Thinnapob/iStock via Getty Images

Maxeon Solar Technologies (NASDAQ:MAXN) has an international presence, designing, manufacturing, and selling solar system components. Their TAM is large and continues to grow YoY. With customers ranging from small-scale companies to bigger and more established ones, the business model is highly scalable and can adjust to different demands.

But with a negative bottom line, the current share price isn’t trading on fundamentals, but instead hopeful future prospects. I think their future is exciting, and I am still optimistic. But this still makes think that selling any shares would be best, at least until we see a positive bottom line.

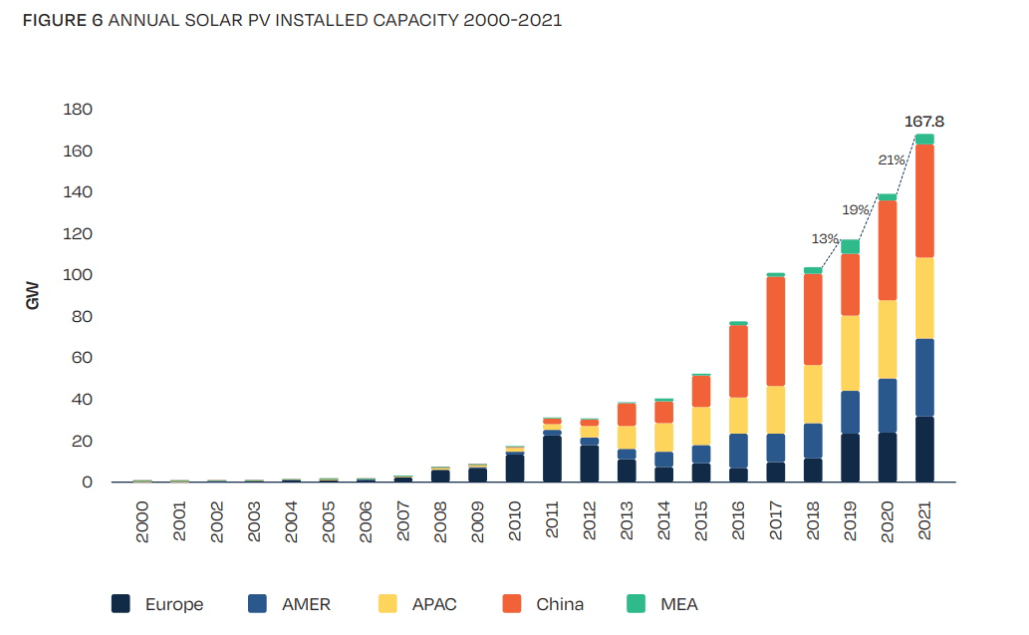

The Solar Market And Maxeon’s Role

The solar market is expected to grow at an annual rate of 20% for the next 10 years. With Maxeon being focused on solar installations for both industrial properties but primarily residential zones, they have so much future potential. The solar market is notoriously a very capital intensive market to get a foot in and establish yourself.

Solar Market Outlook (Maxeon Earnings Presentation)

But as there is more and more demand for solar modules, I would expect that Maxeon might be able to streamline their productions a little bit more. This would hopefully let the company have a lower operating expense and that would help the bottom line take a leap towards profitability.

An interesting point I have found about the residential part of solar adoption is that it’s incredibly underpenetrated. Even if the solar market is expected to grow at the rate it does, there would still be almost 90% of households in 10 years that won’t have solar panels. In my opinion Maxeon should be able to capitalize from this and become a much larger player than it already is, but again, they need to focus on increasing the bottom line and incentives investors to get on board.

Company Concerns

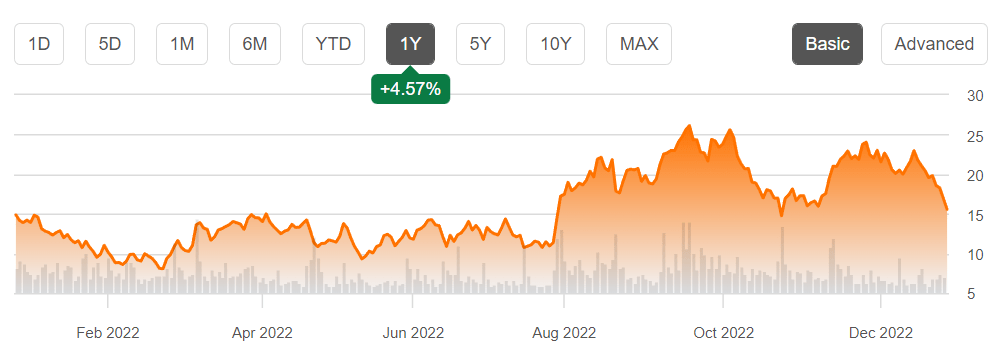

Maxeon Solar Technologies is a smaller solar company compared to a lot of other competitors in the space. With the market cap sitting at just over $1 billion there are a lot of large swings in the share price, like the recent run up. Compared to the rest of the market, however, investing in the company this year would have yielded around 6%. But there are significant risks with this company which I will go through a bit more further down.

Maxeon Share Price (Seeking Alpha)

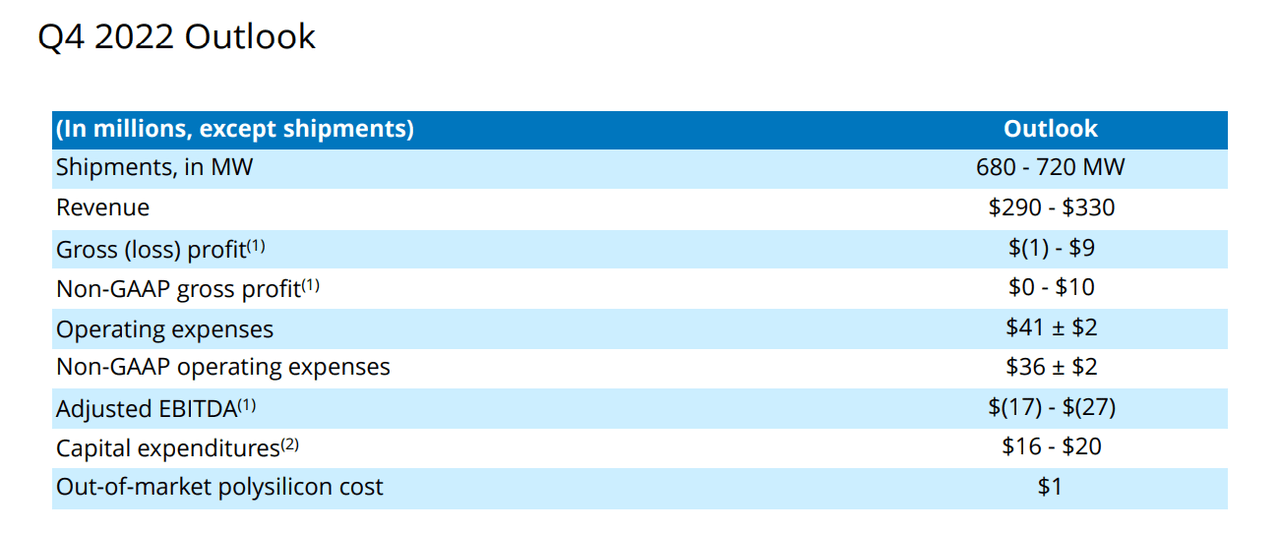

In the last earnings report that the company provided they forecasted to generate between $290 and $330 million, an almost 50% increase from last year’s same quarter. It might seem like a great deal, but that would disregard that the bottom line is not seeing the same increase.

Maxeon Earnings Outlook (Maxeon Q3 Earnings Report)

The bottom line of Maxeon has for a long time been suppressed. They are yet to achieve profitability and that worries me as an investor looking at the company. Maxeon is no longer losing the same amount as a few years ago so it seems they are on the right track. But with net margins sitting at -27% I think that patience will be key.

Besides having quite honestly horrible margins, Maxeon has some other red flags too. One that particularly stands out to me is the negative cash flows. They’re not seeming to get better in my opinion which worries me that share dilution will continue to happen.

Valuing Maxeon Solar Technologies

It’s hard having a number and value on what Maxeon is worth. With most companies that have such negative margins I often stay away from them entirely. With negative EPS that makes it hard to argue why you should pay anything above 1 cent per share from a value perspective. Looking at the price/book the company is trading at over 8 compared to the sectors average of 3. I think that solar related companies are generally a bit more richly priced because of investor optimism. But a p/b ratio of 8 is too high to pay in my opinion, under 1 and you would be getting a great deal.

In the case of Maxeon, I will wait until I can get a clearer picture about how the path to profitability might look. It’s an exciting company that has a booming market to be a part of.

There are some things I would watch out for in the next few quarterly reports Maxeon will provide. Looking at the pace at which operating expenses increase in relation to revenues would be a good one. But also seeing the order backlog the company has, that gives me a good idea about how much demand they are seeing and whether there are any hiccups in terms of manufacturing the product and getting sent out.

Conclusion

Maxeon Solar Technologies is a company operating in the solar energy sector. They manufacture and sell solar modules that get installed in both residential and non-residential zones. They are growing revenues at an impressive pace, increasing 50% YoY in the last earnings report.

Even though revenues are increasing at a good pace, the bottom line is not feeling the same pace. Without good margins it’s hard to run a business for the long term. With net margins sitting at -28% it’s hard for me as an investor to justify putting any money into this company. Until that number gets much closer to 0, I wouldn’t recommend anyone thinking about investing.

Lastly, the valuation for me is just way too rich. I expect that they won’t be profitable for at least another 4-5 years. I hold realistic valuations as one of my most important investment pillars. With a negative EPS that’s not expected to turn positive for a while, investing right now is “dead money” and the downside risk is so much higher than the potential return. Because of all of these reasons I will not invest any capital into Maxeon Solar Technologies, and would suggest investors sell their position.

Be the first to comment