DaveAlan

Alaska Airlines provided its fourth quarter and full year earnings on Thursday before the opening bell. At the time of writing, shares of Alaska Airlines are more or less flat after missing earnings estimates on top and bottom line. In this report, I will analyze the results and comment on my view on Alaska Airlines stock.

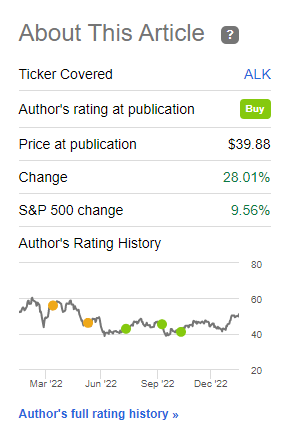

Alaska Airlines Stock Delivered

Seeking Alpha

In my previous report covering Alaska Airlines, I marked shares a buy, citing a disconnect between share price performance and the positive developments in its strategy that are upcoming as the company simplifies its mainline as well as regional fleet. Looking at share price performance, we see that the call has been largely correct.

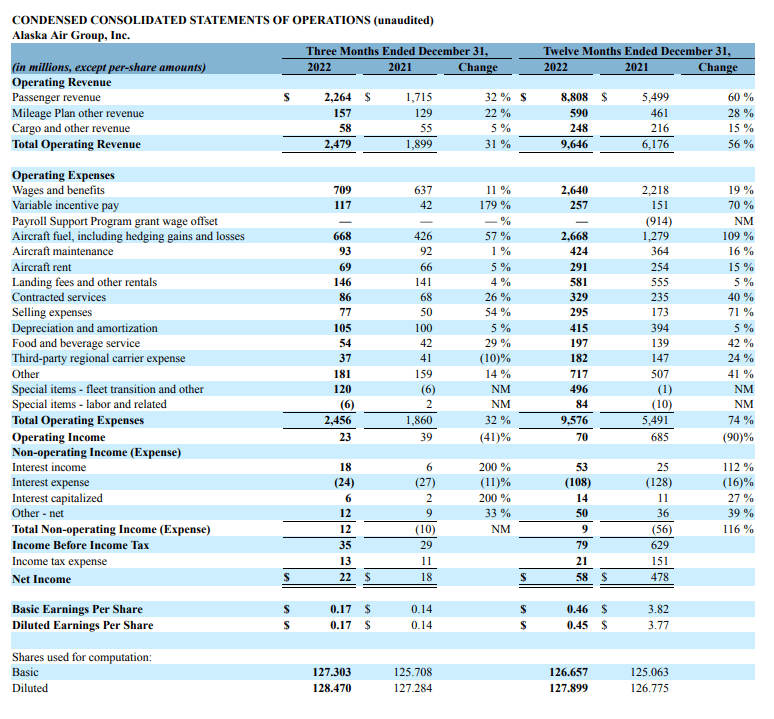

Alaska Airlines Results Decline

Alaska Airlines results (Alaska Airlines )

Looking at the results, we see that revenues were up 31%, driven by 12.3% passenger growth, a 23.4% jump in unit revenues. That really should not come as a surprise, pent-up demand being realized to a constrained market has the modus operandi for all airlines in 2022. It would be off if we would not have seen top line increases in that range for Alaska Airlines. For the full year, the topline improvements are even bigger as we see the annualized effects of the capacity improvement and the improvement in the demand environment which pushed unit revenues up. On quarterly operating income, we do see something interesting. The operating income declined 41% from $39 million to $23 million. I would say the Q4 2021 performance reflects the strength in Alaska Airlines’ business model while the Q4 2022 results reflect a higher cost environment as all airlines are facing due to inflationary and labor cost increases. However, what is unique to Alaska Airlines is that they are currently carrying the costs of fleet transitions that will render the airline more efficient in the future as the airline removes the Airbus fleet and its Q400s. Stripping the special items from the results, operating income would have been $137 million compared to $34 million a year earlier. So, that would indicate a strong improvement with significant room for margins to improve further.

For the quarter, Alaska’s numbers missed the consensus on revenues by $10 million and the EPS estimate by $0.01. I wouldn’t consider those big misses. There are two ways to look at the miss. The first one is that due to the winter storm in December, Alaska lost some revenues as it had to cancel several hundred of flights and I would consider that the most realistic way to explain the miss. The second way that somewhat could explain the top and bottom line miss is timing friction as Alaska Airlines is facing out aircraft. If it was expected that those aircraft would have remained in the fleet somewhat longer that would have led to higher revenues.

For the full year, adjusted earnings were $650 million or a 6.7% margin compared to a $240 million loss a year earlier. So, as we see on adjusted level for both the quarterly as well as the annual results, there was meaningful improvement despite operating on a 10% higher unit cost basis excluding fuel pressures.

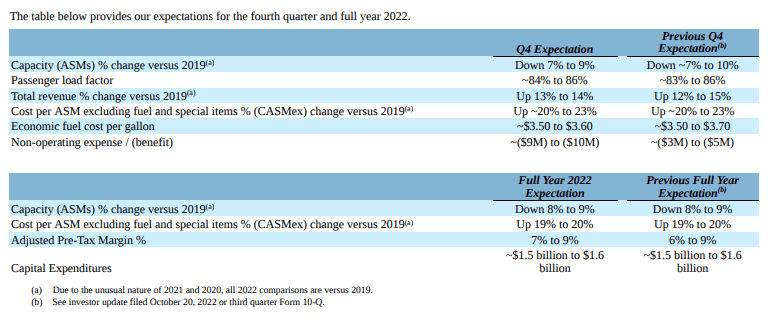

Operating metrics Alaska Airlines (Alaska Airlines)

So, instead of comparing to the analyst estimates, it might be more meaningful to see whether Alaska Airlines was able to deliver on its updated guidance from December 2022. For the quarter, capacity was down 10% exceeding highest capacity reduction compared to pre-pandemic levels guided for while passenger load factor was at the low side of the guided range with 84.1%. Revenues fell short of the guided range as 11% was achieved while an increase of 13% to 14% was guided for. This likely is the revenue impact from the winter storm. Unit costs excluding fuel came in at +24% compared to the +20% to +23% that was guided for while the economic fuel costs per gallon came it at $3.52 within the range.

For the full year, capacity was down 9%, matching the low end of the guided range while unit costs were up 20% as guided for and adjust pre-tax margin was 7.6% falling within the guided range. So, what we do see is that fourth quarter capacity was not quite as what was guided for likely and that drove unit costs up and produced a miss on top line as well as bottom line.

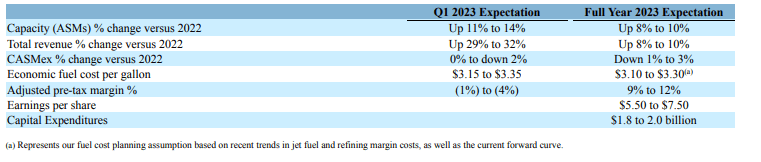

Alaska Airlines Guidance: Efficiency To Improve

Alaska Airlines Q1 2023 and full year 2023 guidance (Alaska Airlines)

For the first quarter, we see that Alaska Airlines is guided for a loss reflecting seasonality, but revenues are expected to improve further and capacity will be up 11 to 14 percent while revenues will be up 30% reflecting the strong demand environment while fuel costs are expected to fall. These items drive improving efficiency within the airline as more capacity is brought back to the market and its single-fleet initiative also is paying off as the last Airbus A320s and Q400 have been removed from service by the end of January. Those strengths in demand, strategy and fuel costs environment are carried forward into year and should drive up adjusted pre-tax margin to 9 to 12 percent, in line with the guidance provided in December.

Conclusion: Alaska Airlines Stock Remains A Buy

As I am wrapping up this report, Alaska Airlines stock is trading down 1.3%, but that is not something I am too worried about. Q4 revenues came in below what Alaska Airlines had guided for, but this mostly reflects the impact from the winter storm which led to cancellations at Alaska Airlines and also pressured capacity expansion and subsequently unit costs.

However, the main drivers underpinning the margin expansion remain in place. As a result, I do not see a reason to alter my buy rating on Alaska Airlines stock.

Be the first to comment