance in a challenging environment and its current valuation, the risk/reward is highly favorable for long-term investors.

Key Takeaway: I rate META a strong buy in the $160s.

Housekeeping Note: I’ll soon launch a Marketplace service on Seeking Alpha focused on generating long-term outperformance through financial engineering. For a short period post-launch, “The Quantamental Investor” will be offered at a heavily discounted legacy price. Stay tuned for more updates!

Thanks for reading, and happy investing. Please share your thoughts, questions, or concerns in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment