Wall Street, Volatility, AUD/NZD, Lunar New Year– Talking Points

- US equity indexes finished higher last week as volatility hit pre-pandemic lows

- Lunar New Year holiday sees majority of Asian markets still closed, lighter volumes?

- AUD/NZD’s rally may soon find significant resistance with a bearish SMA cross on the cards

Recommended by Thomas Westwater

Get Your Free Top Trading Opportunities Forecast

US equities moved higher last week as investors continued to bet on the global economic recovery, boosted by increased Covid vaccination rollouts, loose monetary conditions, and ongoing fiscal support. The small-cap Russell 2000 index gave the most impressive showing of the major ones, with a 2.51% weekly gain. A more notable development, however, is the collapse in volatility seen in the US markets, reflected by the CBOE S&P 500 Volatility Index (VIX) closing below 20, the lowest level since February 2020.

The collapse in volatility via the VIX – which is widely used as a “fear gauge” – follows a strong corporate earnings season. So far, financial results from S&P 500 companies have largely beat analysts’ expectations. The week ahead will see another round of quarterly results cross the wires, with the commerce juggernaut Walmart scheduled to release its figures on Thursday. Still, even with upbeat earnings, some investors are blowing the horn over stretched valuations.

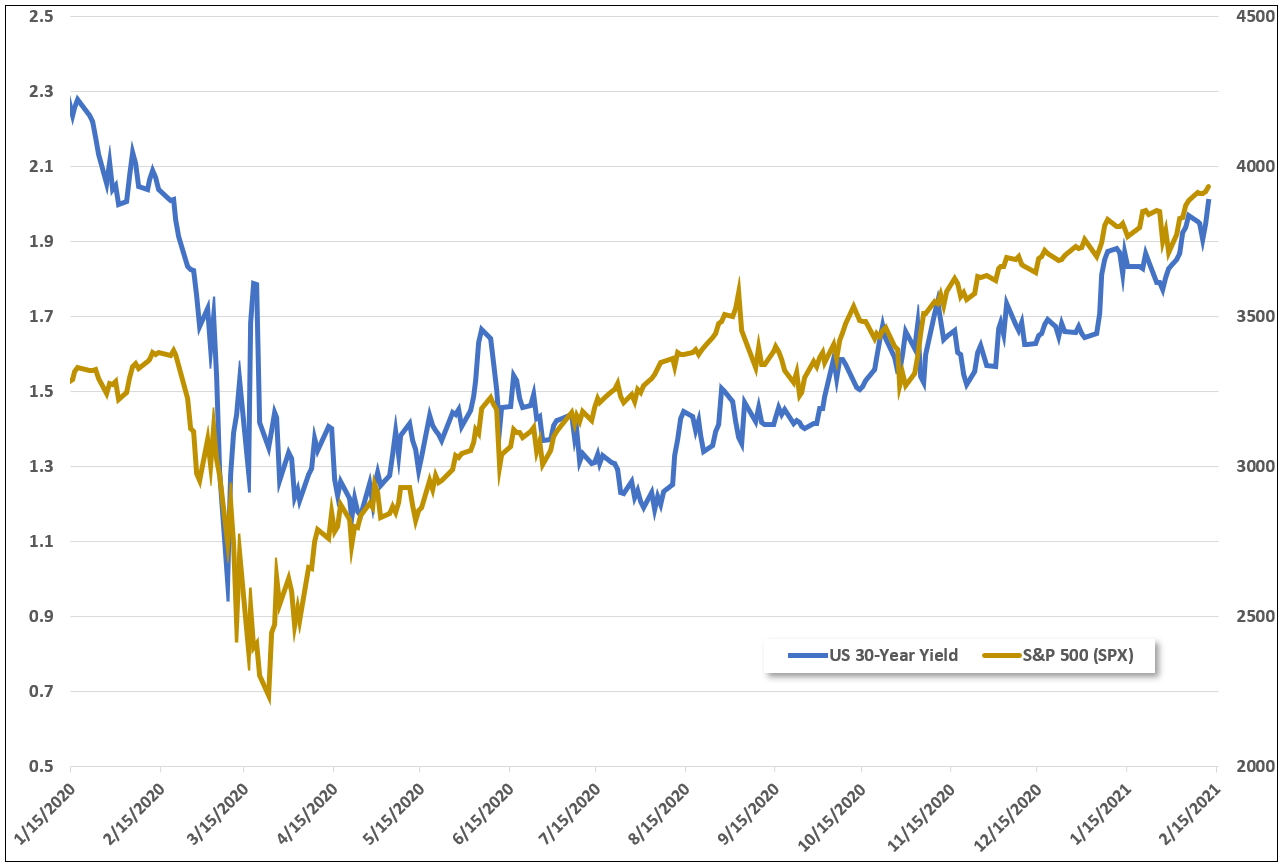

Stocks may have more fuel to continue running higher despite high valuations amid the ongoing support seen from central banks, particularly the Federal Reserve. In a speech to The Economic Club of New York last week, Fed Chair Jerome Powell once again ensured investors that supportive conditions are here to stay for the time being. Long-dated Treasury yields ended the week higher, with the 30-year yield climbing above 2.0%, the loftiest mark since early 2020.

S&P 500 vs 30-Year Treasury Yield

Data Source: BBG

Monday’s Asia-Pacific Outlook

Monday, along with the entire upcoming week, will likely be a quiet one across the APAC region. Exchanges are closed in China, Hong Kong, Singapore and South Korea as traders and investors celebrate the Lunar New Year holiday. Foreign exchange volumes may also see less activity, which could possibly also translate to lower volatility across many currency pairs. Having said that, breaking headlines that could drive markets quickly risk being more volatile due to reduced levels of liquidity.

Consequently, this week’s economic events calendar is also lighter than usual but the front end of the week may see the New Zealand Dollar react to BusinessNZ’s Performance of Services Index (PSI) report, set to cross the wires early Monday morning, according to the DailyFX Economic Calendar. Japan will also release its Q4 GDP data, with analysts expecting a 9.5% annualized increase, down from 22.9% in the previous quarter.

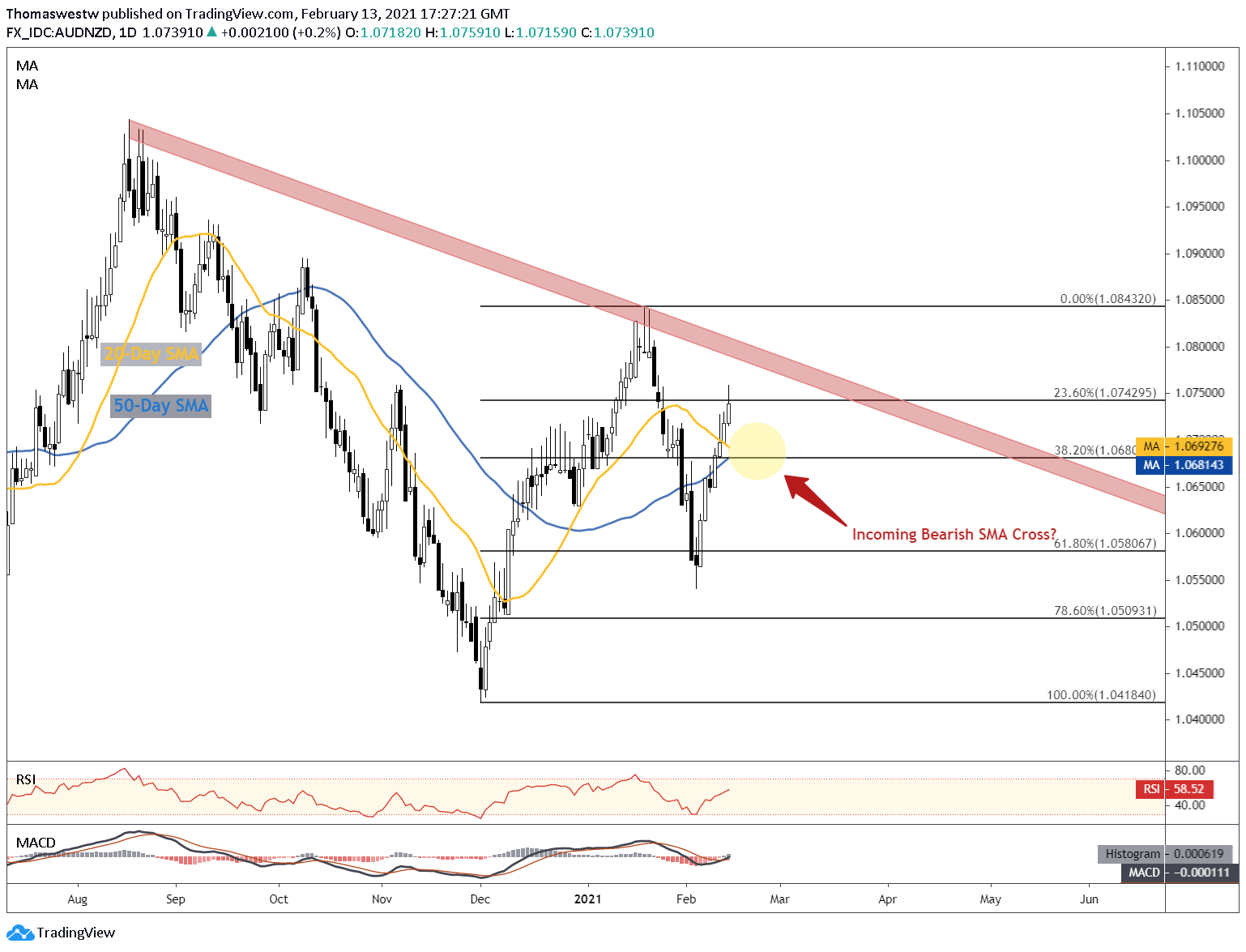

AUD/NZD Technical Outlook

Despite the holiday break and light economic data prints for the week ahead, AUD/NZD presents an interesting technical setup that may give way to actionable movement. The 23.6% Fibonacci retracement from the Dec – Jan move appears to have interrupted last week’s rally. However, the immediate path higher appears poised for further upside.

That upside may soon find significant resistance, however. The 20- and 50-day Simple Moving Averages appear to be on course to complete a bearish cross this week, which could dent AUD sentiment and hinder further gains. Moreover, a trendline from the August swing high also poses a test for bulls. Granted that, the MACD points to near-term upside, with a bullish cross above its centerline on the cards in the coming days.

AUD/NZD Daily Chart

Chart created with TradingView

AUD/NZD TRADING RESOURCES

— Written by Thomas Westwater, Analyst for DailyFX.com

To contact Thomas, use the comments section below or @FxWestwateron Twitter

Be the first to comment