Ninoon

(Note: This was in the newsletter on January 14, 2023.)

So far Medical Properties Trust, Inc. (NYSE:MPW) management is batting 1,000 with their guidance, and that includes main tenant Steward Health Care. The flip side of the coin is likely losing credibility very fast. It is not that the arguments themselves are not logical. It is more about the foundation of the arguments becoming exposed as something considerably less than sound.

Many times, in these disputes, both sides have impressive argument construction. The hard part is always finding out or analyzing where the logical weak part is. In this case, it appears that the suppositions are falling apart. But if the foundation of an argument structure cannot stand, then no matter how attractive the argument structure appears, it is worthless.

Updates

So, let us see what is shifting the debate. From what I can tell, there are three things to begin with.

The latest news was that Pipeline Health, as part of the bankruptcy settlement process, would pay the past due amounts. The contract itself remains in force. However, for those grasping at straws, a bone was thrown. Roughly 30% of the of the 2023 cash rent is deferred to 2024 as a loan to be repaid with interest. So, the bears have a brand-new starting point to begin yet another argument. There is also the proposed ample opportunity to pick apart the proposed construction of behavioral center.

Earlier in December, Steward belatedly announced that the line of credit was extended. The bear market argument that this was not going to happen with Medical Properties Trust incurring at least a contingent liability went out the window, because so far there is no SEC filing to indicate to the contrary a material change. Now, should there be something to this that would require a note in the financial statements, then it will be seen when the 10-K gets filed. But as of right now, Medical Properties Trust does not appear to be materially involved with the actions needed to extend the Steward credit line.

The third part appears to be the communications of management and some management activities or issues like the corporate jets. This appears to be by far the strongest bear argument. The third quarter earnings call transcript appears to have an unusually blunt comment about what management should be disclosing and how fast. With the jets, some things just plain look bad to investors, whether or not they are cost-justified. So, as a public company, sometimes some things are not worth the trouble that they cause.

Other Not So Minor Details

The above did not mean that was the whole story. There are plenty of other issues here that management could really have saved itself a whole lot of trouble by relentlessly (KISS) keeping it simple quarter after quarter, so it would not blow up into a bear raid. (Note: This is not meant to be a comprehensive list, as that would take a book.)

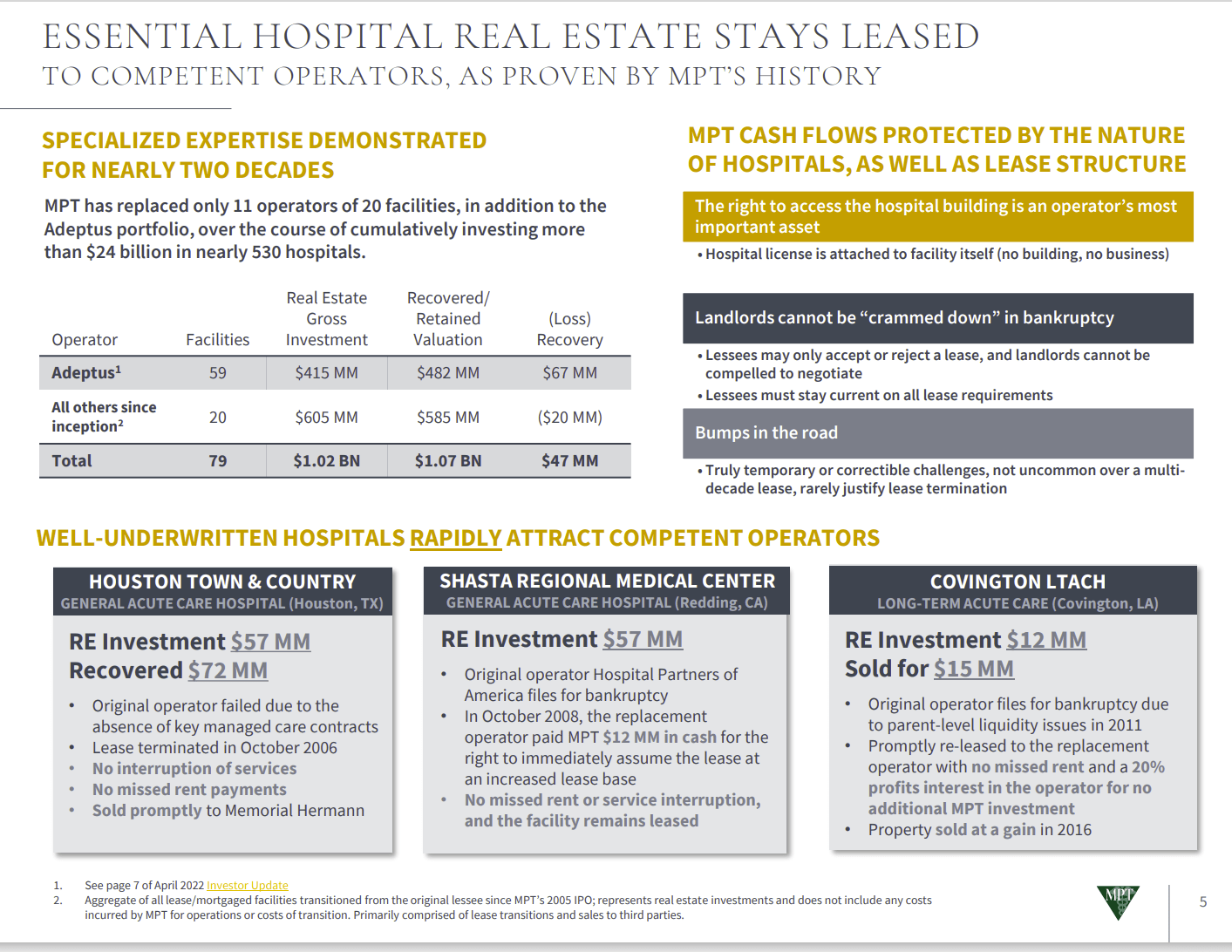

Probably the main issue here is considerable confusion about exactly what the company is concerned about with Steward. First of all, the important part is not Steward at all. It is whether or not management can replace any operator, including Steward, as needed and get the money it is owed.

As the Pipeline announcement demonstrates above, despite the bankruptcy proceedings, management is well on its way to getting every penny. The risk involved with deferring rent is definitely up for discussion, and the agreement on the behavioral center is likely to heat that discussion up more. But the fact is that management has had remarkable success getting every single penny, and there is nothing solid that indicates a future change.

Medical Properties Trust Presentation Of Steward Partnership History (Medical Properties Trust Third Quarter 2022, Earnings Conference Call Slides)

The first detail is that management has provided investors with a remarkable and very profitable history for doing business with Steward. Some would call this a solid business partnership even though it is not a true organized partnership in a literal sense.

There is no basis in the bear argument that the future would be different. There has long been a bear argument implication that Medical Properties Trust has dropped is due diligence requirements “because it is Steward.” But as of right now, that at least implied argument does not appear to have a solid foundation.

Usually that argument quickly transfers to Steward’s financial problems. But that misses the point that if management did their usual research, then any and all of Steward’s properties can be replaced with an operator while the company eventually collects the rent due. Now, the considerable block of business with Steward could potentially cause a cash flow issue that would prove temporary in the worst possible case.

But as the Pipeline case proved, many of these managements have bankruptcy planned ahead of time. So, bankruptcy itself usually wraps up fast and the operator is back in business.

One thing that appears to be out of the back-and-forth discussion is that Medical Properties Trust always has the right to take the property as a secured lender. Even if a bankruptcy were to unimaginably drag out, management could still remove properties from the operator and in effect reassign operators to minimize cash flow issues. A worst-case Steward issue would run up some lawyer bills and maybe delay some cash payments. But management would soon have the cash flowing again one way or another.

Going Forward

Unlike shareholders, the fear of inflation has got a lot of these secured lenders praying for defaults because the escalator costs in a lot of these contracts never saw inflation coming. Therefore, if there is a default and an operator has to be replaced, many times, the next contract is going to be better for the company than the one it replaced.

Medical Properties Trust Review Of Replacing Operators (Medical Properties Trust Third Quarter 2022, Corporate Earnings Presentation)

As an aside, the key thing about communication like this is the ability of management to demonstrate conclusively how the process works. By now, management should be getting the hint that Mr. Market needs constant reminding and lots (and lots and lots) of examples under his nose at all times.

So, while Medical Properties Trust, Inc. investors worry about a default, inflation usually has management with a “bring it on” attitude, because whatever replaces the current relationship is likely to prove more profitable in the future. Management really cannot communicate that point often (and loud) enough. I am forever amazed at the sheer number of investors talking about their view of rampaging inflation and then talk about the dangers of Steward defaulting and how bad that is for Medical Properties Trust. It certainly does not look bad to me in the long term even if there is a significant cash flow hiccup at the start.

But then, reality has to hit as the company reports very few even close to “worst case scenarios.” In the same time-period, there have been several decent results. This has to influence all the talk about Steward financials. The reason is that if management has done the proper due diligence for everyone including Steward, it is not the financials that matter as much as the inflation. Because the more inflation some investors talk about, the better the situation gets no matter what happens.

Medical Properties Trust, Inc. management appears to have done quite a bit of “homework.” So, the way things are right now, Medical Properties Trust, Inc. contracts will likely be honored, and management will have to wait until the end of the contract to catch up for any inflation an investor foresees. If that is the worst that happens, then Medical Properties Trust, Inc. stock is due for quite a rebound.

Be the first to comment