jxfzsy/iStock via Getty Images

Hedge fund manager Boaz Weinstein – famous for his credit default swap and capital structure arbitrage trading strategies that he employed in the early and mid-2000s at Deutsche Bank – who today has $4.6 billion in assets under management, recently issued a grim warning that the U.S. stock market could be headed for a decades-long bear market, stating:

I’m very pessimistic. There isn’t a rainbow at the end of all this. [Quantitative tightening] is going to be a real headwind for investors.

He pointed to the Japanese stock market – which has been struggling for over 30 years (since 1989) – as an example of what the U.S. markets could have in store in the coming decades.

In this article, we will look at these trends in greater depth to test the merits of this prediction, its effects on the S&P 500 (NYSEARCA:SPY), and then will also discuss our approach and some of our top picks in the current environment.

Is A Decades-Long Bear Market Likely?

First and foremost, a decades-long bear market is not without precedent. Japan’s Nikkei 225 index (NKY:IND)(NTETF) reached its peak in 1989 and has remained in a bear market ever since. In fact, it is still ~30% down from its 1989 highs.

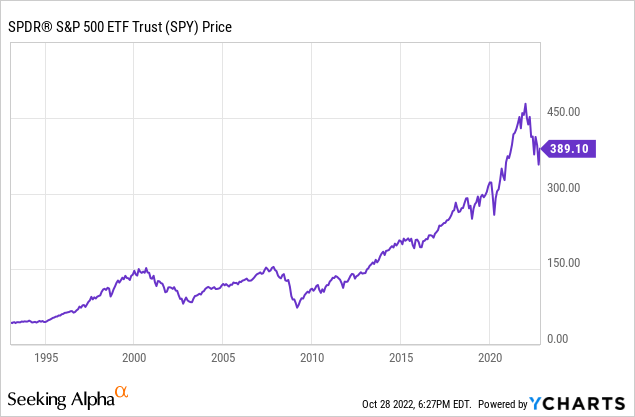

When you look at the trajectory of the SPY over the past decade and compare it to its longer term trajectory, you can certainly see how an extended period of little to no returns could be warranted, as the trendline shot sharply higher from 2016 until the beginning of 2022:

Even this year’s sharp pullback has failed to create a state of undervalued stock prices. In fact, according to a group of models used by currentmarketvaluation.com, the stock market remains 0.4 standard deviations above its long-term fair value trend. This indicates that stocks are not likely severely overvalued, but are most likely not undervalued either.

On top of that, we are still very much in a quantitative tightening cycle where the Federal Reserve is highly likely to further raise interest rates and suck more money out of the economy as it unwinds at least part of its $9 trillion balance sheet before it considers reversing course. On top of that, leading economists continue to predict that the U.S. economy will enter recession next year, despite a brief reprieve in Q3 thanks to several one-time favorable impacts on the GDP number.

In fact, the Fed is on pace to cut $95 billion from its balance sheet per month, despite knowing full well that the U.S. economy is headed straight for a recession. As a result, Weinstein thinks that the coming recession could last for an extended period of time and may also be fairly deep:

There’s no reason that this difficult [economic] period will only last two to three quarters [and] … no reason to think we’ll have a soft landing or a shallow recession.

When you compare current valuations to current macroeconomic trends, the likelihood for the SPY to deliver high returns over the next several years is already unlikely. However, when you also factor in the enormous geopolitical risks that are growing more severe and more strained by the week, the outlook is even gloomier.

If Russia’s conflict in Ukraine were to drag on for much of 2023 or – worse yet – escalate into a broader Eastern European conflict, go nuclear, or even spread into the Middle East (note Iran’s and Saudi Arabia’s growing involvement in the war), it could further drive up energy costs, bring Europe down even further economically, and push the global economy into an even deeper and longer recession than currently expected.

Then there is the risk of war erupting in the far East, which could easily turn into World War 3 if not managed carefully. North Korea has been ratcheting up tensions with South Korea and Japan with its latest round of missile tests, and China is getting ever closer to invading Taiwan, it appears. As the United States’ leading Navy admiral Mike Gilday warned recently, China could invade Taiwan any day now:

When we talk about the 2027 window, in my mind, that has to be a 2022 window or potentially a 2023 window.

If any of these geopolitical risks were to become reality – especially the Chinese invasion of Taiwan scenario – we could very possibly see a global recession that could last for a while. None of this geopolitical risk seems to be priced into the equity markets at present.

In summary, a decades-long bear market sounds a bit extreme to us, given the bullish trajectory of technological innovation and the fact that SPY has already pulled back to the point where it is only slightly overvalued according to the most popular market valuation metrics. That said, given SPY’s valuation and the fact that we are in an economic downturn, we also think it is unlikely that SPY will deliver above historical average returns – especially on a net of inflation basis – in the coming half decade. If one of the major geopolitical risks realizes, then we may very well be in store for at least one lost decade.

The Ramifications For SPY Investors

What does this mean for SPY investors, especially for those who have taken the simple path to wealth and 4% rule that involves the regular dollar cost averaging into low-cost index funds (like SPY) investment strategy and then living off of a ~4% annual liquidation of one’s SPY shares? Well, it means that this approach is more risky than ever.

In addition to the fact that we are likely to see below average real returns from SPY over the next 5-10 years due to high inflation, high interest rates, and a weakening economy against a fair to slightly overvalued price for the fund, there are also geopolitical risks to account for. This means that the most likely scenario for SPY in the coming 5-10 years is one in which it generates a CAGR net of inflation that ranges in the positive and negative low single digits. This means that – at best – 4% investors will be treading water, but they are much more likely to see principal erode at a pretty rapid rate in the coming years, especially if we see a further sell-off in the near future.

Our Approach

As a result of this risk, we think it is much more prudent – especially for investors either in or nearing retirement – to adopt an income investing approach to retirement. This way, investors can live off of the passive income thrown off by their investments without having to eat their principal and lock in losses and long-term wealth destruction by selling during a bear market.

Thanks to high interest rates, many income-oriented investments offer very attractive yields at present. For example, investment grade triple net lease REITs (VNQ) like Realty Income (O), W.P. Carey (WPC), and Essential Properties Realty Trust (EPRT) offer mid-single digit dividend yields along with mid-single digit expected annualized growth rates. Investment grade midstream businesses (AMLP) like Enbridge (ENB), Enterprise Products Partners (EPD), and Energy Transfer (ET) all offer high single digit dividend/distribution yields with attractive long-term payout growth profiles as well. Many preferred shares (PFF) also offer attractive yields at the moment. For example, the Virtus InfraCap U.S. Preferred Stock ETF (PFFA) currently offers a 10.52% dividend yield. Yes, you won’t get growth with this fund, but you get a fat monthly dividend check that more than 2x covers the 4% Rule requirements, giving you some extra breathing room to reinvest excess cash flow or to account for excessive inflation.

Best of all, all of these income streams: investment grade triple net lease REITs, investment grade midstream businesses, and preferred equities are all quite recession resistant and triple net lease REITs and preferred equities generally thrive in a deflationary environment whereas midstream businesses tend to boom along with the broader energy sector during inflationary periods. While we do not think a portfolio of just triple net lease REITs, midstream businesses, and preferred stocks is necessary ideal for everyone in every circumstance, balancing out your exposure to SPY with more concentrated positions in these sectors might not be a bad approach given the aforementioned macroeconomic factors facing us today.

Investor Takeaway

SPY is currently slightly overvalued to fairly valued, the economy is in the early innings of a downturn, the Federal Reserve is in peak tightening form, and geopolitical risks are soaring. While some are warning of a multi-decade bear market, we think that a half decade to a full decade of below average returns is more likely, unless China invades Taiwan or some other major international calamity befalls mankind.

While likely not disastrous for many investors, for those needing to live off of their portfolios in the coming 5-10 years, we think that complementing a core SPY holding with more defensive high yield investments like those we are focusing on at High Yield Investor is prudent.

Be the first to comment