alfexe

Lakeland Industries, Inc. (NASDAQ:LAKE) recently announced that the company’s completion of investments in Vietnam and Mexico could bring significant revenue growth and FCF generation. I also believe that further investments in sales personnel and more CRM capabilities will likely enhance future sales expectations. Even considering the risks from wrong assessment of future demand or failed acquisitions, the company appears too cheap at this point in time.

Lakeland Industries Offers Access To A Diversified Number Of Markets And Regions

Founded in New York and with 40 years of support in its operations, Lakeland Industries is a company that offers the production and sale of security products for industries and retail customers. 95% of its garments are manufactured in plants that are owned by the company, avoiding dependence in this regard for its frontal operation.

Source: Investor Presentation

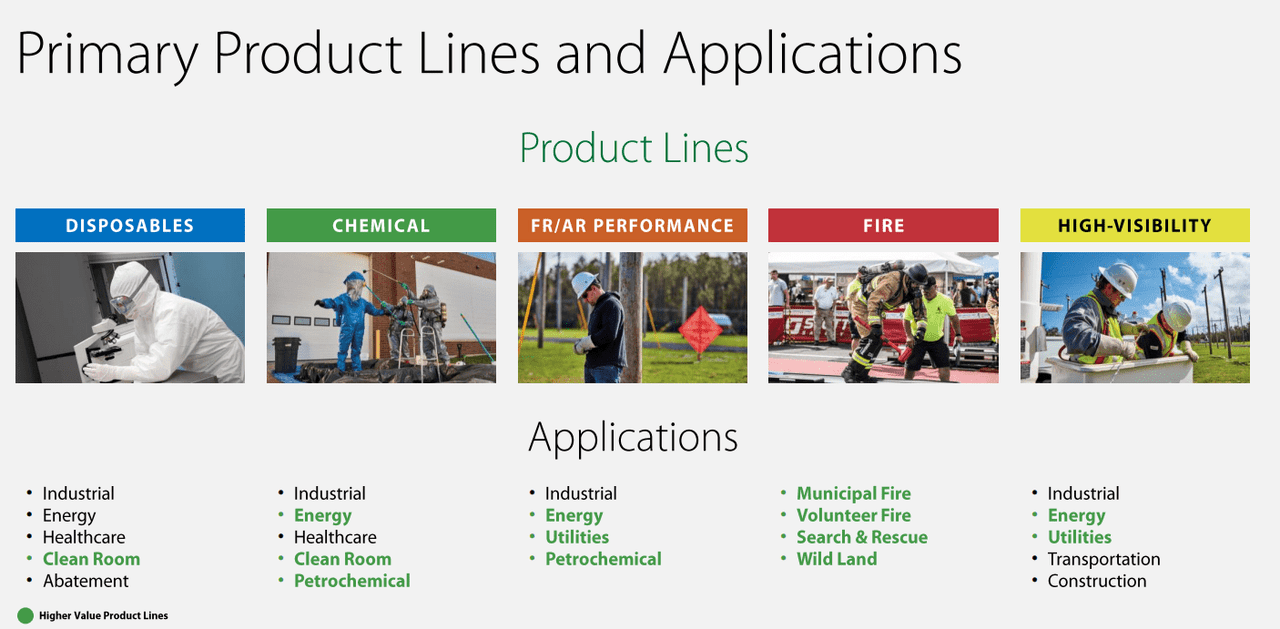

I also believe that the level of diversification of Lakeland needs to be mentioned. Through more than 1,600 official licensed subsidiaries in outlets globally, Lakeland offers its products to end consumers that include a diverse variety of areas such as the scientific, construction, transportation, and automotive industries among others.

Source: Investor Presentation

Currently, its sales expand to more than 50 countries, most of which are in China, the European Union and peripheral countries such as Argentina, Chile, or Kazakhstan, Russia, and some countries in Southeast Asia.

Source: Investor Presentation

Solid Financial Position

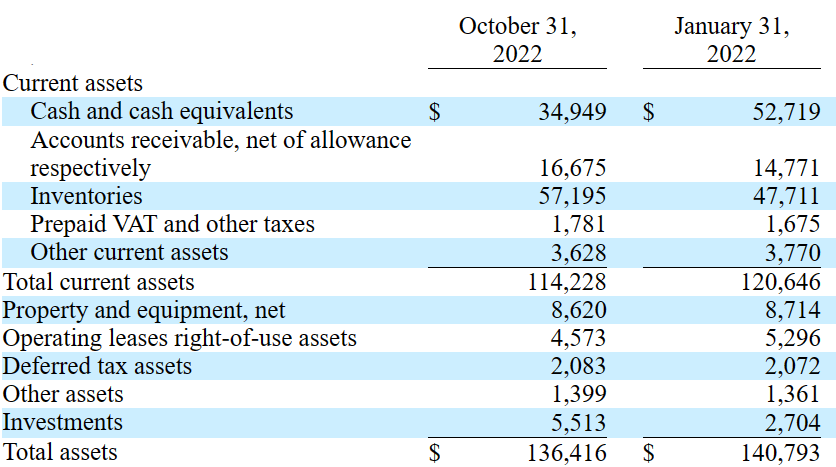

As of October 31, 2022, Lakeland Industries reported cash worth $34.949 million, accounts receivable worth $16.675 million, inventories of $57.195 million, and total current assets of $114.228 million. The current ratio is larger than 10x, so I wouldn’t expect a liquidity crisis anytime soon.

With regards to non-current assets, property was worth $8.620 million with operating lease rights of use assets of $4.573 million. In sum, the total amount of assets stood at $136.416 million, close to 7x the total amount of liabilities. Yes, the balance sheet looks quite healthy.

Source: 10-Q

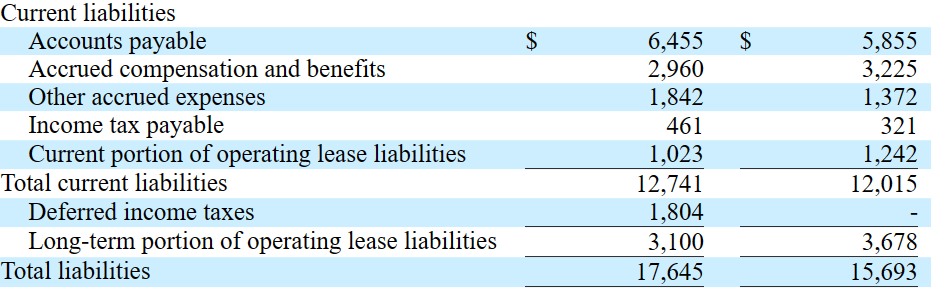

For the liabilities, I saw accounts payable worth $6.455 million along with accrued compensation of $2.960 million, other accrued expenses worth $1.842 million, and total current liabilities of $12.741 million.

Non-current liabilities included deferred income taxes worth $1.804 million and long term portion of operating lease liabilities of $3.1. Finally, total liabilities stand at $17.645 million.

Source: 10-Q

Competitors Are Massive, Which Some Investors May Not Appreciate

DuPont (DD), Kimberly-Clark (KMB), Ansell (OTCPK:ANSLF), and Honeywell (HON) are the main competitors of Lakeland. Out of these, few companies concentrate most operations, especially for what concerns the clothing industry for chemical industries. In this sense, Lakeland considers that entering the podium of these companies is really difficult due to the magnitude of their operations and the ease of their production, but it does not rule out competition at the regional level at different places where their factories are located.

Under Normal Expectations, I Obtained A Fair Price Of $37.29

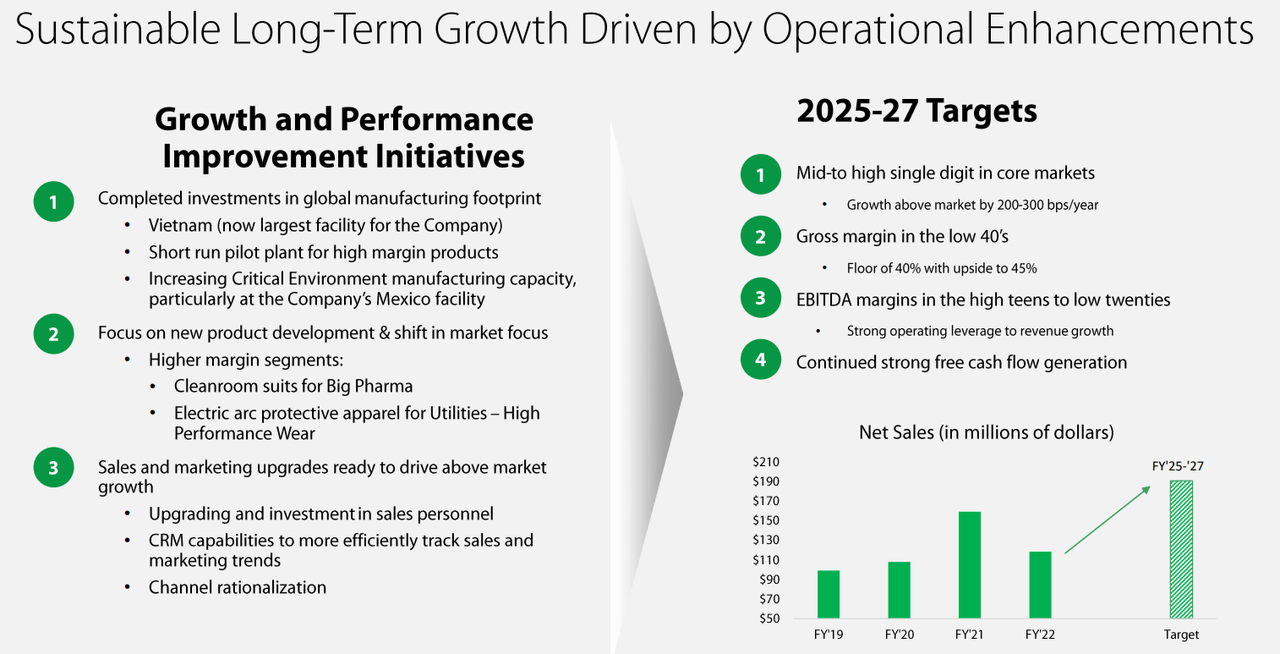

Considering the targets given for 2025-2027, I believe that running a DCF model makes a lot of sense. Management expects continued strong free cash flow generation, EBITDA margins around 14%-24%, and a maximum gross margin close to 45%. Lakeland believes that these financial targets are possible thanks to successful completion of investments in Vietnam and Mexico. Besides, Lakeland Industries also expected investments in sales personnel, more CRM capabilities, and channel rationalization.

Source: Investor Presentation

In my view, continuing with the development and efficiency of its production capacities, which are at this moment the great differential over its competitors, as well as to direct new technological research for potential products may bring FCF generation in the long term.

In the same way, I expect further development of customer service, which is one of the important points in the credibility and approach to its customers, offering immediate solutions as well as advice on the use of its products.

Besides, I am optimistic about future new products and further concentration of the company’s operations in sectors where Lakeland has commercial advantages over its competitors. Under these conditions, which management included in the last 10-k, I would be expecting revenue to trend further north.

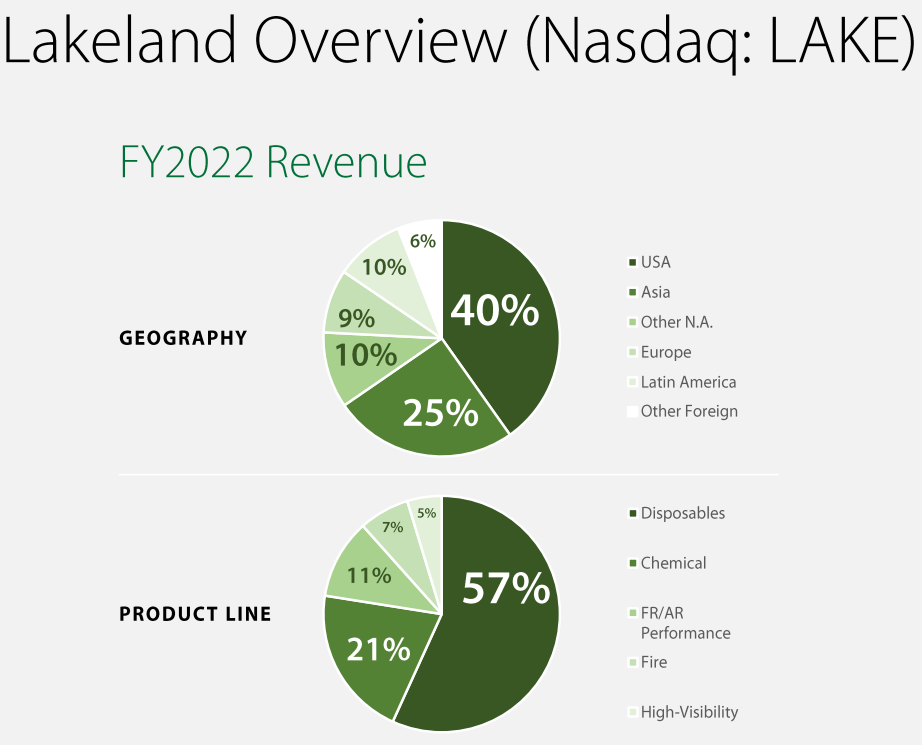

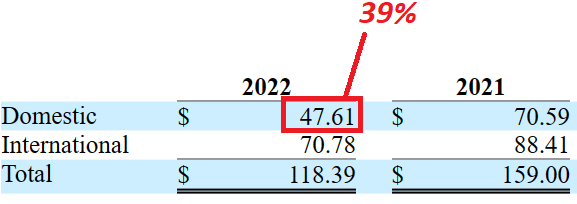

Lakeland divides its business into the domestic sales segment and the international sales segment. The latter is the one that significantly brings more income to the company. It is mainly due to the fact that Lakeland has a single production plant in the United States, located in Alabama, while it has plants in Mexico, China, India, and Vietnam, indicating its position and power in Asian territory.

In 2022, domestic net revenue stood at $47.61 million, 39% of the total amount of revenue. International net sales were equal to $70.78 million. I believe that international revenue and domestic revenue will likely grow at a different pace, so I divided my financial model in two parts, one for each operating segment.

Source: 10-k

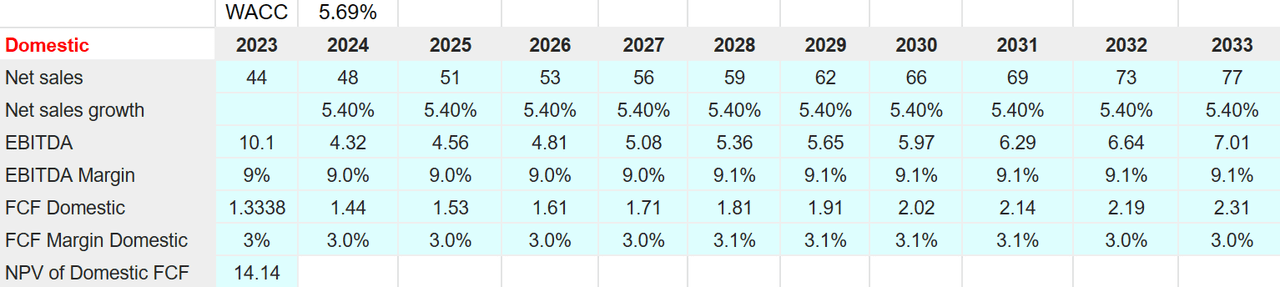

I also considered that the global protective clothing market is expected to grow at a CAGR of close to 6.3%, and the North America protective clothing market will likely grow at a CAGR of 5.4%. These numbers were obtained from market experts:

The global protective clothing market had a revenue share of USD 8,421 million in 2021, projected to reach USD 13,729 million with a CAGR of 6.3% during the forecast period. Source: Protective Clothing Market Trends and Analysis

The North America protective clothing market was valued at $2.9 billion in 2019, and is projected to reach $3.8 billion by 2027, growing at a CAGR of 5.4% from 2020 to 2027. Source: North America Protective Clothing Market Size | Industry Forecast, 2027

With the previous figures, I obtained 2033 net sales of $77 million together with a net sales growth of 5.40%. Besides, I obtained 2033 EBITDA of $7.01 million accompanied by an EBITDA margin of 9.1%. 2033 domestic FCF would be $2.31 million with a domestic FCF margin of 3%. Finally, with a discount of 5.69%, I estimated net present value of domestic FCF of $14.14 million.

Source: Malak’s Work

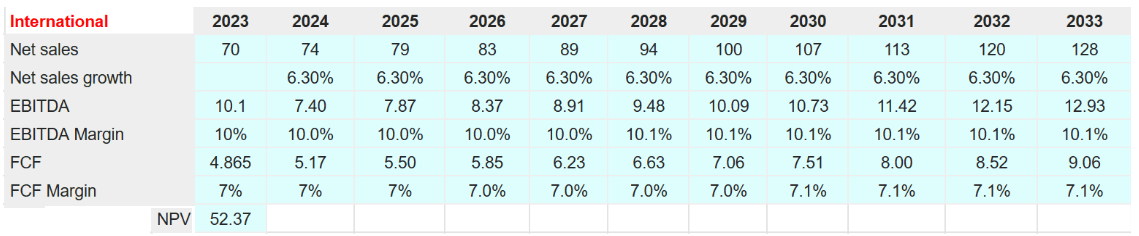

Regarding international net revenue, I also expected 2033 net sales of $128 million with net sales growth of 6.30%. 2033 international EBITDA would be $12.93 million along with an EBITDA margin of 10.1%. I also expect international FCF of $9.06 million accompanied by a domestic FCF margin close to 7.1%. Finally, the net present value of international FCF would be $52.37 million.

Source: Malak’s Work

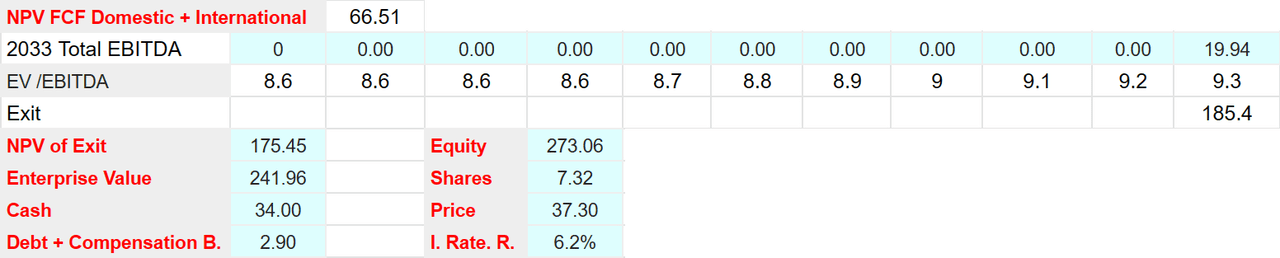

The sum of the NPV of domestic and international FCF would be $66.51 million. With an exit of EV/EBITDA 9.3x, I foresee an exit close to $185.4 million. The NPV of exit would be $175.45 million.

My results would also include an enterprise value of $241.96 million. With cash of $34 million and debt of $2.90 million, the equity valuation would stand at $273.06 million. Finally, I obtained a fair price of $37.29 per share and an internal rate of return of 6.2%

Source: Malak’s Work

Risks Could Include Wrong Assessment Of Demand, Failed Investments Or Acquisitions, And Corruption Outside The United States

Lakeland’s most relevant risks are related to international trade operations, such as variations in the exchange rate, export regulations and production conditions, the instability of the current economy, and the possibility of alterations in the supply lines of raw materials. Considering the situation of increase in demand of gas and oil due to the war in Ukraine, I would lay specific emphasis to this factor.

For the nine months ended October 31, 2022, sales in Russia were approximately 2.4% of our consolidated sales and sales into Ukraine were not significant. We do not have any capital assets in Russia. Source: 10-Q

Besides, Lakeland Industries reports acquisition strategies, specifically with the objective of building new manufacturing plants. Let’s point out, for instance, the investment in Inova Design Solutions Ltd. In line with this rationale, readers should keep in mind that investments and acquisitions could go wrong. The transactions may not bring what the company was expecting, and revenue or synergies could be less than expected.

Acquisitions involve a number of special risks in addition to those mentioned above, including the diversion of management’s attention to the assimilation of the operations and personnel of the acquired companies, the potential loss of key employees of acquired companies, potential exposure to unknown liabilities, adverse effects on our reported operating results and the amortization or write-down of acquired intangible assets. Source: 10-k

On October 18, 2021, the Company made a strategic investment of $2.8 million in Inova Design Solutions Ltd. as a step toward entering the Connected Worker Market for Smart PPE. Source: 10-k

On December 2, 2022 the Company acquired UK-based Eagle Technical Products Limited in an all-cash transaction valued at approximately $10.8 million subject to post-closing adjustments and potential future earnout payments. Source: 10-Q

Lakeland Industries also notes that in some of the countries in which it competes, mainly Latin America and part of Asia, corruption could be a problem for its operations. Since Lakeland complies with both US and UK legislation, while some regional competitors do not adhere to these laws, generating business agreements and commercial operations with the endorsement of governments outside of the usual tenders and official channels may be problematic.

Lakeland Industries could also overestimate customer demand, which may lead to wrong allocation of resources to products that the company may not sell. Underestimation of demand may also lead to insufficient manufacturing capacity. In sum, in my view, wrong assessment of the market could lead to wrong actions, which could bring diminishing FCF margins and lower stock valuations.

If we underestimate customer demand or if insufficient manufacturing capacity is available, we would lose sales opportunities, lose market share and damage our customer relationships. On occasion, we have been unable to adequately respond to delivery dates required by our customers because of the lead time needed for us to obtain required materials or to send fabrics to our assembly facilities in China, Vietnam, India, and Mexico. Source: 10-k

My Takeaway

Lakeland Industries expects EBITDA margin increases and FCF generation thanks to the company’s completion of investments in Vietnam and Mexico. I also believe that Lakeland Industries’ expected investments in sales personnel, more CRM capabilities, and channel rationalization that were recently announced could enhance both domestic and international revenue. I also see risks from wrong assessment of future demand or failed investments corruption cases outside the United States, which may diminish future free cash flow expectations. With that, I believe that Lakeland Industries could be worth much more than what the market currently reports.

Be the first to comment