Tatiana Antonenko

Introduction

Investors are worried that Meta (NASDAQ:META) is pouring too much capital into metaverse investments, such that little is being returned to shareholders. Management says they’re returning capital to shareholders with buybacks, but the timing has been bad. Looking at the trailing-twelve-month (“TTM”) buybacks of $41.2 billion, the average price was higher than what we see today. Also, many contend that the buybacks merely offset share-based compensation (“SBC”) as opposed to reducing the share count. My thesis is that Meta should appease investors who are concerned about capital allocation by committing to a small annual dividend – perhaps $4 billion or about 10% of the TTM buybacks.

Buyback Concerns

The cash flow statement shows trailing-twelve-month (“TTM”) buybacks of $41.2 billion or $21,093 million + $44,537 million – $24,476 million, but this doesn’t return much to investors as the share price has come down since that time. Also, many say these buybacks are more about offsetting SBC dilution than reducing the share count. A November 9th buyback article by Ben Hunt [@EpsilonTheory] says that Google and Meta transferred more than $300 billion from shareholders to employees in their monetization of stock-based comp over the past ten years.

Mr. Hunt breaks down the Meta part of this as $95.8 billion in buybacks to offset SBC dilution along with $23.1 billion in related taxes for a total consideration of nearly $119 billion over 10 years.

Metaverse Concerns

Reality Labs operating losses are $9,438 million for 9M22. Adding the $10,193 million losses from 2021 and the $6,623 million losses from 2020, the cumulative operating losses in this area from January 2020 to present are the prodigious sum of $26,254 million. Again, investors would feel better about these enormous metaverse bets if a small dividend of $4 billion or so per year was returned to them.

Concerns With Reels

Currently, the Reels segment is less profitable than Feed or Stories such that investors worry about less capital being generated from advertising while metaverse investments remain high. Combining Facebook Blue and Instagram, the revenue run rate of Reels is now $3 billion per the 3Q22 call. Also, it is currently less efficient than other ad options, such that the opportunity cost is $500 million per quarter while management works to turn this from a headwind to a tailwind. A September 12th WSJ article caused concern for investors as it said there is a great deal of work to be done with IG Reels. The news from the article isn’t all bad; IG Reels and TikTok can be complementary, as visually appealing content can do better on IG. The article says the IG audience is older with more disposable income such that they are more appealing to direct response advertisers, whereas TikTok is more like YouTube where brand advertising is effective. The stats the article cites from an internal Meta doc are worrisome:

Instagram users cumulatively are spending 17.6 million hours a day watching Reels, less than one-tenth of the 197.8 million hours TikTok users spend each day on that platform, according to a document reviewed by The Wall Street Journal that summarizes internal Meta research. The document, titled “Creators x Reels State of the Union 2022,” was published internally in August. It said that Reels engagement had been falling-down 13.6% over the previous four weeks-and that “most Reels users have no engagement whatsoever.”

Surely, CEO Zuckerberg was made aware of the above WSJ article, and he said some things in the 3Q22 call that can mollify investors with respect to Reels:

There are now more than 140 billion Reels plays across Facebook and Instagram each day. That’s a 50% increase from 6 months ago. Reels is incremental to time spent on our apps. The trends look good here, and we believe that we’re gaining time spent share on competitors like TikTok. Over time, I expect a few things to set our products apart here. First is that our discovery engine work allows us to recommend all types of content beyond Reels as well, including photos, text, links, communities, short- and long-form videos and more. Second is that we can mix this content along posts – alongside posts from your family and friends, which can’t be generated by AI alone. And third is more social interactions move to messaging. We’re developing a flywheel between discovery and messaging that are going to make these apps stronger. On Instagram alone, people already reshare Reels 1 billion times a day through DMs.

Valuation

A November 9th message from CEO Zuckerberg revealed that Meta is reducing the size of their team by more than 13,000 employees. Layoffs will come from both the cash generating family of apps teams and the cash consuming Reality Labs teams:

While we’re making reductions in every organization across both Family of Apps and Reality Labs, some teams will be affected more than others.

It is unsettling not seeing the breakdown of these layoffs, as they can have a big impact on valuation.

There was a question about Apple charging for social media boosts in the 3Q22 follow-up call, but CFO David Wehner didn’t seem to think it is material for the upcoming financials:

And then, Mark, specifically on boost, we’re evaluating that impact, but we don’t expect it to materially impact our guidance on both Q4 and 2023. We’re obviously disappointed to see Apple kind of claiming a share of advertising revenue, and it’s an important tool for small businesses, but this impacts a relatively small percentage of revenue for us. So, it’s not going to impact our guidance on ’23.

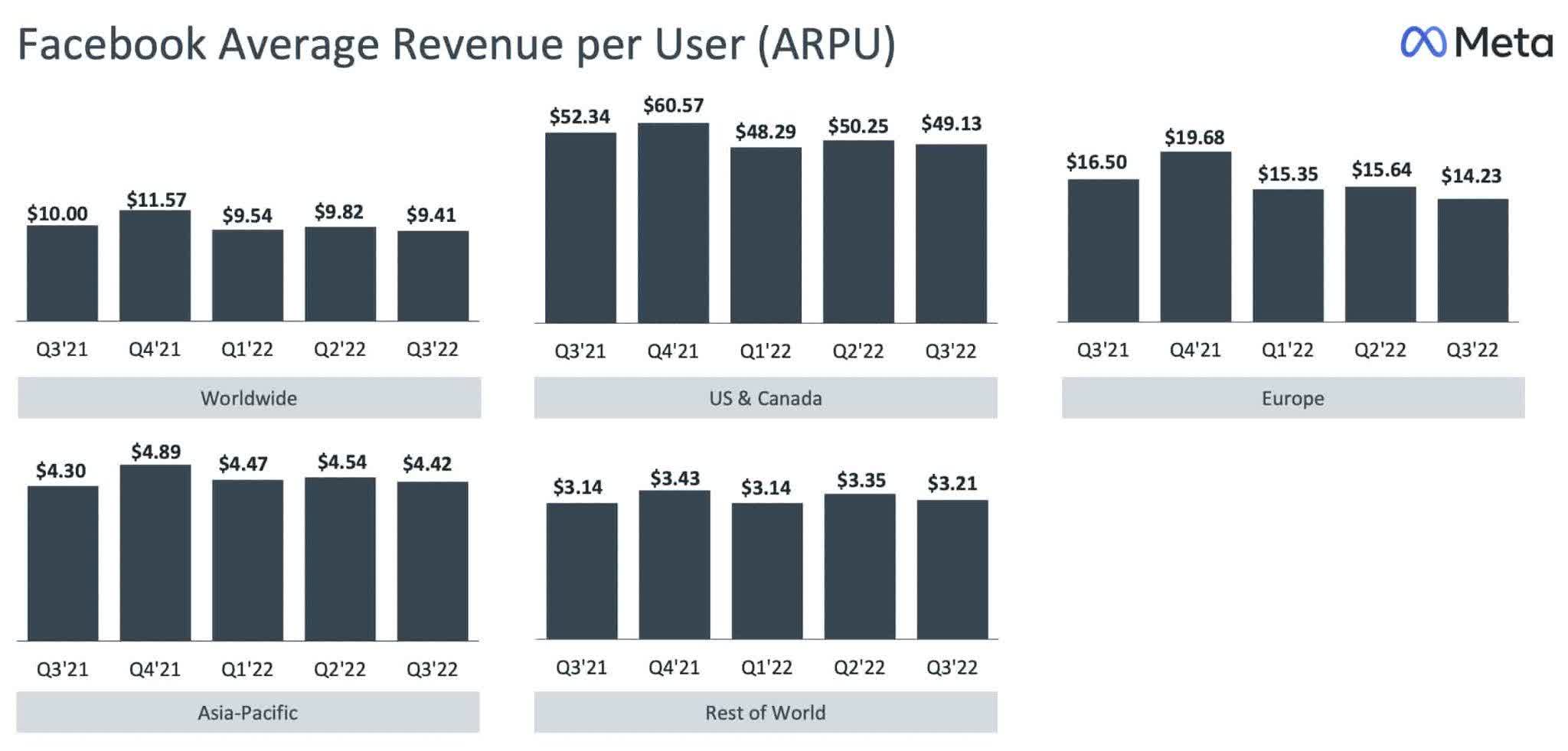

One key component of valuation is the monthly average revenue per user (“ARPU”). The 3Q22 presentation shows that there is no social media company like Meta with respect to ARPU:

Meta ARPU (3Q22 presentation)

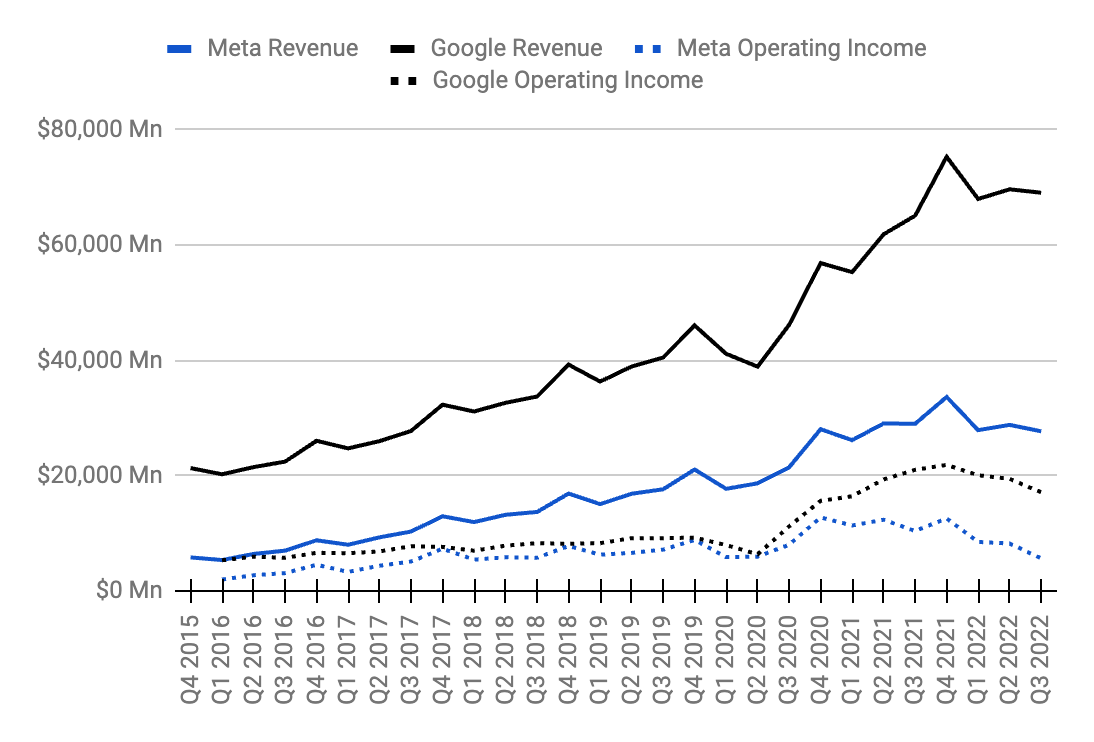

There was a time from 4Q17 to 2Q20 when Meta’s margins were better, such that they were close to Google (GOOG) (GOOGL) with respect to operating income. These days that is not the case as Google is lower in the advertising funnel such that measurement for their ads hasn’t been hampered too badly with Apple’s (AAPL) privacy changes:

Meta operating income (Author’s spreadsheet)

Per the 3Q22 release, 4Q22 revenue is expected to be $30 to $32.5 billion, and it was $33.7 billion in 4Q21. F/X considerations are a substantial factor:

Our guidance assumes foreign currency will be an approximately 7% headwind to year-over-year total revenue growth in the fourth quarter, based on current exchange rates.

Meta has TTM operating income of $35.1 billion or $22,545 million + $46,753 million – $34,168 million on TTM revenue of $118.1 billion or $84,444 million + $117,929 million – $84,258 million. Given the long term opportunities in digital advertising, I think Meta is worth 12 to 18x TTM operating income, or $420 to $630 billion when rounding to the nearest $10 billion.

The 3Q22 10-Q shows 2,248,672,204 A shares plus 402,876,470 B shares outstanding as of October 21st for a total of 2,651,548,674. Multiplying this by the November 10th share price of $111.87 gives us a market cap of nearly $297 billion. The enterprise value is less than the market cap, as the cash and equivalents outweigh the debt.

The market cap and the enterprise value are less than my valuation range, and I think the stock is a buy for long-term investors.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Be the first to comment