krblokhin

Dear readers/followers

In this article, I’m going through my 2023 stance for Linde (NYSE:LIN), a superb industrial gas company – world-leading as a matter of fact. It’s a company with a massive market cap, a massive tradition, and a massive upside.

As I’ve mentioned before, many things about Linde are large – unfortunately, your potential returns are not likely to be among them in the near term, given the company’s premium valuation.

So here is what I’m looking at for 2023.

Linde – An update on the company operations

Linde is a market leader, and if you invest in the company, you’re investing in the world’s largest company for industrial gases. The company was originally a result of a takeover of British BOC in 2006, and again the 2018 merger of Linde and Praxair, a US company.

Praxair was initially thought to be more of a merger, but one that turned out more towards the takeover direction, confirmed not only by soft trends, but by terms of disposals, which leave it with much of Praxair’s original operations, and less of Linde’s.

Linde produces a wide variety of industrial gases, almost all of them purely at their own locations, and sold at bulk-like qualities (called merchant business) or cylinders to a massive variety of different end uses and industries. The operations bear similarities to things like the cement industry, in that Linde goes where the operations and the customers are – because it builds plants at client locations as well, though too much less of an extent compared to something like concrete/aggregate.

Gases are after all much more transportable than cement. The company also operates its own air separation plants, meaning that Linde does not rely on third-party to provide it with products. The company has an impressive degree of vertical integration.

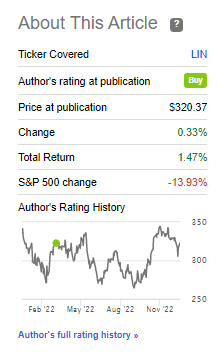

Now, I haven’t written about Linde in a few months – but investing in Linde as of my article when I had a bullish rating on the company would have saved you from losses in the terrible stock market year of 2022.

Linde Article (Seeking Alpha)

Unfortunately, Linde is not cheap. It wasn’t back at the time, and it certainly isn’t today. But Linde is one of the safest investments you can make in the space – even with Russia issues on the block here. There are plenty of people, many contributors, calling Linde a “Buy” here.

But I am not one of them – not here, and not at this price.

Revenues for the company are somewhat split. They show us a 35% cylinder gas split, 25% merchant, and 22% on-site, with the remaining sales revenue generated from its engineering operations.

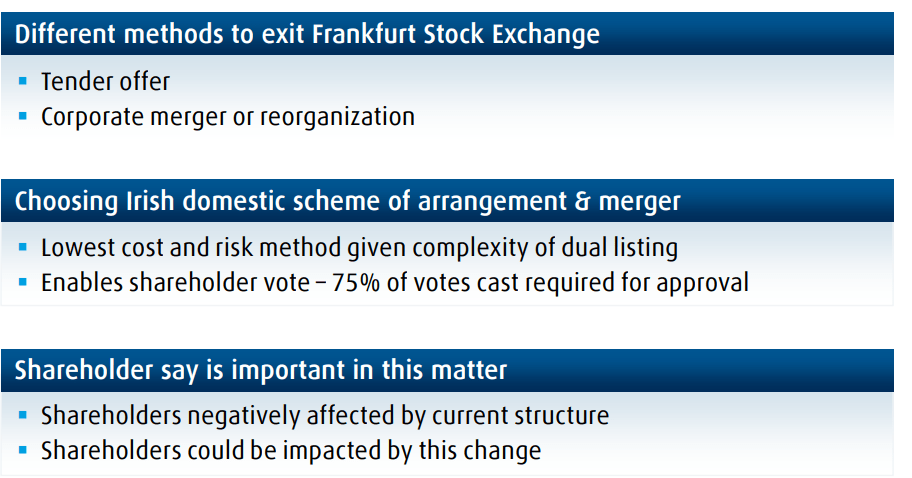

Now, the company also has a very unique share structure – because it has two native listings, one on NYSE and one on Frankfurt, which means that the company has two different regulators and works under 2 different accounting methods with a separate set of shares. This is not effective and is something that the company has been addressing.

Linde’s solution to this problem, back at the end of October, is to fully de-list from Frankfurt.

Linde IR (Linde IR)

We’re in the middle of this at this time, and will see what happens when March approaches, but the company expects this process to take around 100-130 days.

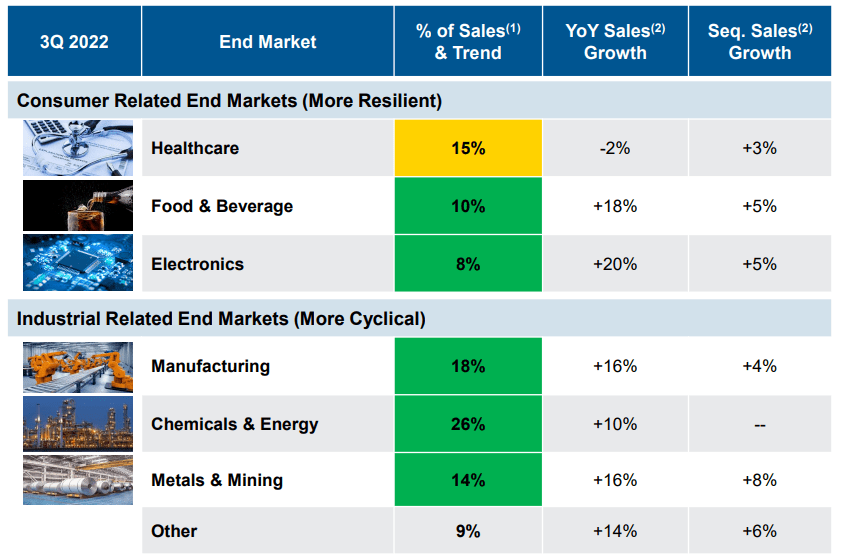

Aside from this, we also have 3Q22 to help us decide if the current price is anything worth justifying for Linde. The company is in a very diverse set of end markets – with more resilient consumer markets and more cyclical industrial markets. Aside from health care, everything is really showing very good growth.

Linde IR (Linde IR)

As with some of my other energy-related articles, Linde also sees impacts from the US inflation reduction act, which is expected to accelerate the U.S clean energy transition. The company sees this as an investment opportunity upwards of $30B, with a mix of blue hydrogen, hydrogen storage, oxygen, Co2 Capture, Nitrogen, and other areas from a mix of decarbonizing the company itself, decarbonizing Linde’s customers, and potential new markets such as electrolyzer. I recently wrote about the world’s biggest manufacturer of electrolyzers and why I’m somewhat dubious of them. One of the reasons was the fact that Linde, or some company like it with better scale and economic possibilities, might simply scale up and “take” their spot in the value chain.

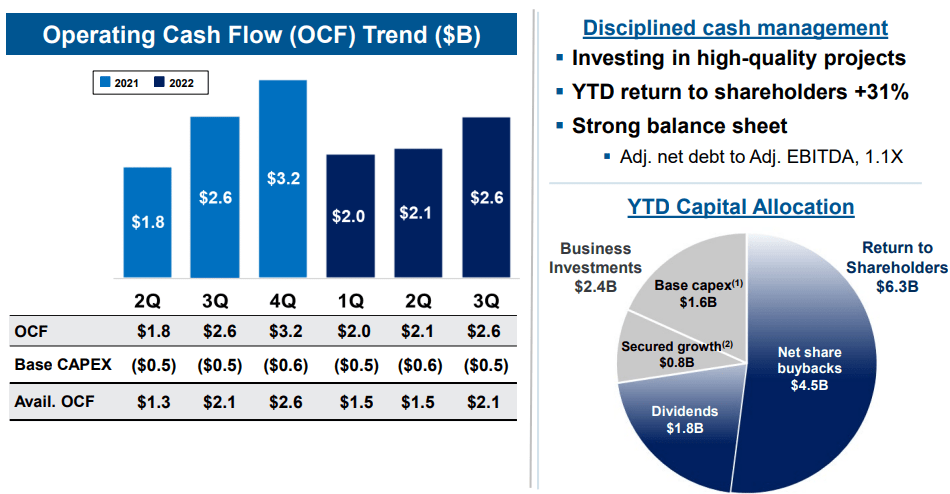

Linde’s 3Q22 results were solid, with a significant operating margin of upwards of 22-23% and a diluted EPS above 2021, a YoY growth in the double digits at 14% – which is impressive.

The sales and profit growth in the company was impressive because Linde was able to push pricing to offset any cost increases seen. Margins were up YoY, and the company’s divestiture of legacy Russian businesses is more or less done. Company OCF isn’t as high as in 2021 except for 1Q22, but it’s still damn solid results, with a very appealing mix of use of capital, buying back shares, dividends, and CAPEX/growth.

Linde IR (Linde IR)

The company also provided us with FY22 forecasts, which are calling for EPS increases upwards of a limit of $12.03, marking a 12-13% increase YoY to 2021, and including a negative FX impact of 5%. This forecast also assumes no economic growth, and marks a raise from the previous forecast, despite current macro uncertainties.

A business like Linde is stable for a couple of reasons, but one of the main ones is predictability. It’s stable over time, and the geographic scope of its overall operations protects it from potential volatility in any one given geography.

It’s hard to consider what could get a company like Linde to experience a downturn. With the company’s incredibly diverse set of end markets, its moat and market leadership, its history and fundamentals, and the way the world is moving, I do not see any one thing that could fundamentally destabilize Linde. Its operations are so spread-out that even natural catastrophes could only impact parts of the company. This is one of the safest investments you can make – but it also won’t really make you rich. It’s not going to provide you with massive amounts of returns unless you buy it incredibly cheaply.

And Linde is not incredibly cheap today. It was not even cheap.

Let’s look at that valuation.

Linde’s Valuation

This remains the major problem not only for Linde but most quality companies. They trade at almost unbelievable premiums to any humane sort of valuation level.

Given their forecastability, and that you can “know” that you’re not going to make more than X% returns here, it requires you to accept a cap on what sort of gains you can have.

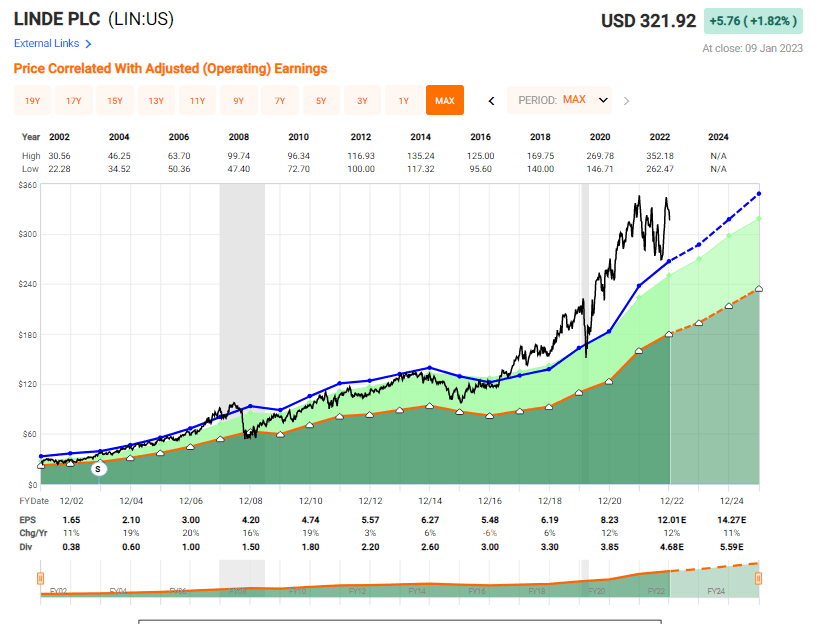

What’s more, and what I want to show you, is exactly how lined has been premiumized over the past 4-5 years.

Linde Valuation (FAST Graphs)

As you can see, the company has actually been fairly cheap for most of the period from 2022. Over 70% of the time, you could not only buy the company below 20x, but you could also “Buy” it close to 18x. Instead, today, it’s almost at 18x, making it one of the more expensive basic materials companies I have the honor of covering.

Yeah, it’s A-rated, but it also has a non-impressive yield of sub-2%. What’s more than that, growth is unlikely to be any sort of impressive here. If we forecast Linde at a 22-24x P/E, the 2025E unimpressive annualized RoR might be as low as 4%, or 14% in 3 years, which is a lot worse than inflation could deliver to you. The company’s EPS, even with growth, would require you to look at premiumized upsides of upwards of 28-30x P/E, to see some really impressive growth rates.

And I don’t consider any basic materials company, even the best ones, worth 28-30x P/E. This company’s valuation has taken outsized turns, and it’s bound to come down sooner or later. We can already see some of the indications of this volatility given how the company is bouncing. Today it’s close to 27x P/E, but it was closer to 23x not that long ago.

Quality is never the problem with Linde. In terms of peers, we have Air Liquide, Air Products (APD), DSM, and Clariant (OTCPK:CLZNY). These businesses have average P/E-valuations of around 20-25X on average. Linde tends to be at those valuations or higher.

I am not arguing that Linde doesn’t deserve some premium. The market believes in and applies a massive premium to this company’s valuation, likely relating to its vertical integration, engineering segment, and history as well as scale. I apply a 30-40% premium range to Linde’s P/E to reflect these qualities, which Clariant and Air products cannot really measure up to.

Other chemical companies offer more – but have closer ties to energy and higher volatility. I recently wrote about Covestro (OTCPK:COVTY), a company I own more in and one that has outperformed quite a bit more as well. I prefer buying it cheaper, even if I have to wait for it.

I would consider Linde a “BUY” below $290/share, but not above it. On those rare times when Linde gets cheap, such as during COVID, the right move is to put massive amounts of capital to work to ensure results well within triple digits. If you bought the company at 20X P/E back in 2020, your return would be close to 45% annually.

That’s what you can expect out of a cheap Linde, and given the safety it offers, it should be on everyone’s list. But until we’re at that level again, this is not a common stock investment I would view in a favorable light.

For the US ticker, analysts following the company go full premium when it comes to Linde. 22 analysts follow the stock, and 14 of them rate it as a “Buy” with a target beginning at $260 and going up to $400/share. I can get behind the $260-$290, but not above that. The current analyst average is $357/share.

I want things cheaper and stick to my PT of $290/share for NYSE – but that’s as high as I am willing to go at this point.

Here is my current thesis for Linde.

Thesis for the Common Share

- Linde is without a doubt one of the safest and most conservative basic materials companies out there. But the business comes at a massive premium that I don’t view as defensible to any extent at this time. While in a market-leading position, the only way to get good outperformance, as I view it, is by buying the company far cheaper.

- Linde is currently valued above $320/share with a P/E of 27x. I would say it’s worth around $290 at most, in order to get the return you want. We may see this valuation in the near term.

- For this reason, I rate Linde a “HOLD” here, and would stay careful about them going into 2023.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion

Thesis for the Options

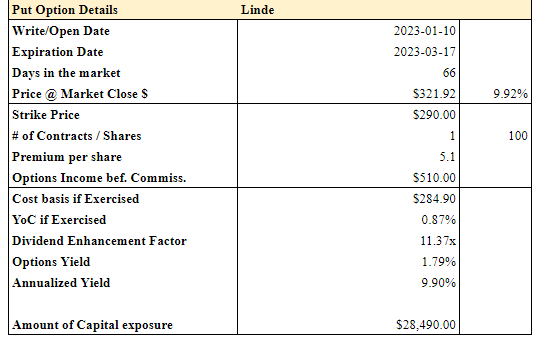

Linde’s options are not easy, due to the high valuation of the company. Even if you managed to score some attractive RoR, chances are you would not be doing so at an attractive strike price. If you own 100 shares of Linde you could check covered calls here, but here is the Put I could find that would put you at an acceptable entry point.

Linde Put Option (Author’s Data)

That’s live options data from today. Not a terrible option, but plenty of capital outlay for a 9.9% annualized ROR, with a $284 entry which is acceptable, but with a very high risk of assignment. I would be careful with this one, and probably wouldn’t write it – but it exists.

Be the first to comment