Vadmary/iStock via Getty Images

The FOMC meeting wasn’t as dovish as the market wants to make it seem. The Fed raised rates by another 75 bps, and Powell repeated on several occasions throughout the meeting that FOMC projections of 3.8% for 2023 are probably the best estimate of where the committee’s thinking is still on the terminal rate.

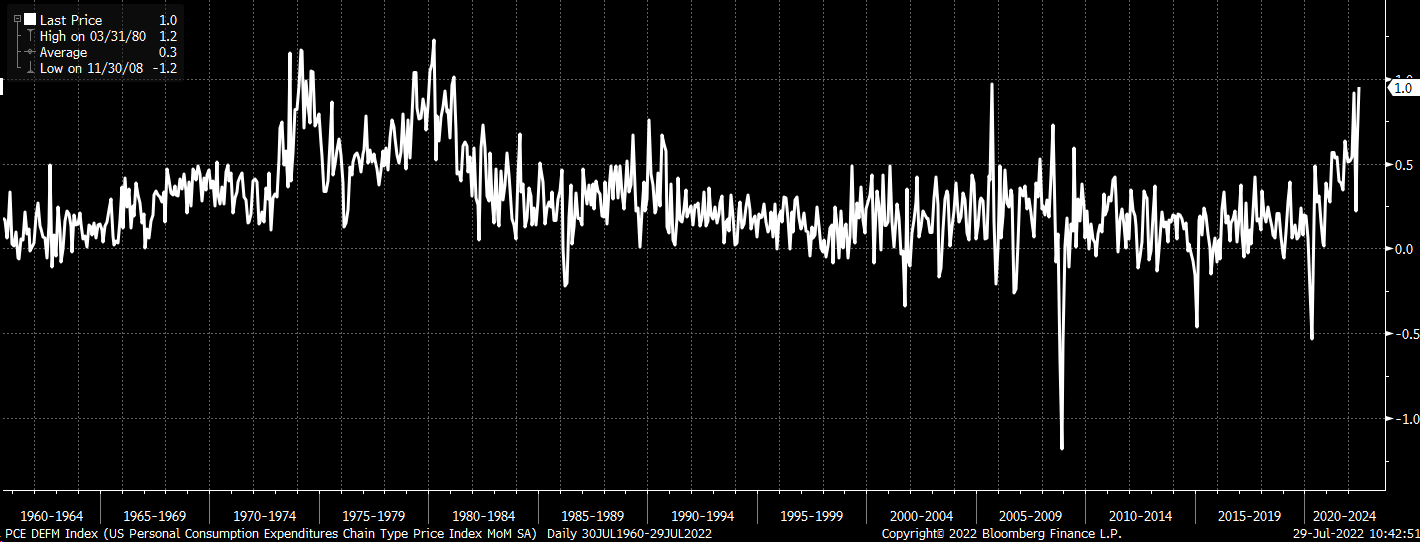

The bottom line is that the Fed remains on course, and the latest economic data from today suggest that the long-term path for rates remains on track. Today’s PCE reading month-over-month rose by 1%, the highest value in this cycle and one of the highest since the 1980s.

Bloomberg

However, the market is dreaming about a Fed pivot that doesn’t exist. The market has decided that inflation has peaked and that the Fed will not be able to raise rates nearly as high. After all, we’re now in a “recession.”

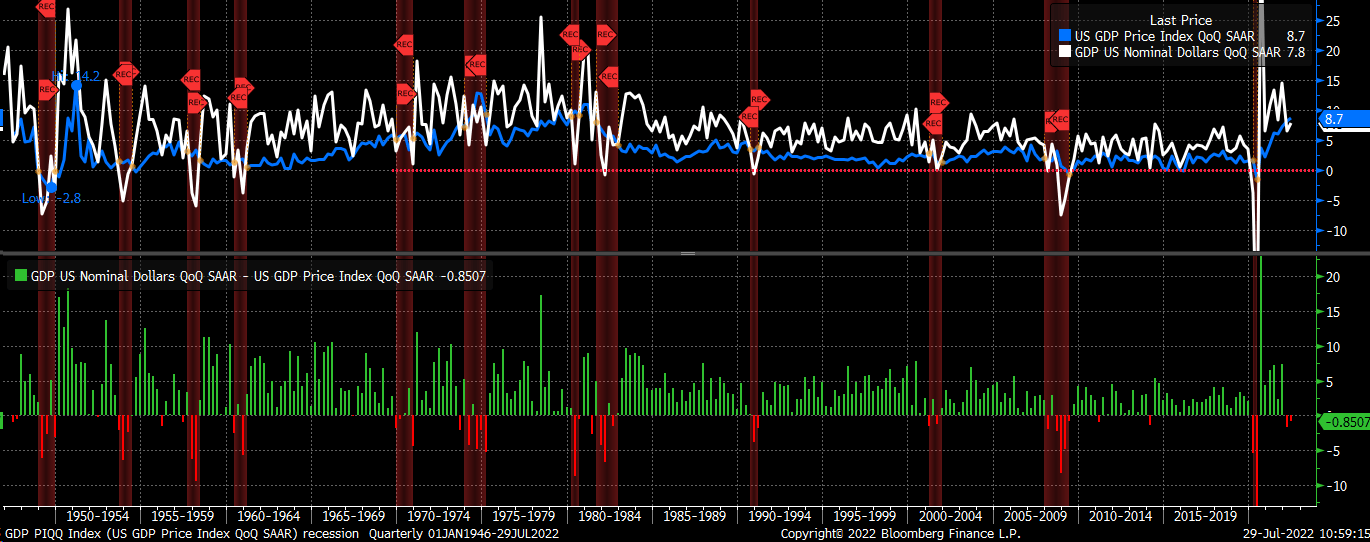

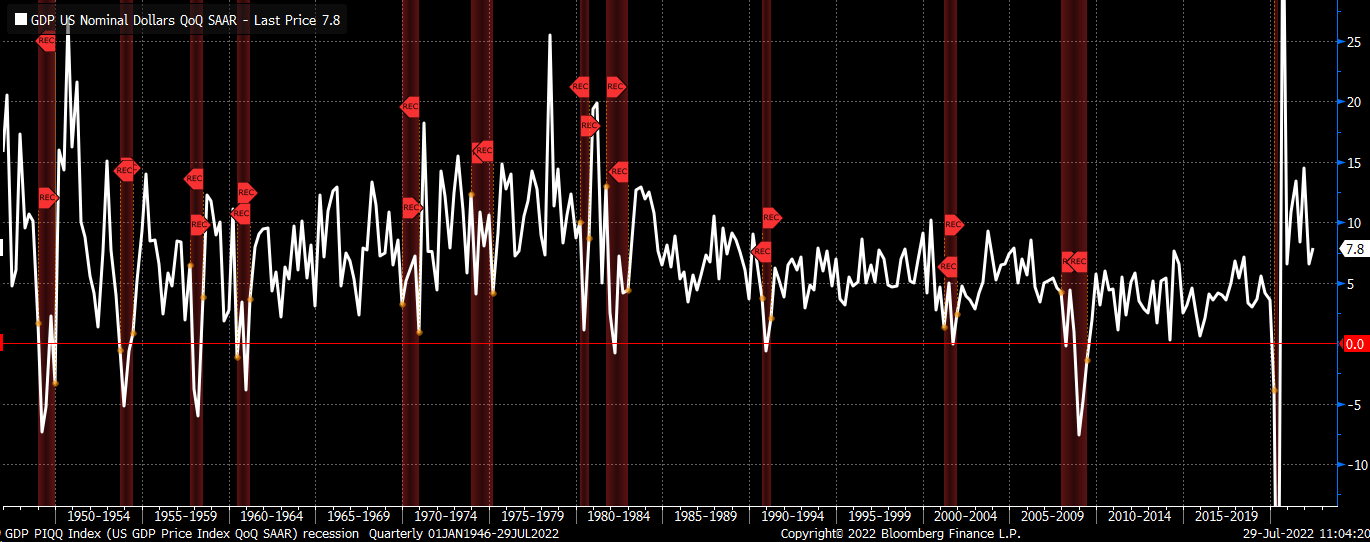

But the recession is caused by high prices, not because demand has deteriorated. Nominal growth rose by 7.8% in the second quarter, up from the first quarter’s growth rate of 6.6%. The negative real GDP print was due to the 8.7% increase in the price index.

Bloomberg

What’s interesting is that typically during a recession, the nominal growth rate trends lower, not higher. Usually, that nominal growth rate goes below 0%, too; it even occurred in the 1970s, when inflation rates were just as high. At this point, it’s tough to say that the economy is in an actual recession. Perhaps it’s the start of one, and nominal GDP will begin to decline. As of right now, that’s not evident.

Bloomberg

Dreams

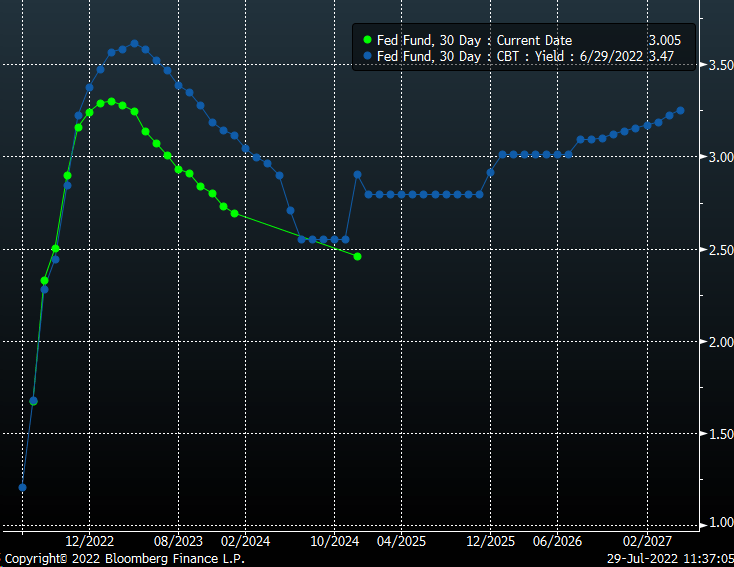

But because the market views the economy as heading toward or in a recession. The Fed fund futures are pricing in the first set of rate cuts in March 2023 and see the terminal rate rising to around 3.3%, which is nearly 50 bps less than the Fed’s projections and what was re-iterated during this July meeting.

Bloomberg

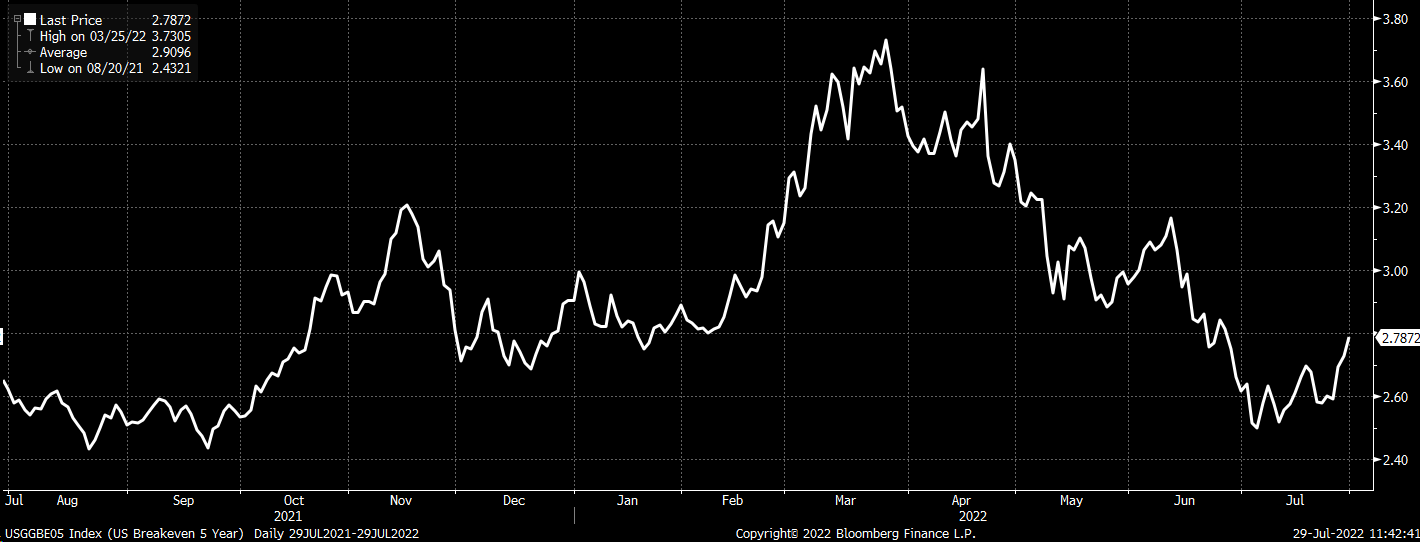

These expectations sent Treasury rates down sharply, especially in the middle of the yield curve around five to seven years. But the hotter-than-expected inflation data today and the past couple of weeks has caused inflation expectations to begin to rise again, with five-year breakeven inflation rates rising back to 2.79% due to real yields falling.

Bloomberg

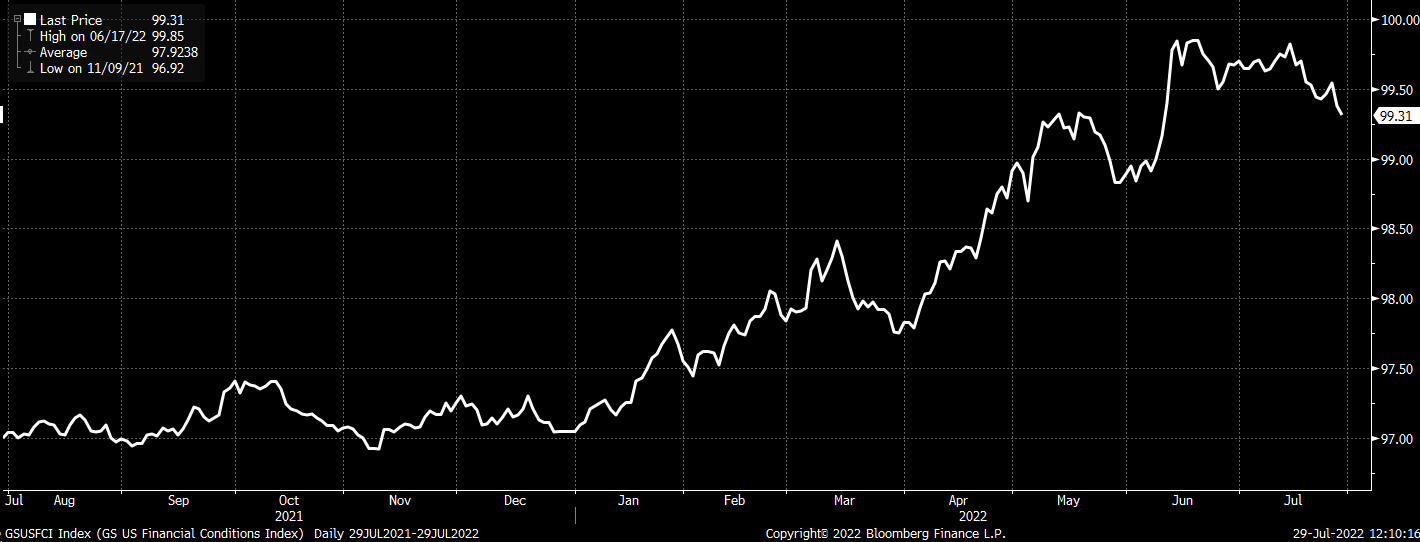

All of this, of course, is working to help lift equity prices and bring a risk-on mentality into the market, which in reality is working to ease financial conditions, which will work against the Fed’s policy objectives. Remember, the Fed wants tighter financial conditions. It will just create more work for the Fed to do at a later date in time.

Bloomberg

No Pivot

The Fed’s data dependency path for the September meeting could lead to more market volatility because economic data will be crucial between now and September. The first test will come next week with the Job’s report. The Fed will not be there to hold the hand of the market through the journey and tell it exactly what will happen next.

The more the market prices in a Fed ease, the more financial conditions ease, the more likely it is the Fed will hit back, and the farther the equity market will need to fall.

Join Reading The Markets Risk-Free With A Two-Week Trial!

(*Free Trial offer is for qualifying subscribers only – consult with the checkout page to see if the offer applies)

Reading the Markets helps readers cut through all the noise delivering stock ideas and market updates, looking for opportunities.

We use a repeated and detailed process of watching the fundamental trends, technical charts, and options trading data. The process helps isolate and determine where a stock, sector, or market may be heading over various time frames.

Be the first to comment