Michael Vi

Yesterday, after the market close, LendingClub Corporation (NYSE:LC) issued a press release announcing its plan to streamline its operations. This includes a reduction of its workforce by 14%. The rationale for the announcement was provided below:

…a cost reduction and reorganization plan to align its operations to reduced marketplace revenue following the Federal Reserve’s historic pace of interest rate increases.

The company also released preliminary results for Q4 2022 and scheduled the full earnings release and conference call for the 25th of January after the market close.

There is much to unpack and for investors to digest. I will endeavor to provide insights as to the impact and what this all means for investors.

The Q4 Earnings

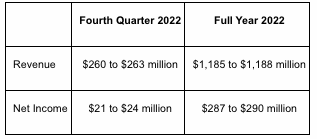

The preliminary results are shown below:

LC Investor Relations

On the face of it, the 4th quarter revenue is in the middle range of guidance ($255 to $265 million) provided in the Q3 earnings call, whereas the net income is in the high range of guidance ($15 to $25 million). Originations were also on the lights side (at $2.5 billion only) compared to $3.5 billion the previous quarter.

However, there were also a number of adjustments and one-off items to consider including:

- – the acquisition of the $1.05 billion MUFG portfolio that closed on the 2nd of December 2022. As such, LC benefited from almost one month of interest (my estimate is an incremental pre-tax income of ~8m), but there would have been some transaction costs involved as well.

- – restructuring cost of $4.4 million in Q4 relating to the cost-cutting.

If I adjust for these, it looks like LC’s earnings would have come at the lower end of revenue and net income guidance. Given that LC typically sandbags earnings guidance, this suggests to me that LC is facing stronger-than-expected headwinds when it comes to its marketplace revenue.

To recap, as I highlighted in my previous article, investors’ appetite for unsecured lending is waning for two reasons. Firstly, the rapidly higher interest rates are changing the economics and return investors are able to generate from the asset class, given that funding costs change immediately as the Fed raises rates (for some investors) whereas the increase in yield of the loans reprices with a significant lag.

The second reason is the fear of a looming Fed-induced recession. Investors are naturally taking a more cautious stance when it comes to high-yield personal consumer lending.

This is clearly impacting LC’s marketplace revenues and origination levels. And this headwind is likely to continue and perhaps even strengthen in the next few quarters.

The Focus On Profitability

LC management is focused on growing its loan portfolio. This is the key strategic imperative and is driving strong operating leverage for the business.

This was explained in great detail in my latest article on LC.

However, to grow its book, LC must generate organic capital, and, therefore, GAAP profitability is a key enabler.

Therefore, I was not surprised that LC announced a cost-cutting exercise given the headwinds in the marketplace. LC must remain profitable to grow and generate organic capital otherwise, it will be capital-constrained. This means pulling all levers available including massive cost cuts.

I expect LC to exit 2022 with ~$5 billion of unsecured personal lending which should deliver a steadily growing income stream at a high yield. Fortunately, LC has already fully reserved for most of these loans under the CECL lifetime expected loss methodology. In 2023, I expect LC to continue to lean into retaining more loans on its balance sheet as opposed to selling these in the marketplace. I also expect it to reduce its marketing spend further and mostly focus on servicing existing LC members. Furthermore, management of credit risk will come to the forefront, especially if a recession ensues during 2023.

Final Thoughts

Mr. Market reacted well to the press release in after-hours trading with the stock up 4%. Let’s see if Mr. Market hasn’t changed his mind during Friday’s trading session.

The full earnings release on the 25th of January will be important, especially, the 2023 full-year guidance which I expect to err on the conservative side given macro uncertainties.

LC, however, should benefit from a steady interest income stream from its large portfolio to cushion the headwinds. I would also keenly look out for its capital ratio (especially the Tier 1 leverage ratio) to assess how much incremental loan capacity it is likely to have in 2023. The MUFC acquisition would utilize ~$110 million of capital, but given the short duration of the portfolio (<1 year), that capital should be released rapidly throughout 2023.

There are currently strong headwinds (rates, recession fears, investors’ appetite) in the personal lending space but the long-term narrative is fully intact. LC should remain profitable throughout 2023 and as it continues to build its unsecured lending portfolio, that profitability will increase materially in the coming years. The marketplace should begin to recover when the Fed pauses and peak recession fears pass.

In a normal economy, with an unsecured portfolio of say ~$10 billion, LC should be able to generate pre-tax income of ~$1 billion. This is the opportunity ahead. I remain very bullish about LendingClub Corporation.

Be the first to comment