nattul

Marvell’s (NASDAQ:MRVL) announced CFO reshuffle last week came as a surprise, but should have a limited impact on the investment case. New CFO Willem Meintjes has been groomed to take the helm for a while now, and the transition should be seamless. The election of a new CFO does, however, mark an important strategic shift – having built an exceptionally strong franchise through acquisitions like Cavium and Inphi, the focus is (rightly) shifting from extending the inorganic growth runway to post-M&A integration (e.g., delivering ~$125m in run-rate synergies from the Inphi deal).

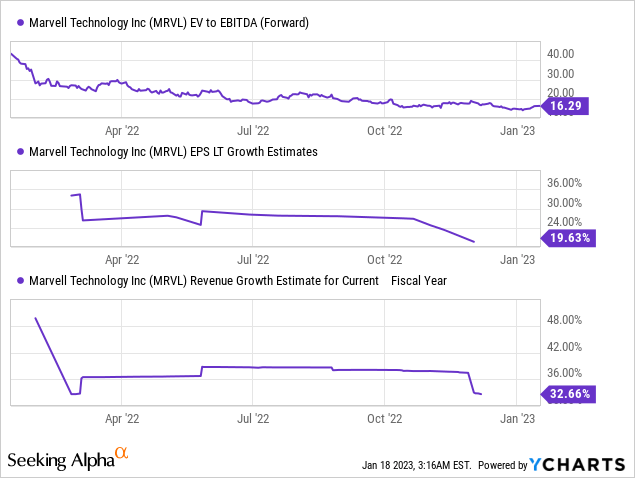

In the near term, MRVL will need to navigate challenges in the key data center end market, but the guidance reset in the last quarter has lowered the bar significantly. And over the mid to long term, the company remains in a great position to tackle massively expanded addressable market opportunities across storage, networking, and embedded processing. In light of the narrowed guidance range at $1.4bn +/- 3% (vs. +/- 5% prior) and upbeat data center commentary from TSMC (TSM), I suspect we could be nearing a YoY bottom for data center sales. The stock isn’t particularly cheap at ~16x EV/EBITDA, but relative to the ~20% fwd earnings CAGR, there remains upside potential from here.

CFO Change Marks an Important Strategic Shift

Over the last week, MRVL announced the appointment of Willem Meintjes as CFO following the resignation of former CFO Jean Hu, who will be taking on the CFO position at Advanced Micro Devices (AMD). For context, new CFO Meintjes has served as the Chief Accounting Officer and Treasurer since 2018, so he has been groomed for some time now. Of note, his tenure at MRVL has lasted as long as the current CEO and CFO, which means he has worked on the multi-year business transition engineered by Ms. Hu, as well as key acquisitions such as Cavium, a developer of ARM and MIPS-based system-on-chips (SoCs), and Inphi, a manufacturer of chips that facilitate high-speed data transfer.

Importantly, the CFO change coincides with a strategic shift at Marvell. Having successfully executed an inorganic growth playbook in recent years, MRVL will now focus on integrating its acquired assets and driving organic growth across the portfolio. That doesn’t mean the company will stop M&A entirely. The company’s $723m cash position as of Q3 (vs. ~$51m in dividends and ~$50m of buybacks) means it still has the dry powder to capitalize on an interest rate-driven valuation reset across the industry. Instead, any new acquisitions will likely be complementary (vs. transformational) tuck-ins and smaller in size. All in all, the latest CFO change shouldn’t affect the status quo, and thus, I feel comfortable underwriting the midterm outlook.

Revenue Guidance Range Narrowed as Q4 Looks to be Shaping Up Well

Alongside the CFO disclosure, MRVL also narrowed its guidance range for Q4, signaling that the quarter is progressing according to plan (note there are only ~2 weeks to go in the quarter). Recall that this update comes on the heels of a major revenue guidance reset to $1.4bn (down 9% QoQ and up 4% YoY) in the prior quarter amid data center demand weakness. In particular, HDD/SSD storage was a major drag on the P&L, in line with commentary from the rest of the storage industry, followed by cloud networking. While this is likely a transitory inventory adjustment issue rather than a structural one, the sharp guidance reset likely means this part of the business has been sufficiently de-risked heading into Q4.

The case for a more benign data center outcome is consistent with the messaging from MRVL at the CES conference (transcript here). Management acknowledged that the data center news flow had been far from positive over the last month, with even TSM citing incremental data center weakness at its earnings call. But management feels it has embedded this weakness in its updated segmental guidance at down ~50% Q/Q (vs. the ~$200m/quarter run-rate prior); thus, even in a bear case scenario where customers aggressively pare down their inventory, there shouldn’t be negative surprises from here.

TSM Earnings Call Validates the Case for a More Benign Semiconductor Cycle

As the bellwether of the semiconductor industry, TSM’s earnings commentary carries a lot of weight when analyzing companies across the value chain. The recent Q4 earnings call, for instance, provided several key insights. For one, TSM management sees a destocking cycle weighing on the H1 outlook, extending the Q4 trend (note sales came in at the lower end of prior guidance). This is to be followed, however, by a rebound in H2 as new customer platforms drive demand, with an implied double-digit % growth in H2 relative to the H1 base. So while we are in the midst of a semi downturn, this down cycle likely won’t be too severe.

The read across for MRVL is positive, validating management’s confidence in the enterprise storage outlook as the semi-custom (hyperscale ASIC) and Innovium switch businesses begin to ramp up. With MRVL also exposed to tailwinds in the high-performance compute segment, which TSM cited as a key growth driver, the company should comfortably overcome lingering automotive supply headwinds. With consensus across both companies being for stockpiles to clear within the next two quarters, easing inventory levels should also allow MRVL to clear its targeted 64-66% gross margin model (vs. 64% in Q3). Incremental operating leverage benefits from revenue growth present further upside to the earnings growth model.

Fade the CFO Reshuffle

The recent CFO change will add some uncertainty, but I see a smooth transition given Meintjes’ tenure at the company and the shift in focus toward integration over more M&A. While the near-term outlook will be challenged by data center headwinds, the bar has been reset lower in Q3, and recent commentary from TSM points to potential upside in the coming quarters. The current ~16x EBITDA valuation seems pricey at first glance, but given the quality of the MRVL franchise and the strong growth outlook, there remains ample upside here.

Be the first to comment