Avalon_Studio/iStock via Getty Images

The past year or so has been rather difficult for investors. Although there have been some companies that have performed exceptionally well, most have experienced some amount of downside. To be invested in a company that achieves even a modest amount of appreciation during a time when the market is down double digits is a victory in and of itself. And one company I could point to as an example of this is Mayville Engineering Company (NYSE:MEC), a firm that’s focused on offering a range of prototyping and tooling, production fabrication, coating, assembly, and aftermarket components. Because of robust fundamental performance, even during difficult times, shares of the company have done far better than the S&P 500 has. The exciting thing is that, given how cheap MEC stock still is, I believe that additional upside could be warranted from here.

Great relative performance

Well over one year ago, in December of 2021, I wrote an article discussing whether or not it made sense for investors to consider taking a stake in Mayville Engineering Company. At that time, I acknowledged that the company had done well to grow its top line over the prior few years. Even so, bottom line performance had shown some signs of deterioration. Fortunately, cash flows remained strong and the risk profile of the company looked favorable to me. Add on top of this how cheap shares were, and I had no problem rating the business a ‘buy’, a rating that reflected my belief that the stock would likely outperform the broader market moving forward. Fast forward just over 13 months, and I think it’s safe to assume that my call was a good one. While the S&P 500 is down 12.8% during that time, shares of Mayville Engineering Company have generated upside of 0.9%.

Author – SEC EDGAR Data

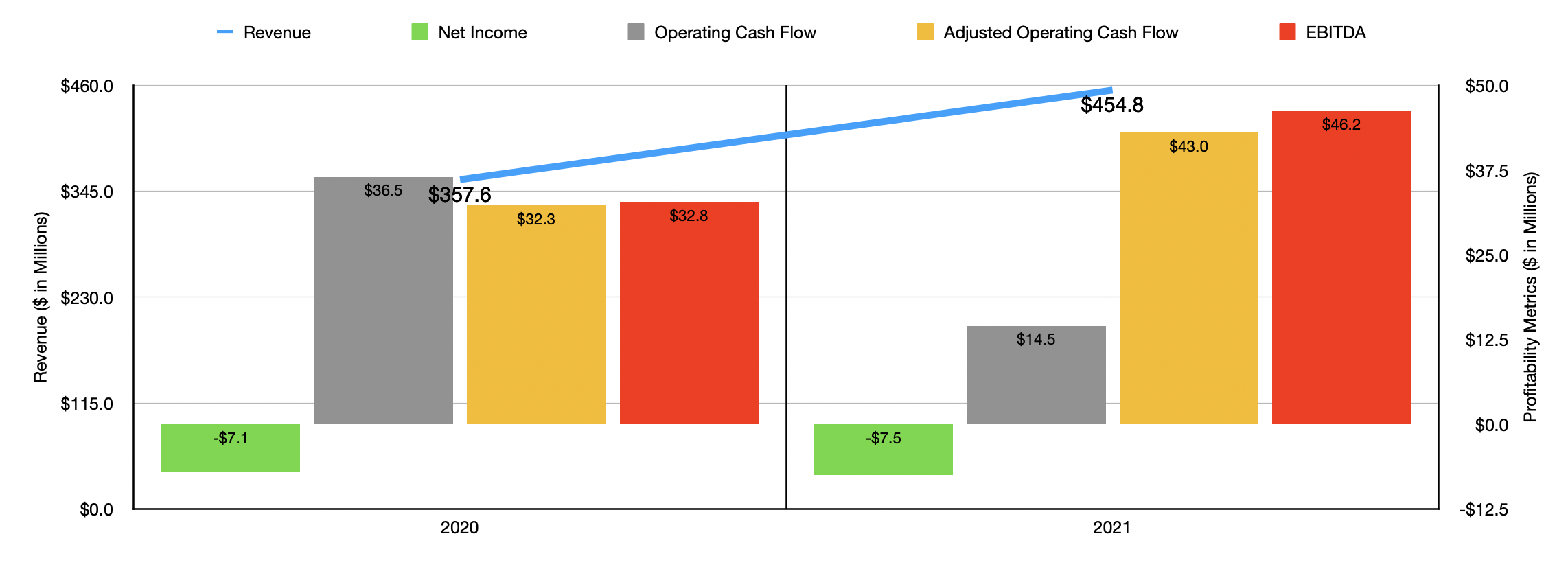

This return disparity is far from being a fluke. To understand why the company is performing this well, I think we should first discuss how it finished its 2021 fiscal year. During that time, sales came in at $454.8 million. That represents a significant improvement over the $357.6 million generated one year earlier. Management attributed this increase mostly to improved market conditions regarding the demand for its offerings, as well as commercial pricing increases implemented in the final quarter of 2021 aimed at combating inflationary pressures. Unfortunately, the firm did suffer some from customer supply chain issues and timing lag associated with contractual raw material price pass-throughs to its customers.

On the bottom line, the picture also improved. It is true that the firm’s net loss actually worsened, going from $7.1 million to $7.5 million. Operating cash flow also took a hit, going from $36.5 million to $14.5 million. But if we adjust for changes in working capital, it would have actually risen from $32.3 million to $43 million. Also on the rise was EBITDA. From 2020 to 2021, this metric rose from $32.8 million to $46.2 million.

Author – SEC EDGAR Data

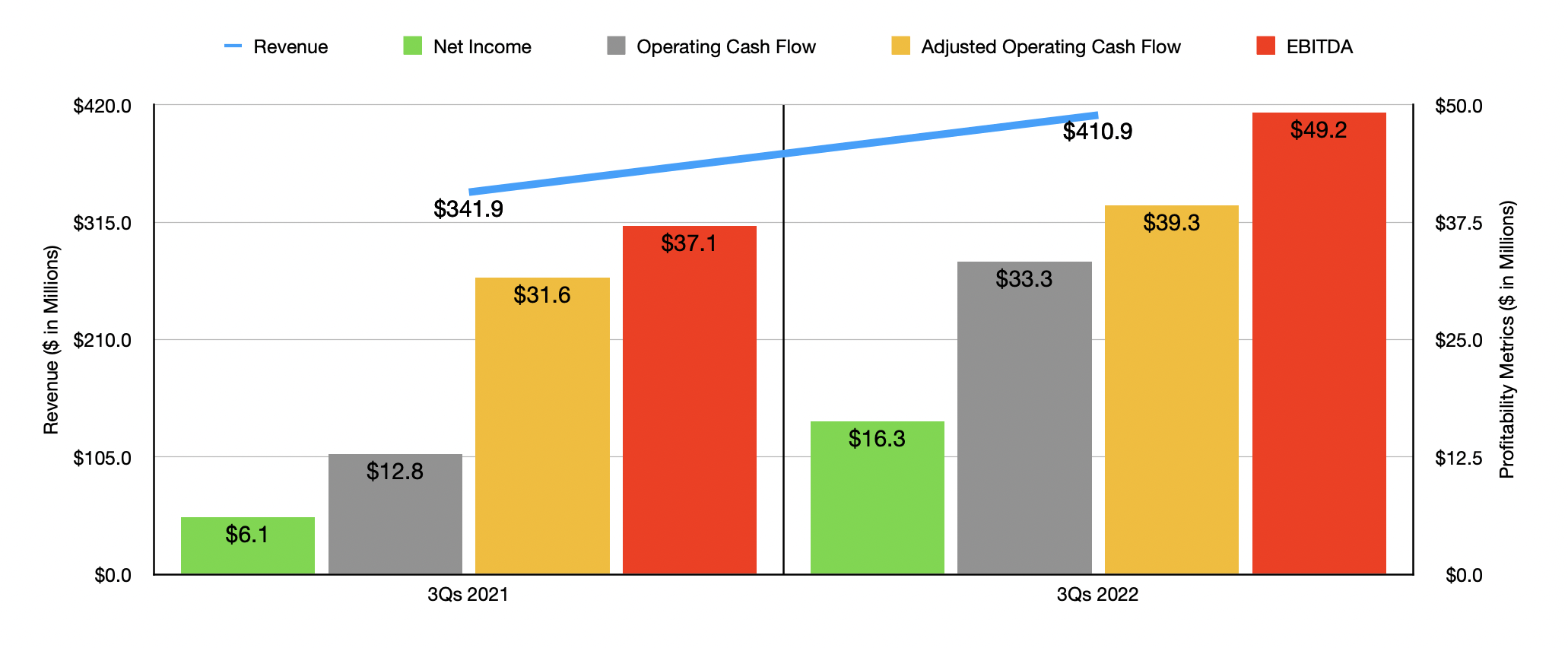

Fast forward to the 2022 fiscal year, and the results for the first nine months that have been reported look even better. Sales of $410.9 million beat out the $341.9 million reported only one year earlier. This increase, amounting to 20.2% year over year, was mostly driven by increased sales volumes associated with strengthened end-market demand and customer restocking efforts as dealer inventories remained at historically low levels. The firm also attributed this to commercial pricing increases and its ability to pass through higher costs onto its customers. With this surge in revenue came a sizable improvement in profitability. Net income jumped from $6.1 million to $16.3 million. Operating cash flow expanded from $12.8 million to $33.3 million, while the adjusted figure for this expanded from $31.6 million to $39.3 million. Also during this time, the firm saw its EBITDA improve, jumping from $37.1 million to $49.2 million.

For 2022 in its entirety, management said that investors should anticipate revenue of between $480 million and $530 million. Even at the low end, this would translate to a year-over-year improvement of 5.5%. On the high end, it would be 16.5%. When it comes to profitability, the only metric management gave guidance on was EBITDA. This should come in at between $58 million and $70 million. If we assume a similar growth rate for adjusted operating cash flow, then we should anticipate a reading for the year of $53.5 million.

Author – SEC EDGAR Data

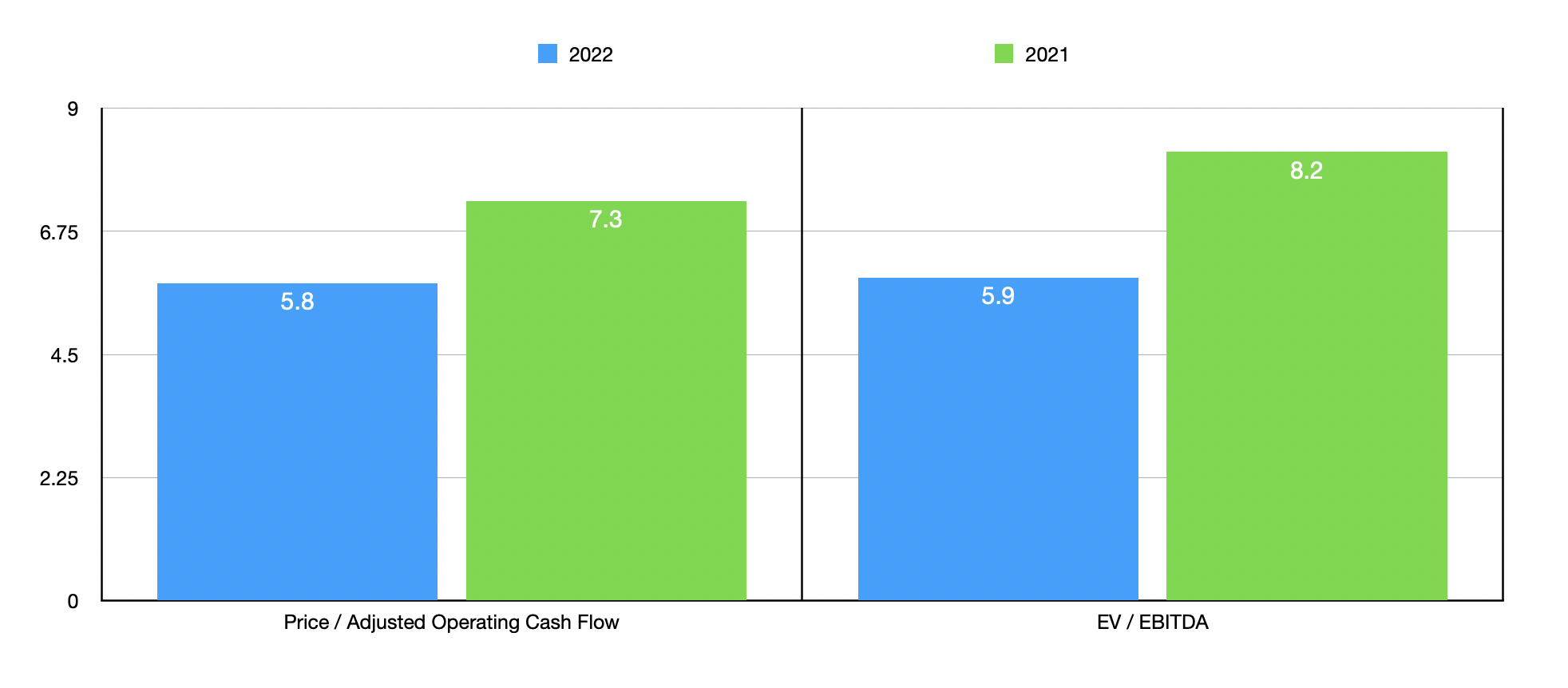

Based on the data provided, this means that the company should be trading at a price to adjusted operating cash flow multiple of 5.8 and at an EV to EBITDA multiple of 5.9. By comparison, if we were to use the data covering the firm’s 2021 fiscal year, these multiples would be 7.2 and 8.2, respectively. As I do with other companies that I analyze, I also compared Mayville Engineering Company to five similar businesses. On a price to operating cash flow basis, these firms ranged from a low of 5.7 to a high of 20.5. Mayville Engineering Company was cheaper than all of its peers except for one. Meanwhile, using the EV to EBITDA approach, the range was from 3.8 to 22.1. In this case also, only one of the companies was cheaper than our target.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Mayville Engineering Company (MEC) | 5.8 | 5.9 |

| Mueller Industries (MLI) | 5.7 | 3.8 |

| Crane Holdings, Co. (CR) | 15.0 | 9.9 |

| Parker-Hannifin (PH) | 18.1 | 22.1 |

| EnPro Industries (NPO) | 14.5 | 8.5 |

| Standex International (SXI) | 20.5 | 11.7 |

Takeaway

By all accounts, Mayville Engineering Company is performing exceptionally well right now. We don’t have any material evidence that suggests a meaningful slowing down of operations. Of course, this could always come to pass. But given how cheap the stock is, I have a hard time believing that we could reach the point where shares become overvalued. Because of this, I suspect that the company will continue to outperform the broader market moving forward. And as such, I have decided to keep the ‘buy’ rating I had on it before.

Be the first to comment