JazzIRT

Real estate is usually amongst the sectors hit the most in a rapidly rising interest rates environment. As one of the multi-billion real estate investment trusts (“REITs”), Medical Properties Trust, Inc. (NYSE:MPW) has had its market price more than halved since the beginning of the year.

Yet, MPW is a healthcare REIT, which should be more resilient to economic downturns, as healthcare is non-cyclical. Looking at this year’s price action in relation to the underlying business, the sharp decline seems unjustified. The debt, although high, is manageable, while management is taking steps to de-risk the company. The dividend is growing and appears to be sustainable. Overall, I think that MPW is a rare 10+% yield opportunity in the REIT space and the share price could be going up soon.

Company overview

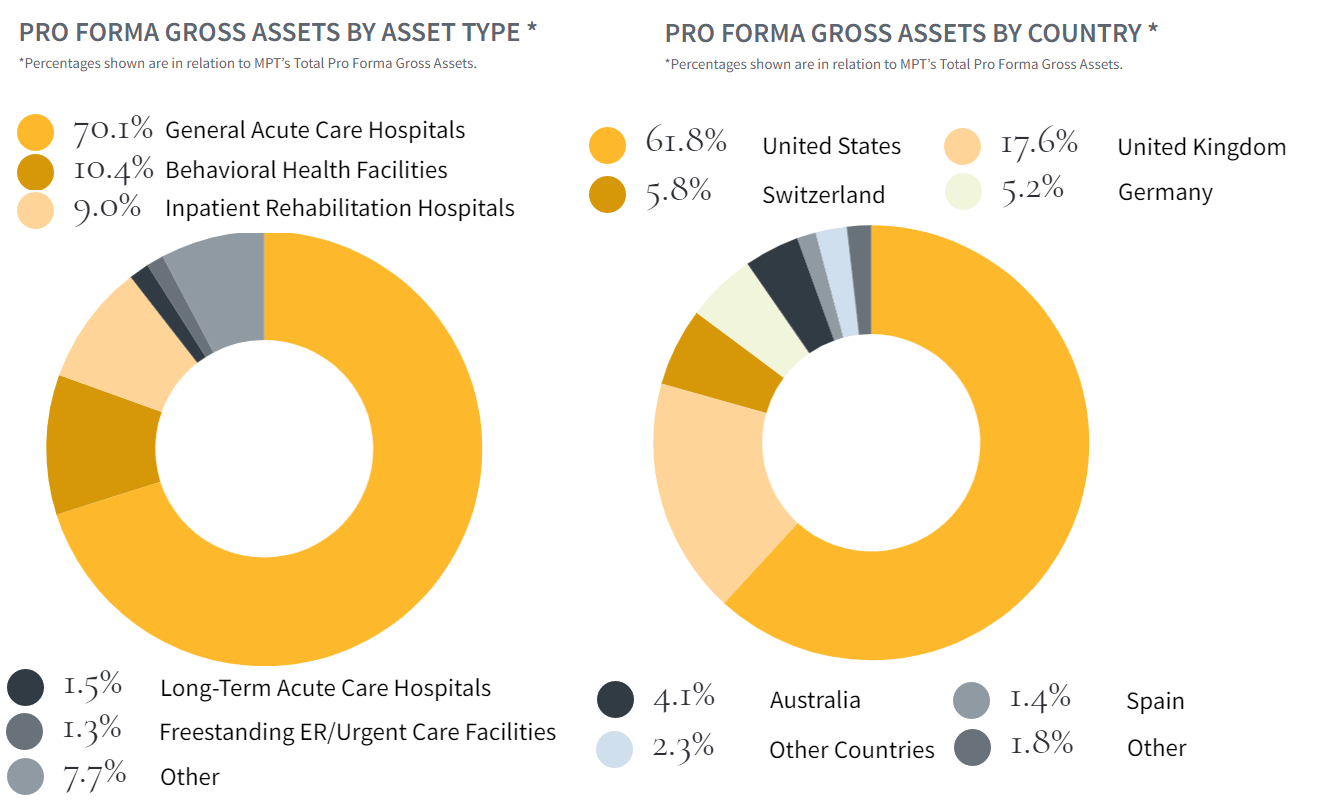

With 434 properties and capacity of 44k+ beds, Medical Properties Trust is the second-largest private owner of hospitals in the world. The company has facilities in 10 countries, but the primary focus is the U.S., accounting for slightly less than 62% of total assets.

MPW’s portfolio (MPW)

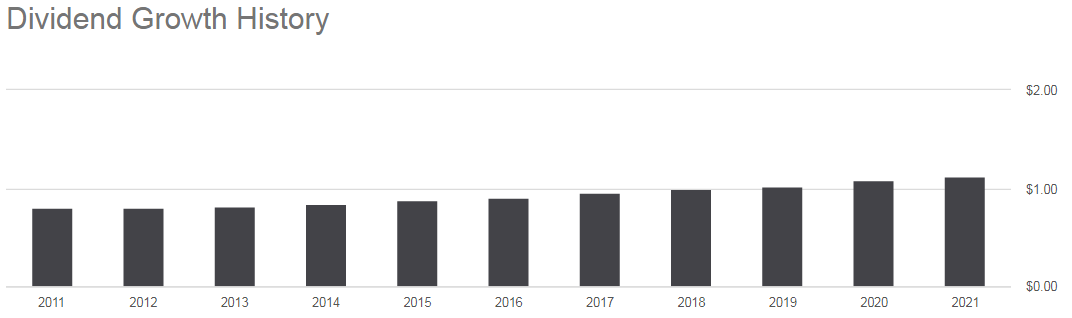

The capital structure of the company consists of 599M shares, with institutions dominating the ownership base with more than 83%. The company has been annually raising its quarterly dividend for the past 8 years. In 2022, the company is paying US$0.29/quarter, which puts the annualized dividend yield at 10.4% – more than double the median for the Real Estate sector.

MPW’s dividend history (Seeking Alpha)

Why has the share price fallen so much?

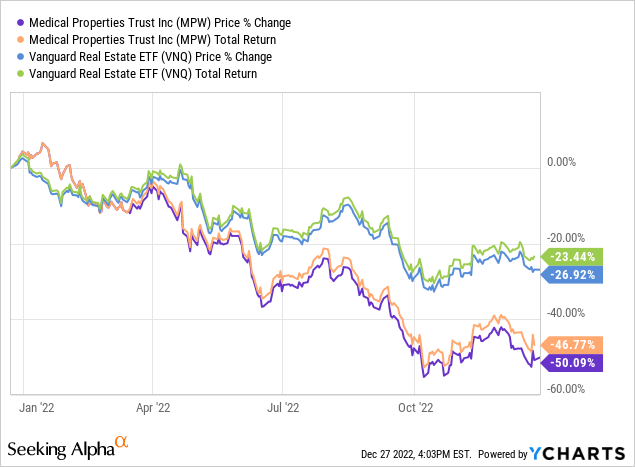

Since the beginning of the year, the share price of MPW has fallen more than 50%, considerably underperforming the sector as measured by the Vanguard Real Estate ETF (VNQ). What’s more, short interest has been climbing and surpassed 13% of MPW’s float, which is very rare for a REIT. So clearly, there are some company-specific reasons that could justify the sell-off.

Debt is high, but manageable

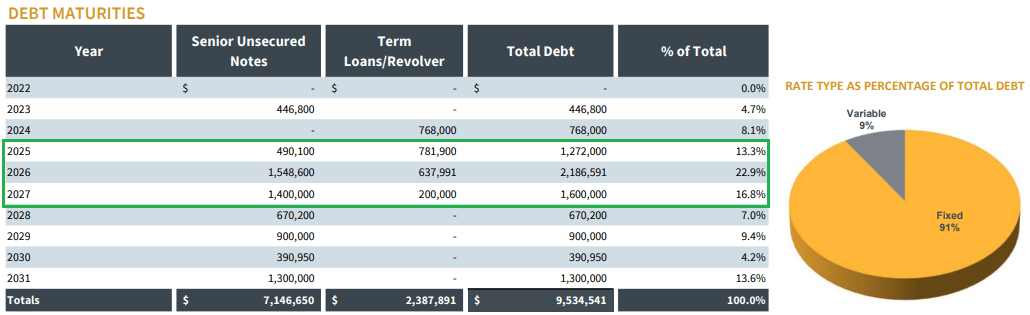

As of the end of Q3’22, MPW has slightly more than US$9.5B of debt, which puts the D/E ratio of the company at 1.4x. The leverage of MPW is indeed a bit worse than the Real Estate sector, as evident from the Seeking Alpha factor grade.

MPW’s leverage grade (Seeking Alpha)

However, a closer look at the debt shows that things are not that bad. Firstly, over 91% is at fixed rates, so the recent interest rate hikes by the Fed won’t be felt immediately. In addition, the maturity structure of the debt looks favorable. It has less than 5% of the total maturing in 2023, while the bulk of loans is due in 2025-2027. This makes rates in that period key for the company. However, I think rates then will be lower than today, as the upcoming recession will force the Fed to go back to a near-zero-rate policy. I discussed this thesis in more detail in my article “S&P 500 In 2023: Brace For A Fed Pivot.”

MPW’s debt (MPW)

Business concentration

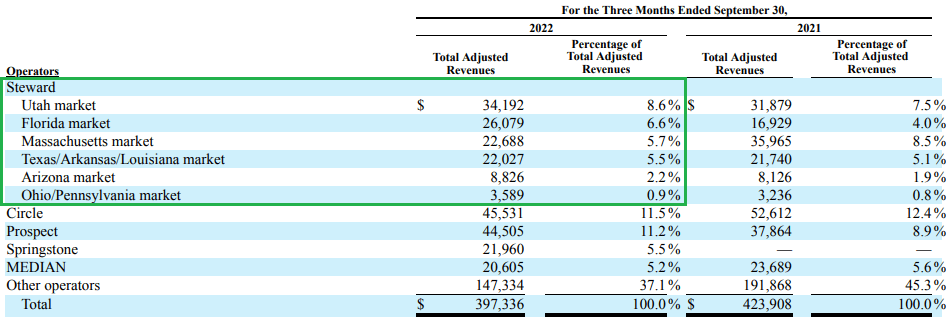

Another area of criticism towards MPW is its considerable dependence on one client – Steward Health Care. As of Q3’22, approximately 29.5% of all revenue came from that business partner. In addition to that, MPW has extended loans to Steward, which amount to US$362.8M and an equity stake carried at US$139M as of 30 Sept 2022.

MPW’s revenue breakdown (MPW’s 10-Q)

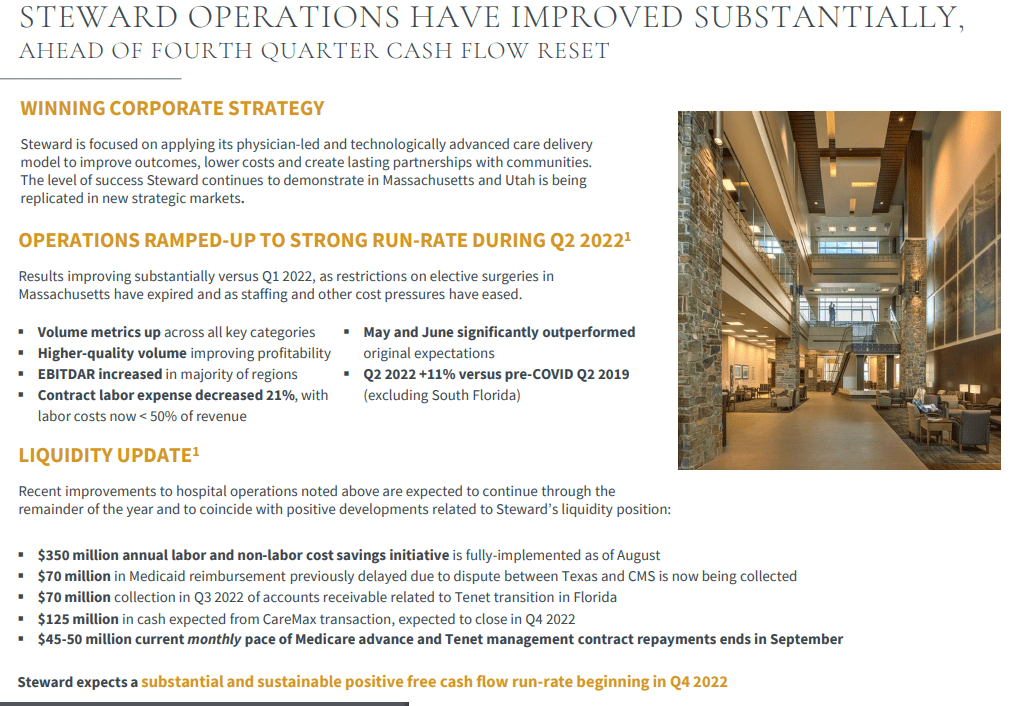

The business relationship with Steward may be perceived as a source of high risk, because the medical facilities operator had financial difficulties in the recent past and MPW came to the rescue in 2021 with funds totaling US$700M in various forms, including debt and asset transactions. Since Steward is not itself a public company, its financials are not transparent on their own. However, MPW provided an update, regarding the situation, highlighting positive development in Steward’s business.

Steward’s results are improving (MPW)

Recently, Steward’s credit line has been extended by its lenders, led by Citibank. This could be used as a third-party affirmation that the medical operator is in a position to service its obligations, including the rent payments to MPW.

Management has been proactive

I think MPW’s management is doing a great job through de-risking the company in the past year. This was done in multiple ways, but some of the most important are:

Deleveraging

In the face of raising interest rates environment, it’s prudent to reduce your leverage. This was done by asset-level transactions. In March 2022, MPW completed the sale of 50% interest in 8 facilities in Massachusetts to Macquarie Asset Management for a total cash proceeds of US$1.3B, which led to approx. US$600M gain on the income statement. The best part of this deal was that the facilities were operated by Steward, so MPW’s management killed two birds with one stone – it reduced its exposure to Steward and got a third-party affirmation of its tenant’s potential to continue to operate. In October, MPW sold three hospitals in Connecticut for US$457M, which covered its investment in the project. While the deal didn’t lead to gain on the income statement, it’s beneficial for MPW’s financial position.

Share repurchase

In October, MPW announced a share repurchase program worth up to US$500M. This would allow management to support the share price and reduce the number of shares outstanding, increasing the value of the remaining shares. I think the current low share price offers a great opportunity for that.

The dividend seems secure

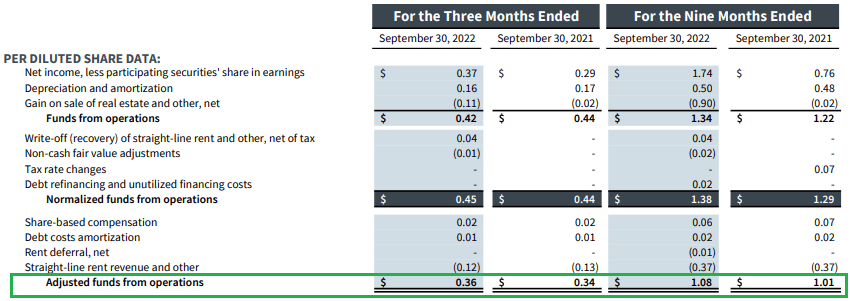

MPW’s results highlights (MPW)

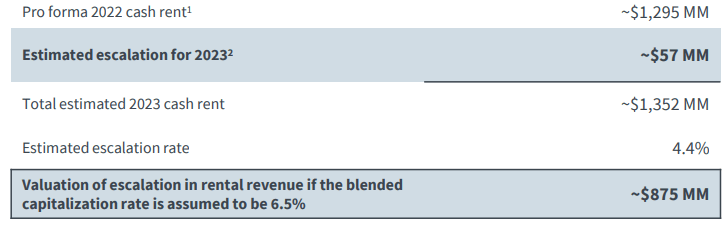

MPW has been paying US$0.29/share of quarterly dividend this year. This figure seems well-covered by the company’s AFFO (adjusted funds from operations), which has been growing YoY. Next year, if the trend of increasing the quarterly dividend by US$0.01 per year is continued, then for the increase in distributions, MPW will need around US$24M for the whole year. This amount seems well-covered by the rent escalation of US$57M expected in 2023.

MPW’s rent escalation (MPW)

Valuation

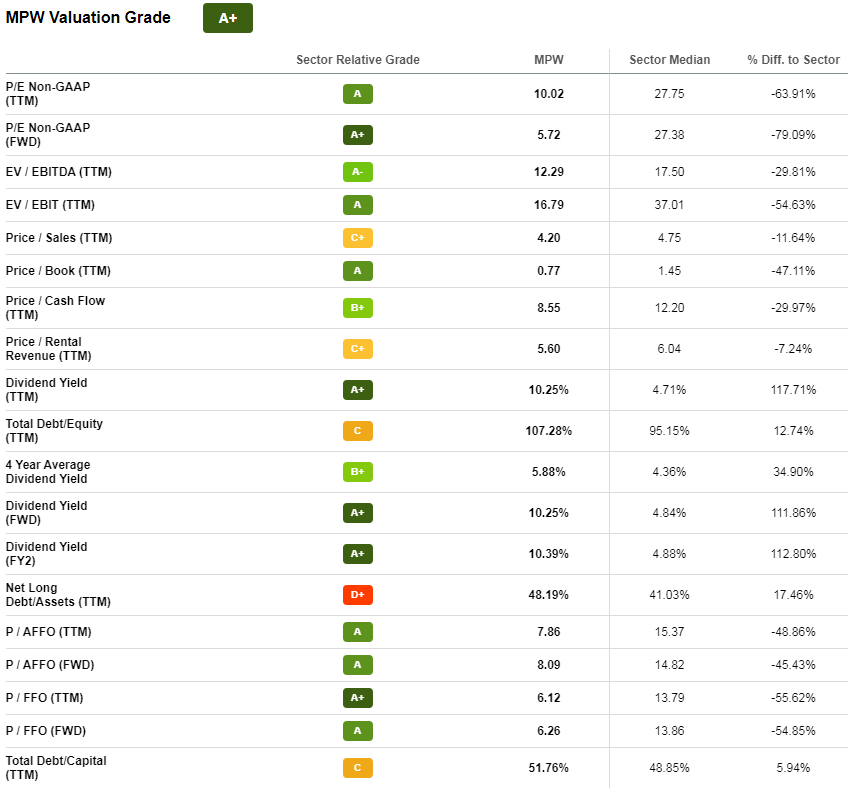

Looking at the valuation metrics at Seeking Alpha, MPW looks quite undervalued compared to the sector. In order for the company to reach the median values for Real Estate companies, its share price should double from the current levels.

MPW’s multiples vs the sector (Seeking Alpha)

I think that the high short interest may end up being a catalyst and drive the stock to the upside, once shorts realize that their thesis may not work and look to close their positions. As 2022 ends, any tax-loss selling should end, too, while in January some of those positions may be re-entered, increasing buying pressure. Another source of buying pressure could be the share repurchase program, announced by MPW.

Conclusion

MPW has been hit quite hard, with the share price sliding more than 50% in 2022. However, the main risks of leverage and the stability of the biggest tenant – Steward – seem to be overblown. MPW’s management has been doing a great job to de-risk the company and the dividend appears to be secure. With the high short interest, MPW may prove to be a serious bear trap and the shares could be heading north, once the shorts start liquidating their positions.

Be the first to comment