BING-JHEN HONG

Company Description

Costco (NASDAQ:COST) is a global retailer which operates “big barn” style warehouses and ecommerce websites. Sales are made exclusively to members only.

At the time of writing this report Costco operates 838 warehouses in the US, Puerto Rico, Canada, Mexico, Japan, United Kingdom, South Korea, Taiwan, Australia, Spain, France, China and Iceland.

The product range includes nationally branded and private label products in a wide range of categories (fresh food, grocery, furnishings, alcohol, clothing and electronics to name a few). Costco also sells auto fuel at most locations.

Fuel is termed a warehouse ancillary category. Other ancillary products available at most locations include pharmacy, optical, hearing aids, food court and auto tire purchases and installation.

Product categories generally comprise high sales volumes and rapid inventory turnover. Costco merchandises around 4,000 active stock keeping products (SKU’s) in its warehouses and around 11,000 SKU’s on its ecommerce site. Many products are only offered in multi-pack or case configurations.

I estimate that Costco is the 3rd largest publicly owned retailer in the world by both market capitalization ($US 223B) and annual sales turnover ($US 231B) with Walmart (WMT) and Amazon (AMZN) being larger. Costco is currently the 28th largest public company in the US by market capitalization.

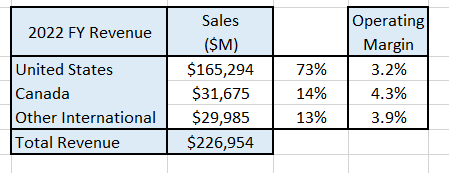

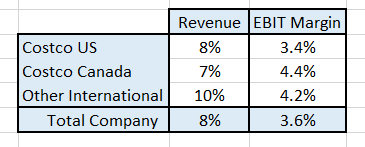

Costco is organized into 3 reportable divisions as shown in the following table:

Author’s compilation using data from Costco’s 10K-filings.

The total revenue includes Membership Fees of $4,224 M.

Costco categorizes its product mix into 4 categories and the 2022 sales mix comprised 39% food and sundries, 27% non-foods, 13% fresh foods and 20% warehouse ancillary and other businesses.

Business Overview

Costco commenced operations with its first store in 1983 and started to gain momentum in 1993 when it merged with another US company called Price Club. Customers must buy a membership in order to access a Costco warehouse.

Costco’s value proposition is based on high quality goods and services at competitive prices. It strives to be recognized by its customers as the price leader in its categories.

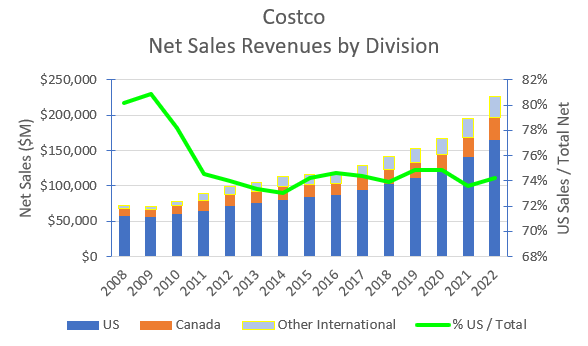

Costco opened its first international location in Canada in 1985. Its international footprint expanded as a result of the merger with Price Club who had established a Mexican operation in 1992. Costco has been expanding the number of its international warehouses both in existing countries and in new countries ever since. Since 2015 the rate of expansion of warehouse numbers is evenly split between the US and the rest of the world and this is reflected in the following chart which shows the net sales by division:

Author’s compilation using data from Costco’s 10-K filings.

Costco has handled its international expansion extremely well. Unlike other global retailers there have been no significant missteps or costly asset write-downs. This particularly shows the benefit of expanding organically and not by acquisition.

Costco commenced its ecommerce operations in April 2001. The reach of the ecommerce site is limited to only a few countries and is likely to expand over time. Unfortunately, the company does not provide any detailed information about the size of this operation.

Costco’s Strategy

Costco originally pitched its target markets as both the wholesale supplier for small business and as a cheaper alternative for individuals (particularly those who purchased in bulk quantities). This is reflected in its choice of trading name – Costco Wholesale.

Costco focuses on a limited range of high-volume turnover goods and aims to be the market price leader for these items. The narrow range of goods allows for a streamlined inventory management system and the high volumes provides Costco with leverage over its suppliers.

The requirement for customers to be members is both a blessing and an impediment to its performance. The key benefit being the cost-free source of revenues generated by membership subscriptions, but the major impediment is that the target market is restricted to those prepared to pay for the membership fee.

Costco’s strategy provides for significant expansion in warehouse numbers (particularly internationally) and within its product offering (although care needs to be taken in the selection to ensure that new products meet the supply chain criteria).

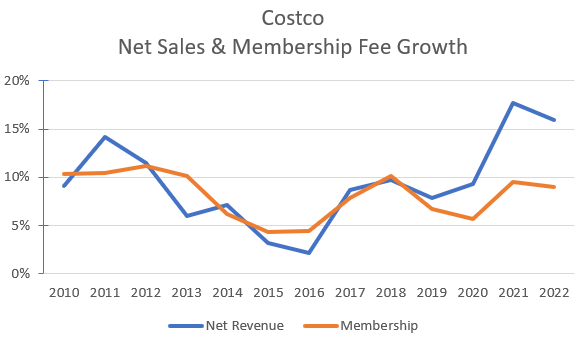

The success of the strategy to date can be observed through the following chart which shows the historical growth rate in Net Sales and Membership Revenues:

Author’s compilation using data from Costco’s 10-K filings.

The chart indicates that Costco has been clearly out-performing its sector in regards to net sales growth for many years.

Costco’s Historical Financial Performance

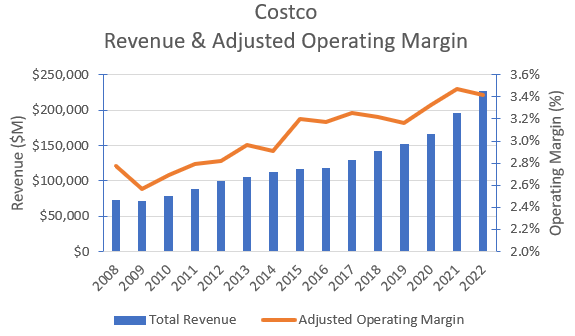

Costco’s consolidated historical revenues and adjusted operating margins are shown in the chart below:

Author’s compilation using data from Costco’s 10-K filings.

It should be noted that I have adjusted Costco’s reported Operating Income by converting operating leases to debt and removing the impact of pre-opening expenses (I have capitalized them).

The chart highlights:

- Revenues have been growing at over 8% compounding for the last 10 years (an even faster rate over the last 5 years.

- Revenues were not noticeably impacted by COVID.

- Unlike many other retailers, operating margins have been increasing every year for more than 10 years.

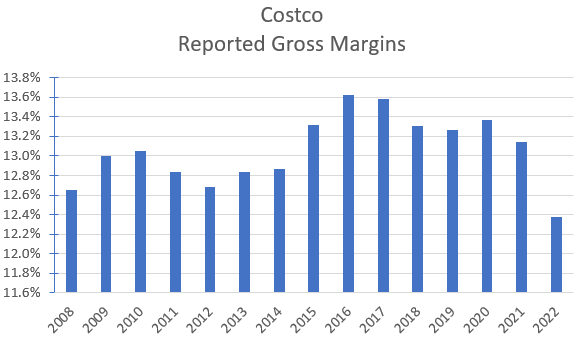

I estimate that Costco’s operating margins are significantly lower than the sector’s median (4.1%) indicating that Costco is keeping true to its strategic market positioning (this is confirmed in the chart below showing Costco’s gross margin trends). This is probably contributing to revenue growth exceeding the sector’s average.

Author’s compilation using data from Costco’s 10-K filings.

I suspect that the recent decline in gross margin is due to higher shipping costs across the supply chain and should be temporary. I estimate that Costco’s gross margin is just slightly higher than the lowest decile for the sector. This once again highlights how Costco’s strategy is being executed.

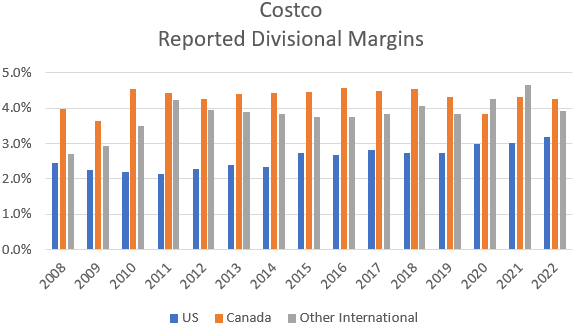

Unlike many other retailers (Walmart for instance), Costco can achieve higher margins in its international divisions. The following chart shows the historical reported margins for Costco’s operating divisions:

Author’s compilation using data from Costco’s 10-K filings.

The data shows that non-US operating margins have been remarkably consistent whilst US margins are slowly moving higher. The important point here is that Costco can potentially continue to increase the rate of international revenue expansion and at the same time increase its net operating margin.

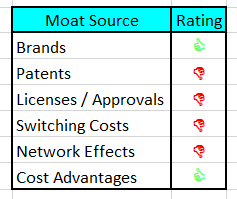

Costco’s Moat

My moat assessment for Costco is shown in the following table:

Author’s model.

The sources of strength in Costco’s moat come from:

- an excellent brand which is well respected by its customer base.

- the relatively lower operating cost model it has created through the strategic criteria used to determine the product range, the configuration of its warehouses and the layout of its stores.

- the low overhead cost culture that appears to be installed throughout the company.

- the potential cost advantages it gains from its suppliers by virtue of its scale.

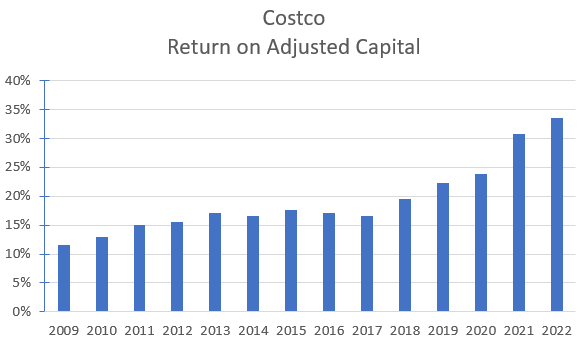

I believe that Costco’s moat may be relatively narrow, but it is very deep. This is supported by the company’s return on invested capital (ROIC) which is shown in the chart below:

Author’s compilation using data from Costco’s 10-K filings.

This chart confirms that Costco is one of the world’s best retailers. Its ROIC is in the highest decile for the sector.

As a result, I conclude that Costco’s moat is strong.

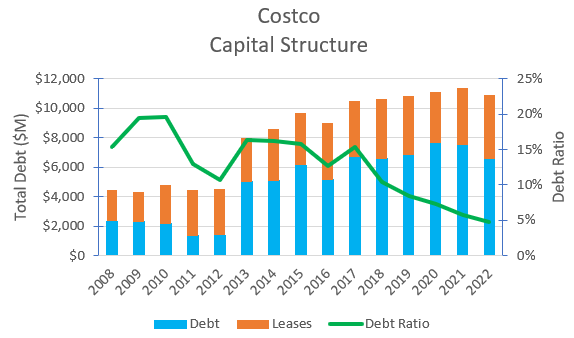

Costco’s Capital Structure

Costco has been progressively lowering its debt ratio for more than 10 years. At the end of their last financial year, I estimate that Costco’s debt ratio is in the sector’s lowest quartile. This is surprising as most major companies strive to maintain many of their balance sheet metrics in line with the sector averages.

Author’s compilation using data from Costco’s 10-K filings.

I have no concerns about Costco’s capital structure, and they have sufficient operating cash flows to more than cover their annual interest payments.

The balance sheet could easily absorb additional debt to fund a significant acquisition or to increase the level of stock buybacks.

Costco’s Cash-Flows

The following table summarizes Costco’s cash-flows over the last 10 years:

Author’s compilation using data from Costco’s 10-K filings.

From the table we can see that Costco’s operations have generated $30,026 M in free cash flow after reinvestment. They have increased their debt levels by $5,945 M. This means that there was $33,129 M available to return to shareholders. The company has paid out $22,341 M in dividends and spent $3,512 M on buying back stock.

It is noted that Costco in some years pays a “special” dividend to shareholders as a means to reduce its excess cash balance. The most recent special dividend was in the FY2021 where $10 per share was paid to shareholders. The company has been paying a special dividend every 2nd year since 2013 (but it was not paid in FY2019 probably due to the uncertainty associated with the pandemic).

Very few large companies return such a high proportion of their free cash flow back in dividends (it is thought to rob the company of flexibility because if the company lowers its dividend rate it is a bad financial signal to the market). The dividend is safe as it is easily covered by the free cash flow. Costco has increased its dividend every year since it paid its first dividend in 2004 and I can see no reason why this won’t continue for the foreseeable future.

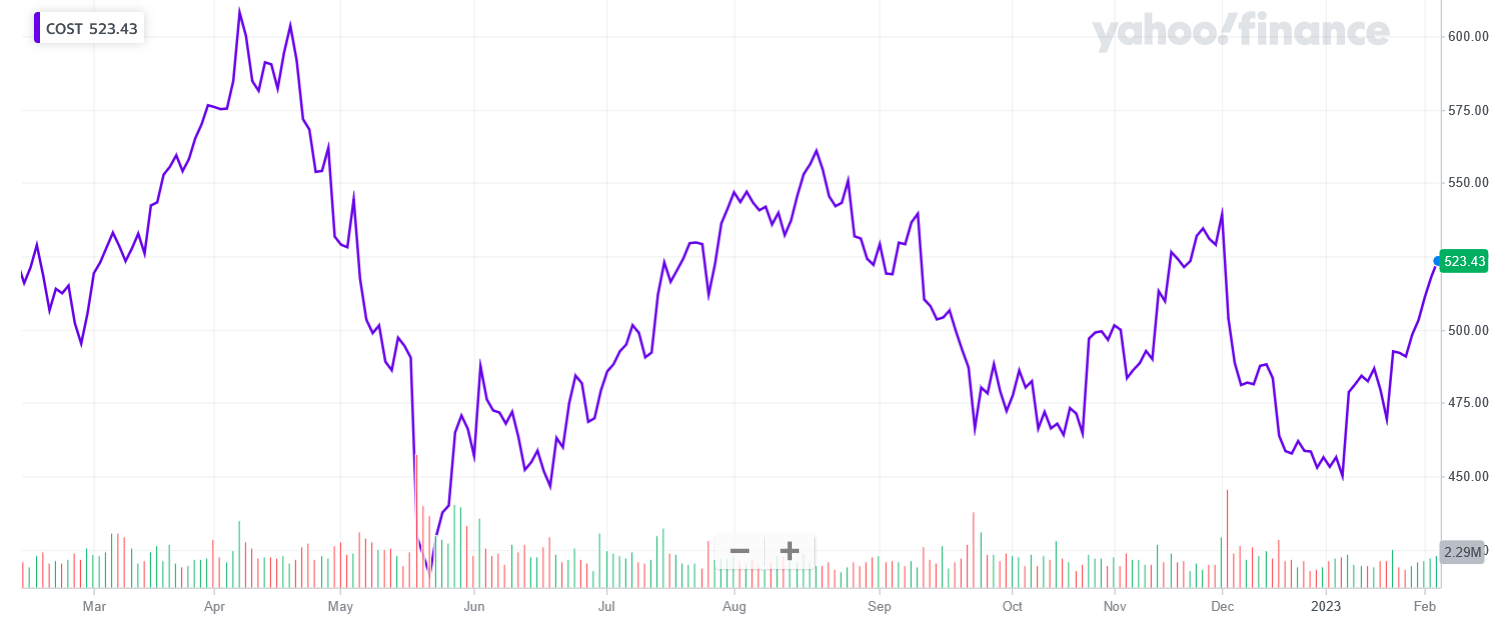

Recent Share Price Action

Yahoo Finance

Costco’s share price has tended to follow the broader market over the last 12 months but in aggregate terms it has out-performed the market by a reasonable margin.

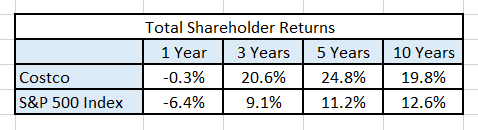

Historical Returns

Author’s compilation using data from Yahoo Finance.

The data indicates that Costco has significantly out-performed the S&P 500 index over the entire economic cycle. This is very unusual for a retailer and perhaps demonstrates how extraordinary a company Costco may be.

Key Risks Facing Costco

Costco appears to be a very special retail company. Its financial metrics are far superior to almost every company in its sector. To a large degree I think the performance of the company has come from the stability of its high-quality Executives and Board. There has been very little turnover within the executive ranks. This is both a blessing and a risk.

Costco’s executive team are extremely experienced and have done an excellent job but they are relatively old (the CEO is 70 years of age and the CFO is 66 years old). My concern is that as these veterans reach retirement, will the replacements be able to continue the discipline of strategic focus in order to sustain the company’s financial performance?

Only time will tell.

My Investment Thesis for Costco

The current macro consensus is that the US and most of the western world is heading into a recession later this year. There is disagreement about how severe the recession will be. During the 2008 / 09 recession Costco’s sales and margins declined although it is noted that during the recent COVID “mini recession” their performance was not impacted at all.

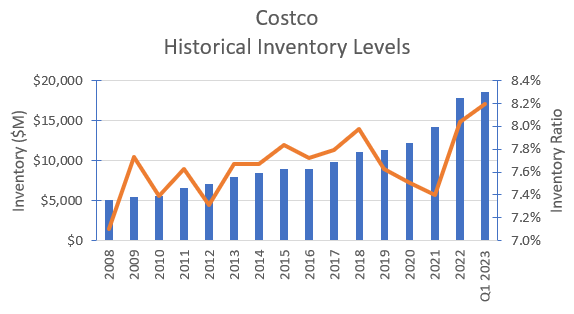

Retailers can often signal a coming recession when their inventory growth begins to outpace sales growth. The following chart shows Costco’s historical inventory levels:

Author’s compilation using data from Costco’s SEC filings.

The chart indicates that Costco’s inventory position started to deteriorate during 2022. The company has acknowledged that there were problems during the COVID pandemic initially with too little inventory but then more recently in the post COVID supply chain recovery.

I am reasonably confident that the Costco executive team will have this issue under control, and it will not be a significant problem.

I have accepted the consensus revenue projections for the next 2 years.

My story for Costco is reasonably positive. As indicated by the consensus estimates, Costco will suffer a slowdown in growth as the western world goes through a mild recession. I expect that Costco will continue to increase their warehouse numbers by around 20 per year for the next 6 years before starting to slowly decline.

Although the US will remain the biggest and most important market for Costco, higher revenue growth will come from outside the US. This slight international bias will allow Costco’s net margin to increase over time due to the higher international margins.

My estimate for divisional revenue growth and operating margins for the calendar years 2025 to 2028 are shown in the following table:

Author’s model assumptions.

Valuation Assumptions

In summary, my forecast scenario for Costco has the following inputs:

- Consensus revenues for 2023 and 2024. Total revenues will then grow at 8% ± 1.5% for the period 2025 to 2028.

- Adjusted Operating Margins (which have been adjusted for the impact of operating lease expenses and expensed new store opening costs) will be 3.6% ± 0.2% to perpetuity.

- Capital productivity (as represented by Δ Sales / Net Capital) will decline from the current levels (12.9 which is extraordinarily good) to 9 ± 1.

- The current Return on Invested Operating Capital (around 33%) will decline over time before settling at 12% ± 1% in perpetuity which reflects the enduring moat around the business model.

- I have used the Capital Asset Pricing Model (CAPM) to estimate the current cost of capital to be 7.1% and I expect that the mature cost of capital will be 7.0% ± 0.25% (reflecting the low range of risks to cashflows).

- I have assumed a long-term effective tax rate of 25% which reflects the various tax rates in the countries in which Costco’s operating profits are generated.

- I have used the diluted share count from the most recent 10-Q as the current share count because insufficient information is provided for me to value the outstanding management options.

- Minority holdings – I have ignored the minority holdings because they are not material.

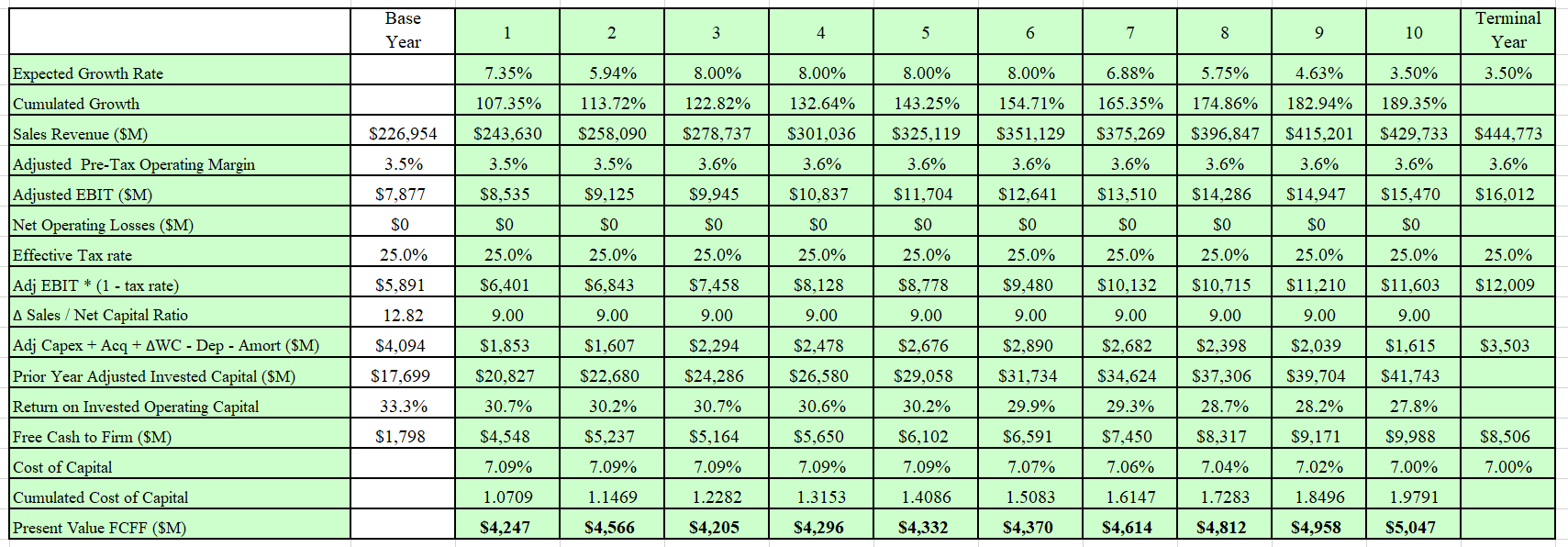

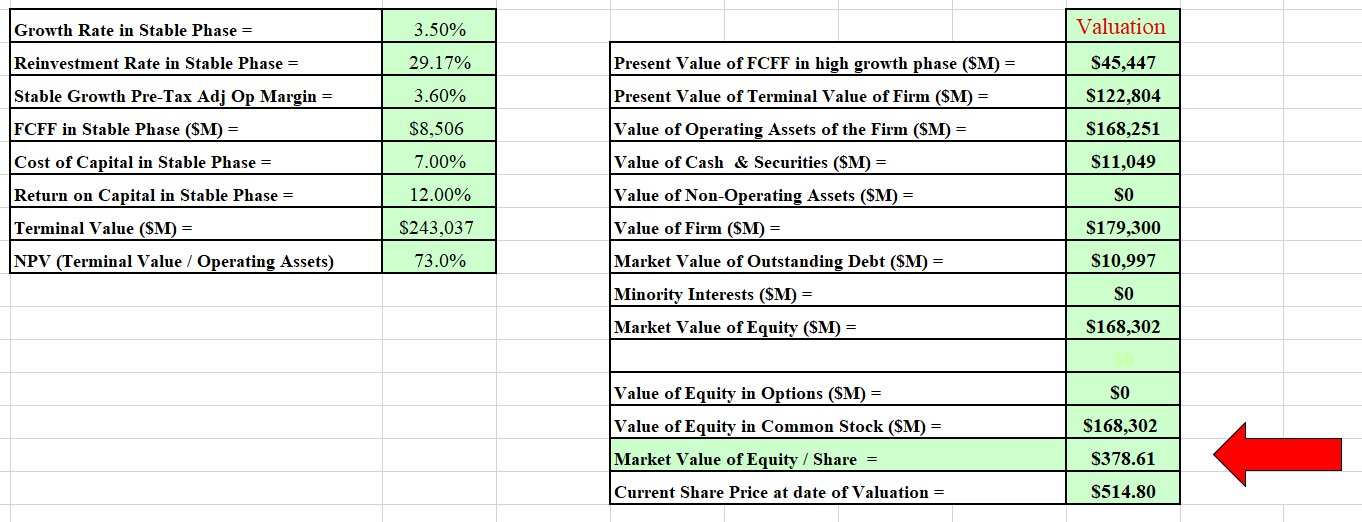

Discounted Cash Flow Valuation

The output from my DCF model is in $USD:

Author’s model. Author’s model.

The model estimates Costco’s Enterprise Value is $179,300 M and the Equity Value is $168,302 M. This equates to a mid-point value per share of around $379.

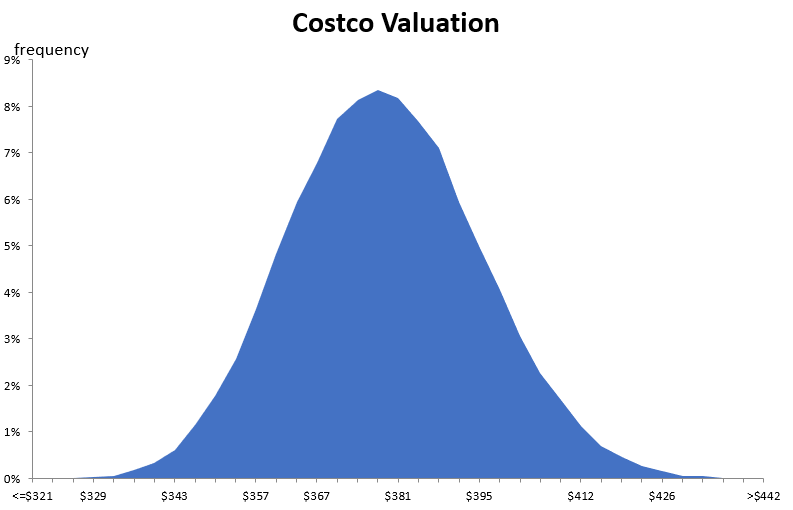

I also developed a Monte Carlo simulation for the valuation based on the range of inputs for the valuation. The output of the simulation is developed after 100,000 iterations.

The Monte Carlo simulation can be used to help us to understand the major sources of sensitivity in the valuation.

Author’s model.

The simulation informs us that the valuation is equally sensitive to the cost of capital, operating margins and the expected sales growth.

The simulation indicates that at a discount rate of 7% – the valuation for Costco’s is between $320 and $442 per share with a typical value around $378.

This would indicate that Costco is currently expensive relative to its intrinsic value.

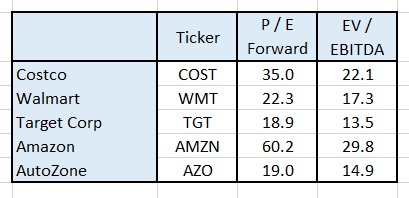

How is Costco priced relative to other retailers and ecommerce companies?

The following table shows Costco’s current relative pricing metrics relative to others retailers:

Author’s compilation using data from Yahoo Finance.

Certainly, the data indicates that Costco is highly priced relative to this group of retailers (AutoZone is not a competitor, but it is a high quality retailer).

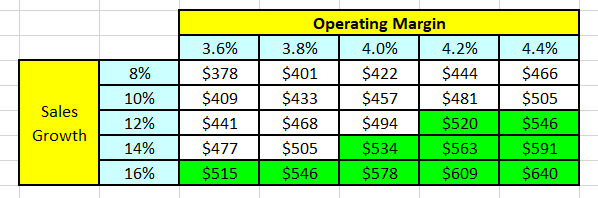

What valuation inputs would need to change for Costco to be fairly priced?

I believe that my estimate of Costco’s cost of capital is fairly reasonable (my estimate is 7%). I have based this conclusion on Professor Damodaran’s 2023 data summary which indicates that my estimate would place Costco in the lowest quartile for all US companies. As a result, I will leave the cost of capital out of this analysis.

The remaining key significant variables in the valuation are the expected sales growth and the terminal operating margin. I have used my model to vary both of these variables and I have noted the corresponding intrinsic valuation. The results are shown in the following table:

Author’s model.

The table indicates:

- If Costco’s margins were to be unchanged then the current share price assumes a revenue growth of 16%.

- If Costco’s sales growth were to be unchanged (8%) then the operating margin must be above 4.8%.

I think that the various combinations which would satisfy the current share price are extremely unlikely. This leads me to believe that Costco is currently over-priced.

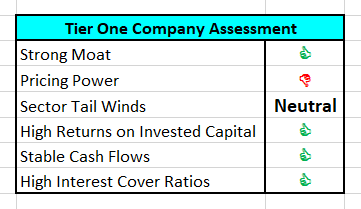

Final Recommendation

For each company that I value I also assess what role this company could potentially play in my portfolio. The cornerstone of my portfolio is what I term “Tier 1” companies. These are the companies that I hold for the long term and where I invest most of my cash.

My high-level assessment for Costco is:

Author’s model.

Costco almost ticks every box – it is an excellent retailer (possibly the best in the world). Costco’s stable cash flows are very attractive during times of economic uncertainty (such as now).

At the right price Costco would be an excellent addition to anyone’s portfolio.

The US economy has entered a period of tightening monetary policy (interest rates have been rising) and inflation is moderating (inflation may have peaked). Historically this has been a very risky environment for the stock market. Many investors (me included) have been trimming their equity holdings in anticipation of a future market correction.

I think that the opportunity to buy Costco near its intrinsic value will come at some point later this year. The last time we had an opportunity to buy it cheap was during the COVID market correction.

For existing owners of Costco I think that the stock is currently a SELL or at least I would be trimming my holdings and taking some profits.

Be the first to comment