Michael Vi

The current tough macroeconomic backdrop makes analyzing most equities very difficult. In the case of LendingClub (NYSE:LC), the fintech faces a hiccup in investor demand due to the rapidly rising interest rate environment impacting financing costs. My investment thesis remains ultra Bullish on the stock trading below $10 due to the normalized earnings power of the company.

Streamline Operations

As with other companies in the tech and fintech sectors, LendingClub is using the current tough economic environment to reduce costs. The fintech just announced a 14% reduction in their workforce.

The company will eliminate anywhere from $25 to $30 million in annual run-rate costs. LendingClub will take a pre-tax charge of $5.7 million to enact this employee reduction.

The biggest reason for the job cuts is that loan originations only came in at $2.5 billion in Q4. The fintech had originated $3.5 billion worth of loans in Q3’22 and even produced $3.1 billion worth of loan originations back in Q3’21.

Source: LendingClub Q3’22 presentation

LendingClub was still growing originations 14% YoY during the September quarter, but the company increased the amount loans retained for investment by 81% in the quarter to $1.15 billion. The fintech exceeded their expected range of retained loans reaching a level of 33%

The management team set a goal of retaining up to 25% of originated loans on a quarterly basis. The problem is the reduction in marketplace demand highlighted back in the previous research following Q2 with the CEO further addressing the problem in the Q3’22 earnings release as follows:

As we anticipated, marketplace volumes were impacted by higher funding costs for certain loan investors, driven by rapidly increasing interest rates. Over time, as rates stabilize and we continue to reprice personal loans, we expect this impact to gradually moderate. Our digital bank and other strategic advantages position us to continue to effectively navigate the evolving economy and to capitalize on attractive growth opportunities as they emerge.”

The business is vastly improved following the model shift towards holding high-yielding consumer loans due to this constant issue with marketplace investors pulling back on investing in loans during economic uncertainty. The fintech now holds $5+ billion in loans held for investment.

LendingClub originally guided to Q4’22 revenues of $255 to $265 million with net income from $15 to $25 million. The updated guidance has revenues of $260 to $265 million versus analyst consensus of $261 million with net income from $21 to $24 million.

The holiday quarter is historically a weaker quarter, so LendingClub generally hit Q4 guidance. The weak originations will feed into lower revenues in early 2023. The fintech will cut $6+ million in quarterly operating expenses going forward to help boost profits in a difficult period.

Boon Ahead

LendingClub has a business focused on refinancing higher interest credit card debt for members. As CEO Scott Sanborn mentioned multiple times on the Q3’22 earnings call, the company benefits from this higher rate environment once the Fed stops rate hikes:

Most notably, record high credit card balances at record high interest rates should be a boon to our core refinance business.

First half, we’ll be continuing with the elevated rate environment and back half, as we mentioned, we’re going to — credit card rates are at a record high. Credit card balances are back near their record highs, and rates have not finished moving, we are going to have a very, very large TAM in a very compelling offer. And the investor dynamics, with the rate — the terminal rate curve continues on the downward flow.

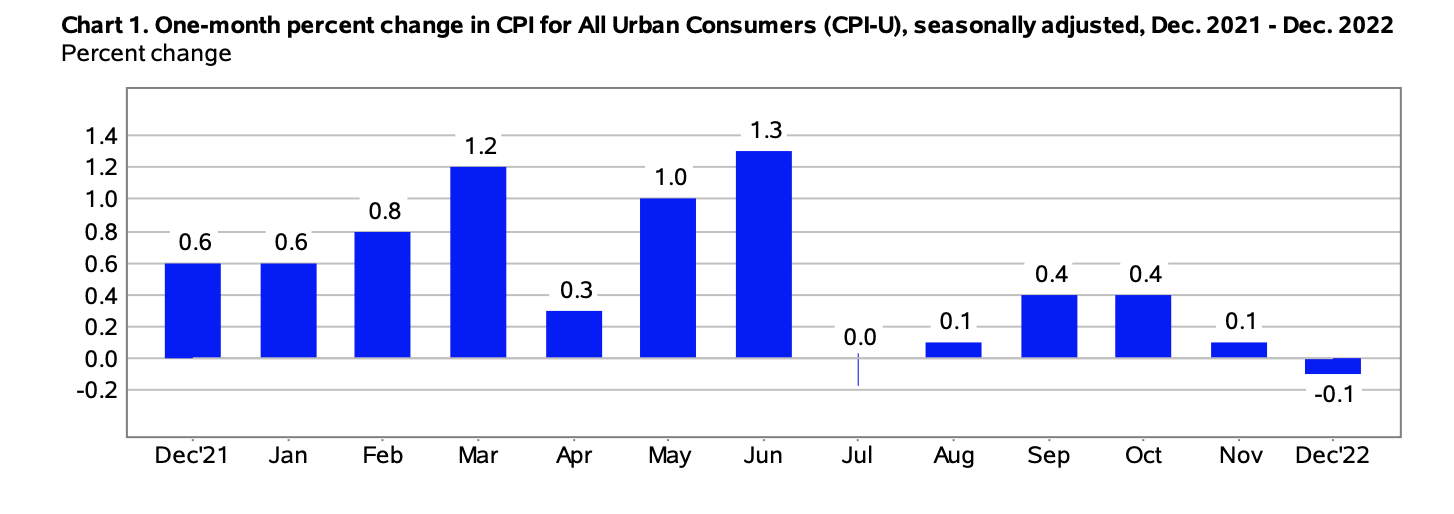

The CPI data this week supports a scenario where the Fed is close to ending rate hikes. The MoM consumer headline inflation was actually negative for December and has trended into the Fed range of 2% inflation over the last 6 months.

Source: BLS

As bank funding costs stabilize or even start to decline, the loan originations will rebound to prior levels. Marketplace revenues will rebound in 2023.

LendingClub has a market cap of just $1 billion, yet the bank is still targeting $290 million in net income for 2022. The fintech is still in the early innings for building their digital bank platform providing years of growth ahead, yet the company is set to earn $1.60+ per share in 2022 with the stock trading at ~6x EPS targets.

Naturally, the biggest risk ahead is higher credit losses. The LendingClub loan portfolio only saw 30+ day delinquencies below 2%. The company has taken credit losses in the 7% range for the personal loan portfolio during 2022. Any higher credit losses would definitely squeeze the profit profile of the lending business and could harm the ability of the fintech to attract more marketplace investors going forward.

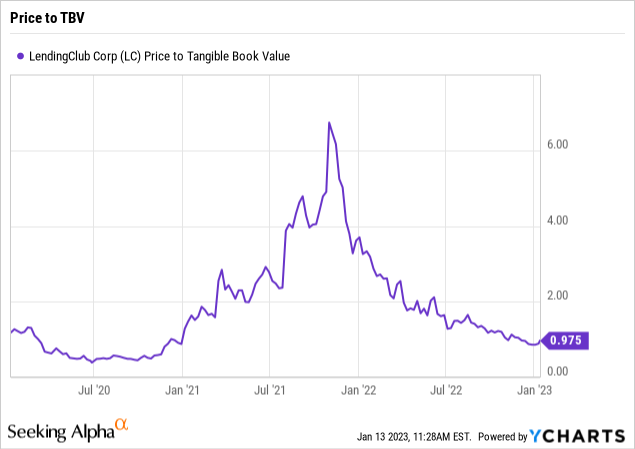

While 2023 could be a tough year, LendingClub ended Q3’22 with a tangible book value of $9.78 per share. The bank boosted TBV from just $7.08 last year due to the massive income generated during 2022.

Hence, the stock has risen from COVID lows, but the P/TBV remains at a similar level below 1x while LendingClub faces far less risk to the business model with the strong digital bank with $5 billion in deposits to fund loans. The stock probably shouldn’t have traded above 5x TBV at the peak, but a valuation multiple in the middle of this range appears logical.

Takeaway

The key investor takeaway is that LendingClub shouldn’t be trading slightly below TBV with the earnings potential ahead for the fintech. Investors should continue to use weakness to Buy the stock at an attractive price.

Be the first to comment