It’s time to talk about MarketWise (NASDAQ:MKTW). In August of this year, I started covering this company. Back then, I wrote that this financial services provider didn’t offer a compelling bull case. That was based on a competitive environment and weakness in its customer base – among other reasons. Since then, the stock has lost more than 45% as headwinds started to get worse. The just-released earnings confirm my worries. In this article, we are going to discuss all of this and look into MarketWise’s ability to offer investors the opportunity to go dumpster diving.

On a side note, even if you don’t care for MarketWise, I included a lot of market trends and comments in this article, which tells us a lot about the health of the “average” trader and the industry.

So, let’s get to it!

What’s MarketWise?

With a market cap of $64 million, MarketWise is now a micro-cap stock. Hence, it makes sense to start with a short overview of the company, as I doubt that it’s a well-known company.

One of the reasons why I cover MarketWise is the fact that I know a thing or two about sell-side and third-party research as I have spent the biggest part of the past 10 years in this business.

It’s a competitive industry that goes well beyond just delivering good research.

Anyway, before we get into that, let’s look at some facts. MarketWise was founded in 1999, with a mission to level the playing field for self-directed investors. Also known as retail investors. Leveling the playing field is a great purpose, especially back then when the early years of the internet provided larger investors with much more opportunities to thrive in the trading and investing world.

Especially in the past few years, MarketWise has invested in new capabilities. It now has 11 customer brands, 180 products, more than 100 people in its editorial team, more than 800 employees, and new tech capabilities.

MarketWise

As I wrote in my August article:

A website like InvestorPlace offers articles for investors to make their own decisions with a history of multiple decades, while Chaikin is a more data-focused service with an automated rating system. TradeSmith is somewhere in between with a selection of daily graphs and investment research that help retail investors to make decisions.

MarketWise

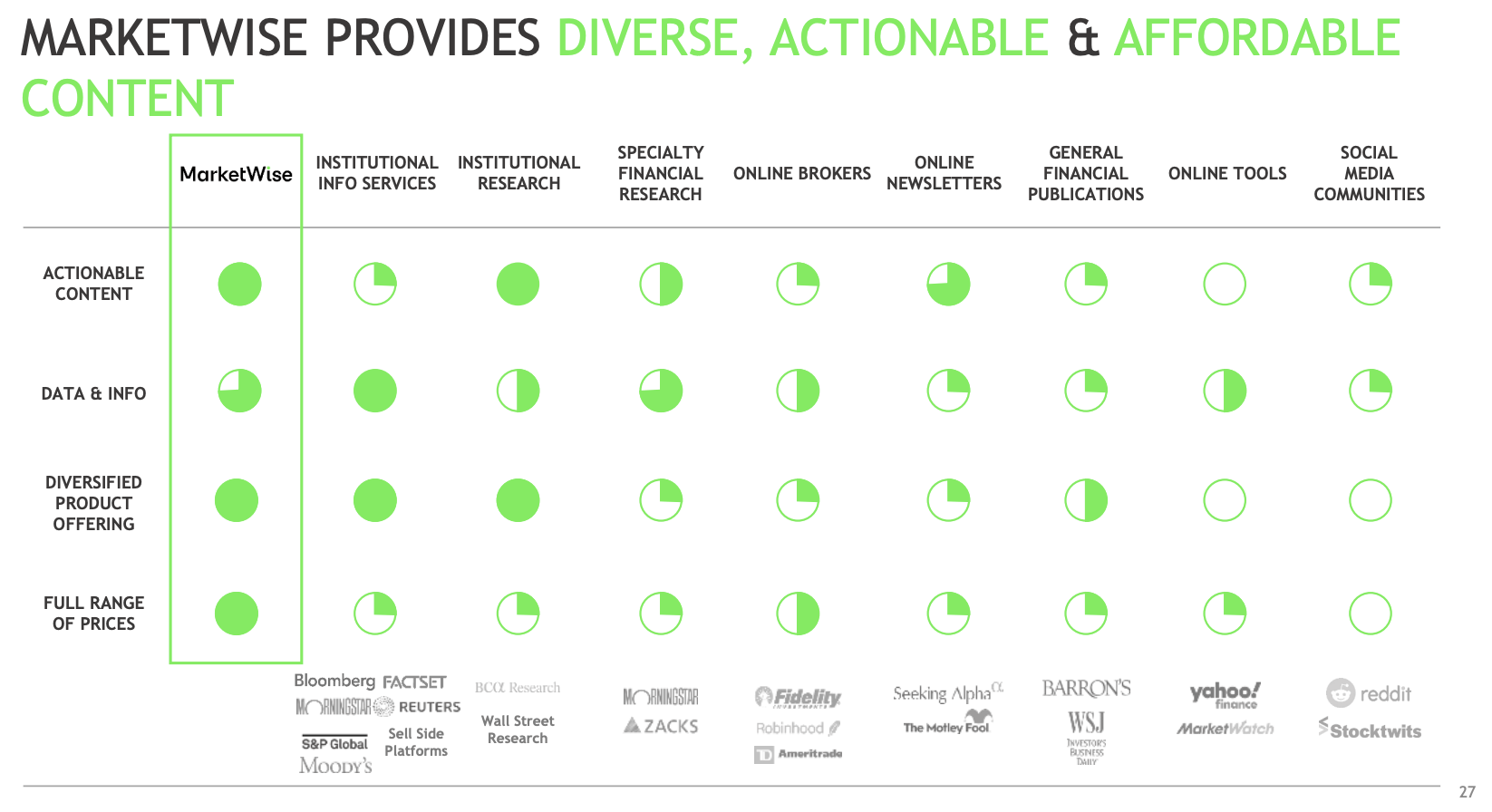

Essentially, the company believes that it offers a full range of products that its competitors cannot compete with. For example, the company beats everyone, except for Wall Street sell-side firms when it comes to actionable content (according to MarketWise!).

MarketWise

Given this list and my own experience, I have to say that I disagree with this list. For example, the company does not offer significantly better info than its peers in the online newsletters segment, one of them is Seeking Alpha. I’m obviously not paid to say that. The same goes for product diversification, competition has become so strong that it’s impossible to make the case that MarketWise stands out. I do, however, believe that the company offers a very broad number of services in different price ranges.

Nonetheless, this doesn’t necessarily give the company an edge as it’s hard to compete in service. In today’s environment, investors use multiple sources to establish their own market views and strategies. Offering an endless range of products doesn’t necessarily end up improving the competitive edge.

For example, I pay various websites for information. Mainly news and data websites that allow me to form my own opinions. I don’t need a single provider. I get whatever I need from multiple sources.

Moreover, having worked with institutional research, the company does not have better data and info. We’re now talking about expensive information from major sell-side companies, but ignoring pricing, data isn’t better.

I can continue, but as my goal isn’t to make MarketWise look bad, the key takeaway here is that competition is fierce. Moreover, entry barriers are very low, and I can name at least 10 more serious sell-side companies that offer retail services at competitive prices, that are not included in the comparison above.

What Happened In 3Q22?

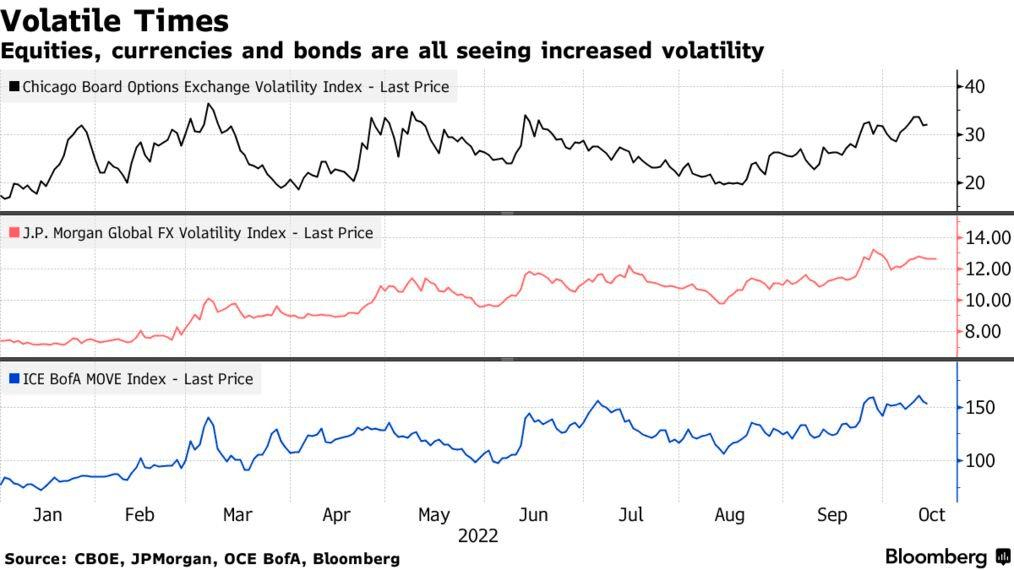

The third quarter was a mess. In general, retail investors have a very hard time this year. Volatility is high in every single market: stocks, currencies, and bonds.

Bloomberg

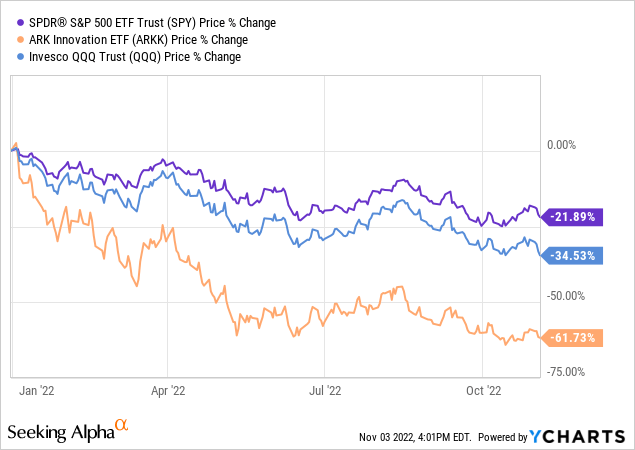

Moreover, the S&P 500 is down 22% since the start of the year. The tech-heavy ETF (QQQ) is down 35% during this period. The retail darling of 2020, ARK Innovation (ARKK) is down 62%.

While it looks like I’m stating the obvious here, I just want to show how tough it is for traders to make money. Markets have been in a steady downtrend this year and high volatility quickly gets rid of traders who lack discipline.

As a result, total billings in 3Q22 were $105.1 million. That’s down from $117.5 million in the second quarter and down from $138.1 million in the prior-year quarter.

The company is also losing paid subscribers but winning new unpaid subscribers. That makes sense as people want to know what the market is up to. Paying for it is a different story – especially in this market environment and given high inflation. People often lack the funds to pay for third-party research.

Paid Subscribers were 894K as of September 30, 2022, compared to 898K in Q2 and 965K in Q3 2021.

Free Subscribers were 15.4M as of September 30, 2022, compared to 15.0M in Q2 and 12.8M in Q3 2021.

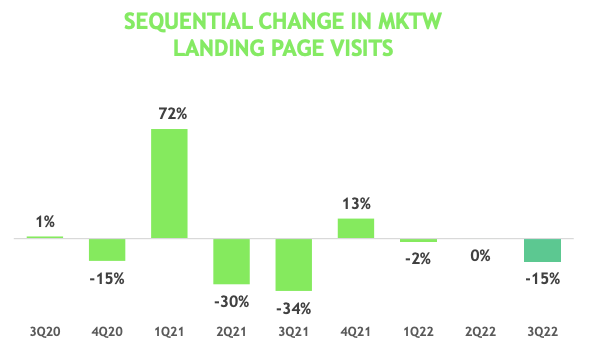

These numbers make sense as it follows the bigger picture. In the third quarter, the average number of daily trades on Charles Schwab (SCHW) fell by 11% (versus the prior quarter). That’s the second consecutive decline after a 5% decline in the second quarter. MarketWise landing page visits fell by 15%, which marks the third consecutive quarter without growth. Since 3Q20, the company had just three quarters showing positive growth. One of these showed 1% growth.

MarketWise

According to the company, prospective and existing subscribers are still assessing the environment and not yet re-engaging at more historically normal rates. As we briefly discussed, that was to be expected as consumer incomes are under pressure, the market is volatile (scary to some), and returns have been abysmal this year.

The company made clear that it shifted its content to address current market conditions as it ran campaigns focused on energy, inflation, global macro, and investing for current income and options trading.

As I’m not a subscriber to any of its services, I’m not commenting on the quality of its content. However, what I can say is that the company saw a new high in cumulative spending, meaning existing customers added more services. That’s a sign of customer satisfaction, and I think it makes current weakness really the result of macro weakness instead of anything worse that could hurt the company on a long-term basis.

With that said, the year-on-year comparison of the GAAP numbers is somewhat tricky. Total revenues declined by 15% as a result of headwinds in the industry and the aforementioned factors. However, operating expenses declined by 81%, allowing the company to grow operating income from a $373 million loss to a $22 million gain. These numbers are caused by last year’s stock-based compensation expenses related to the 2021 Incentive Award Plan and SBC expenses related to the Class B Units of $412.6 million in 3Q21.

With regard to these costs, the company did update on its cost reduction program, which is set to make a rather large positive impact at a time when cost issues are hurting a lot of service-based companies.

As previously disclosed, the Company initiated a cost reduction program in June 2022, targeting $74 million of total expense savings, through a reduction in both overhead and direct marketing expense. In total, we anticipated reducing overhead by an annualized amount equal to approximately $37 million, or 15% of 2022 budgeted overhead. Through the third quarter, we achieved $8 million of overhead reductions in the run-rate of expenses, or $31 million annualized, as compared to first quarter 2022.

Moreover, cash generation remains strong. The company did $13.1 million in adjusted cash from operations. That is down from $34.7 million in the prior-year quarter as a result of lower billings, yet the conversion rate remains at 99.9% as the company does not rely on capital spending. But then again, more than 30 thousand fewer billings caused the free cash flow yield to drop to 12.5%. That’s down from 25.2% in 3Q21.

MKTW Stock Valuation

This is hands down, the trickiest part of the company. We’re dealing with a company that has a market cap of $65 million. The company has assets worth $435 million. $147 million of that is cash. Total liabilities are $763 million, and almost all of it is deferred revenue as a result of its membership structures.

Moreover, while normalized EPS is not expected to grow, the company is trading at just 5.2x normalized EPS.

TIKR.com

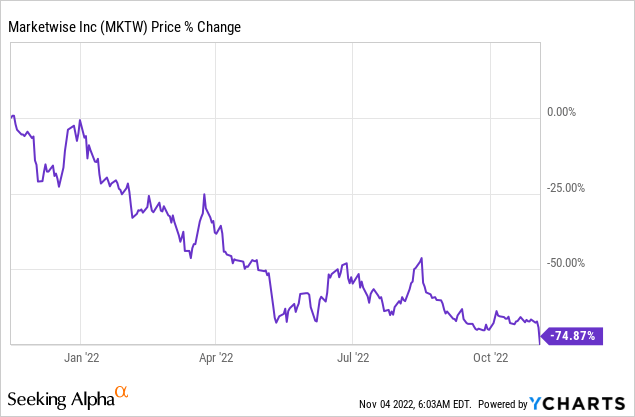

Without looking at the bigger picture, one can make the case that MarketWise is an interesting play. The company is down 75% from its IPO price. However, the company was already rather cheap when I covered the stock in August. Yet, it continued to drop like a stone.

MarketWise isn’t going away. It’s too strong for that. The company has a rather mature business portfolio and core customers that keep the lights on.

However, this year, nobody found a good reason to invest in the company. And given my prior comments, I’m one of these people. Market fundamentals are not at all supportive of customer growth in the months ahead, and things could get even worse if economic challenges remain persistent.

With that said, as I said in my prior article, MarketWise could double or triple in the years ahead and I would look like an idiot. However, so far, I’m glad I didn’t buy, and I do not recommend investors start buying now.

The only reason I see for buying shares is for traders who like to take huge risks. Let’s say the Fed pivots in early 2023, causing the market to rebound based on higher investor sentiment. In that scenario, I have little doubt that MKTW shares will rebound rapidly.

However, who knows where these shares are trading once that happens?

It’s not a risk I’m willing to take.

Takeaway

In this article, we discussed MarketWise. A company I started covering a few months ago. The company is struggling as it is losing customers in an environment of high volatility, a significant stock market downtrend, and high inflation, further pressuring household incomes.

That’s bad in general, however, the market environment is challenging, in general. Competition is fierce, entry barriers are low, and customers can change their minds within minutes.

However, the company continues to have a healthy balance sheet. It has a core of loyal customers that continue to add services, making the case that quality is not a problem.

Free cash flow generation remains high, even though margins are pressured by a steep decline in billings.

While there is a case to be made to buy MKTW equity for investors who love (very high) risks – or at least who don’t shy away from these risks – I continue to stay away as I don’t see a great long-term risk/reward.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment