zhnger

Thesis

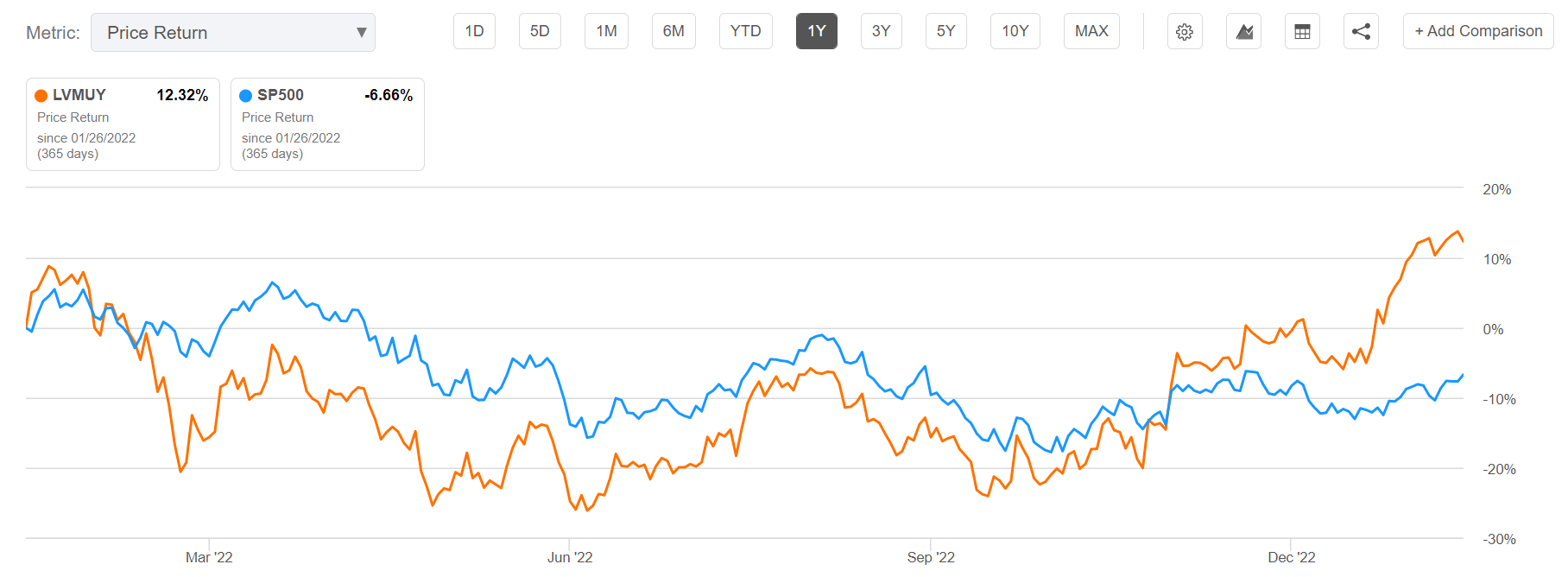

In early August 2022, despite macroeconomic challenges that were clearly not favorable to luxury, I argued that LVMH (OTCPK:LVMHF) (OTCPK:LVMUY) stock is a ‘Buy’. Since then company’s equity investors have gained approximately 21% of value, as compared to a loss of 1% for S&P 500 (SPY) investors.

Reflecting on a likely EPS expansion in 2023 on the backdrop of a likely demand surge anchored on China’s COVID reopening, paired with a globally improving macro outlook, I upgrade my target price for LVMH stock to $190.53 (LVMUY reference). Reiterate ‘Buy’ rating.

For reference, LVMH stock continues to be a strong relative outperformer versus the broad market: for the trailing twelve months, LVMH stock is up approximately 12%, as compared to a loss of almost 7% for the S&P 500.

Seeking Alpha

Closing A Strong 2022

Arguably, LVMH’s 2022 performance has been nothing less than unexpectedly spectacular – reflecting on the multitude of macroeconomic challenges that pressured the demand for luxury goods, including COVID lockdowns in China and a collapsing crypto market.

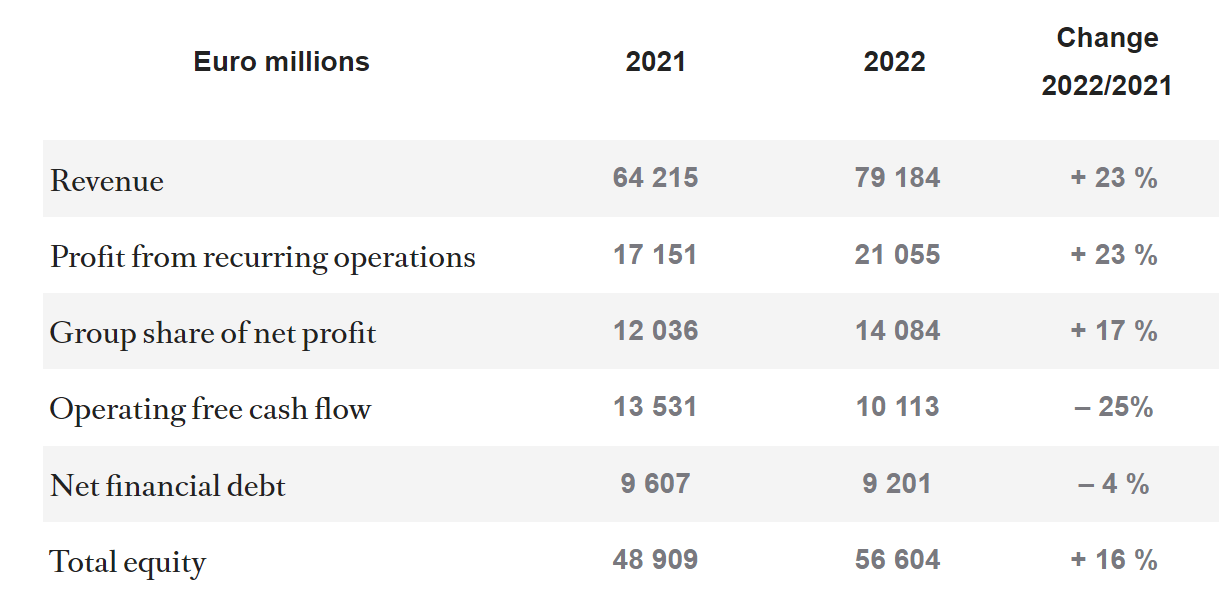

In the FY 2022, LVMH recorded total revenues of €79.2 billion, and profits from recurring operations of about €21.1 billion. Notably, both metrics are up 23% year over year, highlighting not only demand and growth resiliency for the group, but also an exceptional pricing power in light of inflationary forces. LVMH’s annual free cash flow from operations was recorded at €10.1 billion, which allowed the company to reduce net financial debt by 400 million, down to 9.2 billion, as well as raise the dividend to shareholders by 20%.

Other 2022 highlights include:

- A strong growth in all geographic regions (ex China): in Europe, Japan and the United States

- A strong performance across business segments, including the Fashion & Leather Goods business group (with sales of €38.6 billion and organic yoy growth of 20%), Perfumes, Watches & Jewelry Maisons, and Champagne and Cognac

- Louis Vuitton revenue surpassed 20 billion euros, for the first time

- Operating investments of nearly €5 billion, mainly dedicated to the expansion of the store network, the development of production facilities and employment,

- According to the company’s wording: ‘39,000 young people recruited worldwide in 2022’.

LVMH 2022 Snapshot Report

Reasons To Be Confident For 2023

If LVMH can deliver an exceptional financial performance despite macro headwinds, how well can the luxury conglomerate perform with macro tailwinds?

In my opinion, there are reasons to be optimistic for the luxury market outlook going into 2023, given the likely demand rebound coming from China. With that frame of reference, LVMH management has already voiced strong confidence:

China has actually turned the page on the disruption of the pandemic … and [given the trend in January] we can be really optimistic

The company also described the demand rebound in Macau, which opened up again to travel and tourism as ‘incredible’.

But even looking beyond the China reopening boom, investors should also consider that the luxury market remains in a structural growth trend, with the market expected to grow at a CAGR of approximately 4-5% through 2025, double the nominal GDP growth. And with that frame of reference, the LVMH group’s long-term strategy remains well positioned to capture more market potential, independent of cyclical fluctuations. Or as the company’s CFO Jean Jacques Guiony commented:

We work on our brands’ desirability so they can resist in downturns, and have learned to be flexible in a crisis if one materialises … Last year’s strong results, despite the war in Ukraine and challenges in China, show the resilience and permanence of luxury consumers and the strength of our brands.

Target Price: Raise To $190.53

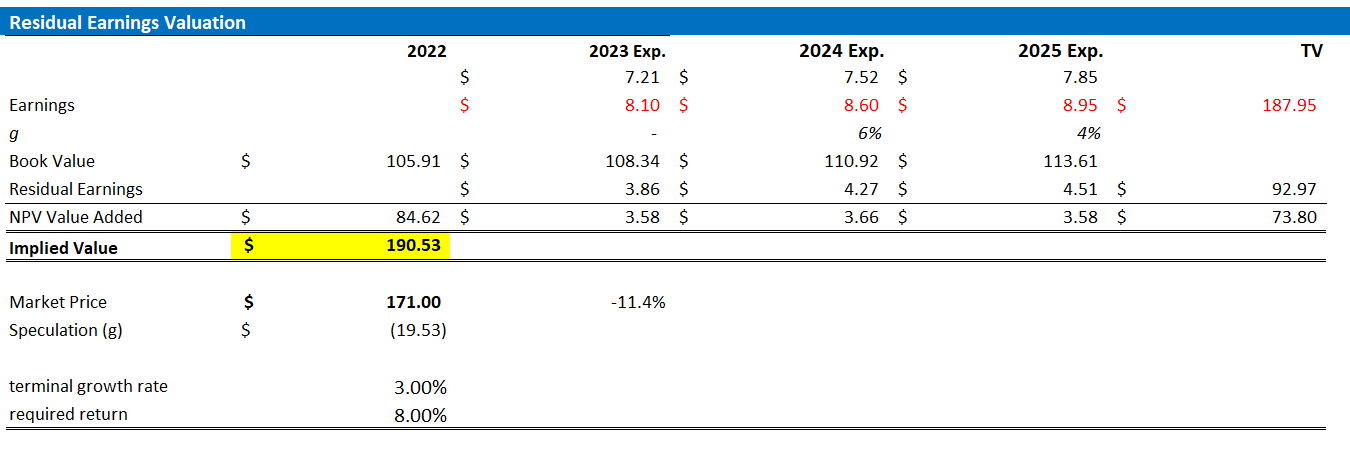

Expecting a sharp economic luxury demand rebound in China, which strongly favors LVMH’s exceptional portfolio of brands, I estimate that LVMH’s EPS in 2023 will likely expand to somewhere between $7.8 and $8.3. Moreover, I also raise my EPS expectations for 2024 and 2025 to $8.6 and $8.95, respectively. I continue to anchor on a 3% terminal growth rate, as well as on an 8% cost of equity requirement.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price of $190.53 (LVMUY reference).

Author’s EPS Estimates & Calculations

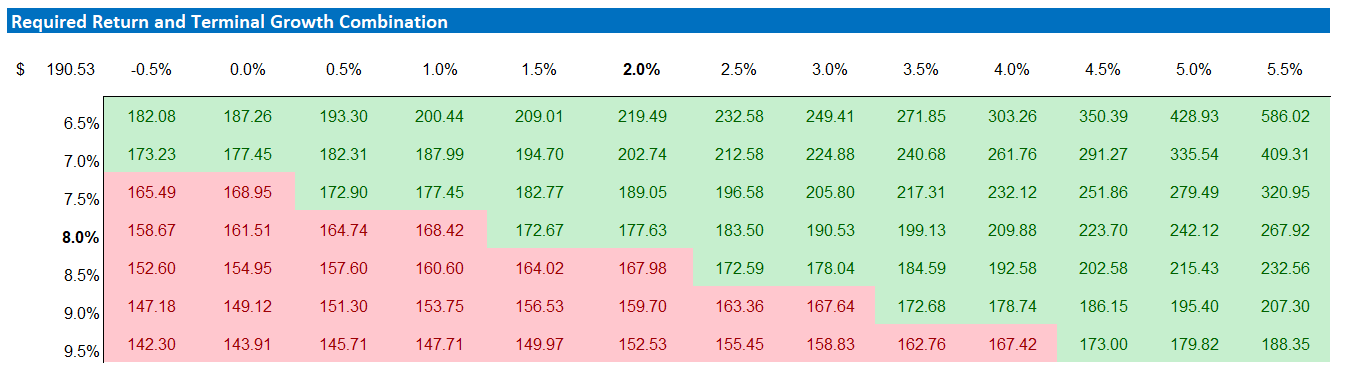

Below is also the updated sensitivity table.

Author’s EPS Estimates & Calculations

Risks and Headwinds

As I see it, there has been no major risk update since I initiated coverage on LVMH stock. Thus, I would like to highlight what I have written before.

… investors should note the following risks that might cause LVMH stock to significantly deviate from my target price: 1) slowing consumer confidence due to inflation outpacing wage growth, rising interest rates and increasing unemployment; 2) LVMH’s significant exposure to China, which is especially Covid-19 lockdowns; 3) macroeconomic uncertainty relating to the monetary policy actions of the ECB and actions of the European government against Russia.

Conclusion

Arguably, LVMH’s 2022 performance has been nothing less than unexpectedly spectacular, reflecting on the multitude of macroeconomic challenges that pressured the demand for luxury goods. I am optimistic for the luxury market outlook going into 2023, as the COVID reopening in China will likely provoke a surge in the demand for luxury goods. Looking beyond the China reopening boom, the luxury market remains in a structural growth trend, expected to grow at a CAGR of approximately 4-5% through 2025. I upgrade my target price for LVMH stock to $190.53 (LVMUY reference). Reiterate ‘Buy’ rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment