mauro_grigollo

Introduction

In the past few months, I sold out of most of my energy stocks as I locked in some gains. I owned a bit of Exxon (XOM), Chevron (CVX), Enbridge (ENB), Crestwood Equity Partners (CEQP) and Alerian MLP ETF (AMLP). On the other side, I decided to stick and increase my position in Eni S.p.A. (NYSE:E) because of two reasons:

- It is still trading at a discounted price compared to its pre-Covid price

- Most importantly, starting next week it will implement a new dividend policy which I think will make me benefit from the current high oil price

A company with a key role in Europe

Eni S.p.A. is the Italian oil company, part of the so-called seven oil supermajors. After TotalEnergies (TTE), it is the second-largest European oil company, with a market cap of $50 billion. In the current European energy crisis, the company is playing a significant role in source diversification to disentangle Europe from its relationship with Russia.

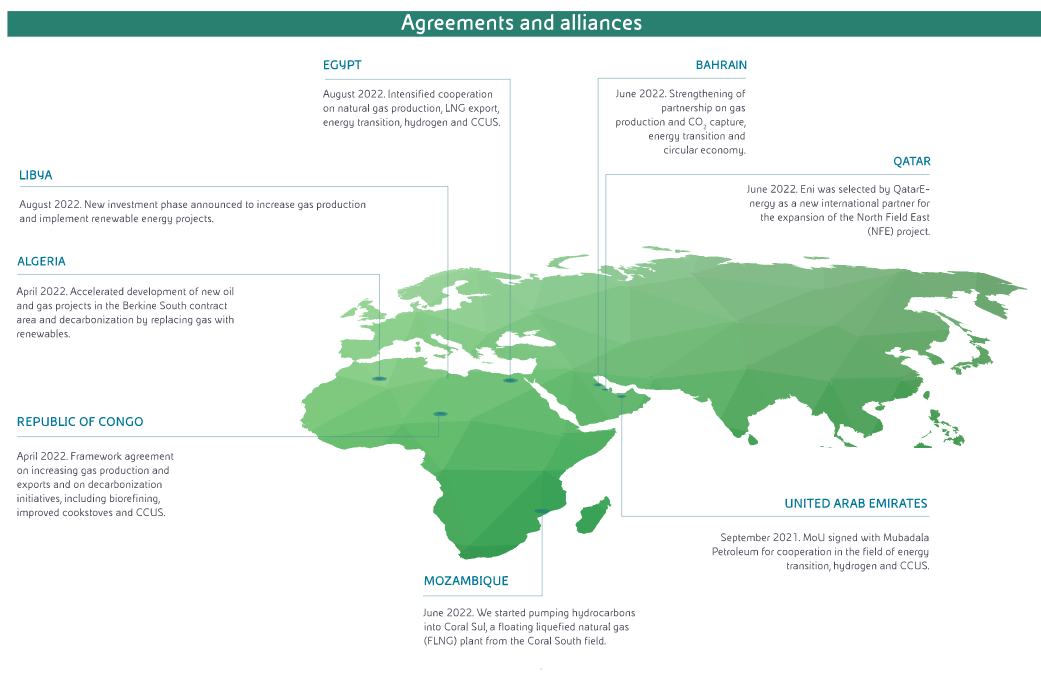

Recently, Eni strengthened its relationship with Algeria that respectively led to an increased supply of 4 billion cubic meters of gas to Italy. Furthermore, alongside other oil majors such as TotalEnergies, Eni signed a new contract to operate in the Berkine basin that led to the opportunity to exploit significant quantities of gas. In Egypt, Eni is playing a key role to help the country become a regional hub for natural gas, thanks to the Zohr field discovered by Eni in 2015, which is, so far, the largest ever gas discovery in the Mediterranean Sea. In addition, Eni is talking with Egypt about undertaking projects in solar and wind power, with up to 10GW of installed capacity over the next few years.

In June 2022, Eni also reached a partnership with QatarEnergy, which makes the Italian company as a new international partner for the expansion of the North Field East project, the world’s largest LNG project.

In the same days, Eni started pumping gas from the offshore Coral South field in Mozambique into Coral Sul, a Floating Liquefied Natural Gas facility. This is the first FLNG ever installed on the African continent in deep waters. With it, Mozambique joins the ranks of LNG-producing countries and offers further diversification.

Here is a map that shows all the other agreements signed within the last year and half by Eni.

Eni Website

To this map, we have to consider two recent news.

- Eni announced a big gas discovery at the Cronos-1 well offshore Cyprus with first estimates that indicate 2.5 trillion cubic feet of available gas, not counting further discoveries in other wells nearby.

- Just a few days ago, Eni added yet another source when it announced its acquisition of BP’s business in Algeria, which controls two major gas fields. These two fields, called “In Amenas” and “In Salah” are located in the Southern Sahara and their production of gas and associated liquids began in 2006 and 2004 respectively. In 2021, they produced approximately 11 billion cubic meters of gas, 12 million barrels of condensates and LPG.

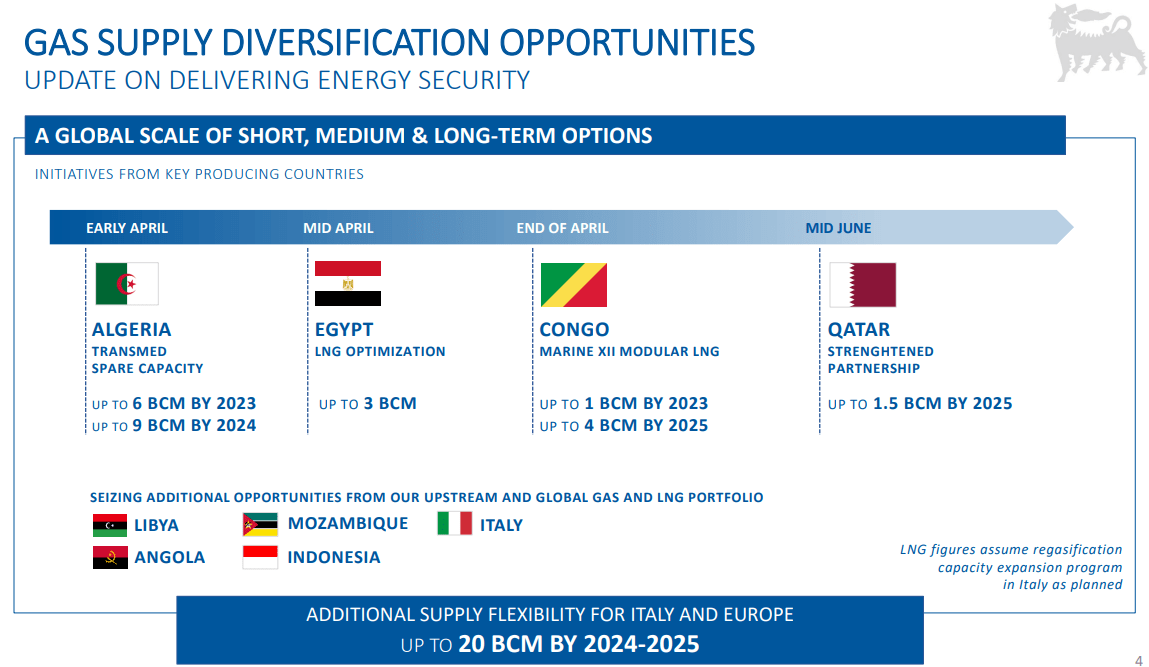

All these news make me consider Eni as a strategic play in the current geopolitical environment because it will play a key role not only in diversifying Italy’s gas sources, but it will also contribute to create a Mediterranean gas hub for Europe, as the slide below shows.

Eni 1H 2022 Results Presentation

As we can see, Algeria and Congo will both contribute starting from the upcoming late winter, which will be the most troublesome time for Europe in terms of gas supplies, as stocked gas will be low and demand still high. This makes the company confident in stating that by 2024 it will have replaced 100% of the current Russian supply.

Currently, the company is in any case able to meet all its obligation without utilizing its Russian sources, as Eni CEO Descalzi said in the last earnings call:

I want to emphasize that the company’s remaining 2022 contracted obligation can be fully met with no Russian sources without any additional costs.

Other recent news

In June, Eni said it expected to launch the IPO of Plenitude, which is the renewables division of the company. There was great interest for this IPO, but due to deteriorated market conditions, Eni decided to postpone it. Though at first disappointing for many investors, I thought the move was right because it showed two things:

- Eni doesn’t need this IPO to raise cash, showing that it is pretty confident of its balance sheet.

- With European utilities under pressure, it is better to use Eni’s strength to protect the value of Plenitude until the situation clarifies.

Since energy prices are very high, many European governments decided to tax the extra profits energy companies made. Eni, too, will be subject to a 25% windfall tax in 2022 that will cost the company €1.4 billion, instead of the expected €550 million. Even though this is a high amount, we have to keep in mind that it taxes the extra profits, meaning that the company is making, like all the oil majors, a lot of money this year, as we will see in a moment.

Financials

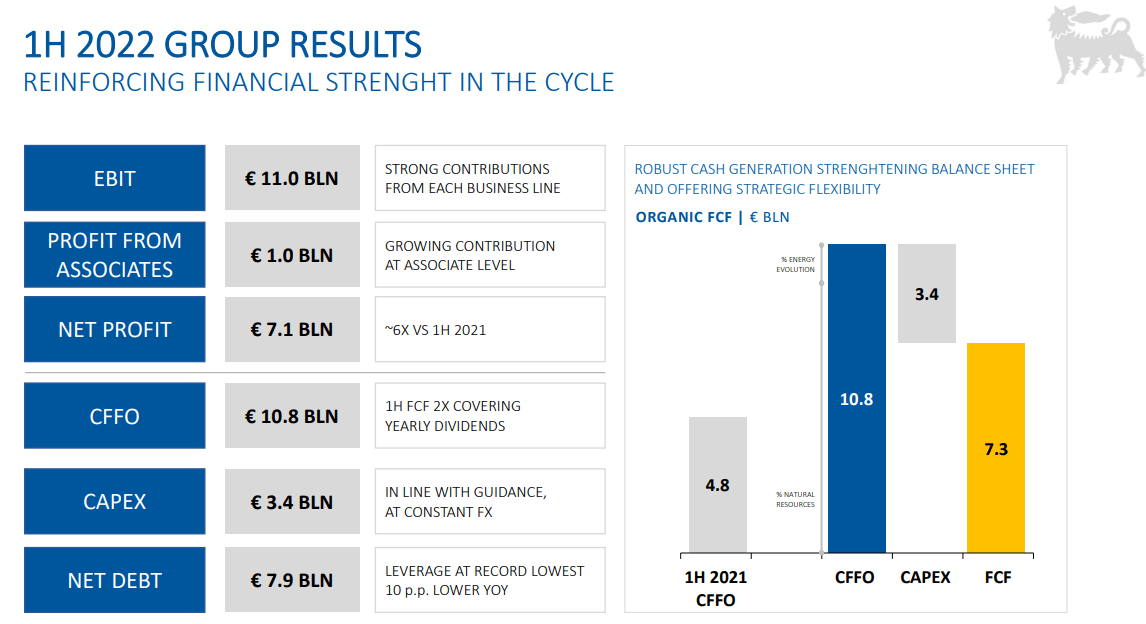

If we say that Eni is performing really well, this is no surprise given the current conditions. As summarized by the company in the slide below, we see a very strong EBIT of €11 billion and a net profit 6 times greater YoY at €7.1 billion. The cash flow from operations of €10.8 billion is already enough to cover more than twice the yearly dividends Eni will pay. This is one of the most important data that are leading me to writing this article and sharing it with the Seeking Alpha community. But we will get there in a minute.

Eni 1H 2022 Results Presentation

What is really important is that Eni, despite a huge increase in profits, is keeping its capex under control, thus taking advantage of the current situation to further deleverage its balance sheet which currently sees a TTM net debt of €16 billion which is more than covered by the €26 billion of TTM EBITDA.

Eni also improved its efficiency and brought down its cash neutrality from $45/bbl in 2018 to the current $40/bbl.

New dividend distribution policy

Now, despite high oil prices, Eni has yet to recover to its pre-covid price, unlike other peers that are close to ATH. Though Eni has been always discounted more than other oil companies, I still see the stock able to recover at least to the low $30s.

I think a support of the stock price will come from the new dividend distribution policy that Eni announced. Until this year, Eni used to pay its dividend twice a year in May and September. Starting from this September, Eni will pay a quarterly dividend in September, November, March and May, making the stock more attractive for income-seeking investors.

There are, however, two caveats. The first one is that the Italian dividend tax is 26%. The second one is that Eni’s distribution policy, as shown from the graph below, makes the dividend variable based on oil prices. However, I decided to keep Eni in my portfolio because it currently has a very high yield that I expect to continue through 2023 as oil prices are forecasted to remain high.

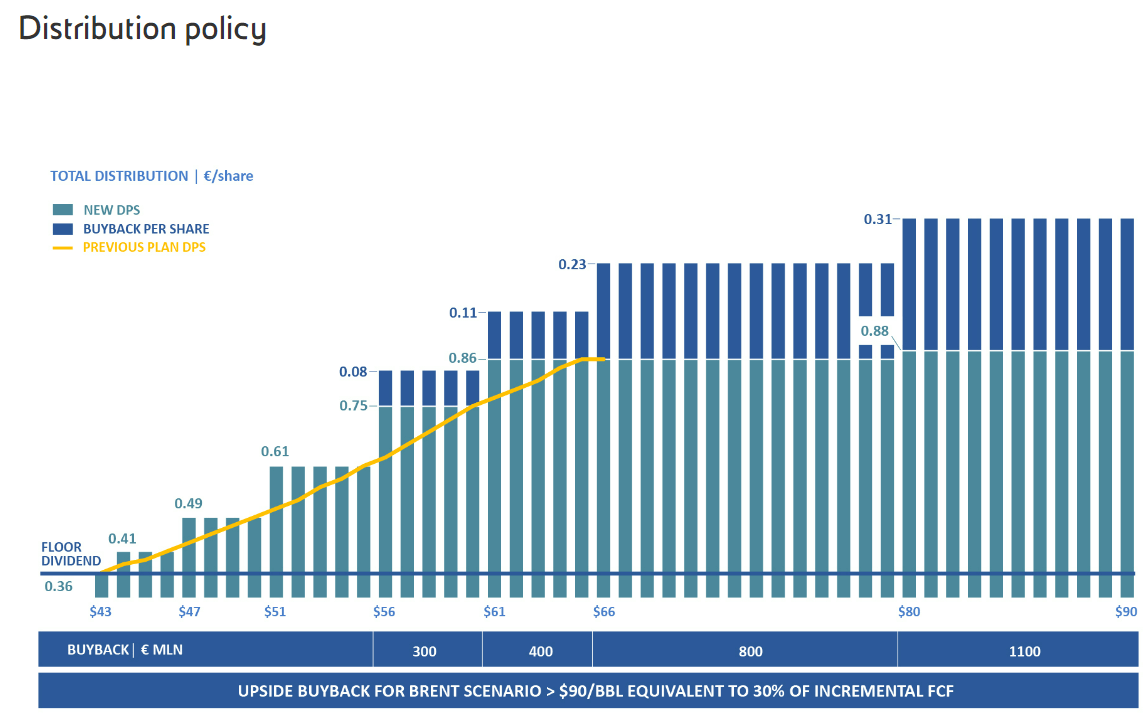

Now, let’s look at the graph and see how Eni’s dividend policy works.

Eni website

Eni’s shareholders’ remuneration policy is structured as follows. First of all, the dividend is linked to the oil price scenario assessed in July and then updated in October. To start, there is a floor annual dividend of €0.36 per share, and it will be paid as long as the Brent price is at least $43/bbl. It is very unlikely to see oil price go below this benchmark for a long period of time. The annual dividend per share then increases in the following manner:

- €0.41 per share for Brent Reference Price between $44 and $46/bbl

- €0.49 per share for Brent Reference Price between $47 and $50/bbl

- €0.61 per share for Brent Reference Price between $51 and $55/bbl

- €0.75 per share for Brent Reference Price between $56 and $60/bbl

- €0.86 per share for Brent Reference Price between $61 and $79/bbl

- €0.88 per share for Brent Reference Price between $80 and $90/bbl

Whatever the dividend amount, it will be divided by four and paid quarterly, with the first ex-date on September 19th.

In addition to the dividend, a share buyback program is triggered starting from a Brent Reference Price of $56/bbl with a value of €300 million per year. This amount rises in the following way:

- €400 million per year for Brent Reference Price between $61 and $65/bbl

- €800 million per year for Brent Reference Price between $66 and $79/bbl

- €1.1 billion euro per year for Brent Reference Price between $80 and $90/bbl

If we reach a Brent Reference Price above $90/bbl, Eni will add a further buyback equivalent to 30% of the associated incremental FCF made.

Now, we are currently under the best scenario with a dividend of and a share buyback program that has been hiked from €1.1 to €2.4 billion. The buyback is something I really like at the moment, because Eni, as said above, is not trading at a very high valuation. Regarding the NYSE shares of Eni, the annual dividend is not €0.88, but $1.80. The dividend yield of 8.30% is however the same as the shares traded in Europe.

Since the start of the buyback program, Eni purchased about 1.92% of the share capital for an aggregate amount of €821 million. This means that Eni still has €1.6 billion to deploy, which is equal to another 4% of the total market cap. Eni has stated that it will conclude its buyback by the end of Q1 2023. This leads to an expected annual total return of 12%, which kept me invested into the stock and actually buying some more shares recently as we approach the first quarterly dividend.

Conclusion

Eni for sure discounts its variable dividend policy and some country risk since it is linked to Italy and Europe. However, with a PE of 3 against a PE of 7.4 and 8.2 for XOM and CVX respectively and an fwd EV/EBITDA of 2 compared to the 4.2 and 4.8 for the two mentioned above, considering that Eni has a higher return on capital employed of 16.5% against 13.6% for XOM and 10.9% for CVX, I think the company is discounted enough to provide a margin of safety while delivering better shareholder return at least for a year and a half. This is why I rate it a buy.

Be the first to comment