TebNad/iStock via Getty Images

Mercury Systems (NASDAQ:MRCY) is a defense stock specializing in military, satellite and electronics systems which has had a difficult past few years. After a period of solid outperformance from 2014 to 2019, it has fallen on hard times with weakened billings and earnings metrics. However, the turnaround is afoot, with strong billings growth and improved cash flow coming in 2023 helping to lift the stock. Mercury is a solid buy at these levels, as geopolitical issues should put a floor under defensive names in an uncertain environment in 2023. The recent Chinese balloon incident underscores the need for additional monitoring capabilities and how reductions in budget for defense are unlikely.

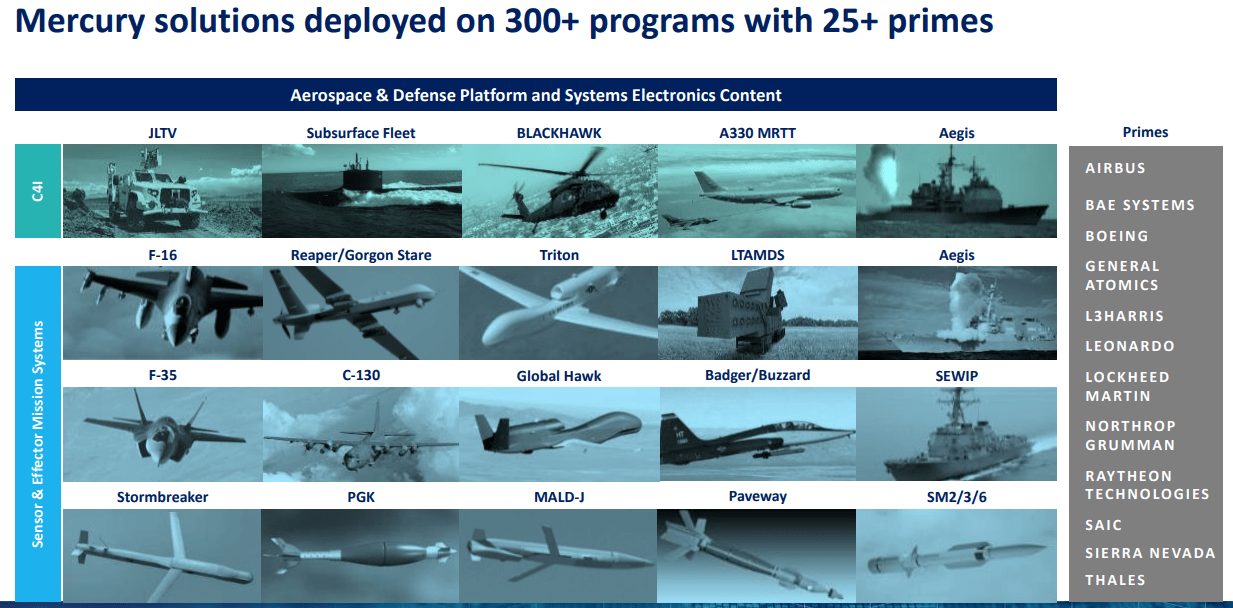

The company is strategically lowering costs and focusing more on improving cash flow and earnings in the coming years. Also, the board has recently initiated a strategic review, which could end in a potential sale of the company or other initiative that could boost the share price. While this is never a reason alone to hold an equity position, you need to keep this optionality in mind with Mercury being a small cap stock. The company outsources and deals with over 25 of the largest military manufacturers in the world providing electronics. The continued expansion of electronics as a portion of spend is a long term tailwind to Mercury’s growth and market share. The more complex the program, the higher margin it tends to be, with the long-term increase in electronic needs meaning higher margins over time.

Mercury Investor presentation (William Blair Conference Presentation)

Recent Fiscal Q2 2023 earnings

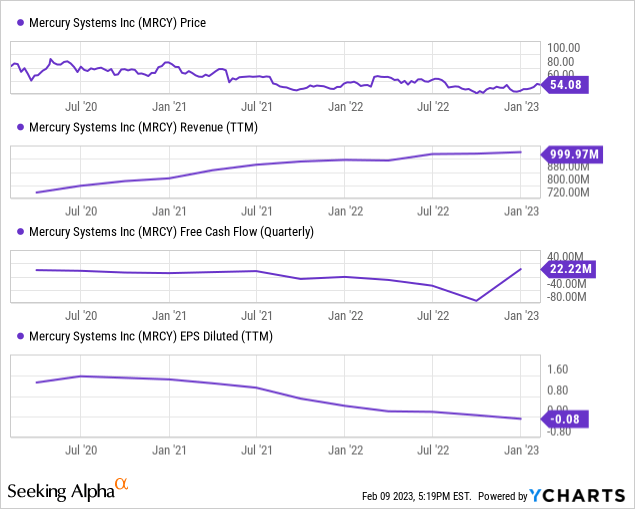

The recent Fiscal Q2 earnings for Mercury had several positive data points that one could point to foreseeing a share rebound. Mercury had solid new business billings in the quarter, with $270.3 million in billings 18% ahead of the revenue number for the quarter. Demand continues to be strong for defense spending, and the continued war in Ukraine is likely to increase defense budgets in Europe over time. Total backlog of orders was $1.12 Billion, or $164 million ahead of this point one year ago. The solid backlog growth of 17% presages future revenues and cash flow, and change in backlog growth speed is a preferred metric to assess MRCY’s business. Revenue increased to $229.6 million, just 4% growth over the prior year, but the billings number is considered more predictive of long-term performance. As such, the stock has actually gotten cheaper over the past year, with a 1% gain trailing the billings growth over that time. Revenues continue to increase, as seen below, but cash flow has been the sticking point for MRCY in recent years.

GAAP net loss was $10.9 million in Q2, which should be the low point as they guided to a loss of $6m to positive $1m for Q3 2023. Operating margin for the year will be around 2% with longer term operating margin above 10%. This is achievable over the next few years once supply issues abate and working capital is worked down to lower levels. Free cash flow went from positive $100m per trailing 4 quarters to negative in mid 2022. As you can see below, free cash flow rebounded to positive last quarter, a welcome sight for market participants. Mercury has been holding additional inventory and working capital to help mitigate supply chain challenges the past 2 years, but that should unwind in the coming year, with the market giving credit for improvement there by the end of 2023. Part of the issue for MRCY is continued supply chain disruptions in the microelectronics space, preventing them from getting product out the door as fast as they can. Semiconductors continue to be an area where supply chain issues and lockdowns have hurt consistent order flow. Analysts see this situation as continuing throughout 2023 with a chance for more significant improvement in the second half of 2024.

Trends and Tailwinds

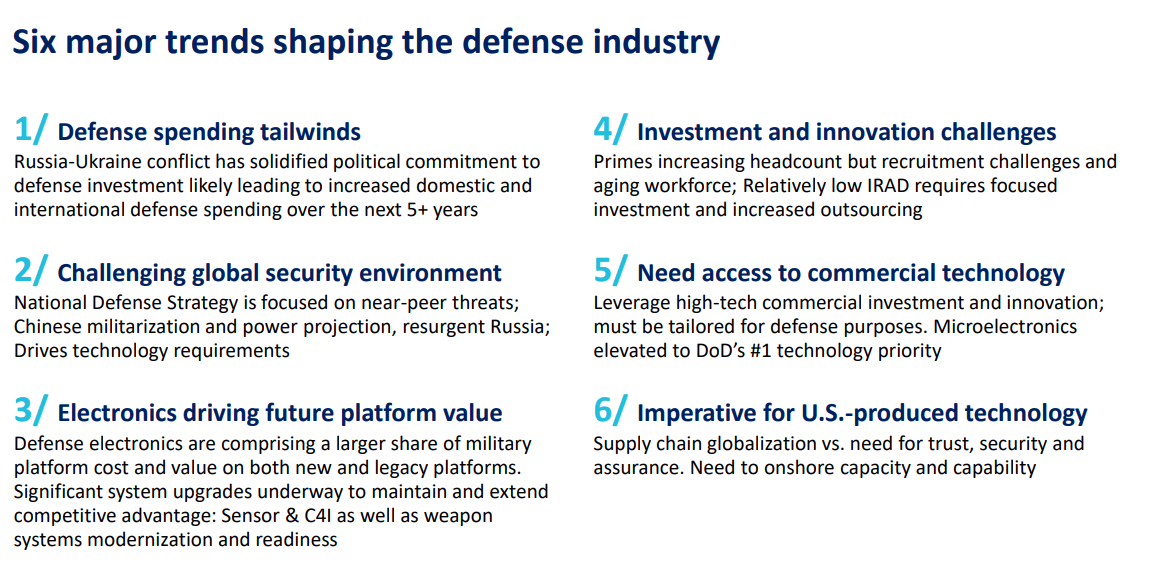

Below, you can see some of the strongest arguments to hold Mercury stock for the next few years. The biggest one right now would be the strong tailwinds from both the Ukraine conflict and increasing worry about China in the future. This counters one of the potential risks as spending cuts in the United States potentially loom after a period of large deficits. However, bi-partisan support seems to exist to continue increasing the DOD budget and providing advanced support to allies globally. Electronics such as those that Mercury specializes in continue to become a larger share of military platform cost, which increases potential revenue long term. Public defense companies are slowing research and development expense in order to increase earnings and drive share price appreciation – leaving room for Mercury to supplement them. Older equipment had a much smaller share of electronics, which is being changed by large programs like the F-35, for example. Larger military primes are continuing to outsource more of this work to Mercury, who continues to acquire and consolidate the electronics space.

MRCY Investor Presentation (William Blair 2022 Investor Presentation)

Also, the US in general wants to onshore more of these capabilities for security and to increase homegrown capability. Having too many of these capabilities in places like China is a risk to national security, whereas bringing more programs to the United States helps alleviate that concern. Additionally, Europe may increase spend over time as pressure on NATO allies increases to spend to the 2% of GDP target on defense. This could mean between $80-100 Billion US in additional spending each year by European countries if it materializes. The ongoing Ukraine situation and sabre-rattling by Russia makes it more palatable to the population from a cost perspective. This is an optimistic outcome, with something in the middle likely, as governments feel free to improve capabilities for political optics if nothing else.

Risks

The largest risks to Mercury stock continue to be those self-imposed by the management and company. Execution has been questionable in the past, and the large number of acquisitions over the years has created operational complexity. This means it is difficult to say which portions of the business are performing better than expected and which are more lagging based on purchase prices. 15 acquisitions and over 3x the employees since 2014 has led to some missteps in generating earnings. This kind of roll-up strategy has mixed results in public companies, with many having similar struggles as Mercury, trying to balance so many different moving pieces. The stock also trades at a premium to its peers at 23x forward earnings. This shows MRCY has a significantly higher risk profile than its more stable, slow growing defense contractors that have better earnings visibility. Also, US stock valuations and the US market in general are at risk of a drawdown with weakening economic activity and high interest rates in 2023. Many investors are turning to Europe or Emerging Markets for lower valuations right now, with MRCY running quite contrary to that theme.

Conclusion

MRCY is a higher risk name in the defense sector that continues to benefit from the modernization of military subsystems globally. While the company has some potential risk, it has significant upside through improved cash flow generation or a possible sale by the end of 2023. Investors with a high risk tolerance should look closely at Mercury stock for its potential for medium term gains in an industry less correlated to other risk assets. A potential sale or re-rating of the shares closer to its previous average 2016-2019 multiple of around 3x book value could mean more than 50% upside from here to above $80. Thus, I would recommend adding positions to Mercury at this time due to its potential upside and improvement of its current issues likely over the coming 12 to 24 months.

Be the first to comment