Annie Otzen/DigitalVision via Getty Images

The Lovesac Company (NASDAQ:LOVE) designs, manufactures, and sells furniture. We have published an article on the firm in June 2022, titled: “Declining Consumer Confidence May Slow Lovesac’s Growth”. At that time, we have rated LOVE’s stock as a hold, due to the following reasons:

- Strong financial performance in the first quarter with double-digit sales growth across all distribution channels.

- Gross margin contraction in Q1 due to the increased inbound transportation costs, despite the improving product margin.

- Declining consumer confidence has been expected to result in lower demand for Lovesac’s products in the near term, potentially slowing the firm’s growth.

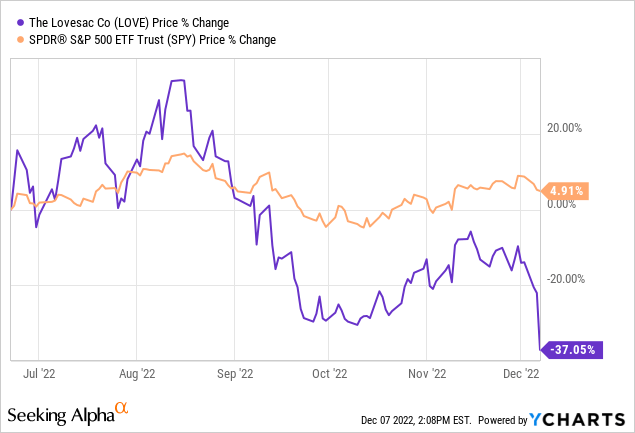

Since our writing, the firm has lost more than 37% of its market value, substantially underperforming the broader market.

Today, we are revisiting our thesis on LOVE’s business and highlight some of the key results from the third quarter.

Q3 results

Sales

LOVE’s net sales have increased once again by double digits, 15.5%, year-over-year.

Results

While growth has slowed compared to the prior year, we believe that in the current market environment these results may be a proof that there is a demand for LOVE’s products, even during periods of poor consumer sentiment.

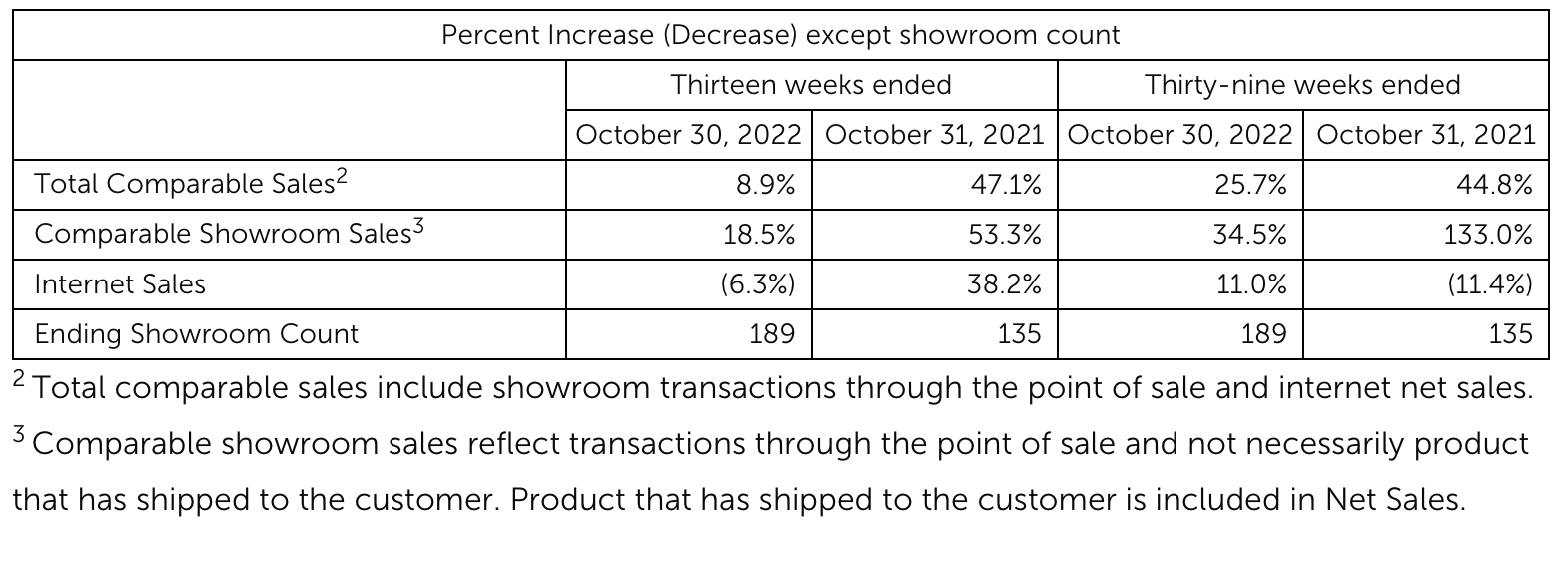

The following table breaks the sales results further down.

Percent increase

Total comparable sales have increased by 8.9% (in contrast to the more than 47% increase in the year ago period), comparable showroom sales have grown by 18.5% (in contrast to the more than 53% growth in the year ago period), while internet sales have declined by 6.3%.

The main drivers of the comparable showroom sales growth, compared to the prior year period, were:

- Higher point of sale transactions

- Strong promotional campaigns

- Addition of 41 new showrooms and 13 new kiosks

The reintroduction of physical pop-up-shops in Costco and the addition of 17 new Best Buy shop-in-shops, for a total of 22 Best Buy shop-in-shop locations have also contributed to the revenue growth.

The reason for the internet sales decline can be largely explained by the changing consumer behavior. As the impacts of the Covid-19 pandemic are fading, people are spending more time shopping in physical stores, rather than online, causing the internet sales metrics to decrease, in the case of LOVE.

Costs

While the gross profit has increased along with the net sales, the gross margin has contracted by as much as 300 basis points compared to the same period in the prior year. The two primary factors leading to the contraction were:

- Increase in total distribution and related tariff expenses (~160 bps)

- Decline in product margin (~140 bps)

We would like to pay attention to the declining product margin here. In order to support the sales growth, the firm has had to spend substantially more on advertisement.

Advertising and marketing expense increased 20.3% due to continued investments in marketing spend to support our sales growth and expand brand awareness. As a percent of net sales, advertising and marketing increased by 50 basis points due to a slight increase in media spend to support our third quarter net sales growth.

They have not been able to offset these cost increases by pricing, meaning that the demand for their products is likely to be relatively elastic. For this reason, we believe that as long as the consumer sentiment is poor, we are not likely to see a reversal of the margin contraction.

Further, SG&A expense as a percent of net sales have also increased, by as much as 720 basis points. Deleveraging of employment costs, infrastructure investments, rent, selling related expenses, travel, and insurance have been the primary contributors, partially offset by the increase in the equity-based compensation.

As a result of the cost increases, the firm ended the quarter with an operating- and net loss of $11.6 million and $8.4 million, respectively.

Inventory

Inventory management plays a key role, when it comes to margins. Rapidly increasing inventory may be a sign that the demand for a certain product is not as strong as expected. It may be a temporary or a permanent phenomena. If it is a permanent one, then the firm likely needs to use significant discounting to get rid of their “obsolete” goods and reduce their inventory.

The firm has made the following comment one their inventory levels:

Total merchandise inventory was $154.5 million as of October 30, 2022 as compared to $94.5 million as of October 31, 2021 with the year over year change principally related to a stock inventory increase of $43.2 million coupled with an increase in freight capitalization of $16.9 million related to an increase in inbound freight expense.

In our opinion, an increase of $43.2 million in the stock inventory is substantial. When considering investing in LOVE’s business, one has to keep in mind that margins may be hurt in the near term by inventory management issues.

Conclusion

In our opinion, the firm has done a great job by achieving sales growth despite the challenging macroeconomic environment. On the other hand, we need to highlight that growth has substantially slowed compared to the prior year and that they have spent a lot more on advertising, which has led to margin contraction.

The firm has not been able to pass over the excess costs to the customers, which may signal that the demand for LOVE’s products is elastic. For this reason, we do not foresee a substantial improvement in the margin in the near term.

The growth of inventory levels may be concerning. If inventory becomes obsolete, larger discounting may be needed to get rid of the excess inventory, which may hurt the margins.

We maintain our “hold” rating.

Be the first to comment