guvendemir

Lockheed Martin (NYSE:LMT) boosted its dividend by 7.1%, which seems like a major dividend hike. In this report, I will be analyzing the hike by comparing it to the forward yield, previous dividend hikes, and the company’s cash flow generation to assess the hike.

Dividend Growth Does Not Outpace Inflation

Let’s start with the rather obvious and that is that with a quarterly dividend increase from $2.80 to $3.00, the dividend hike does not keep up pace with inflation. So, in some way, this is a hike that makes inflation hurt a bit less. I would say we live in extraordinary times and for companies, it is challenging, nearly impossible, to provide a dividend increase that at least matches inflation. Inflation is simply too high for that and at this point, many companies are dealing with labor and supply chain issues themselves putting a damper on top line growth.

The increased dividend brings the forward yield to 2.25%. If you are looking for juicy dividend yields, this might not be the most attractive name to own. Still, while interest rates are increasing, it is better to have your money invested in a dividend name such as Lockheed Martin than letting it sit in your bank account to cumulate a meager interest.

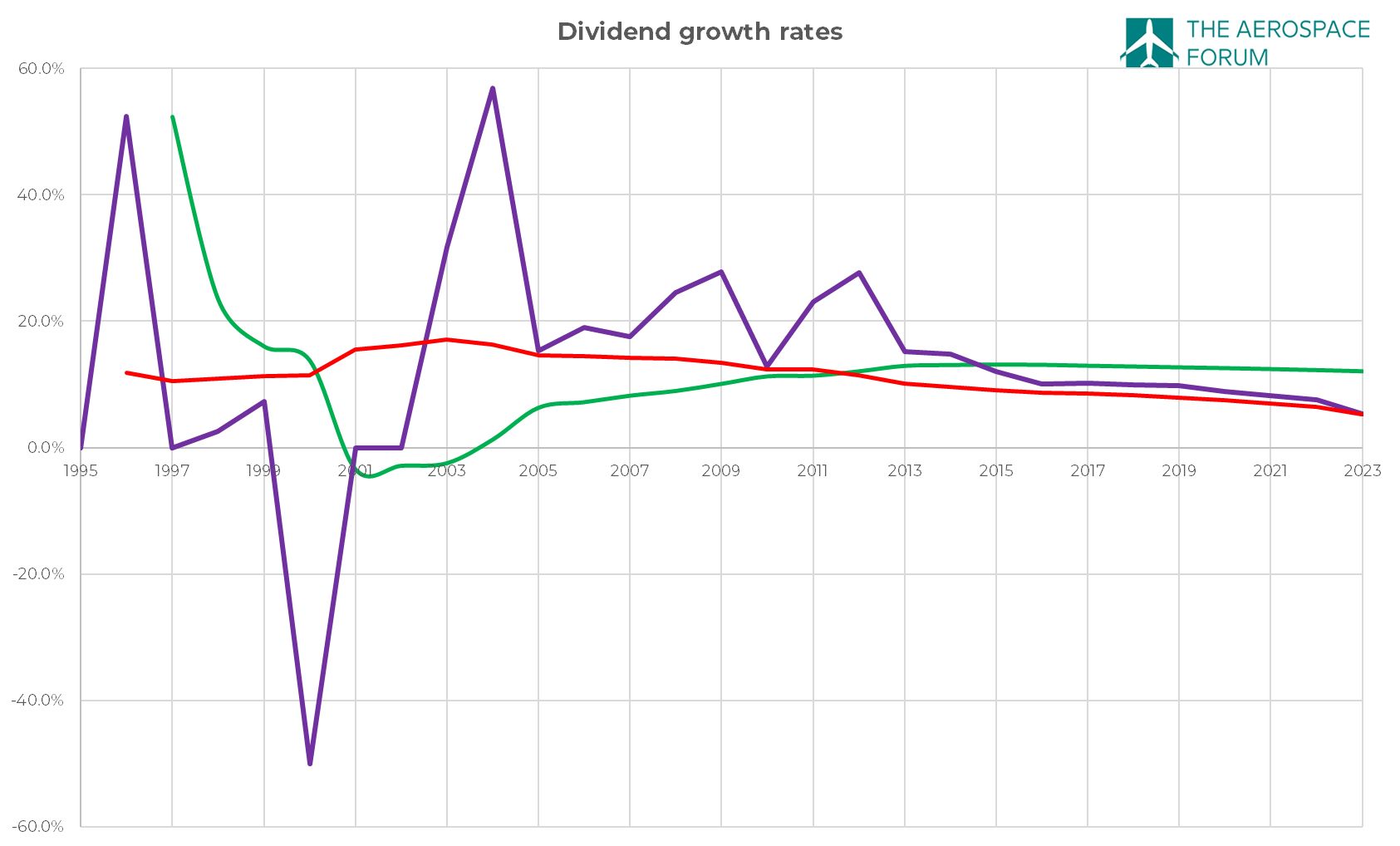

LMT Dividend Yield: Slowing Growth Story

Dividend curves Lockheed Marting (The Aerospace Forum)

While I absolutely believe that Lockheed Martin is a very nice name to own, it does seem like dividend growth is losing steam. In purple, I mapped the annual dividend hikes and what can be seen is that the hikes have been losing steam since 2012. It is not necessarily a bad thing. I believe a company should not pay a dividend that it cannot sustain or at least a growth rate it cannot sustain. What we see in the years prior to 2012 is that Lockheed Martin saw significant boosts in dividends but it also plateaued at time and even declined at one point. So, I am perfectly fine with more streamlined and modest but sustainable increases as we saw in recent years. In green, we have mapped the CAGR (compounded annual growth rate) since 1995 as a 1995-to-Year X CAGR. What becomes apparent from that is that the compounded annual growth rate is plateauing since 2013 and even is showing slight declines since 2015. So, the momentum seems to be evaporating for Lockheed Martin and that also shows in the red line which shows the CAGR but then measured from Year X to 2023. For Lockheed Martin to maintain a CAGR of 12%, it would need to hike the quarterly dividend by 18% while annual growth rates have not seen double digits growth since 2018. While Lockheed Martin has a fantastic product line up, it is facing some challenges increasing its dividends. That might also be the reason for Lockheed Martin to review its strategic plan. I don’t want to rely much on extrapolating growth rates, but with some fits Lockheed Martin’s dividend growth is set to stall by 2026. Later on in this report, I will set out my expectations for future hikes.

Share Repurchases As A Proxy To Dividend Hikes

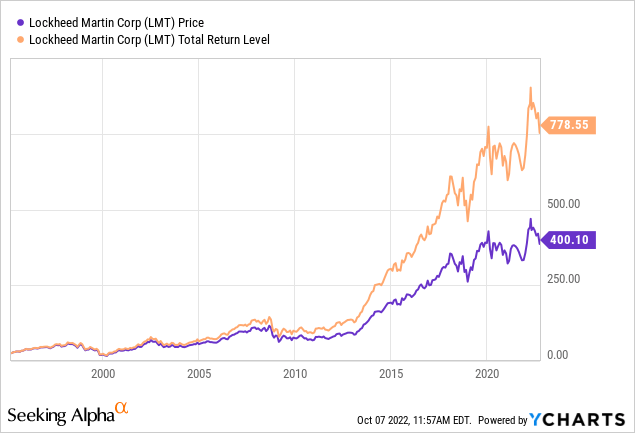

What should be noted is that things are not really bad for Lockheed Martin. Its price including dividends stands at around $400, but including dividends that are $778.55 providing a normalized growth of 14.5x and 29.2x since 1995 easily outpacing the 94% inflation since 1995. So, over the longer term things are looking good for Lockheed Martin.

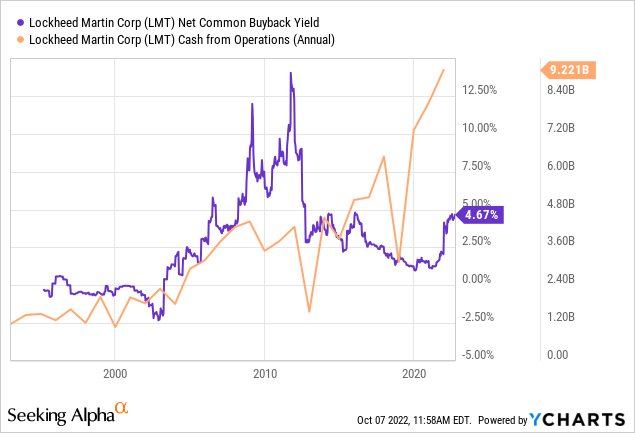

What is helping the company is that it buys back shares, which is not a substitute for dividends but can be considered somewhat of a proxy. Cash flow from operations has been growing and that is money that can be returned to shareholders minus CapEx in the form of dividends or share repurchases and a quick look at the share repurchase yield shows us that the yield has been increasing lately as does the operating cash flow. So, the dividend growth might be tapering but that is also because Lockheed Martin is committed more to repurchasing stock which subsequently allows dividend to be hiked sustainably over the longer term.

Conclusion: Dividend Growth Is Slowing, But Lockheed Martin Stock Is Still A Winner

When it comes to the dividend yield, with a yield of 2.25%, there really is nothing to get excited about. However, Lockheed Martin has a strong product portfolio and my expectations are that they will maintain an annual dividend hike of $0.80. While some trendlines would suggest that at some point dividends will plateau, I do believe that given the increased demand for defense equipment and Lockheed Martin’s positioning in the market, we will see hikes of at least $0.80 in annual dividends for the foreseeable future in addition to continued share repurchases. With a 4.67% repurchase yield and a 2.25% forward yield, I do believe that Lockheed Martin continues to be an attractive investment for long-term oriented investors who will see appreciable total returns and yield on cost.

Be the first to comment