JHVEPhoto

When we last covered Magna International Inc. (NYSE:MGA), we suggested that a defensive mode may be better for those looking for returns in this company. The extremely high implied volatilities on the stock, coupled with a small expected return on our part, made options superior risk-adjusted returns. Specifically, we said:

We like the stock here as one of the high-quality cyclicals with a pristine balance sheet and firm commitment to shareholder returns. We rate this a Buy, and maintain our two year price target of $75/share. We still think cash secured puts are the best way to play it as they offer high annualized returns than our expected return profile, with lower risk.

Source: “Inflationary Pressures Continue To Dominate.”

The stock had provided a total return of about 4% till February 9, 2022. The released results this morning wiped those gains out, with pre-market guiding for an 12% lower open.

We look at the Q4 2022 numbers and see if this requires a “cut and run” approach.

Magna Q4 2022 Earnings

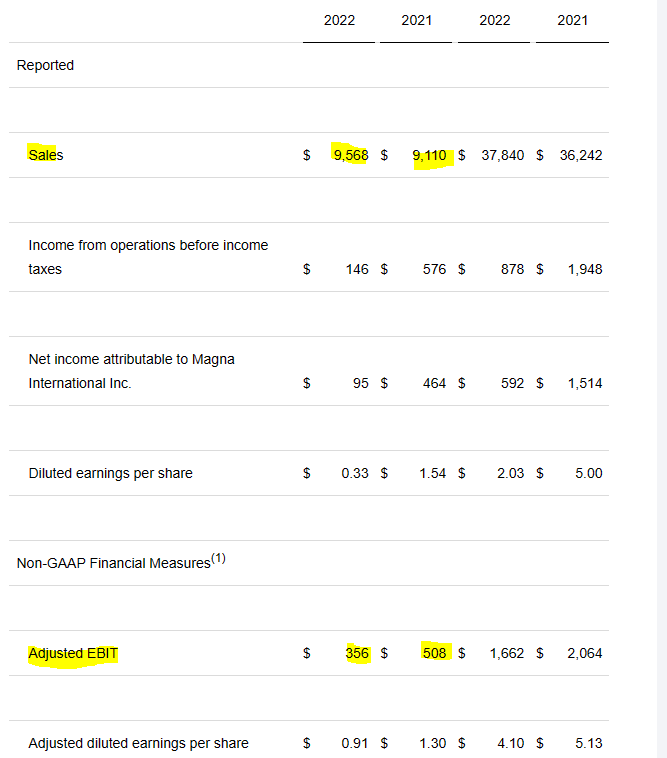

The common theme du jour is that companies are beating the top line estimates and missing the bottom line. Inflation is powering nominal sales, but pricing power is not keeping up with cost increases. MGA was no different in this regard, with top line beating by a healthy $60 million and bottom line coming in short by almost 18%. The non-GAAP EPS of $91 cents was also far below the numbers achieved last year for this quarter ($1.30). The adjusted EBIT was just $356 million and came in even lower than Q2-2022 EBIT.

MGA Q4-2022 Press Release

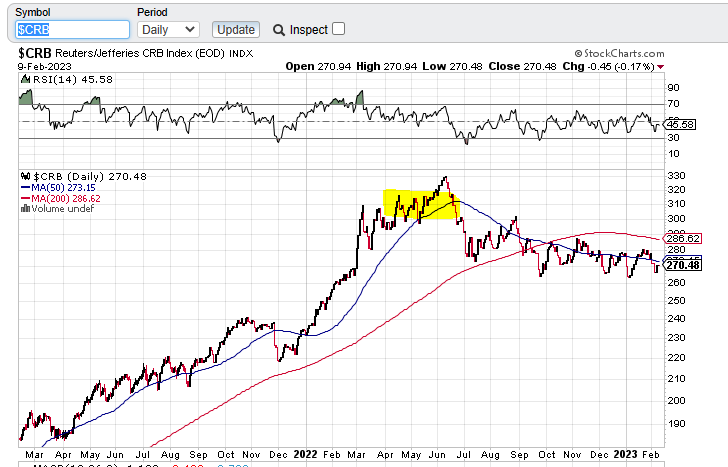

Investors will recall that Q2 2022 EBIT was abnormally pressured by the start of the Ukraine war with commodities flying high. The CRB index is now more than 10% lower than at that point, and MGA is still struggling.

Stock Charts

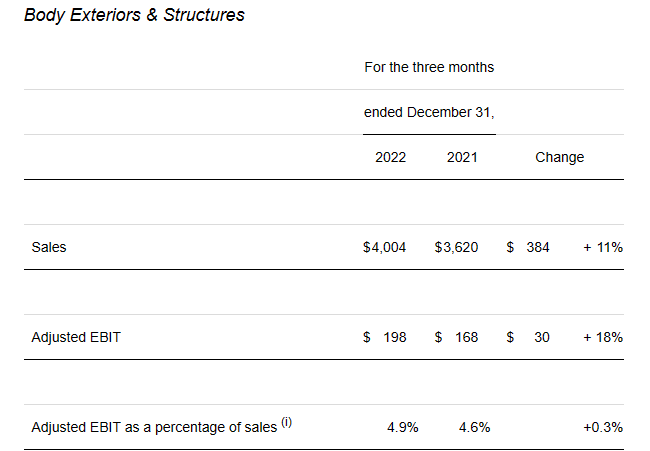

Interestingly, not all its segments are struggling. Body exteriors and structures did quite well with EBIT margins expanding.

MGA Q4-2022 Press Release

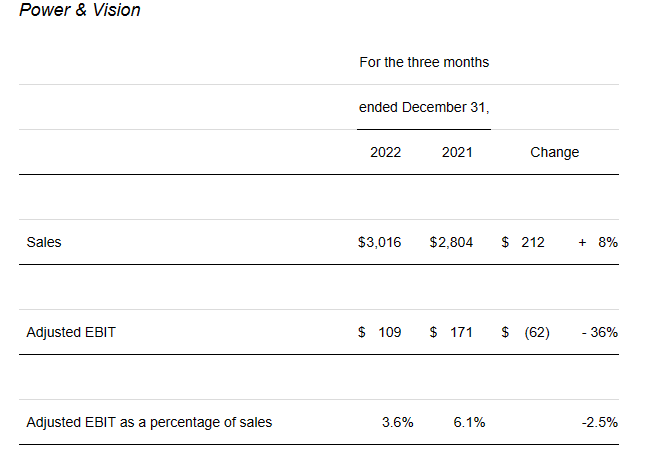

Power & Vision was the primary culprit with EBIT margins dropping sharply.

MGA Q4-2022 Press Release

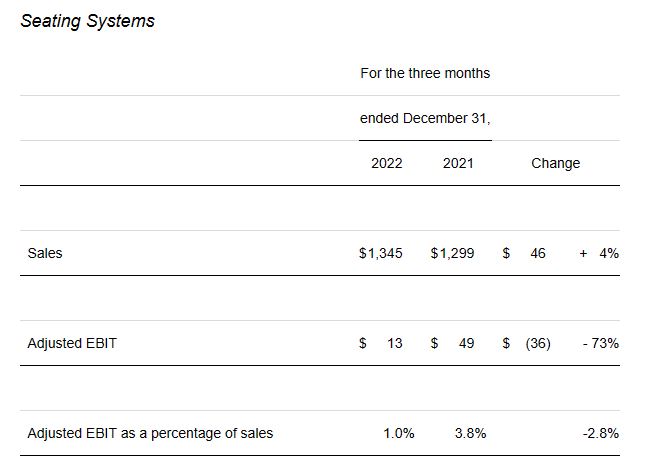

Seating systems did worse on an EBIT margin basis, but since this segment provides less thrust to MGA’s earnings, it did not impact the bottom line as much.

MGA Q4-2022 Press Release

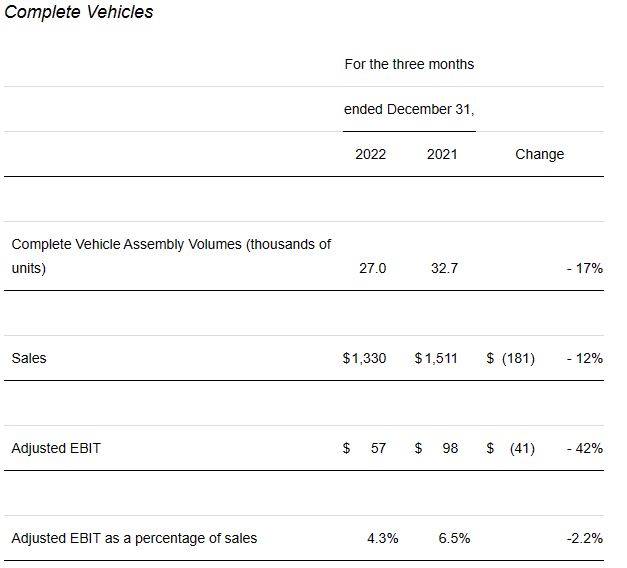

Finally, complete vehicles showed a sharp drop in margins as well.

MGA Q4-2022 Press Release

MGA’s overall numbers for 2022 highlighted the problem with buying cyclical stocks with great looking earnings. Those earnings can and do change very quickly. This is particularly true for low-margin companies like MGA, where small differences between revenues and cost of sales can create big movements in EBITDA and EBIT.

Outlook

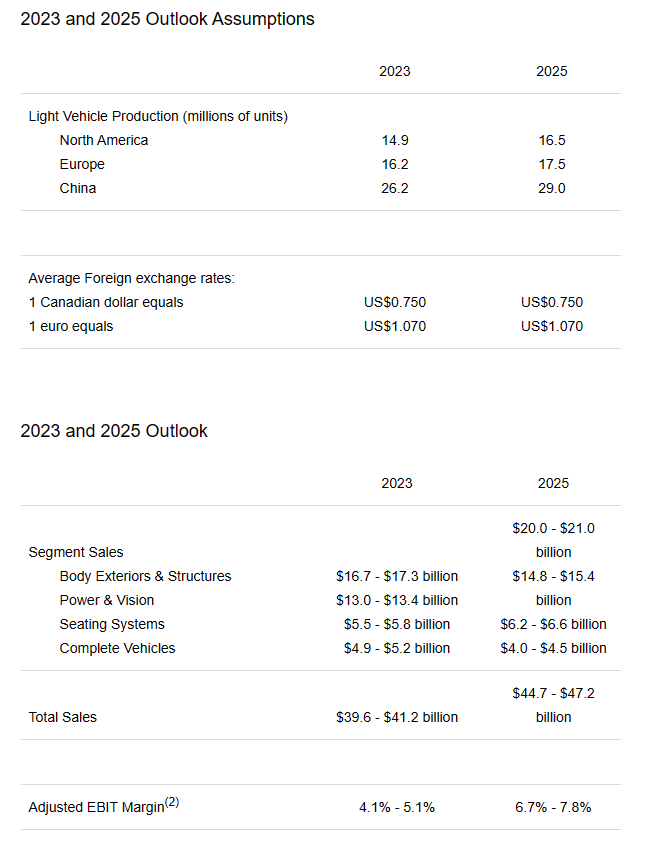

MGA provided a 1 and 3 year outlook in its press release.

MGA Q4-2022 Press Release

The sales estimates for 2023 are in line with where MGA is.

Seeking Alpha-MGA

The adjusted EBIT margin is not. Analysts were expecting earnings to ramp up to $5.85 per share in 2023.

Seeking Alpha-MGA

Taking the midpoint of MGA’s EBIT estimate gets you to about $1.9 billion in EBIT and possibly $4.70-$4.80 in earnings. The final number will definitely have some impact from taxes and other factors that we really cannot account for with certainty. Nonetheless, MGA has essentially guided down by about 20% versus the consensus. Keep in mind that analysts will burn the midnight oil to make sure you beat their estimates. This can be clearly seen in the trend here for 2023.

Seeking Alpha-MGA

So we have issues here and MGA is finding it hard to get efficiencies in the face of persistent non-commodity inflation.

Verdict

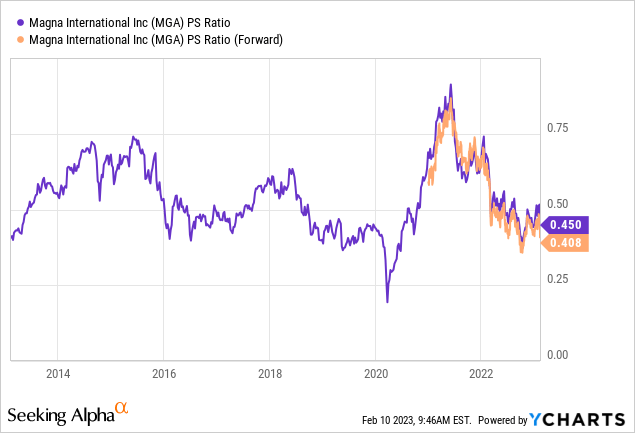

Magna International Inc. stock is now on the cheap side of things, with price to sales ratio in the bottom quartile for all readings.

Today, we have the stock looking cheap on this metric while appearing “ho-hum” on earnings. This is the opposite of what we saw in 2021 when we suggested investors move to the sidelines.

Seeking Alpha

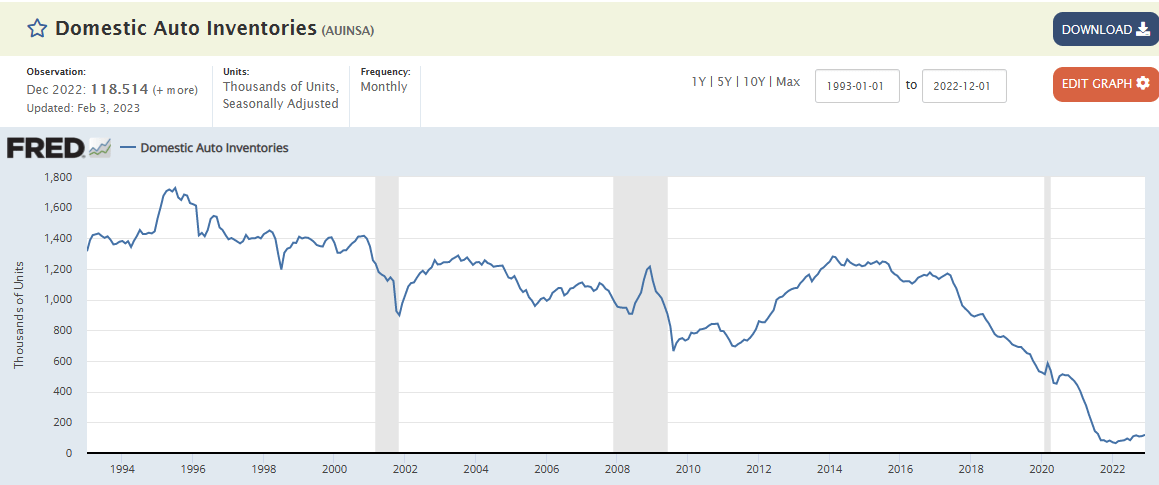

The stock looked very cheap on earnings per share but was incredibly expensive on a price to sales basis. So, at the current valuation you can take an educated long position, knowing that you will likely get decent forward returns. To this factor, we will add that domestic auto inventories remain exceptionally low and they will have to be built up at some point in the future.

FRED

When exactly that happens is anyone’s guess. MGA for its part thinks that there will a good build up by 2025. Certainly, its sales outlook suggests that it believes a powerful rebound is coming. We are a little more circumspect. Historically, we have never built these inventories up to that extent during a recession. Peak to trough, during a recession, inventories decline. Nonetheless, we see this as a long term tailwind to MGA. You have a cheap valuation, alongside a good tailwind for MGA. We think that creates a buyable opportunity. Ideally you don’t want to use the first day of a big selloff to buy, so perhaps waiting improves the odds. Also combining the waiting with option premiums in the $50-$55 range can get you a bulletproof entry. We rate Magna International Inc. shares a buy, with the caveat that you want to use a wider margin of safety here and only enter via options.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment