Andrzej Rostek/iStock via Getty Images

Lincoln Electric Holdings, Inc. (NASDAQ:LECO) is coming off a solid third quarter, led by Automation and Energy, with overall total organic sales in the company up 21 percent year-over-year.

Automotive/Transportation revenue soared 40 percent, while Energy revenue jumped by 20 percent. Heavy industry contributed approximately 15 percent to revenue growth and General Industries and Construction added another low double-digit percent in revenue growth in the third quarter.

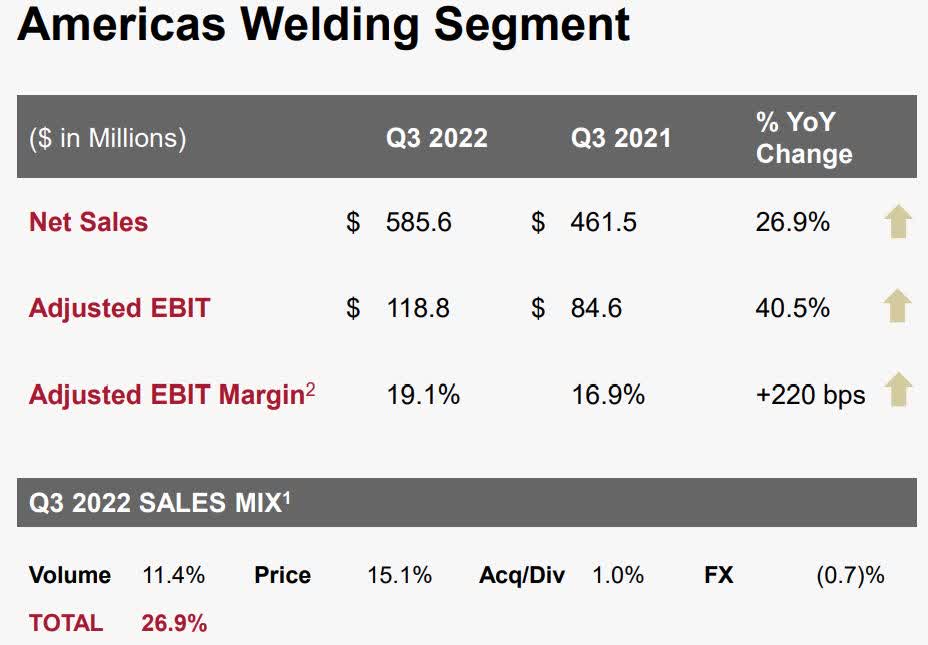

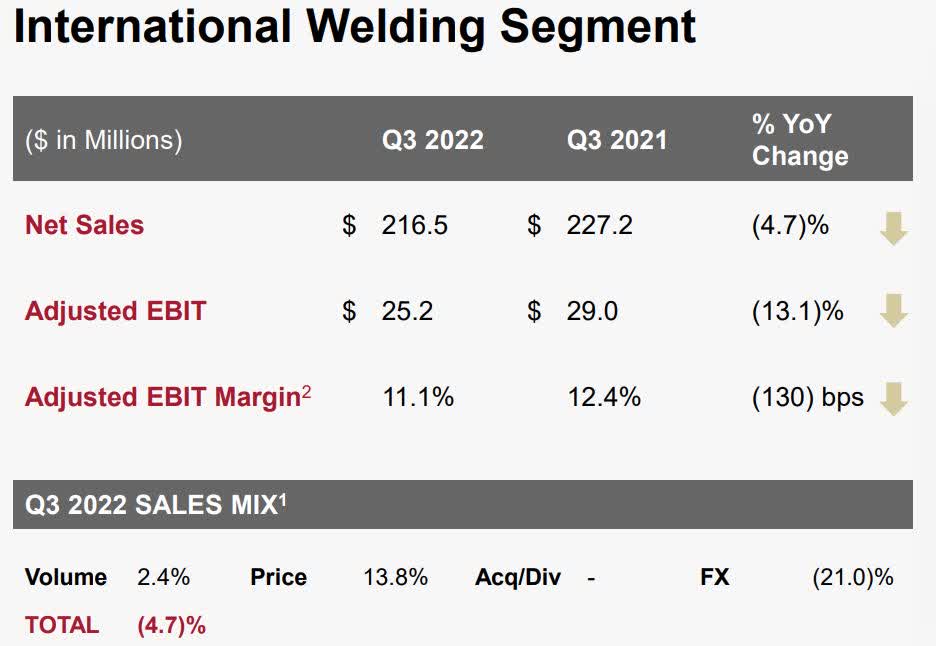

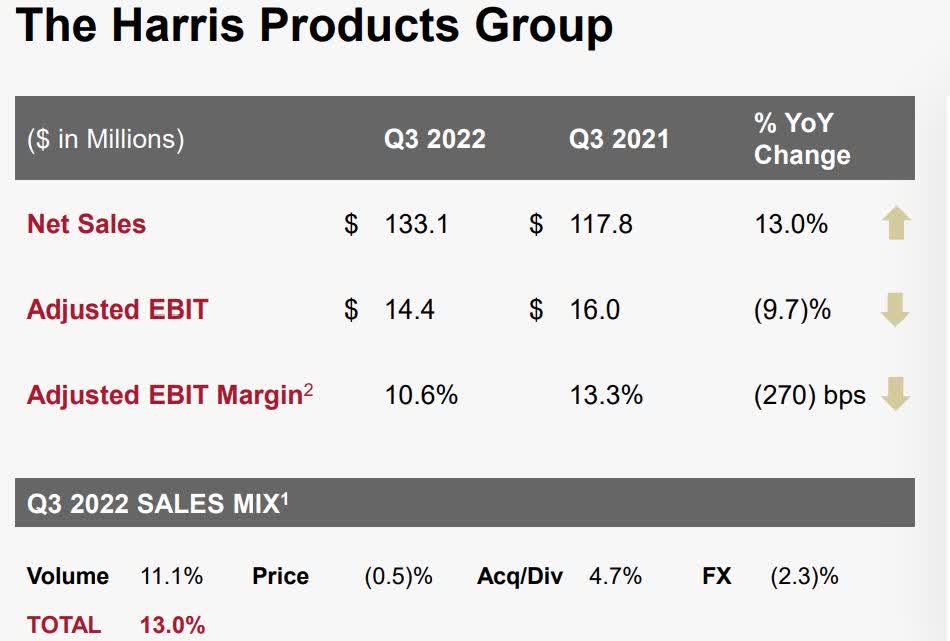

Revenue sales from its Americas Welding segment was up 26.9 percent year-over-year, International Welding revenue was down (4.7) percent, and Harris Products Group revenue increased 13 percent from the prior year in the same quarter.

In this article we’ll look at some of LECO’s latest numbers, and how Automotive and Energy should continue to drive growth going forward.

Some of its latest numbers

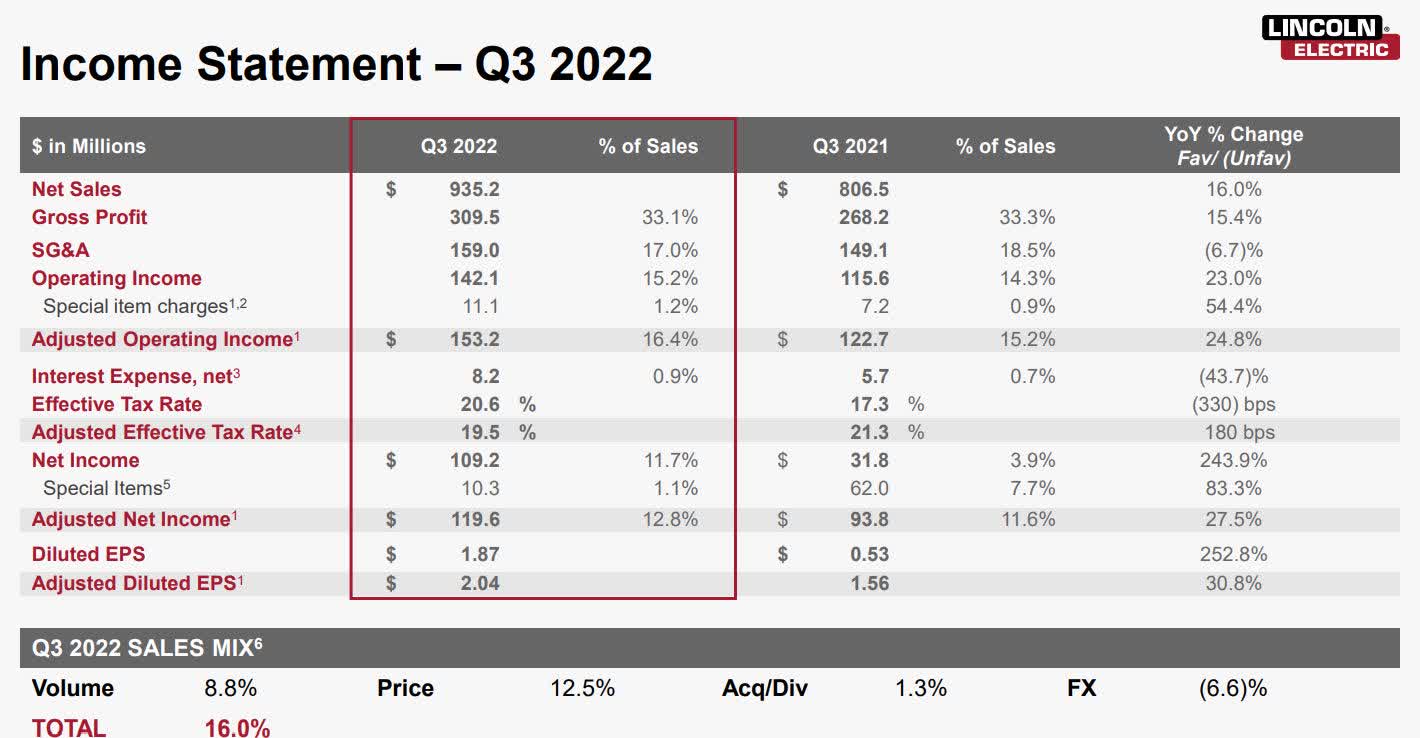

Revenue in the third quarter of 2022 was $935.2 million, compared to revenue of $806.5 million in the third quarter of 2021. Revenue for the first nine months of 2022 was $2.8 billion, compared to revenue of $2.4 billion in the first nine months of 2021.

On a quarterly basis, the good news to me for revenue was 12.5 percent of it was related to price increases and about 9 percent was from higher volumes. Approximately 1.3 percent in revenue for the third quarter of 2022 came from acquisitions.

Investor Presentation

I consider this a positive because of pricing power and demand. That was a strong tailwind in Americas Welding, with sales up 26.9 percent, adjusted EBIT up 40.5 percent, and adjusted EBIT margin at 19.1 percent, up 220 basis points. Price in the segment accounted for 15.1 percent of the revenue total, while volume accounted for the remaining 11.4 percent.

Investor Presentation

In its International Welding segment revenue was $216.5 million, down (4.7) percent year-over-year. Adjusted EBIT was $25.2 million, down (13.1) percent from adjusted EBIT of $29 million in the third quarter of 2021. Adjusted EBIT margin was 11.1 percent, down (130) basis points from the third quarter of 2021. Lower margin came from product mix and timing of pricing actions taken or not taken.

Investor Presentation

For Harris Products Group revenue in the third quarter of 2022 was $133.1 million, up 13 percent year-over-year. Adjusted EBIT in the reporting period was 14.4 percent, down (9.7) percent year-over-year. Adjusted EBIT margin was 10.6 percent, down (270) basis points year-over-year. Lower margin in the segment came from a decrease in operating leverage and lower prices in specific metal offerings.

Investor Presentation

In listing these numbers, I wanted to show the importance of Automotive and Energy continuing to perform well to support future revenue and earnings growth. If either of them stumbles, it would put significant downward pressure on the performance of LECO.

Automotive and Energy

While all end market sectors were up in the quarter, the company particularly pointed out the sustainability of growth in automotive and energy.

Management pointed out the fact the company is benefiting from the increased investment activity in energy in the Americas and globally. Investment has been pouring into energy in the Americas based upon the need to expand production activity and capacity, or to launch greenfield projects.

One of the areas in energy specifically called out by management was in regard to wind turbine fabrication, where its proprietary solutions are resulting in capturing share in the trending sector.

In Automotive it also pointed to the opportunity in the manufacturing of EV battery trays. Both the Automotive and Energy segments offer a number of similar opportunities in a wide variety of categories that the company sees continuing to trend for a significant length of time.

I agree with that assessment, and believe that how Automotive and Energy goes, so will go the company, as together they accounted for approximately 60 percent of revenue growth in the third quarter, and together they should continue to be the main catalysts of revenue growth on a consistent basis.

That said, the performance from quarter to quarter could be lumpy because of ongoing weakness in industrials, construction and infrastructure, which will probably perform unevenly over the next year or so, until we get a clearer picture on the state of the economy.

Other uncertainties in the quarters ahead are how China and Europe do in regard to demand and how the two giant economies will do if the macro-economic environment worsens in 2023. The other side of the coin is if they do better than expected, it could be a possible strong tailwind in the year ahead.

Conclusion

The last quarter was a mixed bag for LECO, as Automotive and Energy drove revenue, while industrials, construction and infrastructure weighed on its performance, as did Harris Products Group and International Welding. How much inflation and product mix will continue to have an impact on EBIT and EBIT margin in the quarters ahead will determine the health of its bottom line in 2023.

The other major positive I saw in the reporting period was that organic sales as a whole were up 21 percent year-over-year. Not relying solely on acquisitions for growth is a strength for the company because of the impact it has on the bottom line in times where margins can get squeezed in certain segments of the market, as they did in the third quarter.

As mentioned earlier in the article, organic growth not only came from increasing prices, but also an increase in volume, which means demand was a key driver in sales in the quarter, and not having to lower costs in order to stimulate sales over the entire portfolio of the company.

Over the next year I see Automotive and Energy being the two main growth catalysts for the company, and if the two segments can maintain growth momentum, they should support the bottom line while incrementally adding to the top line.

Since my primary focus in this article was the organic growth strength of the company, I didn’t want to focus on its acquisition of Fori. One thing to keep in mind there is management says it should add another $225 million to Automation, which would bring the total annual revenue in that segment to $850 million. If it is able to maintain margins while adding that revenue, it could be a nice tailwind for LECO in 2023.

Be the first to comment