everythingpossible

A Quick Take On Mangoceuticals

Mangoceuticals, Inc. (MNGO) has filed to raise $5 million in an IPO of its common stock, according to an S-1 registration statement.

The firm seeks to operate an online telemedicine platform for men’s wellness products and services.

Given the company’s pre-revenue status, selling shareholders and thin capitalization, I’ll pass on the IPO.

Mangoceuticals Overview

Dallas, Texas-based Mangoceuticals, Inc. was founded to develop a men’s erectile dysfunction product and related online telemedicine platform to connect men with wellness service providers.

Management is headed by Chairman and Chief Executive Officer Jacob D. Cohen, who was previously Chief Financial Officer of The Renewed Group, an apparel manufacturer.

As of September 30, 2022, Mangoceuticals has booked fair market value investment of $2.2 million from investors including individuals.

Management plans to use a variety of marketing channels such as social media, television, radio, and online search to drive traffic to its website.

The company also intends to offer subscription plans for the purchase of its products.

Mangoceuticals’ Market & Competition

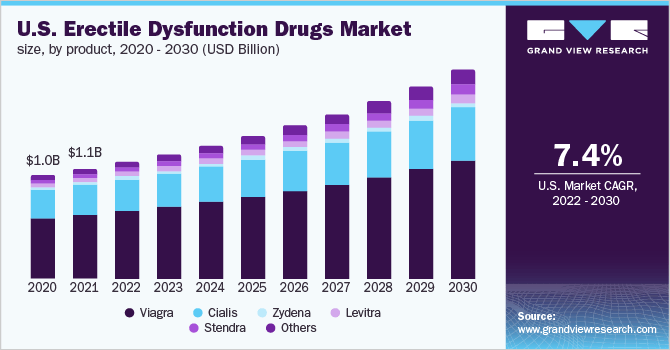

According to a 2022 market research report by Grand View Research, the global market for erectile dysfunction drug treatments was an estimated $2.3 billion in 2021 and is forecast to reach $4.8 billion by 2030.

This represents a forecast CAGR of 8.5% from 2022 to 2030.

The main drivers for this expected growth are an aging male population combined with a predominantly sedentary lifestyle.

Also, below is a chart showing the historical and projected future growth trajectory of the U.S. erectile dysfunction market:

U.S. Erectile Dysfunction Drugs Market (Grand View Research)

Major competitive or other industry participants include:

-

Pfizer (PFE)

-

Eli Lilly and Company (LLY)

-

Teva Pharmaceutical Industries (TEVA)

-

Sanofi (SNY)

-

Sun Pharmaceutical Industries

-

Bayer AG (OTCPK:BAYZF)

-

Petros Pharmaceuticals (PTPI)

-

VIVUS, Inc. (OTCPK:VVUSQ)

-

Auxilium Pharmaceuticals

-

Adamed

-

Others

Mangoceuticals, Inc. Financial Performance

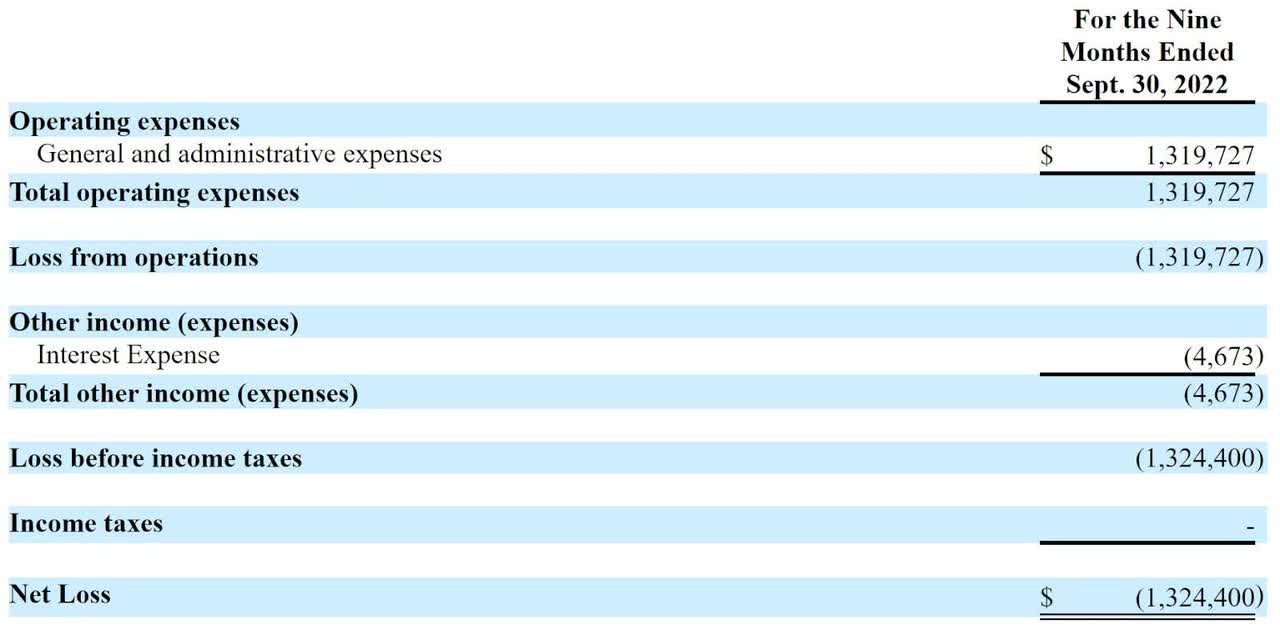

Below are relevant financial results derived from the firm’s registration statement:

Statement Of Operations (SEC)

(Source – SEC)

As of September 30, 2022, Mangoceuticals had $873,491 in cash and $89,871 in total liabilities.

Mangoceuticals IPO Details

Mangoceuticals intends to raise $5 million in gross proceeds from an IPO of its common stock, offering 1.25 million shares at a proposed midpoint price of $4.00 per share.

No existing shareholders have indicated an interest in purchasing shares at the IPO price.

The firm has also registered for sale 4.69 million shares by selling shareholders.

Assuming a successful IPO, the company’s enterprise value at IPO would approximate $54.3 million, excluding the effects of underwriter over-allotment options.

The float to outstanding shares ratio (excluding underwriter over-allotments) will be approximately 8.35%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Management says it will use the net proceeds from the IPO as follows:

We currently intend to use the net proceeds we receive from this offering for general corporate purposes, including working capital ($1,107,000, or approximately 27% of the net proceeds), to finance the marketing and operational expenses associated with the planned marketing of our Mango ED product (approximately $1,804,000, or 44% of the net proceeds), hiring additional personnel to build organizational talent ($902,000, or approximately 22% of the net proceeds) and capital expenditures for software development and maintenance ($287,000, or approximately 7% of the net proceeds).

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management said ‘there are no pending or threatened legal proceedings involving our company.’

The listed bookrunners of the IPO are Boustead Securities.

Commentary About Mangoceuticals’ IPO

MNGO is seeking U.S. public capital market investment to fund its product development and commercialization.

The firm’s financials show no revenue and significant general & administrative expenses.

The company currently plans to pay no dividends and to reinvest any future earnings back into the firm’s growth initiatives.

The market opportunity for erectile dysfunction products is large and expected to grow substantially in the coming years.

However, the industry is subject to fierce competition from major pharmaceutical companies with deep pockets.

Boustead Securities is the sole underwriter and IPOs led by the firm over the last 12-month period have generated an average return of negative (72.3%) since their IPO. This is a bottom-tier performance for all major underwriters during the period.

Risks to the company’s outlook as a public company include no revenue history and shareholders selling into the IPO.

As for valuation, management is asking investors to pay an Enterprise Value of approximately $54.3 million for a non-life science company with no history of revenue.

Given the firm’s pre-revenue status, selling shareholders and thin capitalization, I’ll pass on the IPO.

Expected IPO Pricing Date: To be announced.

Be the first to comment