Octavio Jones

Lululemon Athletica Inc., (NASDAQ:LULU) together with its subsidiaries, designs, distributes, and retails athletic apparel and accessories for women and men. We have published an article in 2022 on the firm, rating LULU stock as a “hold” back then, despite the impressive growth figures. The primary reason for our neutral rating has been the challenging macroeconomic environment in 2022, including elevated costs and low consumer confidence levels.

Analysis history (Author)

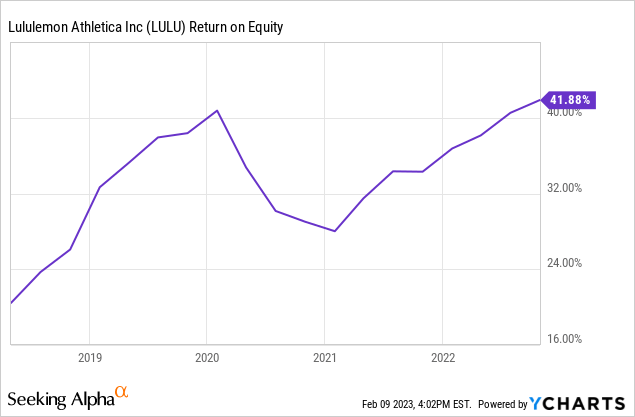

Today, we are looking at the company from another perspective, focusing primarily on its efficiency and profitability. We will be analyzing LULU’s return on equity (ROE) and its components. We will also comment on how we expect these measures to develop in the coming quarters.

Return on equity

ROE is a measure often used to gauge the profitability and the efficiency of companies. It essentially measures a company’s ability to generate profits from shareholders’ equity.

LULU’s return on equity has been trending upwards over the past 5 years, despite the relatively sharp decline during the pandemic. To put this figure into perspective, we need to compare this measure with LULU’s peers. The following table shows a set of profitability measures including ROE for a set of firms in the Apparel, Accessories and Luxury Goods industry.

Comparison (Seeking Alpha)

LULU takes a very attractive place on the list.

But, we have to look a bit further and understand the drivers behind this outstanding ROE. So now, we will be decomposing this measure into three parts.

ROE decomposition (investopedia.com)

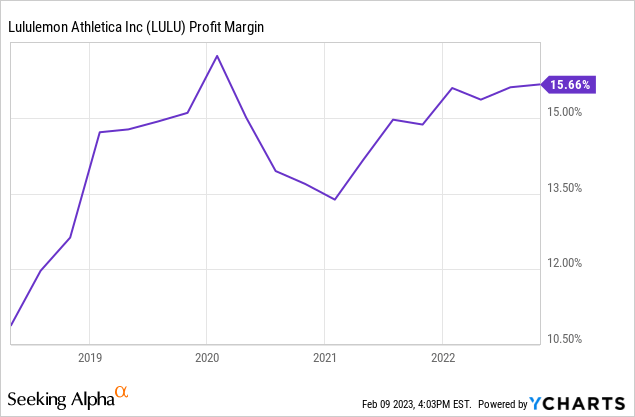

Net profit margin

Net profit margin is often used as an indicator of profitability. It essentially measures the percentage of revenue that a company keeps as profit after accounting for fixed and variable costs.

Just like the ROE, net profit margin has also been trending upwards, except for the year 2020, which has been largely influenced by pandemic related events.

In general, expanding margins are a good sign. Especially, when we appreciate how challenging 2022 has been from a macroeconomic perspective. Energy and raw material prices have been skyrocketing, inflation has gone up substantially, consumer confidence has fallen to historic lows, while geopolitical tensions around the globe have increased. Therefore, we believe that LULU’s ability to maintain its net margin throughout the past year is quite impressive.

The primary question now, is it likely to continue? We will try to answer this question from three aspects.

1) Inventory

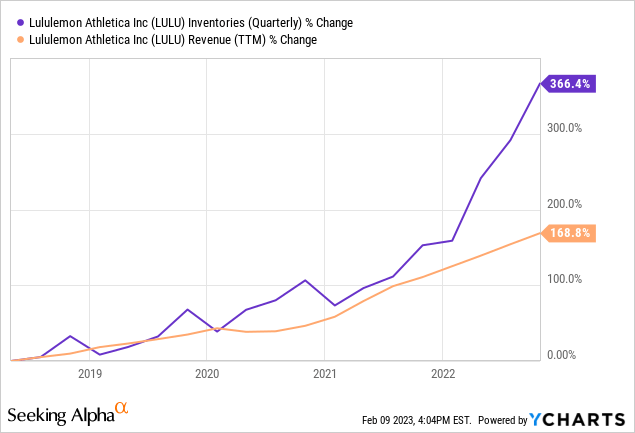

Many firms have been struggling with inventory management issues in 2022. Even large retailers like Walmart (WMT) and Target (TGT) had to deal with excess and obsolete inventory, and therefore had to use promotions and discounts to get the levels back to normal.

Inventory management problems for LULU has been raising concerns for analyst as well. They have observed significant promotional activity in LULU stores, indicating that the firm is already trying to take some actions to mitigate the further increasing of inventory levels. The following chart shows how inventory has skyrocketed compared to sales.

Worse than expected guidance for the holiday season is also not a particularly sign at the moment and can have substantial negative impacts on the firm’s Q4 results. This could also lead to a negative impact on the stock price in the near term.

All these together are likely to put a downward pressure on the margins in the near term.

2) Patent infringement

Patent infringement has also been a hot topic lately. Nike (NKE) has been filing several lawsuits against LULU in the recent months. Such events always represent significant risks. And, if LULU is found guilty, that may have substantial consequences on the firm’s financial performance.

3) Macroeconomic environment

Overall, the macroeconomic environment appears to be improving. Consumer confidence levels have rebounded sharply, which may indicate that the growth in consumer spending may accelerate in the coming quarters. This could fuel demand also for LULU’s products. At the same time, energy and raw material prices have come off of their peaks, which is likely to have a positive impact for LULU on the costs side. Inflation has been also moderating. The reopening of China can also present opportunities for LULU.

From this perspective, we are quite optimistic looking forward.

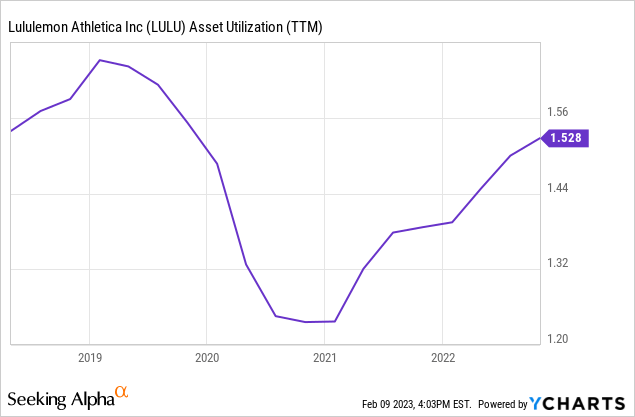

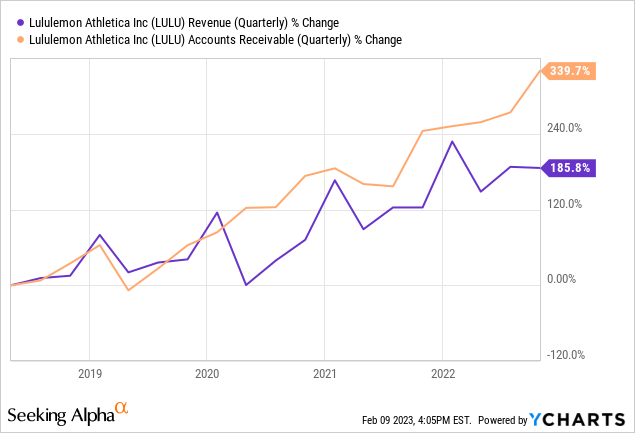

Asset turnover

Asset turnover (or often asset utilisation) is a measure of efficiency. It indicates how effective the firm is in generating sales using its assets. Over the past 5 years, LULU’s asset turnover has been quite volatile.

First of all, during 2020, revenue has plummeted, leading to a substantial decrease in turnover. From 2021 onwards it has started to improve once again as sales have gained momentum. What is concerning about this, is that accounts receivable, especially in the second half of 2022, have been growing much more rapidly than sales. It may indicate that the firm is selling more on credit, or is using more aggressive accounting practices to avoid declining revenue. Ideally, we would like to see the growth in accounts receivable falling, before we would consider upgrading the stock to “buy”.

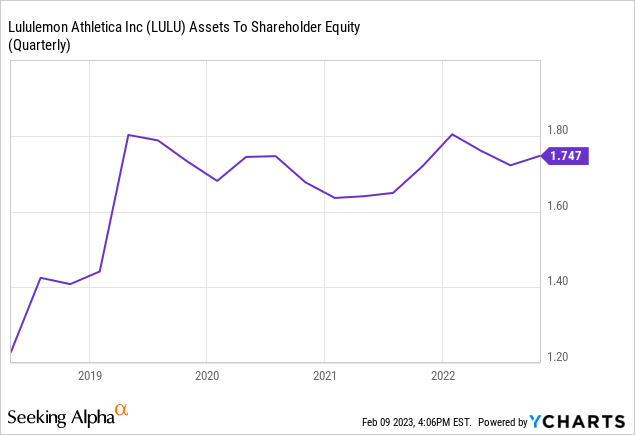

Equity multiplier

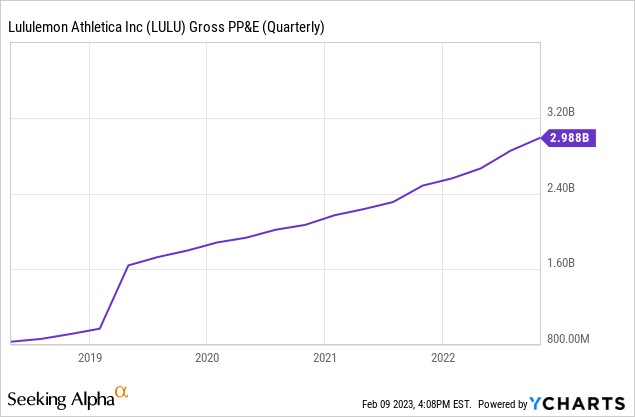

Equity multiplier is the ratio of assets to shareholder equity. It shows, how much of the firm’s total assets are supported by equity. Except the sharp increase in 2019, the equity multiplier has stayed largely flat, indicating that there have been no significant changes to the capital structure.

The large jump in 2019 has been caused by the doubling of gross PP&E back then.

Compared to its peers, LULU appears attractive from an equity multiplier point of view, however when looking at the company’s liquidity, the picture is mixed.

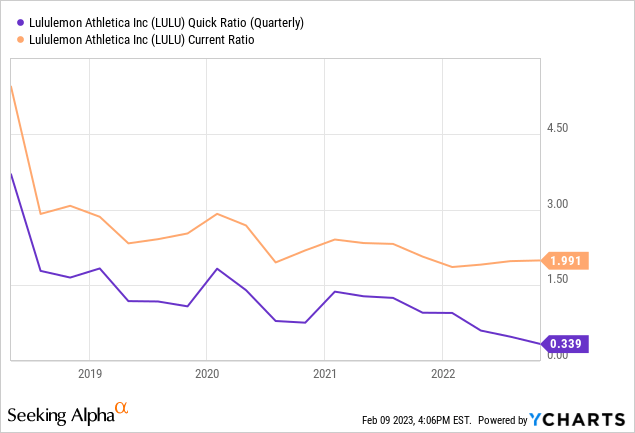

While the company’s current ratio is well above 1, which is a good sign, the quick ratio is only around 0.34. The difference between the current- and the quick ratio is the treatment of inventory. The quick ratio excludes the inventory. The high growth in inventory levels have been affecting LULU’s liquidity significantly in the past quarters. As a result, in the industry LULU has one the lowest quick ratios.

While the capital structure appears to be adequate at the moment, we would like to see LULU’s liquidity improve, potentially by reducing the inventory levels.

Key takeaways

We expect the macroeconomic environment to keep improving, which is likely to have a positive impact on the firm’s financial performance from the second half of 2023.

On the other hand, there are certain risks and uncertainties that we have to appreciate as potential investors. These include: risks and costs related to patent infringement, inventory management problems and worse than expected guidance for the holiday sales.

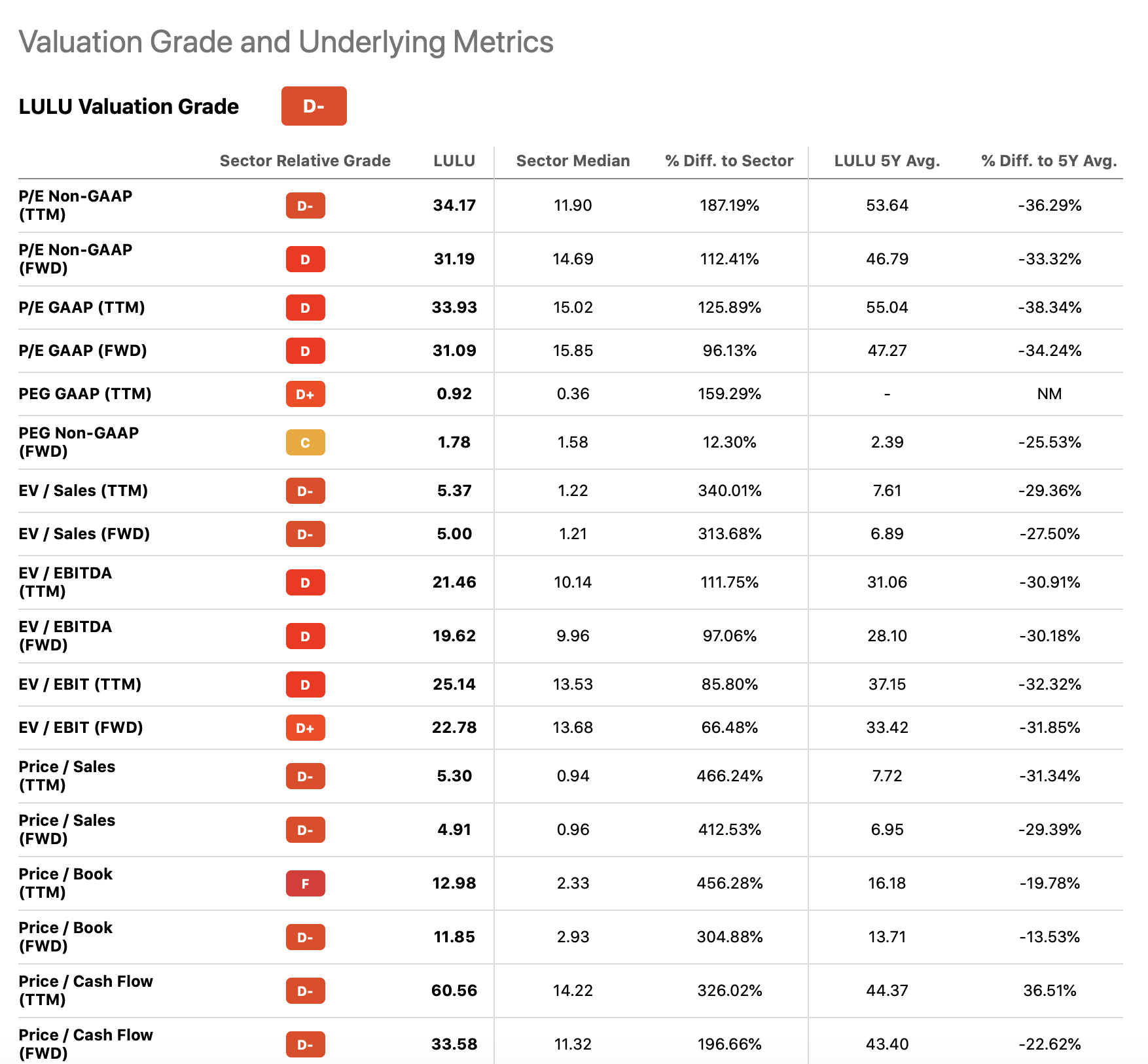

At the same time, LULU is selling at a significant premium compared to the sector median, which we believe is not justified in light of the uncertainties.

Valuation (Seeking Alpha)

For these reasons, we maintain our neutral rating.

Be the first to comment