DNY59/iStock via Getty Images

Don’t give up on the Santa Claus rally! Things were looking pretty grim on Wednesday when investors started to fear that the end of China’s Zero-Covid policy, intended to stoke economic growth, might have the opposite effect by leading to a global resurgence of the pandemic. Announcements of measures being taken in China, the US, and other nations around the world to limit the spread appears to have alleviated those concerns. Yesterday, investors refocused on the welcome news that unemployment claims rose modestly to 225,000, suggesting that the labor market is starting to weaken. That was all it took for the major market averages to rip to the upside and wipe out losses from the prior two days.

Finviz

The weak spot in the claims report had to do with the increasing number of unemployed who continue to seek benefits, which is up to a February high of 1.7 million. This indicates that those who have lost their job are having a more difficult time finding a new one. It shows that the labor market is starting to loosen, which should result in slower wage growth, and that is what the Fed wants to see before it stops raising interest rates. Yet the labor market has been weakening for months, which was obvious in last month’s jobs report, and I hope for further confirmation in next week’s jobs number for December.

Bloombeg

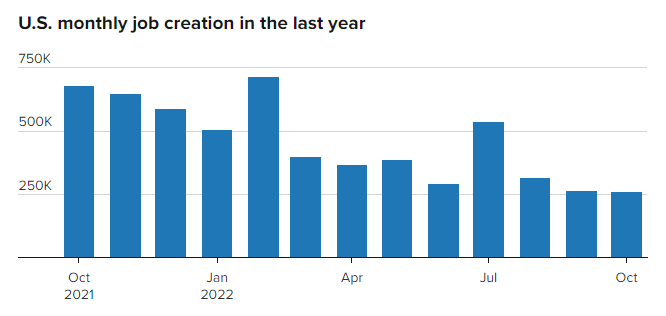

The number of job gains each month has decelerated over the past year by more than 50%. The number of hours worked each week has also been declining. While the average workweek was 34.8 hours in November of 2021, it declined to 34.4 hours in November of this year. That may not sound like much, but it has a meaningful impact on weekly take home pay, which does not show up in average hourly earnings.

CNBC

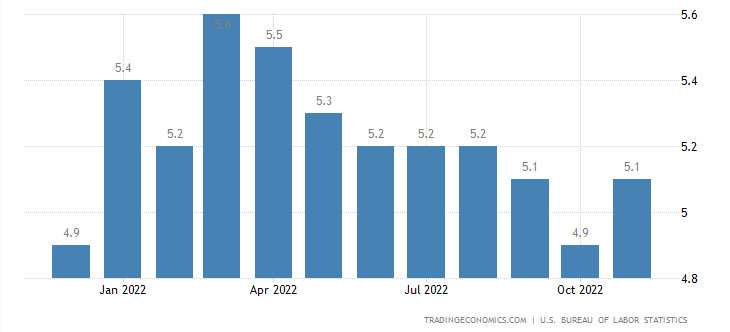

Still, average hourly earnings growth for all employees peaked in March of this year at 5.6% and has been gradually declining as well.

TradingEconomics

In fact, every metric for the labor market has been gradually weakening with the exception of weekly claims, which is what we want to see in a soft landing scenario. This should continue in 2023 at the same gradual pace, and the rate of inflation should follow with a lag. We do not want to see a jaw-dropping decline in any of these reports, as that will just incite recession fears.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment