grandriver

Company Overview

Mammoth Energy Services (NASDAQ:TUSK) offers well-completion services and natural sand products for the production of oil and natural gas from onshore wells in North America. In addition, the Company’s Infrastructure segment offers construction and repair services for electric utilities and the U.S. electricity grid.

Investment Thesis

U.S. oil and natural gas prices reached 5-year highs in 2022, driving U.S. energy producers to double the number of working rigs compared to 2020 levels. TUSK’s Well Completion segment supplies hydraulic pressure pumping equipment to oil and gas producers, while its Sand segment supplies proppant sand for hydraulic fracking. Both segments have seen increased volumes and higher realized pricing in 2022. The Company forecasts that industry-wide scarcity of well-servicing equipment will keep pricing high through 2023. TUSK projects a 70% increase in frac fleet utilization in 2023 and an 8% increase in sand volumes. We forecast EBITDA generated by the Well Completion segment to exceed $100 million in 2023, driving Company EBITDA to $150 million, 50% above the Q3:22 run rate.

We initiate coverage with a BUY rating and a $10.50 price target.

Trends in Demand for Well Servicing

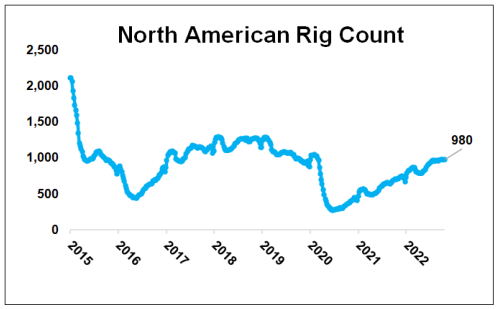

Driven by higher oil and natural gas prices, North American energy producers have doubled the number of producing rigs compared to 2020 lows, returning to pre-pandemic levels.

“North America Rig Count.” Baker Hughes, 29 Oct. 2022, rigcount.bakerhughes.com/na-rig-count/

With both oil and natural gas prices forecast to remain elevated through 2023, the number of wells and the demand for well servicing is likely to remain at high levels. According to the Company, demand for well-servicing equipment is currently outstripping industry-wide supply, and supply shortages have shifted pricing power to suppliers of servicing equipment. The Company forecasts this supply/demand imbalance will continue through 2023.

Summary Of TUSK Advantages In Well Servicing

High energy prices have driven higher demand throughout the energy servicing industry. In addition to this macro trend favoring all servicing industry participants, TUSK stands out with several competitive advantages:

- With the energy servicing industry as a whole suffering capacity constraints, TUSK’s in-house service and build capability provides flexibility in responding to opportunities. TUSK is considering converting an additional frac spread to dual fuel, which would give TUSK a total of three dual-fuel fleets.

- Natural gas wells are a higher share of TUSK’s servicing revenue than oil wells, a favorable factor since natural gas prices have greater support from long-term macro trends.

- The Company’s Sand segment benefits from a dry storage capability, allowing sand to be mined and stored in warm weather to support the continuity of sand deliveries during the winter months.

Trends in Infrastructure

TUSK’s Infrastructure segment has two key drivers, revenue from multi-year master service agreements with investor-owned utilities and repairs to the electrical grid in response to storm damage.

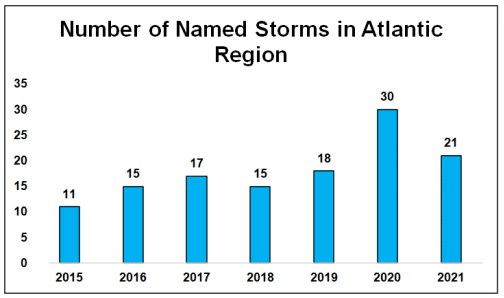

Revenue from TUSK’s repair work for the U.S. electrical grid varies from year to year, depending on the amount of storm damage in any given year. Future storm damage is obviously difficult to predict, but we can be mindful of overall trends in storm activity. The number of significant storms has trended upward over the past several years.

“North Atlantic Ocean Historical Tropical Cyclone Statistics.” Colorado State University Department of Atmospheric Science, 30 Sep. 2022, tropical.atmos.colostate.edu/Realtime/index.php?arch&loc=northatlantic

Our DCF model uses income statement values for year one, and we assume EBIT grows at a CAGR of 8.3% per year for years two through eight. This DCF model produces a value of $8.99. We then average the two price targets of $11.97 produced by the relative valuation and $8.99 produced by our DCF model to come to a final target price of $10.48, which we round up to $10.50.

Best of the Uncovereds offers new initiation reports on roughly two dozen companies per year, with a focus on under-followed small and mid caps with significant potential. We provide a quarterly earnings update reports on all companies covered, as well as flash reports on significant news announcements by companies. We go further for members, providing recorded interviews with management teams of covered companies when available and a monthly quantitative based “Market Indicators and Strategy Report.”

Be the first to comment