Tsuji

Introduction

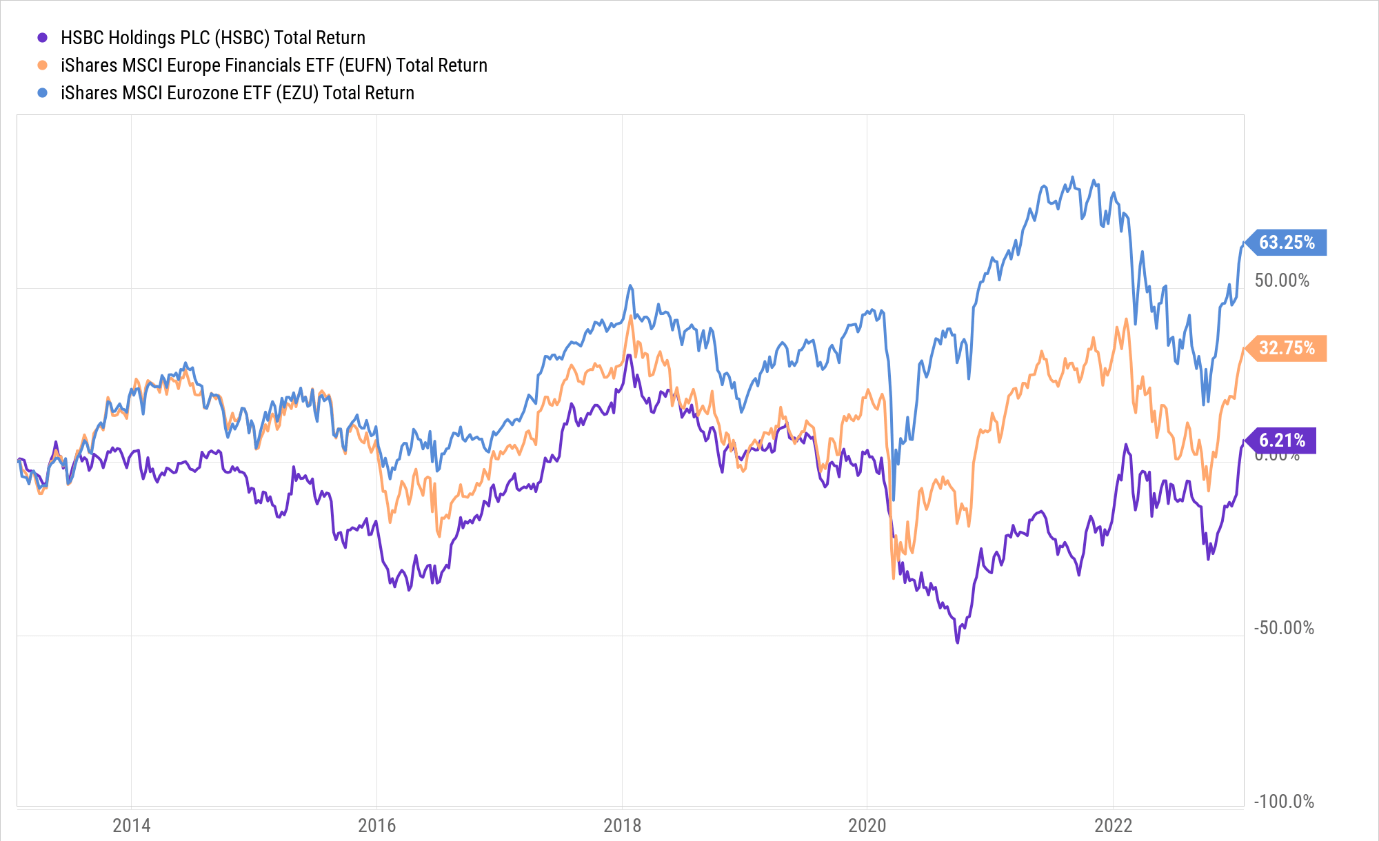

Over the last decade, the ADR of Europe’s largest bank by assets- HSBC Holdings PLC (NYSE:HSBC), hasn’t been a very rewarding investment for investors. We’ve only seen returns within the single-digit terrain, even as a broader European banking portfolio (EUFN), and another diversified portfolio of European stocks (EZU), comfortably outperformed HSBC by roughly 5x and 10x respectively!

YCharts

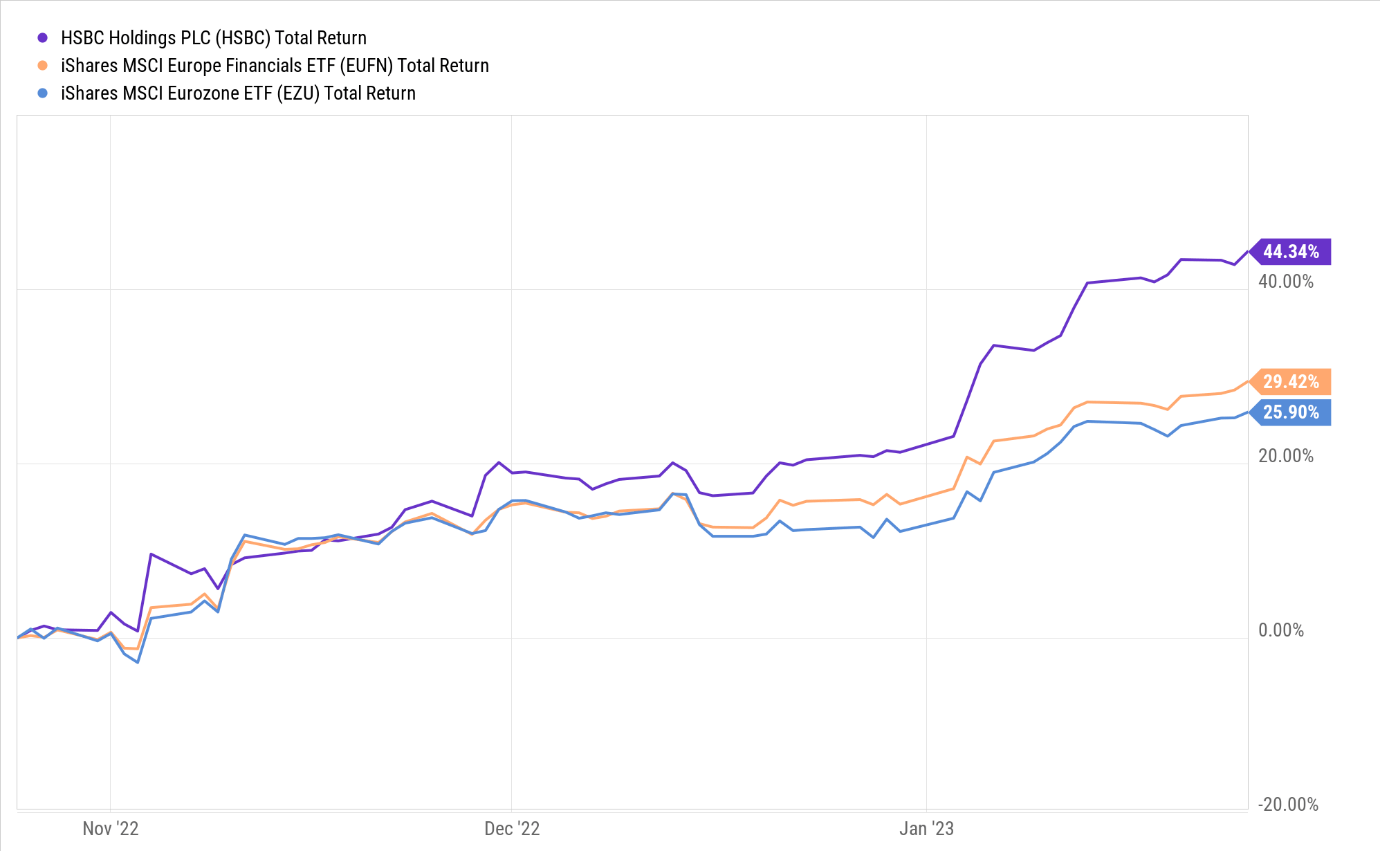

Whilst the long-term alpha track record has been underwhelming, momentum in HSBC has picked up off late, with the stock generating solid returns of 44%, and beating the other two options over the last three months.

YCharts

Prospective investors may now be wondering if it’s a good time to get on board, or will this prove to be another false dawn of sorts? Here are a few pointers to help you take a call on HSBC.

A Few Pointers

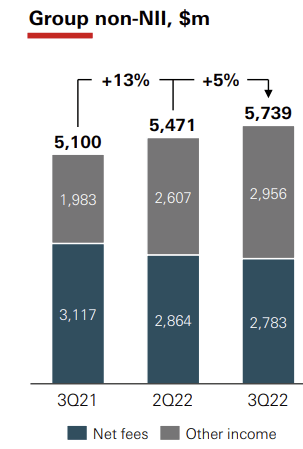

- HSBC’s long-term goal is to become a mid-single-digit revenue growth stock, and much of the revenue growth is expected to be driven by fee and insurance-based services. Put another way, you ideally want HSBC’s Wealth and Personal Banking Division (WPD) to be firing on all cylinders for that to happen. Just for some context, WPB currently contributes 42% of HSBC’s group revenue and accounts for 29% of tangible equity (management wants to grow this ratio by 600bps in the medium to long term). Unfortunately, HSBC’s net fees have been trending lower both on a YoY (down 11%) and QOQ basis (down 3%), and much of the weakness was driven by subdued wealth management fees on account of challenging equity market conditions. In Q4, this will likely have shown some improvement given the pick-up in risk sentiment. In the medium term, HSBC ought to solidify this business and make it less volatile by shifting the focus from HNW individuals to mass affluents who are increasingly growing wealth organically and benefitting through inheritances. I believe HSBC is exploring opportunities to service the mass-affluent group in China, but there’s potential to make further inroads and build a loyal client base over the world, given that only 27% of global wealth management firms currently service this cohort.

Q3-22 Presentation

- HSBC’s confidence in its asset quality took a turn for the worse in Q3 and much of the outlook here will rest on what happens in the UK, and the Chinese commercial real estate market. Just for some context, in Q3, the estimated credit loss charge ratio spiked to 0.43% from 0.18% in Q2 (a year ago the bank had benefitted from ECL releases which accounted for 0.23% of average gross loans). In FY23, the ECL ratio will likely hover closer to 0.4% levels. If you look at HSBC’s global mortgage book, the bulk of this comes from the UK (~42%). In recent periods, HSBC’s LTV (Loan to value ratio) on fresh UK mortgage lending has spiked to 67%, well above the average LTV of 49%. This puts it in a vulnerable spot as the cycle appears to have turned. In 2023, UK home prices are expected to be the worst hit across the globe (Fitch expects a decline of 5-7%, whilst local experts expect a bigger decline of 10-15%). The indication is that the base rate in the UK could rise from current levels of 3% and cross 5% by the final quarter of this year. Think about what that could do for mortgage debt servicing and the consequences on asset quality when a substantial chunk of fixed-rate mortgages will likely expire this year and need to be refinanced. Nonetheless, the recent BoE credit survey points to a likely spike in default rates in Q1, at the very least. In the Chinese commercial RE sector, certain aspects should improve after a difficult 2022, but vacancy rates in tier 1 cities such as Beijing are still expected to grow even further to 20% as a lot of delayed supply comes to the market.

- The trajectory of HSBC’s cost dynamics in the near-term look encouraging. Firstly the company is in the midst of a transformation program which should bring through another $1bn of cost savings in FY23, following a likely cost-saving figure of less than $5.5bbn in FY22. Investors should also note that the Opex base effect for Q4-22 will be quite high (Q4-21 was $7.7bn), so there’s a good chance you actually see a YoY decline in Opex (just for some context, in Q3-22, opex per quarter stood at $7.2bn. Going forward in FY23, management expects to keep costs well controlled at just 2% YoY growth.

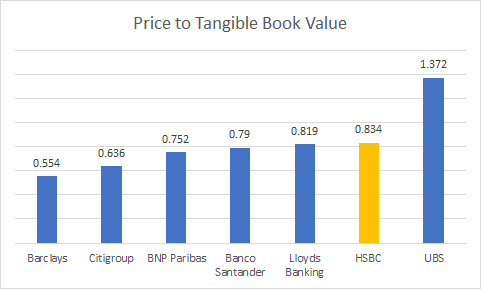

- The valuation facet of HSBC doesn’t look too attractive. Yes, it continues to trade below its tangible book value, but it is hardly the only bank with that unique characteristic. In fact, as noted in the image below, HSBC’s current price-to-tangible book value multiple of 0.834 is one of the highest amongst its peers, with only UBS trading at a superior multiple. Besides, relative to HSBC’s own valuation history, the current P/TBV multiple is ~7% pricier than its 5-year average.

YCharts

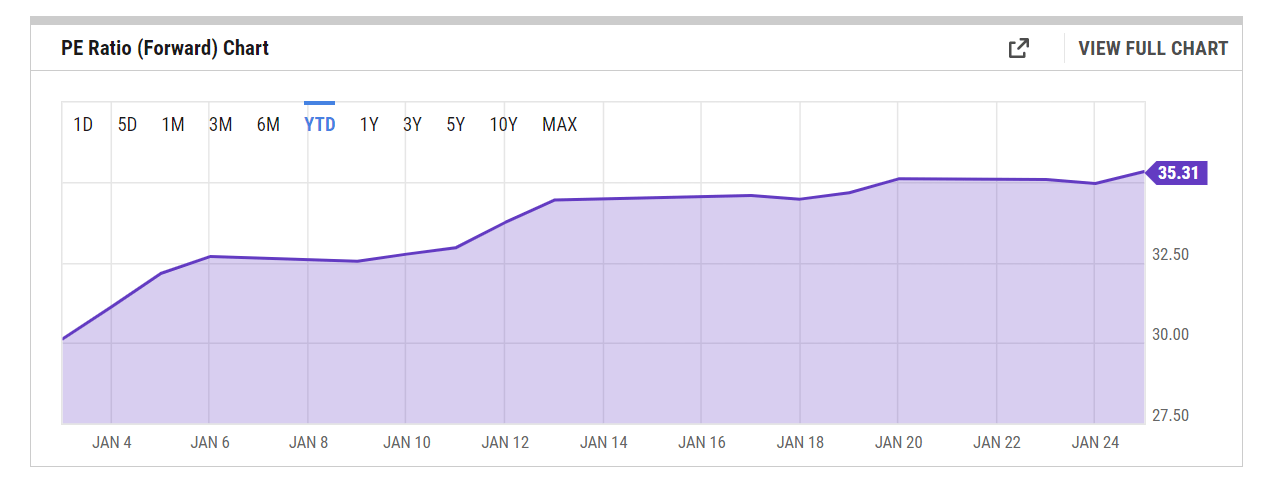

On the earnings front, YCharts consensus is currently expecting forward earnings growth of ~13%. When you juxtapose that figure against the pricey 35x forward P/E multiple you’d be expected to shed out, it doesn’t reflect well, particularly as that multiple already represents a ~5% premium over the 5-year average.

YCharts

- If you’re an income investor, you might be enthused to note that HSBC intends to reinstate its quarterly dividends this year with the intention of eventually reverting to “pre-Covid levels”. For the uninitiated, this had been canceled during the pandemic and was only initially brought back to 50% of the old level. Sell-side EPS estimates for FY23 point to a figure of $1.05. Based on the current share price of $37.08, and using the management’s target payout ratio of 50%, you’d be looking at a fairly useful forward yield of 1.4%.

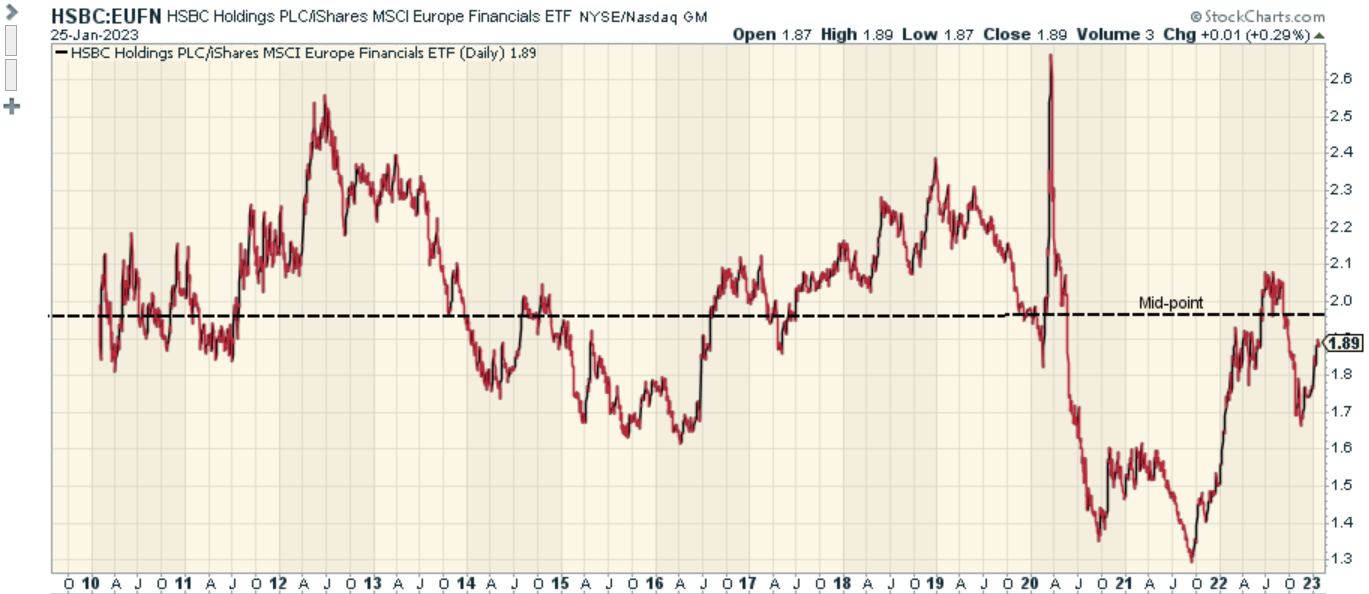

- HSBC may have been an attractive mean-reversion candidate in the European financials space towards the end of 2021 or early 2022, as the relative strength ratio of HSBC and EUFN was at record lows back then. That is no longer the case, and in fact, currently, the RS ratio is very close to hitting the mid-point of its long-term range.

Stockcharts

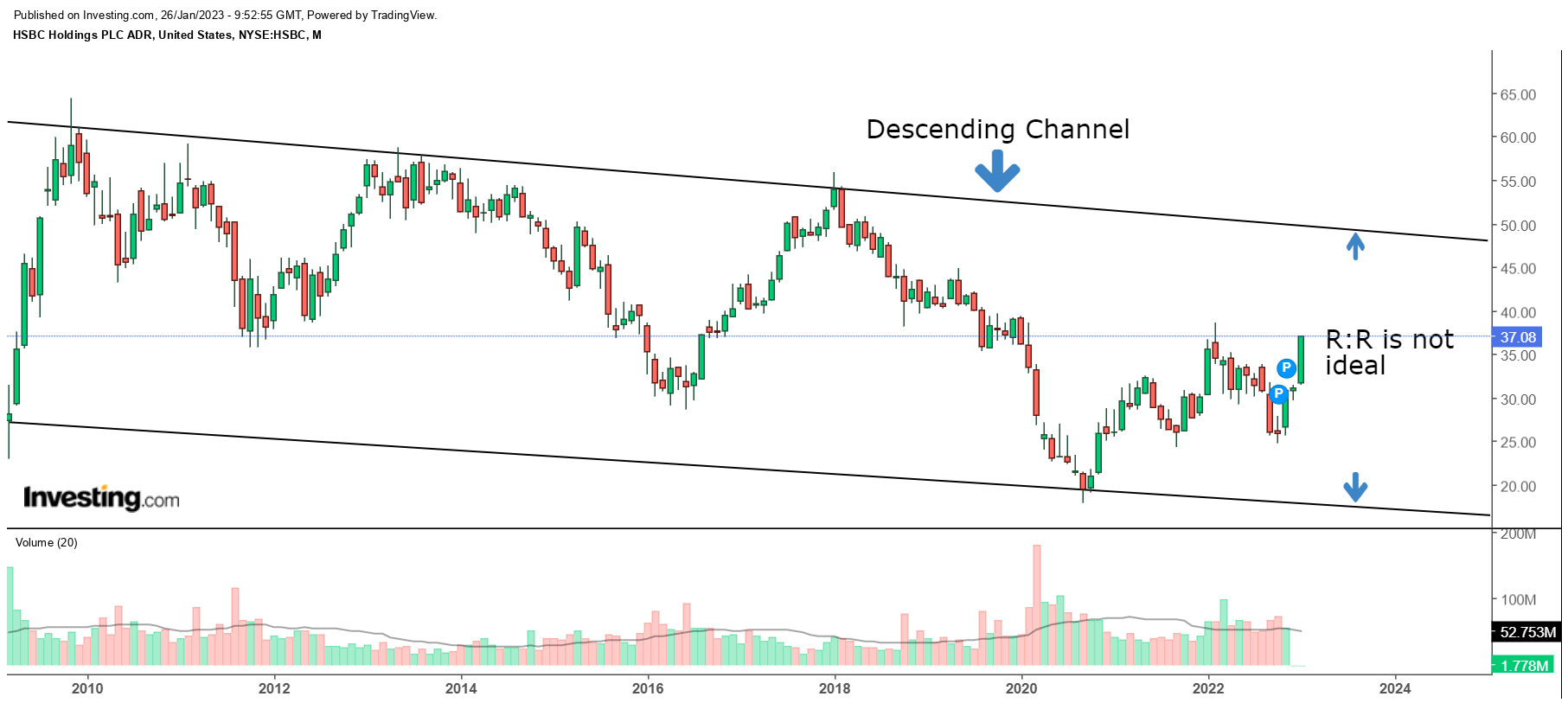

- Finally, I’d conclude by stating that the risk-reward for a long position in HSBC does not look too compelling at current price levels. The image below gives you a sense of the monthly price imprints since the GFC; in effect, what you have is a faint descending channel. Considering where the upper and lower boundaries of this channel are currently placed, it’s hard to feel overly enthused about entering the stock at the current price. Basically, you’re looking at sub-optimal reward-risk of less than 1x (0.54x, to be more precise)

Investing

Closing Thoughts

Considering the mixed narratives surrounding the fundamentals, the technicals, and the valuations, we rate the HSBC stock as a HOLD.

Be the first to comment