La-Z-Boy is aiming to increase its store count by around 14%, while also increasing the number of company-owned stores, which would improve its profit margins.

SOPA Images/LightRocket via Getty Images

The most recent addition to my portfolio surprised me a bit when I dug into it, because when it popped up on my value stock screener, I didn’t expect La-Z-Boy Incorporated (NYSE:LZB) to be a company with a long-term plan for future growth. I expected it to be a value stock at a good price, with a conservatively run business with a strong balance sheet, and an ability to bounce back when the macroeconomic headwinds turn.

As it turns out, it’s that and more, with a new marketing plan centered around “Long Live the Lazy.” Turns out, the first half of that adequately describes the company’s earnings growth as well.

Investment Thesis

La-Z-Boy is undervalued based on a strong balance sheet, no debt, an impressive track record of earnings growth, and a plan to deliver more growth in the future. Over the last decade of full-year results, LZB has grown its earnings per share at a compound annual rate of 15.14%.

The 2024 consensus estimates call for a pullback, which will likely be the case, but forward estimates of no earnings growth seem too bearish given the company’s history and long-term strategies.

About La-Z-Boy

La-Z-Boy is the leading global producer of reclining chairs, and the second largest manufacturer and distributor of residential furniture in the United States, according to their annual report. LZB has five major manufacturer locations and 12 distribution centers in the US, and four in Mexico. They also have a global trading company in Hong Kong to manage their Asian supply chain.

Per that annual report, their primary distribution is through 349 La-Z-Boy furniture galleries, of which they own around half, as well as 522 Comfort Studio locations that are all independently owned and operated.

Founded in 1927, La-Z-Boy is approaching its 100th anniversary, and they are in the process of executing a plan to set them up for the next century of business, which we’ll break down in more detail below.

Value Fundamentals

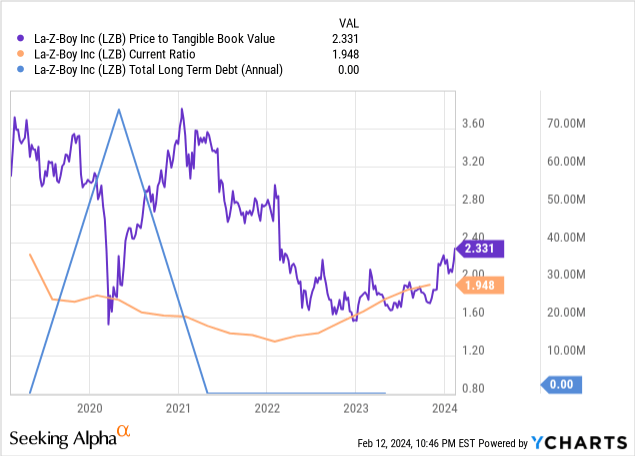

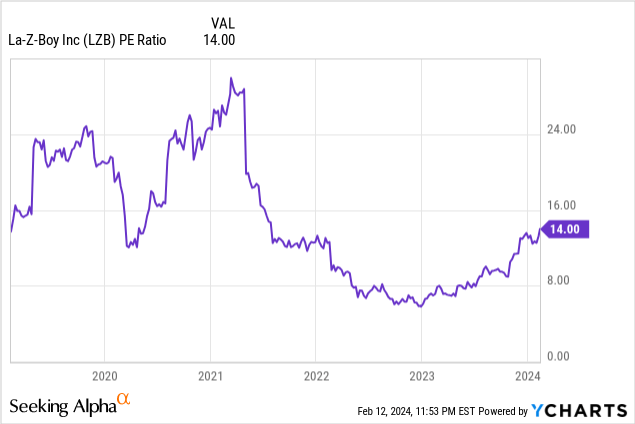

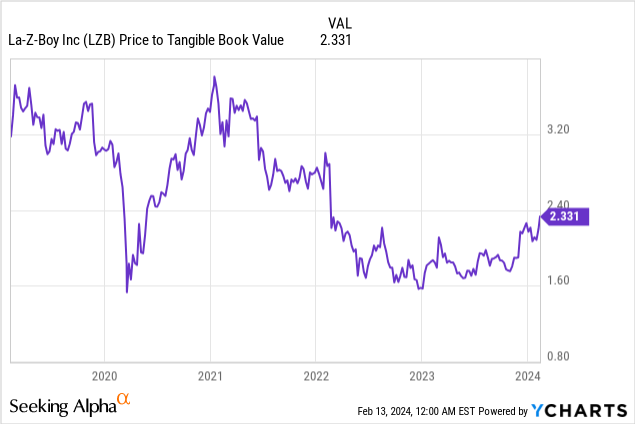

La-Z-Boy is trading reasonably close to its tangible book value, at about 2.33x the $16.60 per share of tangible book value calculated from the balance sheet as of the second quarter. The business is well capitalized with a current ratio just under 2, and there is no long-term debt.

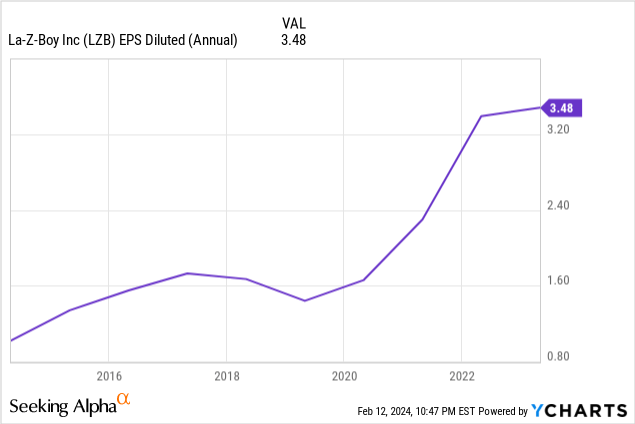

But perhaps the most impressive metrics for value investors with La-Z-Boy are the earnings history. In addition to the impressive CAGR mentioned above, you can see that pullbacks in earnings have been rare for LZB – and generally minor.

This is a tough stretch for the furniture industry, but La-Z-Boy beat earnings estimates by $0.12 per share in the second quarter to come in at $0.74. For the year, their earnings are expected to be down year over year, but they’re still more than respectable and the analysts’ estimate of $2.91 would still continue the trendline of growth over the long term.

Part of the reason I expect the earnings growth to continue in the years to come is the plan to continue acquiring retail locations, which I’ll detail in the growth catalysts section below.

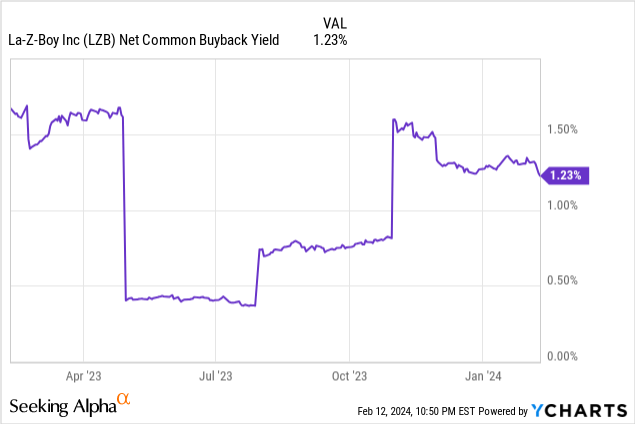

Last but not least, the company currently has a dividend yield of 2.1%, with a buyback yield of a little over 1%.

That combines to be a decent return of capital, with a long-term plan to return half of their cash flow to shareholders. That said, they will not be married to that number in a given year – it’s a long-term target, which is the right way to run a business.

On the first quarter earnings call, La-Z-Boy CFO Bob Lucian explained their intentions.

The 50-50 split may vary in any given year. In the near term, including fiscal ‘24, we have numerous strategic investments to make as we execute Century Vision and anticipate capital allocation to be more skewed towards investments in the business, where our ROIs are two to three times our cost of capital. That said, presuming no significant worsening in macroeconomic trends, we expect to continue share repurchases at dollar levels consistent with pre-COVID.

Risks and Headwinds

It’s always important to understand why a stock is priced cheaper than it should be, to make sure the market isn’t seeing something we’re missing as a potential value investor.

Macroeconomic Headwinds

I believe this is the main reason LZB, like other furniture stocks, is trading relatively cheap. With persistently high interest rates, there is less homebuying. Fewer people moving into new homes means fewer people furnishing those homes, which hurts furniture manufacturers and retailers. Likewise, furniture falls under discretionary spending. So if consumers are squeezed, business will be slow for LZB.

For a period of time after the COVID-19 pandemic, cyclicals were thrown out of whack due to supply chain pressures. In the most recent annual report, the company explained that things are normalizing.

However, during fiscal 2023, demand trends have returned to pre-pandemic patterns and therefore, in fiscal 2024, we anticipate furniture demand and purchasing cycles to respond to macroeconomic conditions as they historically have.

This is good and bad. In many industries, we saw retailers build up inventory to mitigate supply chain risks – that has to get sold through as things normalize. In addition, low interest rates and a flurry of home purchases meant more business and perhaps an extended up cycle for LZB.

Investors can’t be happy to hear that the cyclical nature is going to respond to macroeconomic conditions at a time when rates are persistently high. Many expect the Fed rate to drop significantly this year, but as a value investor, I’m not concerned with it beyond identifying the risk factor.

As you’ll see below, this situation is also creating opportunities for LZB.

Tough Industry to Compete In

As LZB identifies in their 10-K, “The residential furniture industry is highly competitive and fragmented.” In other words, it’s harder to track competitors, established brands are always subject to being undercut on price or beaten on quality, and it can be a tough balance to strike.

This prevents challenges and can lead to lower multiples in the industry. However, I believe there is ample upside for taking that risk, and La-Z-Boy’s long history shows they have navigated the furniture industry well.

Shrinking Middle Class

La-Z-Boy primarily sells furniture to the middle class and upper middle class. So, as they explain in their 10-K, this opens them up to risks if fewer people are shopping at that price point.

“We compete in the mid to upper-mid price point, and a shift in consumer taste and trends to lower-priced products could negatively affect our competitive position.”

They refer to consumer tastes, but I think of this more as a risk with the middle class shrinking. There are a variety of metrics you can consider, but Pew Research has the size of the middle class shrinking by about 40 basis points per year over a 50-year stretch, while Consumer Affairs points out a decrease in the percentage of income brought home by the middle class as opposed to the upper and lower classes.

These are definitely concerns, but the trends seem to be moving slow enough for businesses to adjust accordingly. La-Z-Boy is researching lower price points for value seeking consumers, starting by opening a couple Outlet by La-Z-Boy stores and mining the data.

“This is a great opportunity for us to explore new formats and broaden our reach to value-seeking consumers,” said president and CEO Melinda Whittington on the Q1 earnings call.

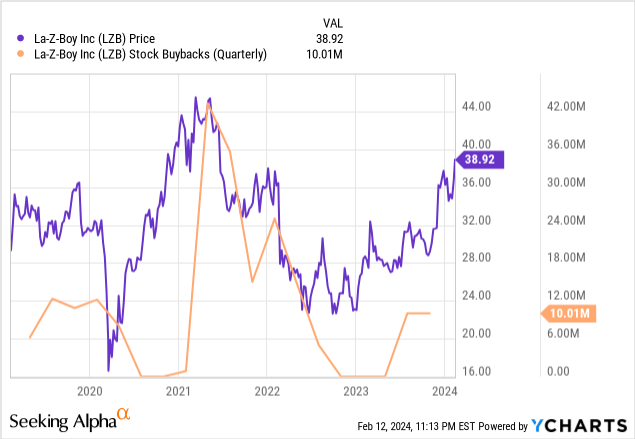

Poorly Timed Buybacks

From looking at their history of buybacks, I do have some concerns over the timing. Over the last five years, some of the highest rates of buybacks have occurred at the highest prices, and then the buybacks have dropped off as the stock price has dipped.

There are two schools of thought on this. As a value investor, I only want companies I’m invested in buying back their stock when it is discounted. Others are happy to see buybacks any time because they drive prices higher.

Of course, it’s possible that the company believed the stock was undervalued at $44 a share in 2021, and that there were other reasons to stop buying for a stretch in 2023. However, it’s something I’ll be keeping an eye on. That said, it’s a relatively minor concern because if they’re buying the stock back at too high of a price, that should create an opportunity for a profitable exit.

Potential Growth Catalysts

Once I’ve identified a stock trading at a discount and have a good understanding of why, I’m most of the way to making an investment. But it’s also important to see a path to realizing the value – so identifying a few potential growth catalysts is ideal.

Century Vision

La-Z-Boy is undertaking a strategy they’re calling Century Vision, based on setting the business up for the next 100 years as they approach their 100-year anniversary in 2027. I applaud long-term thinking, and it’s something that’s sorely lacking in corporate America, in my opinion.

There seem to be a few pillars of the strategy, but one of the first is to modernize the brand, which Whittington talked about on the Q1 call.

“We will broaden La-Z-Boy from a brand seeped in nostalgia to an active, dynamic and distinctive brand for modern audiences, to increase our top-of-mind awareness and relevance. As I mentioned, following extensive consumer research and segmentation work, we launched our new national brand campaign, Long Live the Lazy.”

If the first commercial is any indication, they’re on the right path in my opinion. The modernization is also not just in branding. They will also be leveraging their database for consumer insights.

Perhaps the most important part of the strategy for investors, though, is their targets of achieving sales growth ahead of the industry and double-digit operating margins. Obviously, it’s easy to throw targets around, but they have a focused plan to reach those goals.

Lucian broke it down on the Q1 call.

“First thing is Retail, and that’s growing that business to that 400 store level that we’re talking about and getting ourselves into a consistent, middle teams operating margin. The second one is the Wholesale business and getting it back to a 10% operating margin. Pre-pandemic, we were operating at around 10% in that business for a number of years in a row. We’re below that now. We expect over the next two to three years, we’ll be getting back to that 10% with a lot of work we’re doing with our supply chain, and how we’re managing manufacturing throughout the company.”

One example of the streamlining of the supply chain was the closing of a facility in Mexico that they had opened to expand capacity when the supply chain was more at risk to make sure that they could deliver for customers. Lucian told investors on the call that they were able to absorb all of that volume into their other existing plants because of improved productivity. They expect the move to improve their operating margins by 50 to 60 bps.

Refocusing on efficiency like that will go a long way towards improving the margin to their 10% target.

Growing Owned Store Count

As I mentioned earlier, there are 349 La-Z-Boy Furniture galleries, and now 177 are company owned – up from 171 at the end of last year. Increasing this number as much as possible is significant because the operating margin in fiscal year 2023 was 16.5% in retail and 6.8% in wholesale, according to their 10-K. Whittington said on their second quarter earnings call that they’re making sure their gallery owners are aware that they are looking to acquire more locations.

“We have talked over the last couple of years about being a little more strategic in those conversations on our end, rather than kind of waiting to see if someone knocks on the door, making sure we are proactively partnering with our long-term independent furniture gallery owners so that they know we are here, if they are interested and what that would look like for them financially.”

She also pointed out that those acquisitions are immediately accretive to LZB’s profitability. La-Z-Boy is also opening new stores, with plans to open high single digit stores in 2024, according to the most recent annual report. With $337 million in cash on the balance sheet and no long-term debt, the company has plenty of room to maneuver in this regard.

Expanding towards the 400 stores Lucian mentioned above would mean approximately a 14% growth in store count and further improve their margins.

Playing Offense As Competitors Struggle

One reason value investments into struggling industries can yield great results is that, if the company is well-run and opportunistic, a strong balance sheet can lead to some good opportunities. Whittington confirmed that La-Z-Boy is looking to grow and expand when other companies fail due to high interest rates or tightening consumer discretionary spending.

“It’s a tough industry out there, and in our highly fragmented market, there’s been a decent number of both manufacturers and retailers that are leaving the business. And so we’re opportunistic about that, right? And even across some of our, not just our La-Z-Boy brand, but across some of our other smaller brands, we’re making sure that we’re mobilizing to help retailers that have lost some of their supply sources as manufacturers have gone out.”

Again, that lack of debt and $337 million in cash could prove quite useful if the downtrend in the cycle continues.

Rate Cuts and Improving Economy

On the other hand, if things turn back sooner, then the top line numbers will improve sooner and earnings should follow anyway. It’s a bit like: heads LZB wins, tails their competition loses.

The CME FedWatch markets are predicting a 100% likelihood of rate cuts by the end of the year and around an 80% likelihood of cuts of 1% or more. That could be enough to lead to increased homebuying and thus increased purchases of furniture.

I personally think the FedWatch markets are a bit too bullish on rate cuts, but as I’ve explained, I see opportunity either way for La-Z-Boy. It’s just a matter of the timeline this all plays out over because I believe LZB is positioned well with ample resources.

Joybird

Finally, one of the cooler things I learned about in my research. Let’s be honest, La-Z-Boy is not the sexiest investment. But Joybird is pretty intriguing. It’s an internet-based furniture brand that La-Z-Boy acquired in 2018. They make mid-century modern furniture, and they have strong long-term growth potential.

It’s not at all what you think of when you think La-Z-Boy, and the style of their furniture reminds me more of West Elm, a Williams-Sonoma brand that is popular with younger consumers.

LZB is expanding the brand to brick-and-mortar locations, with 12 open as of the most recent earnings call. Obviously, it remains to be seen whether they can execute this strategy, make Joybird profitable, and grow it successfully.

That said, mid-century modern furniture is popular with younger generations, and West Elm has recently been the fastest growing brand for Williams-Sonoma (WSM).

Valuation

My primary strategy is to identify bargain stocks and a range to consider exiting that is well above my entry point, based on multiples the stock has reached in recent history.

As we can see, LZB has achieved a P/E ratio above 24 on numerous occasions, and has spent significant time trading above 20x. Their trailing 12-month earnings are $3.26, and their forecasts for the next two years are $2.91 and $3.17. So this gives us a range over the next two years of $58.20 to $63.40.

I personally am more bullish on their earnings potential than the analysts, so it could get better over time.

In terms of price to tangible book, we’ve seen it spend significant time above 3.2x, which would currently correspond to $53.13. Assuming the tangible book value grows a couple of dollars per share over the next couple of years, a 3.2x multiple would hit somewhere in that $58.20 to $63.40 range mentioned above.

Obviously, investors should monitor developments and earnings reports to see how these numbers shift, but for now, it looks reasonable to expect an opportunity to exit this investment in the $58 to $63 range within the next couple of years.

Conclusion

As a result, I think La-Z-Boy is a buy that should deliver strong returns over the next couple of years. If the company is able to execute its Century Vision plans, the earnings per share should grow and the stock should get some more attention and find a more reasonable price around $58 to $63, which would show investors tremendous returns at current price levels.

LZB reports earnings for the third quarter next week, so investors should keep an eye on that. The consensus estimate is for flat earnings in Q3 versus Q2, at $0.74. I’m not too worried about hitting the number in any given quarter, rather I’ll be listening to the guidance going forward – in particular about the progress in acquiring existing stores and opening new stores.

Be the first to comment