Alex Wong/Getty Images News

Investment Thesis

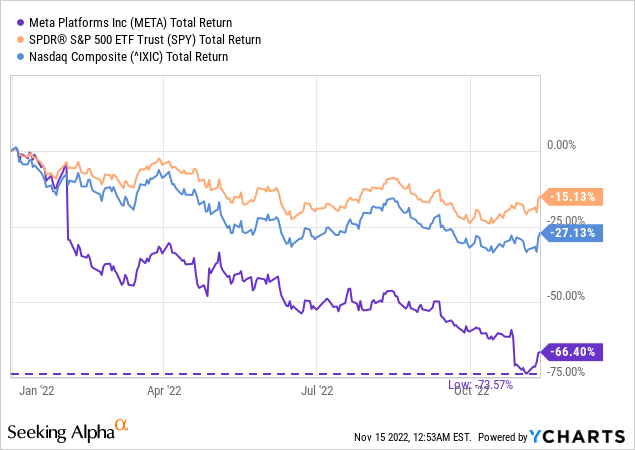

Last week, Mark Zuckerberg, CEO of Meta (NASDAQ:META), announced that he will lay off 11,000 people, or 13% of the workforce. This came after Meta’s advertising revenues seemed to be peaking, and the company had already spent US$36BN on its Metaverse project, without much success.

We believe Meta, like Coca-Cola (KO) at the time, will turn its business model around and become more profitable again. In 1985, Coca-Cola made one of its biggest and boldest moves by introducing “New Coke,” a reformulated version of the classic Coca-Cola that would taste better according to blind taste tests. They took the bold step and tried to replace Classic Coke with New Coke.

They did this because their market share was declining, and they were losing much of that market share to PepsiCo (PEP) and others. The launch received a lot of resistance from consumers who were used to the classic formula, so Coca-Cola re-released the classic version just 79 days later. With the return of Coca-Cola Classic, sales of the classic version were significantly higher than those of New Coke and Pepsi. In fact, Coke’s sales increased more than twice as fast as Pepsi’s.

Similarly, we think Mark Zuckerberg may realize that his Metaverse investments will not yield the same ROI as the core advertising business, and will refocus on his core business as the economy threatens to go into recession. If Mark Zuckerberg ever announces he is refocusing on his core business, we think the stock could rise significantly based on its fundamentals.

Corporate Governance At Fault

The main reason why Mark Zuckerberg is able to spend billions on his Metaverse project, and invest aggressively in other projects that yielded a much lower ROI, could be attributed to corporate governance. Looking more closely at how voting with Meta Stock is structured, we have 2 types of shares: Class A shares and Class B shares.

Class A shares are the common shares traded on the Nasdaq, while a Class B share has 10x the voting power of Class A shares. This means that although Mark Zuckerberg only owns 13.6% of all shares, he still controls 53% of the company, as he owns 82% of the company’s Class B shares.

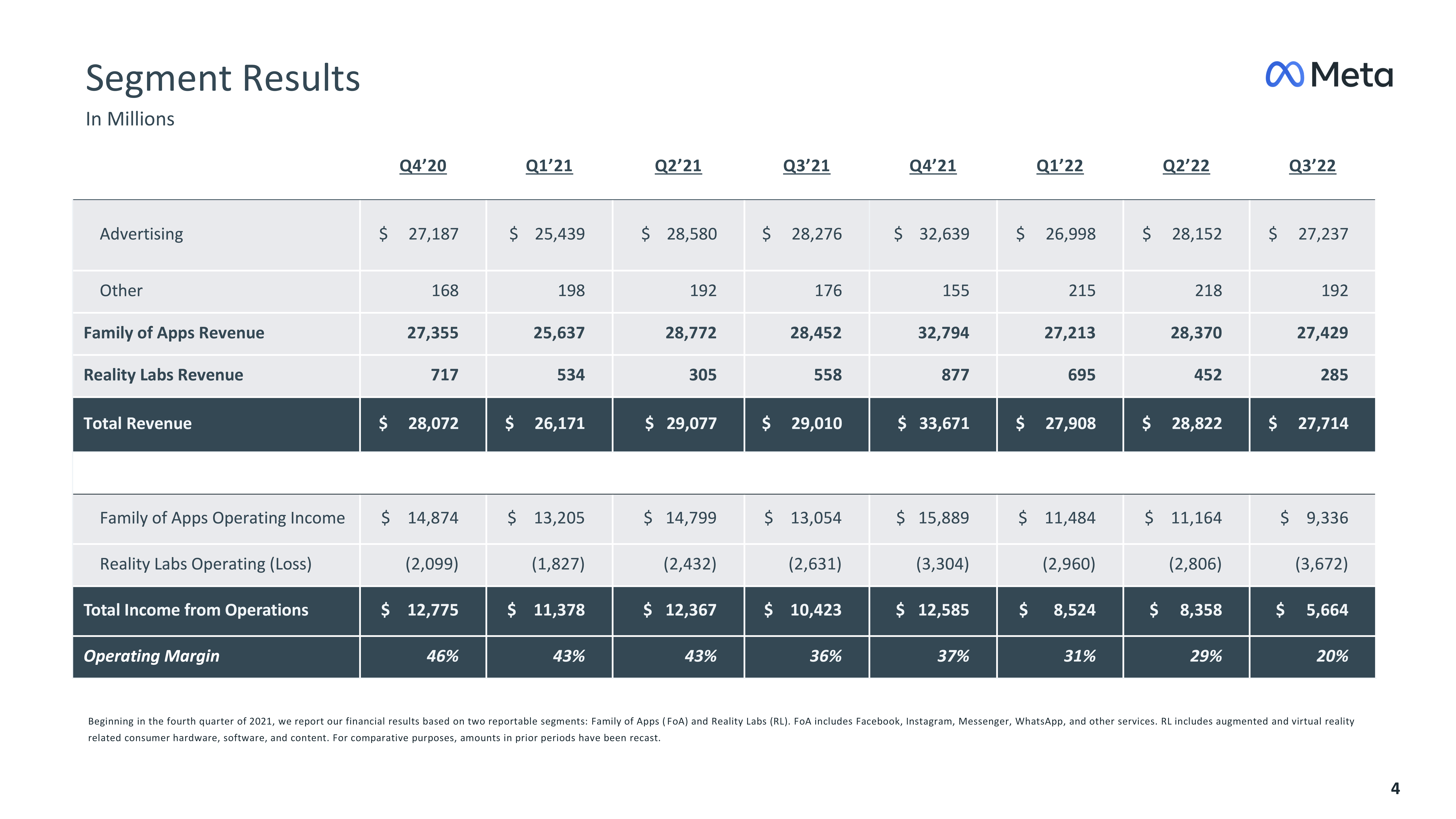

We believe that while the Metaverse has future potential, it is not currently a viable investment because it lacks a clear path/business model to generate revenue from the Metaverse, in addition to revenue from selling VR hardware to customers. That currently still leads to an operating loss in that segment of US$1.8BN-US$3.6BN per quarter.

TIKR Terminal

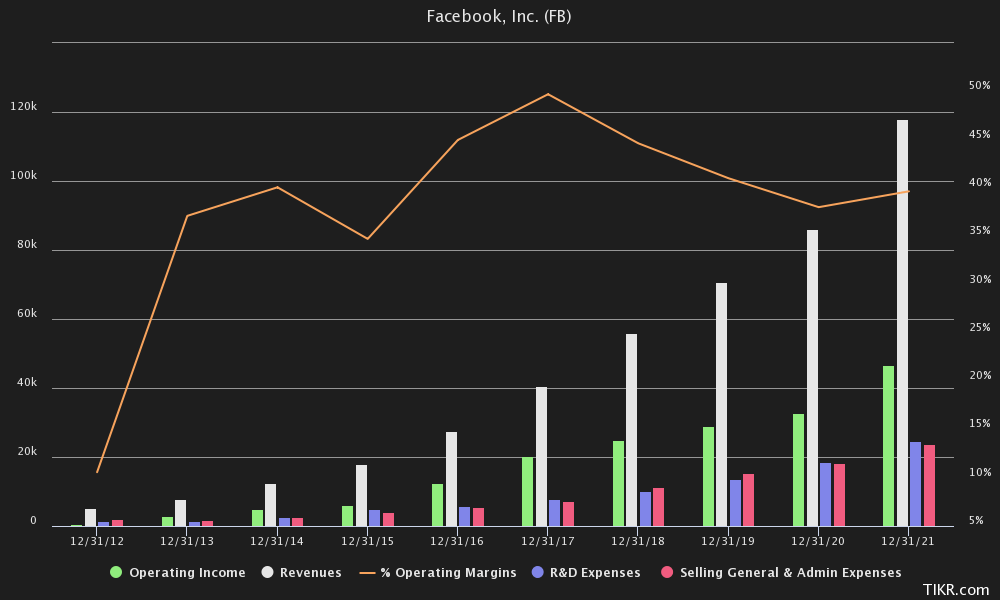

By contrast, looking at Meta’s history, they have been profitable from day 1, which is not a feat that many companies going public today can say. Especially being profitable from day 1 with 35-40% operating margins. We believe this scenario was the perfect storm, as online advertising is cyclical and Meta made the mistake of taking on too much.

But it seems to be taking the right steps to return to operational efficiency. Management also announced last week that it is discontinuing Portal and its smartwatch hardware projects.

Meta Is Still A Cash Cow

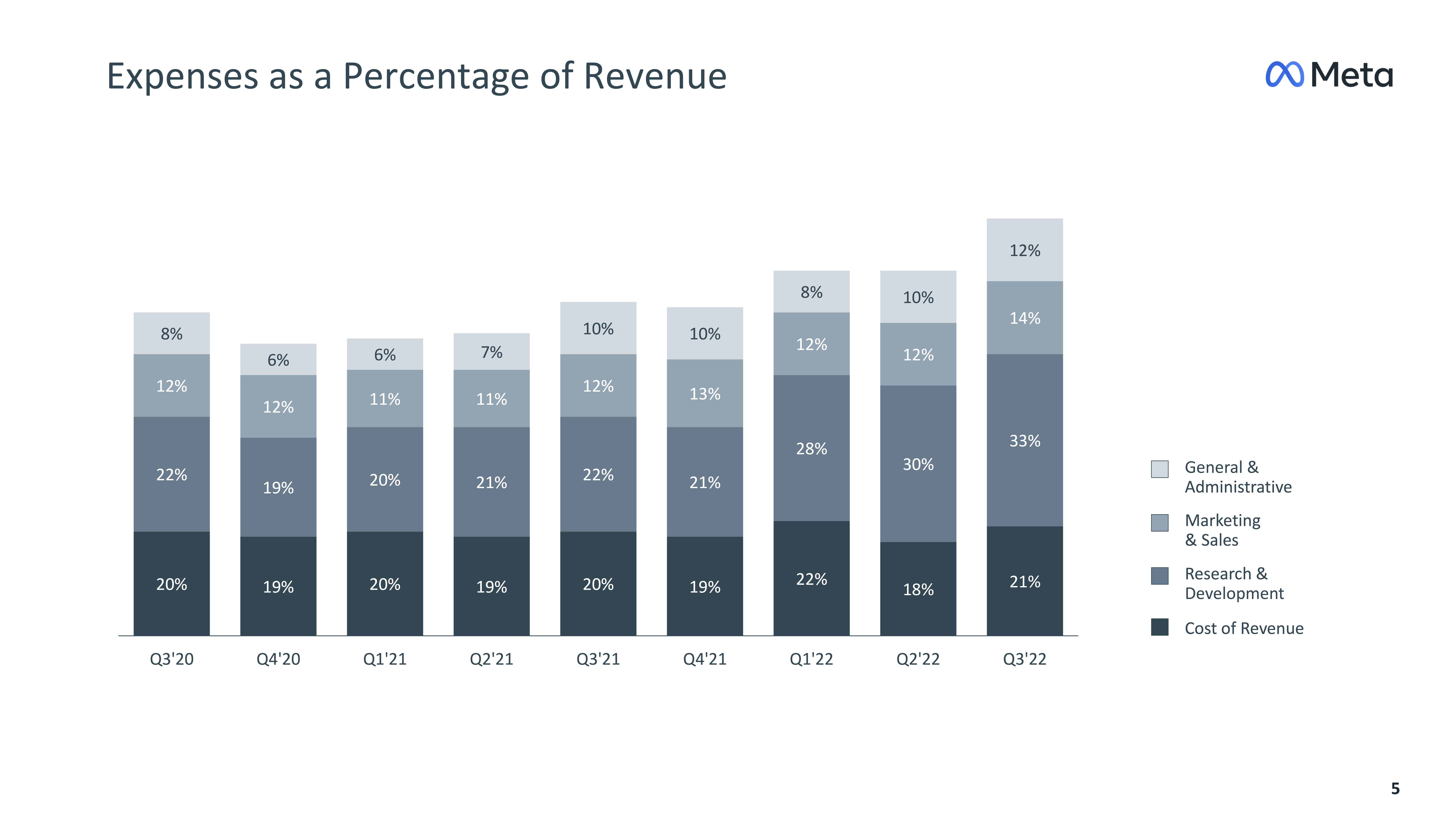

Yet Meta still seems like a cash cow. Even more so if we take into account the huge amount of R&D and CapEx currently being floated by the company. R&D, for example, rose 45%, mainly due to hiring within the Family of Apps and Reality Labs segments and the cost of developing Reality Labs technology.

Marketing increased 6%, and sales and general and administrative expenses increased 15%, also primarily due to personnel costs. Knowing that Meta is laying off 13% of its staff, and may soon turn away from heavy investment in Metaverse projects, that percentage of R&D spending could drop significantly, returning to a base level of 20-24%.

That 13% layoff itself could save Meta an immediate US$1.55BN in spending per year in the long run, assuming an average salary of US$141,000 per employee.

Meta IR

Another big part of Meta’s demand comes from the huge increase in CapEx, which from US$18.6BN in 2021 is now expected to reach US$32BN-US$33BN for fiscal year 2022. Much of that investment is driven by Meta’s investments in AI. However, an important note came out of the third quarter that we believe is of paramount importance going forward:

Our level of CapEx investment will depend on the returns that we generate through these investments in AI. And if we generate significant engagement and revenue gains, we will continue investing here. And if we don’t, we will pace our spending accordingly.

CapEx in 2023 is expected to be slightly higher than in 2022, although we think the company may seriously cut back on investments, and may have overestimated its CapEx projections if revenue or engagement disappoints. That clearly seemed to be the case in Mark Zuckerberg’s letter, in which he said the following:

I made the decision to significantly increase our investments. Unfortunately, this did not play out the way I expected. Not only has online commerce returned to prior trends, but the macroeconomic downturn, increased competition, and ads signal loss have caused our revenue to be much lower than I’d expected. I got this wrong, and I take responsibility for that.

This also surprisingly came about 1 month after the launch of its Quest Pro headset, one of the most highly anticipated headsets priced at $1,500, aimed primarily at the work force. Although, many news outlets questioned what audience the headset was actually intended for. This again reinforces our contention that their Metaverse project is not a real business model. Perhaps the layoffs are also related to a lower than expected number of orders for the VR headsets, but we will have to wait until the fourth quarter to see the results.

Meta IR

Meta Is Too Cheap To Ignore

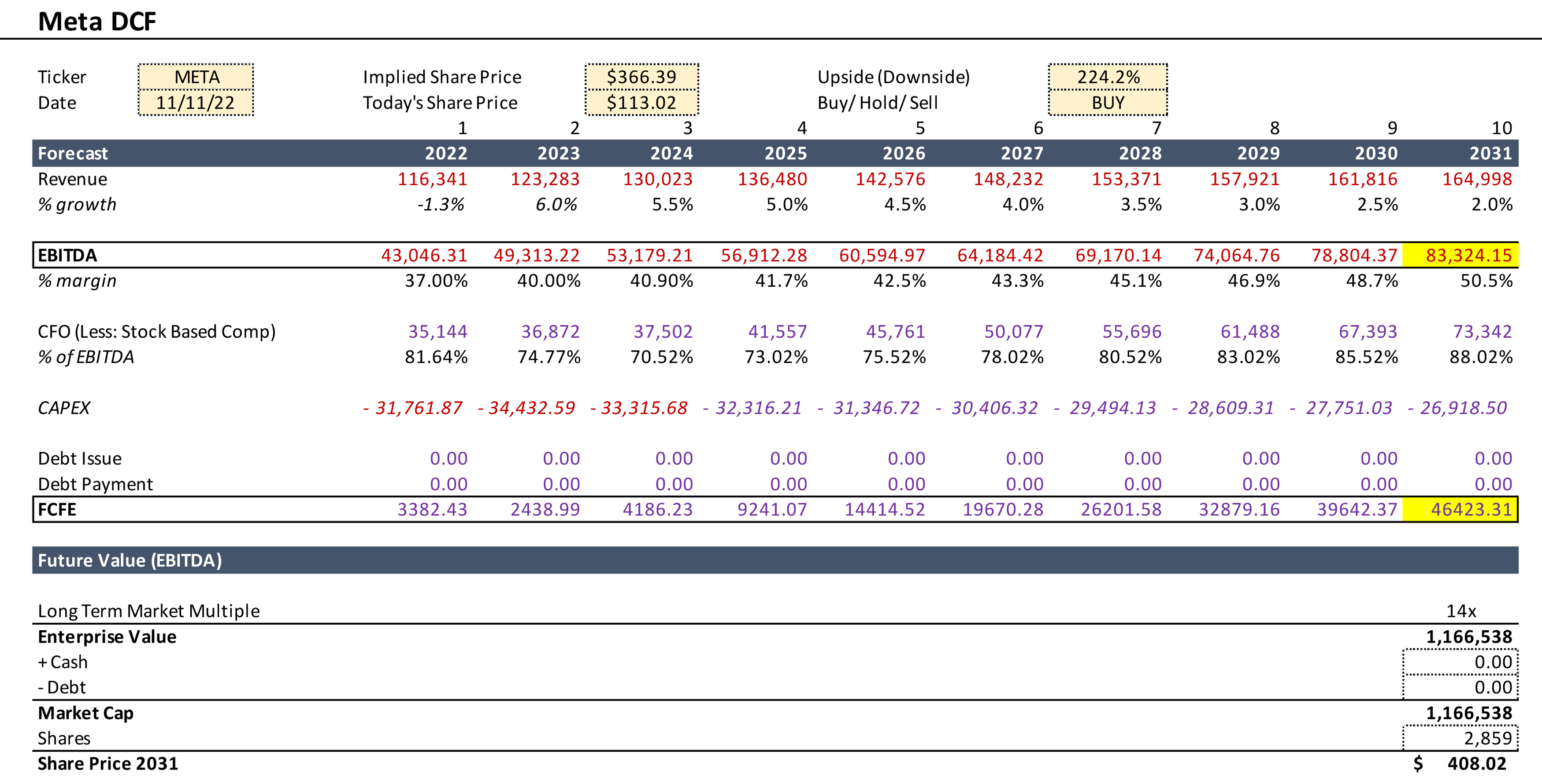

In our financial model, we accepted Wall Street’s consensus estimates for both 2022 and 2023, because short-term estimates are usually relatively reliable. However, we modeled Meta as a mature company in a later growth phase, and slowed revenue growth to a terminal growth rate of 2% by 2031.

That means our expectations are well below Wall Street’s revenue estimates, which come in at about US$219.5 billion for 2031. On the other hand, we think that operational efficiencies, such as reductions in R&D and sales and general management costs, could bring EBITDA margins back to 50% in the long run. We think those reductions will occur mainly after 2023. In 2017, Meta had EBITDA margins above 57%.

The same is true for CapEx, in our view. And as mentioned in the Q3 earnings call, CapEx should return to baseline as a percentage of revenue. The median percentage of CapEx to revenue between 2014 and 2021 was about 16%, which we took into account in our financial model.

Author’s Financial Model

Since Meta currently has almost no debt, we have taken their cash balance into account for simplicity. On an EV/EBITDA basis, we believe Meta should be worth $408.02 if valued at a reasonable 14x EV/EBITDA multiple below market value.

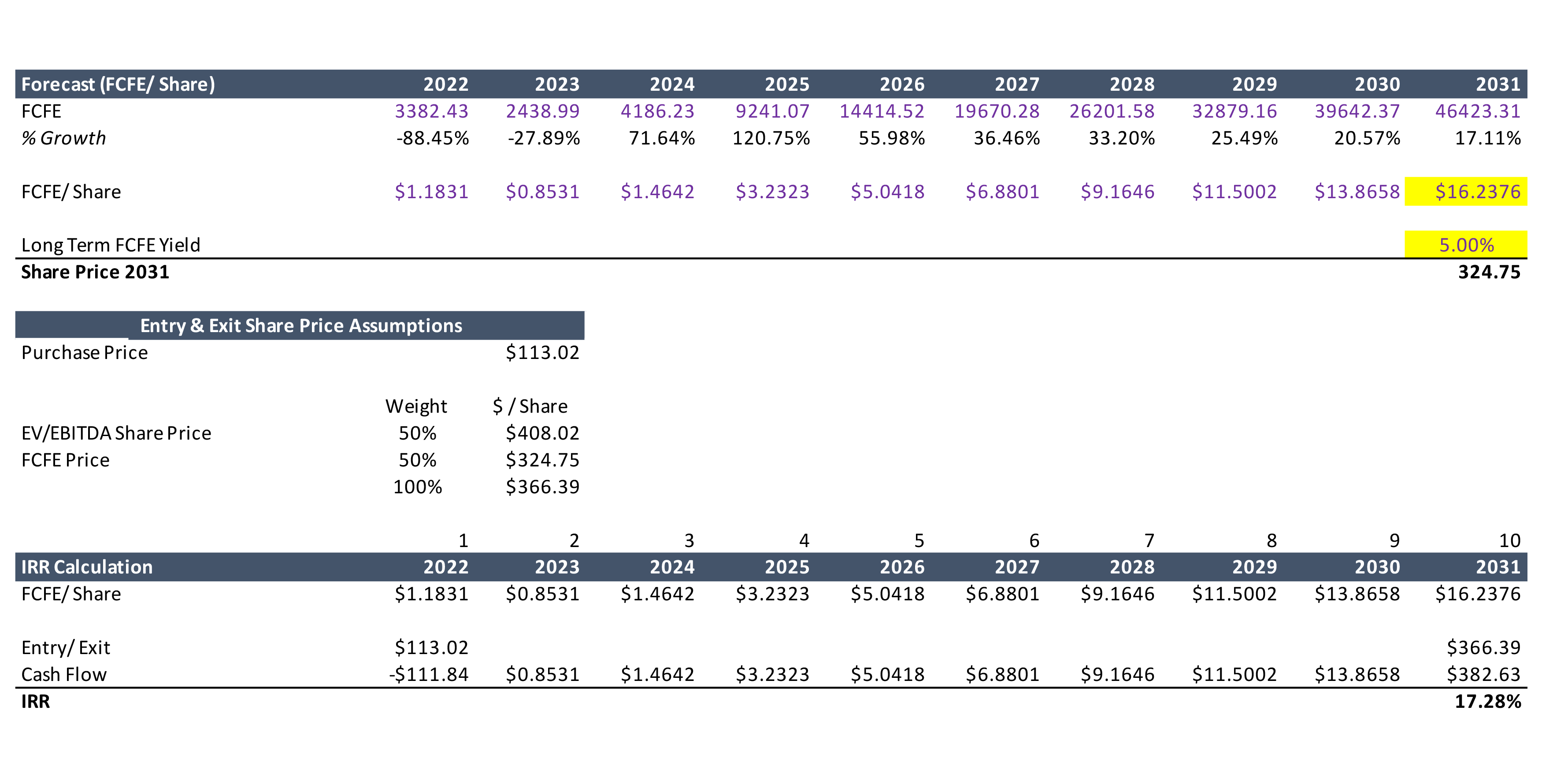

On a free cash flow to equity basis, we believe Meta could be worth $324.75 at a 5% FCFE yield. We believe this yield is very conservative, given that Meta has historically traded at a yield of 1.92% between 2012 and 2021. Only now in 2022 was that return over 6.2%.

We took both EV/EBITDA and FCFE valuations at a 50% weight, and concluded a price target of $366.39. If you could buy the stock today for $113.02, that would be a potential IRR of 17.28%, giving investors great potential to generate significant alpha above broad benchmarks.

Author’s Financial Model

There are risks to this proposition, of course, such as increasing competition from platforms like TikTok, Twitter (TWTR) and others. We also think there is significant risk in the area of corporate governance, since we have already pointed out that Mark Zuckerberg holds most of the power over the company.

This could still lead to serious mismanagement of the company, or to the deployment of capital in areas that do not yield sufficient ROI. Although we think, with Mark Zuckerberg’s latest letter, that he might realize how important his core business actually is.

The Bottom Line

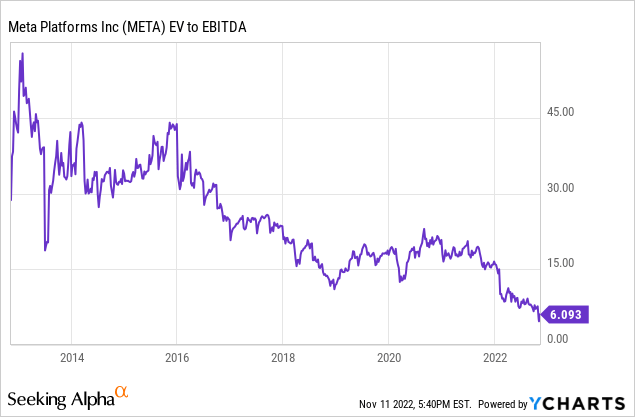

To us, Meta seems ridiculously undervalued, with an EV/EBITDA ratio of 6x. We think most investors have completely written Meta off because of their aggressive spending plan when it comes to Reality Labs, despite their stated goal of total operating income growth.

Moreover, the fourth quarter is usually the best quarter for earnings, and the bad news may have already been priced in after management announced layoffs and a slowdown in earnings.

We think Mark Zuckerberg realizes that he was wrong about Meta’s growth, which will cause him to reconsider his long-term investments in Reality Labs, and perhaps scale back his investments when it becomes clear that there is not enough ROI to be had in the segment. As Michael Burry tweeted not long ago, “Meta has a New Coke problem.”

Be the first to comment