ivanastar

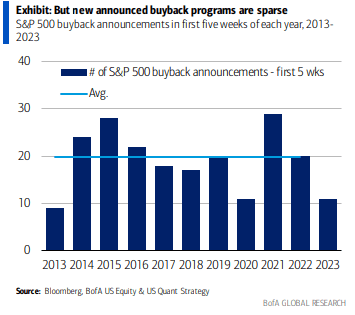

New buyback programs have been sparse lately. While major announcements from Chevron (CVX) and Meta Platforms (META) have stirred up share repurchase chatter, total announcements have been down this month.

One consumer name approved a $15 billion buyback plan last December, and I see value in its shares despite a shaky macro backdrop. Let’s investigate Lowe’s.

Buyback Announcements Become Few and Far Between

BofA Global Research

According to Bank of America Global Research, founded in 1946, Lowe’s Companies (NYSE:LOW) is a leading home improvement retailer with 1,970 stores in the US and Canada. The company has tempered its new store opening plans and is focusing investments on technology and e-commerce capabilities, in addition to improving its retail store productivity.

The North Carolina-based $20.5 billion market cap Specialty Retail industry company within the Consumer Discretionary sector trades at a near-market 20.5 trailing 12-month GAAP price-to-earnings ratio and pays a 2% dividend yield, according to The Wall Street Journal.

Back in November, the firm reported better-than-expected earnings and sales and raised its guidance. It also announced that it would divest one of its low-margin operations out of Canada, which shows good management discipline to focus on areas with better profitability potential.

Something to watch going forward is how consumer confidence ebbs and flows – with awful homebuilder sentiment lately, the consumer might be feeling just a bit better which would be a tailwind. Rising interest rates would hurt Lowe’s as that would likely lead to a weaker housing market. Also, a higher unemployment rate would reduce consumer spending and damage margins.

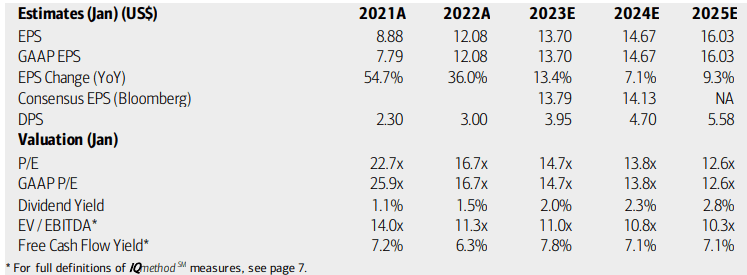

On valuation, analysts at BofA see earnings having surged 36% in 2022, continuing a period of strong growth as consumers spend excess savings. EPS growth is seen as moderating to a still strong rate this year before settling in the high-single digits through 2025. The Bloomberg consensus forecast is slightly less sanguine compared to BofA’s outlook.

Dividends, meanwhile, are seen as rising at a fast clip in the coming quarters, pushing up the yield should the share price keep consolidating near $200. Both LOW’s operating and GAAP P/Es are reasonable given the robust earnings growth rates. Moreover, the firm’s free cash flow yield is steady and impressive above 7%. I like to assess a stock’s forward operating PEG ratio to get a sense of the valuation considering the growth outlook. With a forward PEG of just 0.82, it’s a massive 47% discount to the sector median and 20% to the cheap relative to the company’s five-year average. With robust return on capital, profits should flow through nicely to shareholder via the rising dividend and share repurchase program.

Overall, if we apply a market P/E of 18 to 2023 earnings of $13.70, that would yield a target of $247, so I see the stock as a solid buy on valuation today.

Lowe’s: Earnings, Valuation, Dividend Forecasts

BofA Global Research

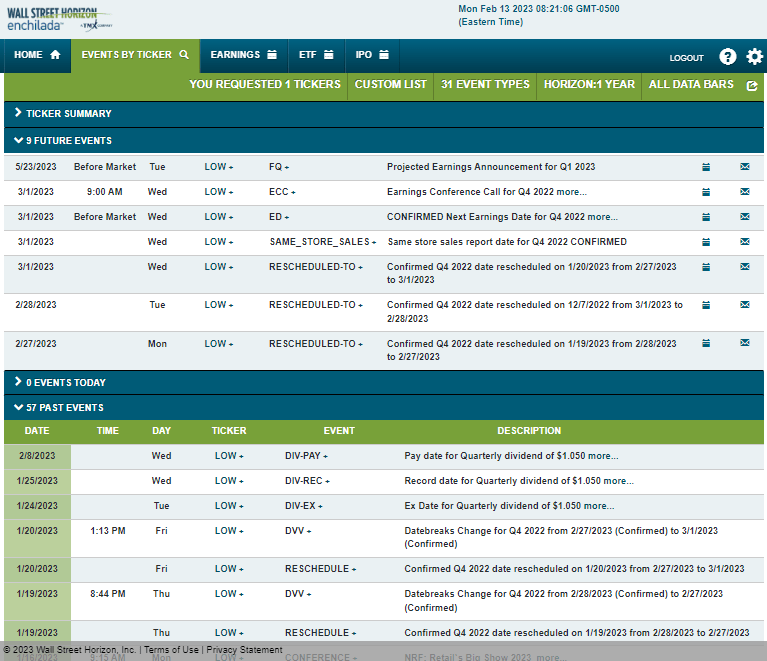

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Wednesday, March 1 before market open with a conference call later that morning. You can listen live here. Lowe’s has rescheduled the earnings date three times, but the original reporting date is where it has landed. If a firm delays an earnings report, that can portend poor news to be reported, but that’s not the case here.

Corporate Event Risk Calendar

Wall Street Horizon

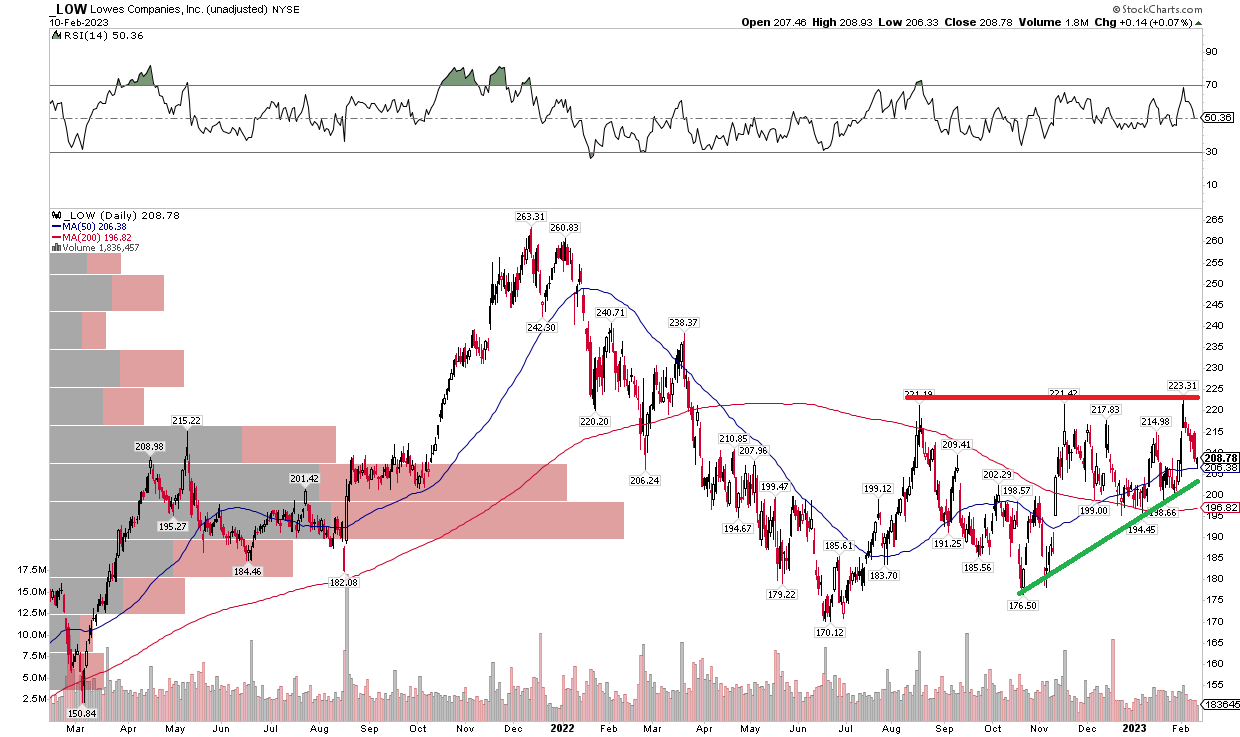

The Technical Take

With a good valuation and an earnings date on tap, how does the chart look? Notice in the graph below that shares are consolidating under resistance in the $221 to $224 range. It’s an ascending triangle pattern that has taken shape after the stock notched a low in June – well before the market’s October nadir. It’s hard to determine if this pattern is a continuation of the downtrend off the late 2021 high or if it’s a continuation from the June bottom.

The key is to watch for a breakout above $225 or a breakdown below $195 or so. That’s also where the rising 200-day moving average comes into play. What’s encouraging for the bulls is that the 200-day has gone from downward to upward sloping – indicative of a bearish to bullish trend change. Overall, the technicals suggest a wait-and-see approach.

LOW: Consolidation With Resistance in the $220s

Stockcharts.com

The Bottom Line

I like the valuation ahead of earnings next month, even though the chart is more neutral. Overall, though, long-term investors should like the earnings multiple and profitability of Lowe’s. I see upside potential here that can really get going above $225.

Be the first to comment