Chesky_W

Thesis highlight

I think Luminar Technologies (NASDAQ:LAZR) has plenty of upside if it manages to hit its FY30 targets. The growing focus on autonomy in the mobility industry, coupled with the rising interest in electric and hydrogen drivetrains, is opening up the possibility of autonomous vehicles made possible by advanced sensing and computing technologies. I believe LAZR’s lidar technology is a key enabler for autonomous driving, as it provides enhanced vehicle situational awareness that can facilitate the transition from current driver assistance to autonomous driving. I expect the autonomous vehicle market to be significant in the long run and LAZR is positioned to be a market leader in lidar technology.

Company overview

Luminar Technologies develops vision-based machine perception and lidar technologies, primarily for use in autonomous vehicles.

Growing focus on autonomy in mobility

There is a rising interest in autonomy, in particular autonomous highway driving for cars and trucks. In my opinion, the trend toward electric and hydrogen drivetrains opens the door to the possibility of autonomous vehicles made possible by sensing and computing technologies. These are grounded in the idea that enhanced vehicle situational awareness can facilitate the transition from current driver assistance to autonomous driving. LAZR products give drivers this kind of insight in a variety of road conditions, letting them confidently detect obstacles and plan ahead regardless of speed. (Note: readers should read up to understand the levels of automation defined by The Society of Automotive Engineers [SAE]).

Putting aside the specifics, it seems to me that the market can be broken down into two distinct subsets at the moment: advanced driver assistance system [ADAS] and autonomous driving, the latter of which offers substantial benefits to customers.

Active safety and highway autonomy, in particular, stand out to me as promising areas for profits within these two markets because they address two of the most pressing concerns of both businesses and consumers: the increasing standardization of safety technologies and the growing importance of pain points for the latter.

It’s easy to see why commercial vehicles would benefit from autonomy from both a use case and a business perspective: lower operating costs and improved efficiencies. Passenger vehicles, on the other hand, are more difficult to develop because of the added emphasis placed on the passengers’ convenience and safety. Most importantly, from a business and synergy perspective, the technology requirements of these two applications are sufficiently similar to warrant LAZR’s continued concentration on a single solution that enables OEM partners to accomplish both.

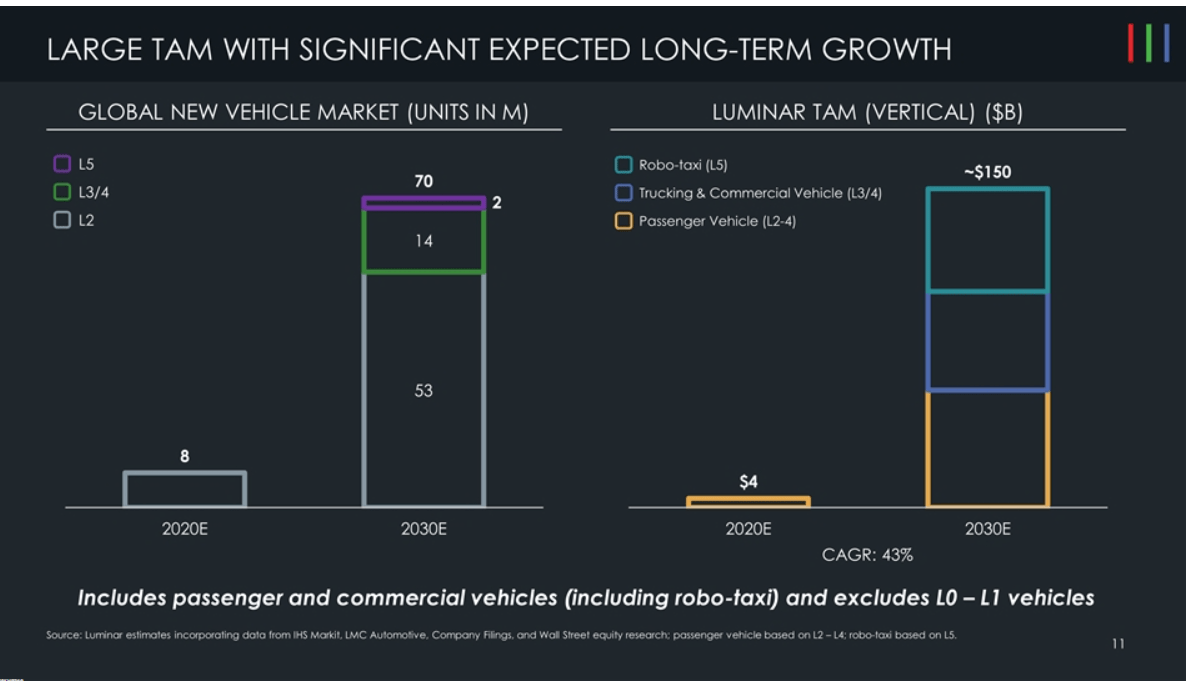

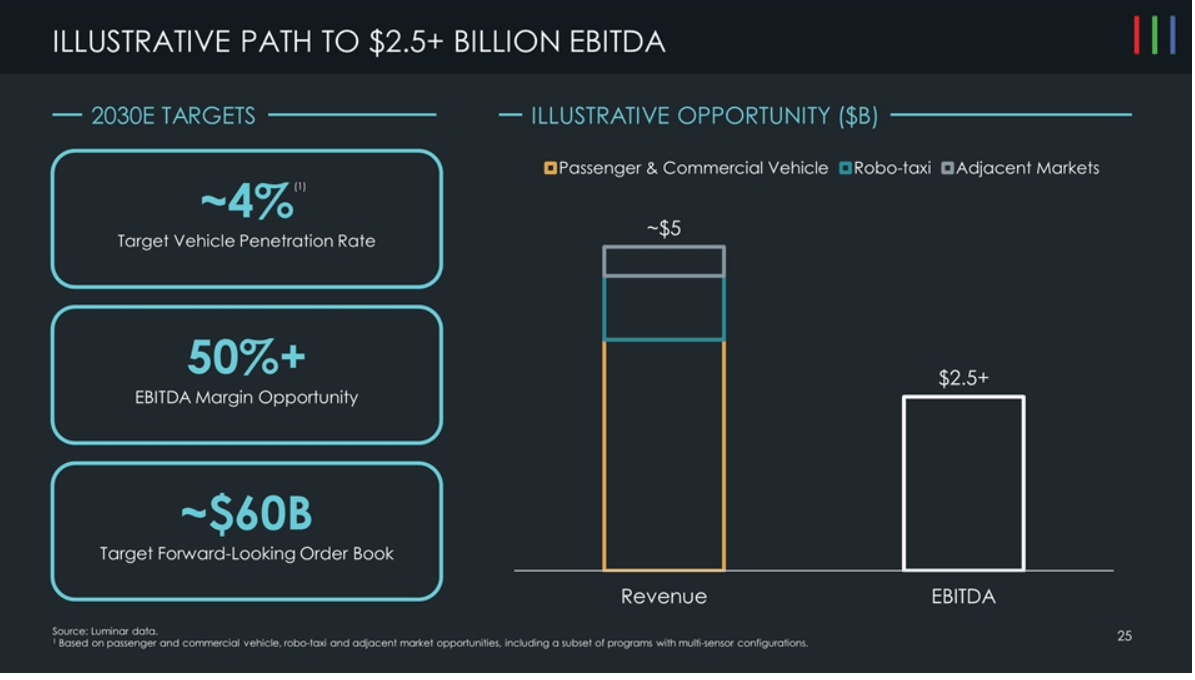

This market aside, I also see great potential in the autonomous vehicle market as a whole in the long run, but widespread adoption still appears to be years away. Here’s a snippet from LAZR SPAC’s pitch deck revealing the potential size of the market.

SPAC Deck

Proprietary tech is a differentiator

Currently available ADAS features are made possible by cameras and/or radar sensing technologies. It is common practice to combine information from the two types of sensors in order to give the vehicle’s system a better picture of the road conditions the driver will encounter. The problem is that these systems don’t provide enough of an improvement in safety to warrant widespread adoption.

The purpose of ADAS is to help drivers recognize potentially hazardous situations and take corrective action when necessary. The most advanced ADAS available today can apply the brakes and steer the vehicle in the event of a driver’s inattention, but these features do not always respond to impending danger. These ADAS systems perform admirably in ideal conditions but drastically worsen in less than ideal ones. In my opinion, adding LAZR lidar to an ADAS system will definitely reduce the number of reported collisions.

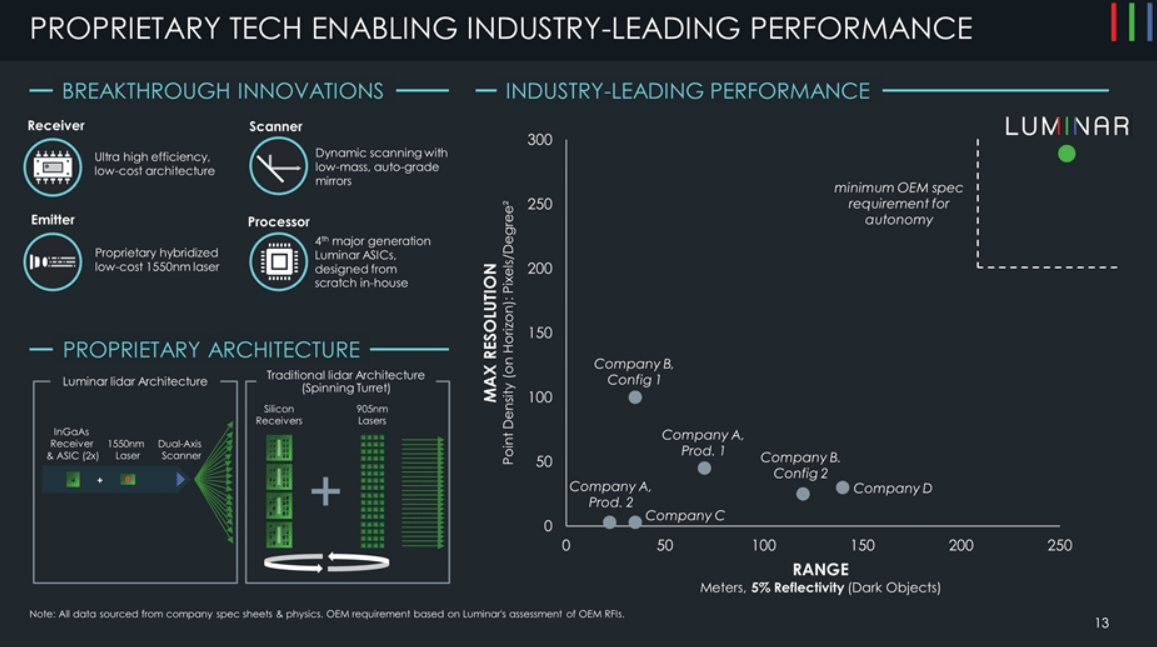

Most global efforts to develop autonomous vehicles reflect skepticism that radar and cameras alone will enable the technology, given the performance of legacy sensors in ADAS. When semi-autonomous vehicles are involved in fatal accidents because of faulty cameras, the need for improved sensors and processors becomes more pressing. I believe LAZR lidar is at the forefront of this next-generation automotive technology with its innovative, patent-pending technology and perception systems.

In my opinion, Luminar is in a prime position to become a market leader in lidar before the inevitable explosion of this technology. The passenger light vehicle and commercial vehicle markets, with their emphasis on high-speed and long-range premium lidar, seem like the most natural fit for LAZR’s technology. When contrasted to the vast bulk of competitors’ sub-200m range products, LAZR’s estimated range of 250 meters is a distinguishing factor for on-highway applications.

SPAC Deck

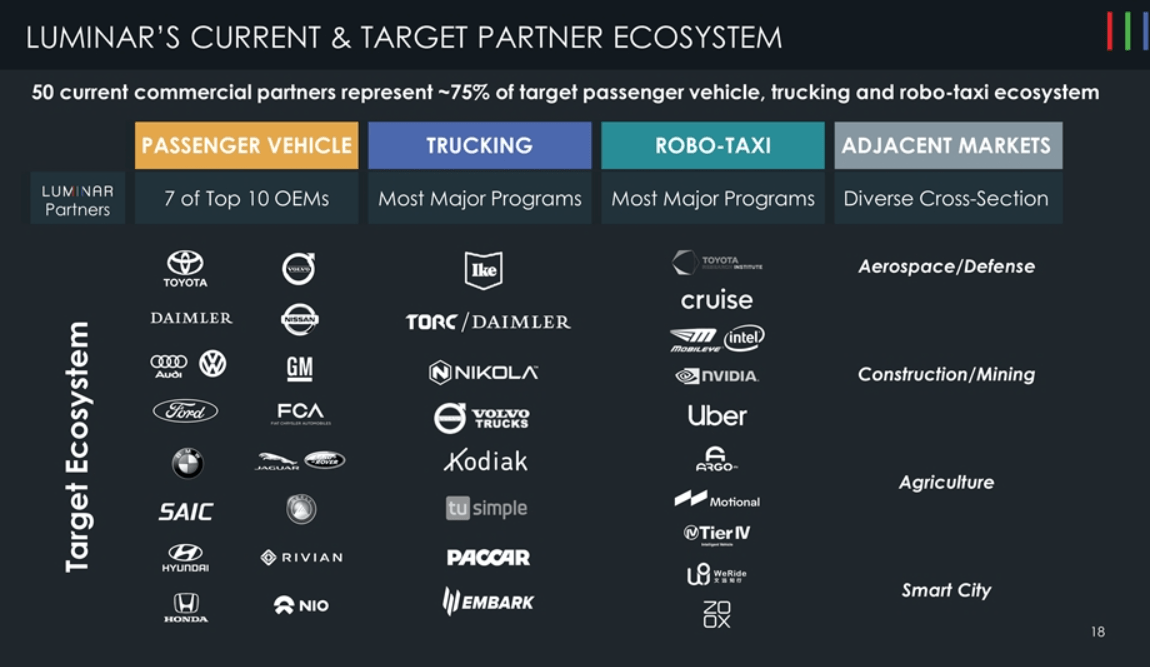

Luminar claims partnerships with the majority of the world’s top ten OEMs and numerous other industry heavyweights. I believe these successes and alliances lend credence to my opinion that LAZR has a product that fits the requirement of many manufacturers.

SPAC Deck

Scalable manufacturing capacity

Instead of using mass-produced, mass-market parts, key components in LAZRs are custom-built or designed by the company. This, in my opinion, serves as a technological barrier to entry because it creates legally enforceable and long-lasting distinction between lidar and competing or alternative technologies. Because LAZR is still in its infancy, the expertise and processes involved in its production are a major selling point.

Rather than bringing in outside help to create their products, LAZR has trained their own employees to develop these skills and capabilities. The end result of all this effort is a long-range detection system that functions as expected and doesn’t break the bank.

Highly competitive market

Assessing lidar’s competitive positioning is challenging due to the technology’s infancy in the automotive industry and the complexity of its many technical aspects.

Different lidar hardware vendors use different signal measurement techniques, light scanning strategies, and wavelengths among other factors to set themselves apart from one another. Different lidar manufacturers take various approaches to vertical integration, logic silicon, and software. Several lidar companies, LAZR included, have solid technical specifications, but I believe that the ability to develop cost – effective solutions, distribute software, and target important end markets will ultimately determine which companies will be more commercially successful in the long-term.

3Q22 earnings provided updates on execution milestones

LAZR’s third-quarter results surpassed analysts’ projections due to the early signing of contracts with new customers. However, SAIC’s quicker launch was the most notable development, as it allowed the company to begin series production slightly ahead of schedule. After Tesla and GM, Volvo and Polestar will introduce LAZR-enabled vehicles in 2023, driving up demand for sensors. With the opening of the highly automated manufacturing line in their Mexico facility in the second half of the year, LAZR will be able to handle the production ramp through 2023.

In my opinion, LAZR’s ramp will be aided by the earlier-than-anticipated start of series production, while 2022 revenues will remain low. Beginning mass production also serves as rebuttal evidence to the concerns of bearish investors who believe the company will fail to deliver what were promised to customers. At LAZR’s investor day update early this year, we should learn more about the long-term effects of the series production milestone.

Valuation

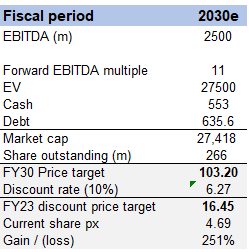

My model suggests an intrinsic value of $16.45 in FY23, representing a 251% upside. Note that this is based on a FY30 EBITDA target started by the management, and as such, the path to realizing LAZR intrinsic value is likely to be back-end loaded when it shows more evidence of hitting the target.

Own valuation

Given the strong secular trend for autonomous vehicle which means higher demand for lidar, I believe LAZR will be able to achieve its FY30 targets eventually. This is especially after reviewing the good performance in 3Q22.

Due to the lack direct comps that are at maturity, I valued LAZR using a market EBITDA multiple with the reason that LAZR should at least be valued similar to the market since it is likely to be growing faster.

SPAC deck

Risk

Lower than expected adoption

I expect most OEMs to initially sell lidar equipped vehicles, such as L3 autonomous functionality as an additional option available for purchase to consumers relative to standard. In the event of lower-than-expected ramp in adoption of L3 equipped vehicles could result in more moderate revenue for LAZR than anticipated

OEMs might not adopt LAZR software solution

OEMs could be more hesitant to adopt the higher levels of the software stack beyond perception software from lidar companies, limiting the opportunity for Luminar despite having the capabilities.

Margin pressure over the long-run

Also, in the long run, I believe there could be a case of margin headwinds for lidar industry participants due to factors such as the competitive landscape, the possibility that ADAS systems can function without lidar, and the need for high volumes by lidar suppliers in order to meet their cost objectives, which may be challenging to meet.

Conclusion

Autonomous vehicles made possible by cutting-edge sensing and computing technologies stand to benefit from the rising prominence of autonomous technology in the mobility sector, as well as the rising popularity of electric and hydrogen vehicles. I think the market for autonomous vehicles is expected to be significant in the long term and LAZR is well-positioned to be a leader in the field with its lidar technology.

Be the first to comment