Gado/Archive Photos via Getty Images

Logitech International S.A., (NASDAQ:LOGI) through its subsidiaries, designs, manufactures, and markets products that connect people to digital and cloud experiences worldwide.

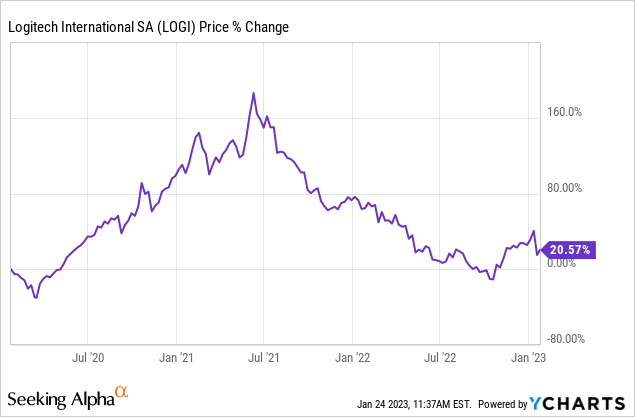

The firm has increased significantly in market value after the start of the Covid-19 pandemic, as more and more people had to set up their home offices. Since its peak in June 2021, the stock price has been gradually falling. The decline can be largely explained by the diminishing positive effects of the pandemic on the demand for LOGI’s products

In today’s article we are going to take a look at the firm’s latest earnings report and try to gauge, how the firm and its stock price may develop in the coming quarters.

Q3 FY2023 Results

Recently, LOGI has announced its latest quarterly earnings results, and it has missed both top- and bottom line estimates.

Sales came in at $1.27 billion, representing a decline of 22 percent in US dollars and 17 percent in constant currency, compared to the same period in the prior year. The decline has been observed across all segments.

- Gaming sales declined 16 percent

- Video Collaboration sales declined 21 percent

- Keyboards & Combos sales declined 22 percent

- Pointing Devices sales declined 14 percent

The CEO of the company has been highlighting the challenging macroeconomic environment as the primary reason for the declining sales figures:

These quarterly results reflect the current challenging macroeconomic conditions, including currency exchange rates and inflation, as well as lower enterprise and consumer spending, […] With these external headwinds, we continued to aggressively manage our costs in the quarter, while at the same time growing market share in key categories. Our long-term strategies remain unchanged and we remain committed to the growth trends that fuel our business.

Along with the sales, operating income and EPS have also declined by 33% and 31%, respectively.

As a result, Logitech’s outlook for fiscal 2023 has been downwards revised, expecting now a 13% to 15% decline in sales.

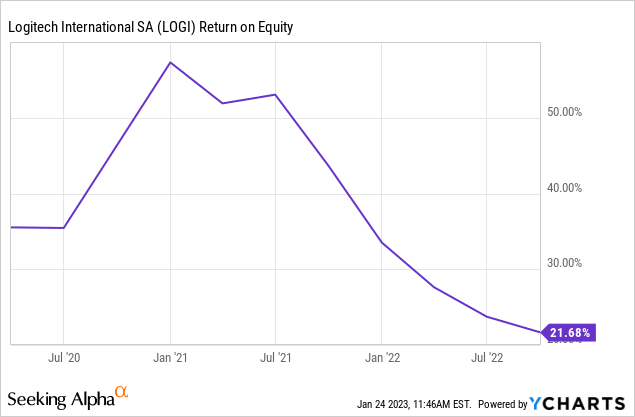

As the Q3 results were disappointing, we are now going to take a look at the development of the return on equity of the firm, and the factors influencing it the most. We will also discuss, how the challenging macroeconomic environment is reflected in this financial measure.

Return on equity

ROE is an important measure of financial performance and it is often used to gauge the corporation’s profitability and its efficiency of generating profits. As investors, we are aiming to invest in firms, which can demonstrate that their profitability and efficiency is improving or is sustainable at a sufficiently high level.

Since 2021, the firm’s return on equity has been trending downwards, which is not what we would ideally like to see.

Using the DuPont analyses we can decompose the ROE into three components and identify the primary drivers of this decline.

ROE decomposition (investopedia.com)

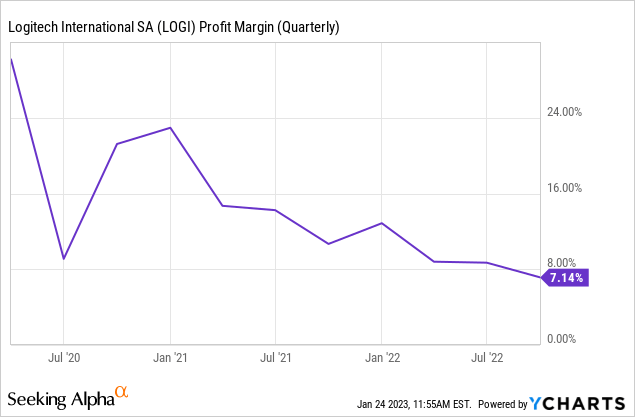

Net profit margin

Net profit margin measures how much net income or profit is generated as a percentage of revenue. Logitech’s net profit margin has been declining steadily since 2021. Over the past 24 months the ratio has declined from almost 24% to 7%, which is significant. It means that the firm is much less profitable and much less efficient in turning its sales into net income.

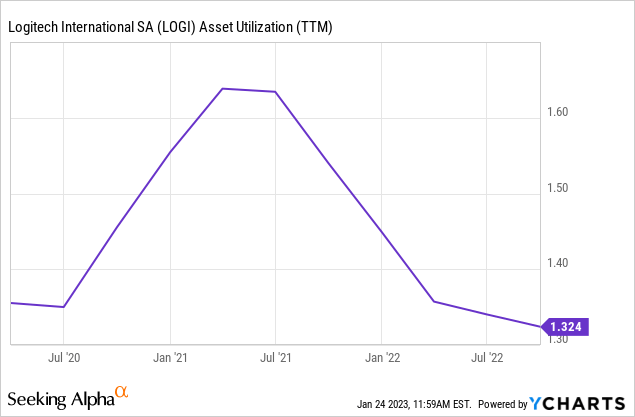

Asset turnover

The asset turnover ratio (or sometimes called asset utilisation) measures the value of a company’s sales or revenues relative to the value of its assets. It indicates, how effectively the company is using its assets to generate sales. In the case of Logitech, this ratio has been also steadily declining since 2021, which is also not appealing.

So both net profit margin and asset turnover have been declining. What could be the explanation of this from a macroeconomic point of view?

In our opinion, and as pointed out by the CEO, the challenging macroeconomic environment, including the poor consumer sentiment has the primary driver.

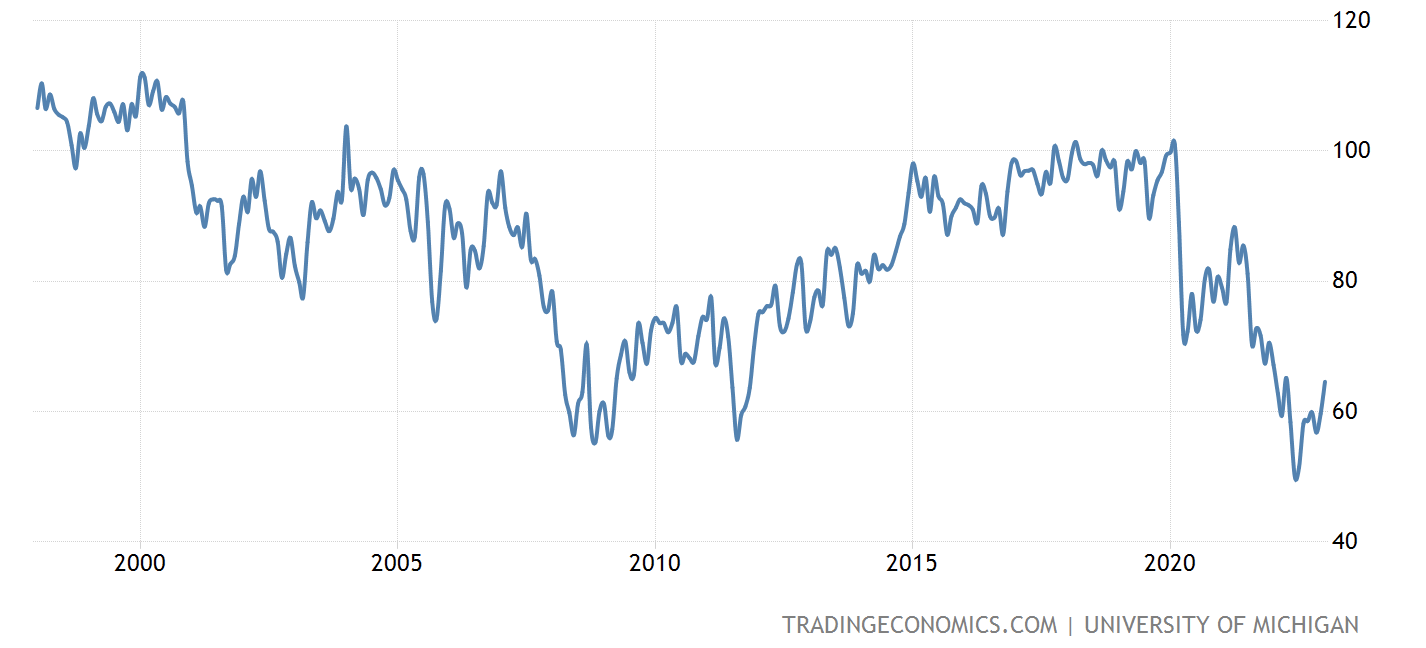

Consumer confidence is a leading economic indicator, which is often used to gauge how the consumer spending behaviour may change in the near future. Low readings indicate that the consumer is relatively pessimistic out their financial outlook and about the health of the economy as a whole. In general it leads to increased savings and lower spending on durable, non-essential goods. Logitech’s products fall into these categories. Therefore, naturally we would expect that the financial performance of the firm is significantly impacted by the poor sentiment.

Consumer confidence in the United States has been gradually decline since the start of the pandemic. Despite the recent rebound from its lows, it remains at historically low levels.

U.S. Consumer confidence (Tradingeconomics.com)

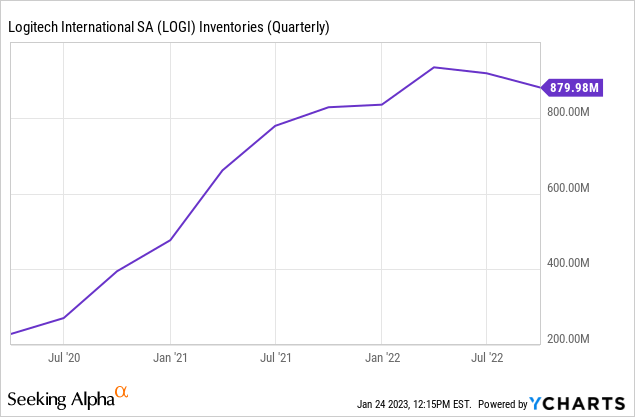

As demand is lower during periods of low consumer confidence, sales are likely to fall. At the same time, the increase of inventory levels is also usual. In order to get rid of excess or obsolete inventory firms are likely to use promotions, which in turn lead to the contraction of the margins. The below chart shows that the inventory has quadrupled in the past 3 years.

While we expect the improvement of the consumer confidence to continue, we first would like to see the inventory levels normalising and some of the financial measures improving, before we would consider investing in LOGI’s stock.

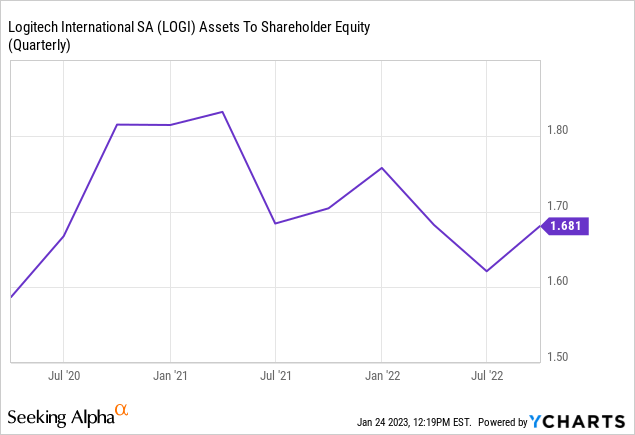

Equity multiplier

The last part of the three step decomposition of the ROE is the equity multiplier, which is simply the ratio of assets to shareholder equity. A higher ratio indicates more leverage, meaning that the firm is using a larger amount of debt to finance its assets.

So is it a good sign that this ratio has been also trending downwards lately?

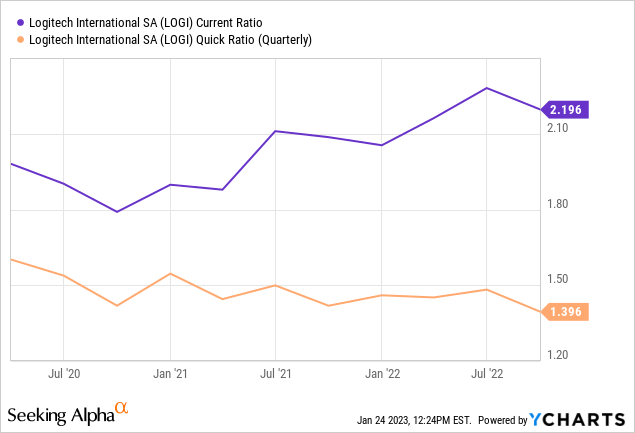

While often a lower level of debt is more appealing, we believe that Logitech may be too conservative in the use of leverage. Both of the firm’s key liquidity ratios indicate that the firm is easily able to meet its current liabilities using its current assets. Of course, better liquidity ratios could be very advantageous during times of downturns as it enables the firm to have a higher degree of financial flexibility.

For this reason, we are not particularly concerned about the decline in the equity multiplier, but we definitely would like to see the trend changing in the dynamics of the net profit margin and the asset turnover.

To sum up

The firm’s latest quarterly results were poor and they have come in below estimates, both top- and bottom line.

The return on equity of the firm has been gradually declining in the past years, primarily driven by the contracting net profit margin and the worsening asset turnover. The decline of the equity multiplier also played a minor role.

The decline of these ratios can be largely explained by the poor macroeconomic situation, leading to lower demand, lower sales, increasing inventory levels and eventually to contracting margins.

While we expect the macroeconomic environment to improve, we do not recommend buying LOGI’s stock until we do not see a change in the trend of profitability and efficiency.

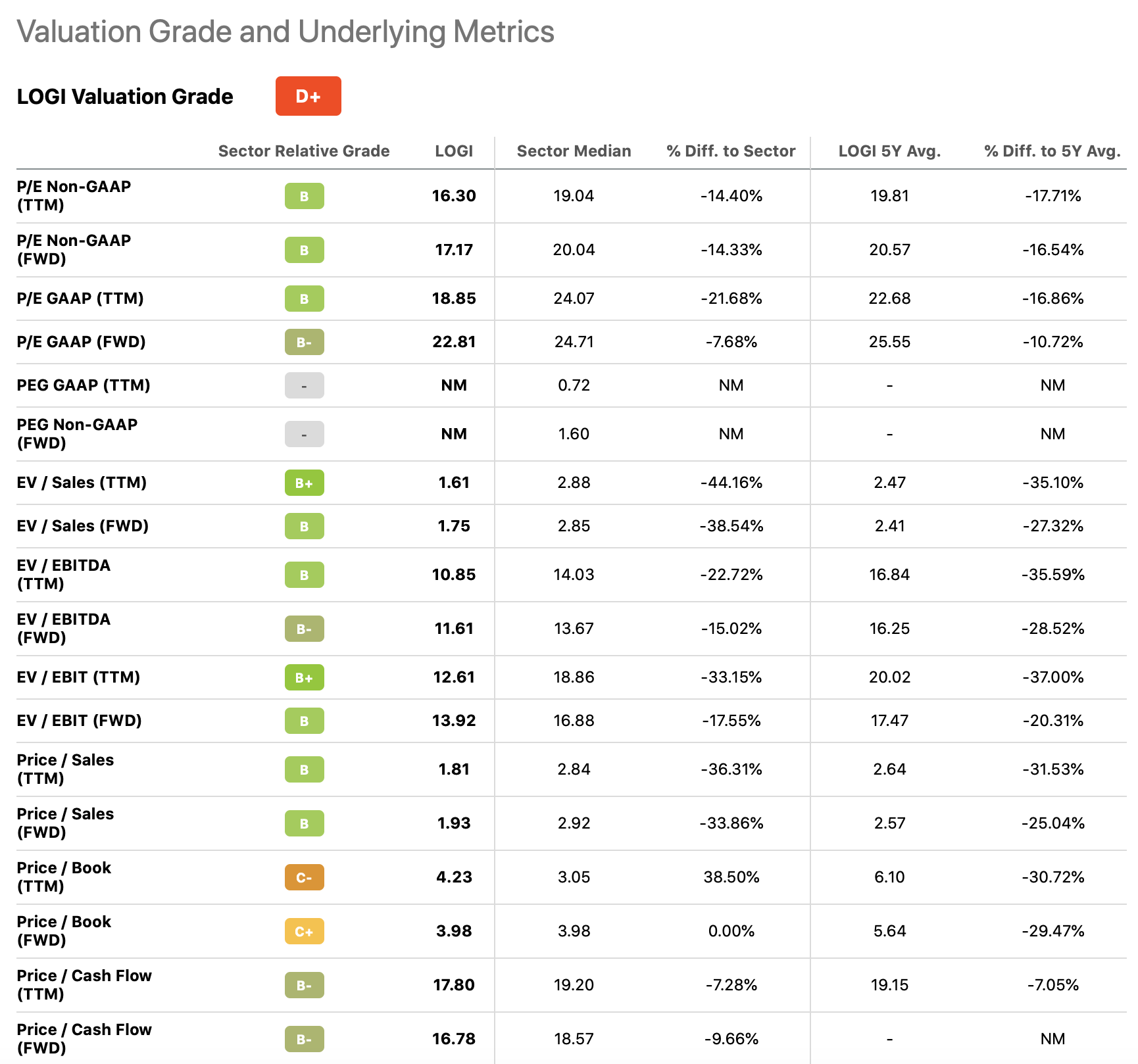

As the company is current trading at a discount compared to the sector median of the information technology sector, and also compared to the firm’s own 5Y averages, we believe that it is also not worth selling the stock.

Valuation metrics (Seeking Alpha)

For these reasons, we currently rate LOGI’s stock as “hold”.

Be the first to comment