Editor’s note: Seeking Alpha is proud to welcome Jared McCutcheon as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

xavierarnau/E+ via Getty Images

Investing in Saudi Arabia via KSA

Are you looking for a way to profit from an established country’s economic transformation? When the iShares MSCI Saudi Arabia ETF (NYSEARCA:KSA) launched in 2015, investors gained an easy way to access broad exposure to the country. The fund is a market-cap-weighted index that tracks the broad-based index composed of Saudi Arabian equities. The ETF is traded on the NYSE and is an iShares product powered by BlackRock.

Cost

The fund’s expense ratio comes in at 0.74%. This is higher than average for both the miscellaneous region category and what investors typically expect from a passive ETF. The ability to easily gain exposure to a country that has historically been inaccessible to foreign investors makes this relatively high management fee more palatable. The only other option for U.S. investors is the the Franklin FTSE Saudi Arabia ETF (FLSA) with a respectable expense ratio of 0.39%. However, FLSA has failed to gain significant assets since its launch in 2018 and, sitting today at only $5M AUM, investors should prefer to pay an extra 0.35% for KSA to avoid potential liquidity and spread issues.

AUM, Liquidity, and Institutional Adoption

KSA is approaching $900M in total AUM (assets under management). The fund saw $7M in outflows in 2022, less than 1% of AUM – an impressive feat considering how challenging the year was for the stock market.

FactSet Analytics Block Liquidity, a measurement that shows how easy it is to trade a $1M block of a security, rates KSA at a 4 out of 5. The average daily share volume over the last 45 days exceeds 400,000 shares with an average spread of 0.03%. Liquidity should not be a concern.

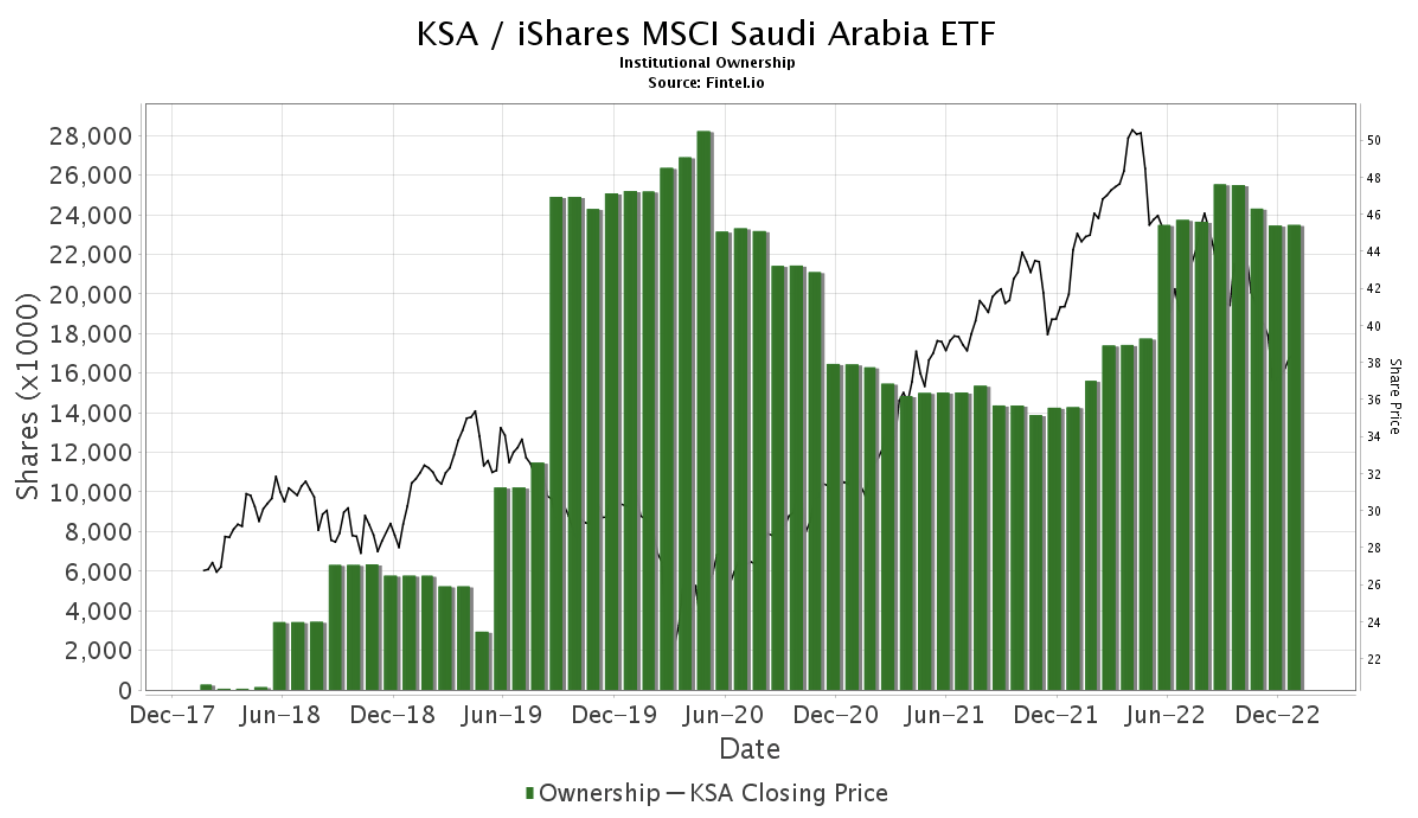

Institutional ownership has drastically increased in 2022, almost completely recovering from the 2020 sell-off and a lackluster 2021. According to the latest 13F filings, at least 18 institutional investors hold more than 250,000 shares of KSA.

fintel.io

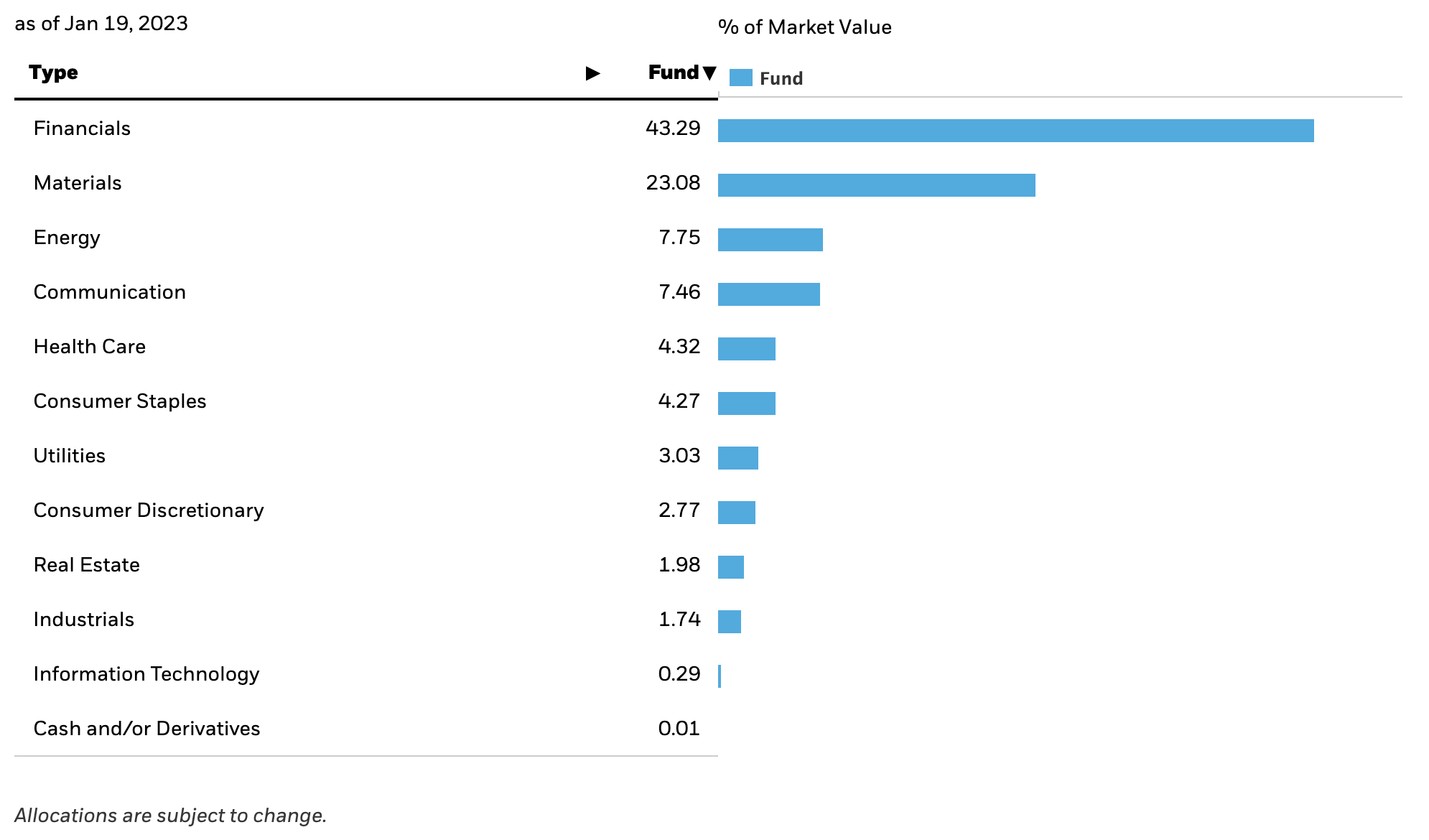

Sector Weights and Market Capitalization

The financials and materials sectors comprise two-thirds of the fund, followed by modest allocations to energy, communications, healthcare, and consumer staples.

ishares.com

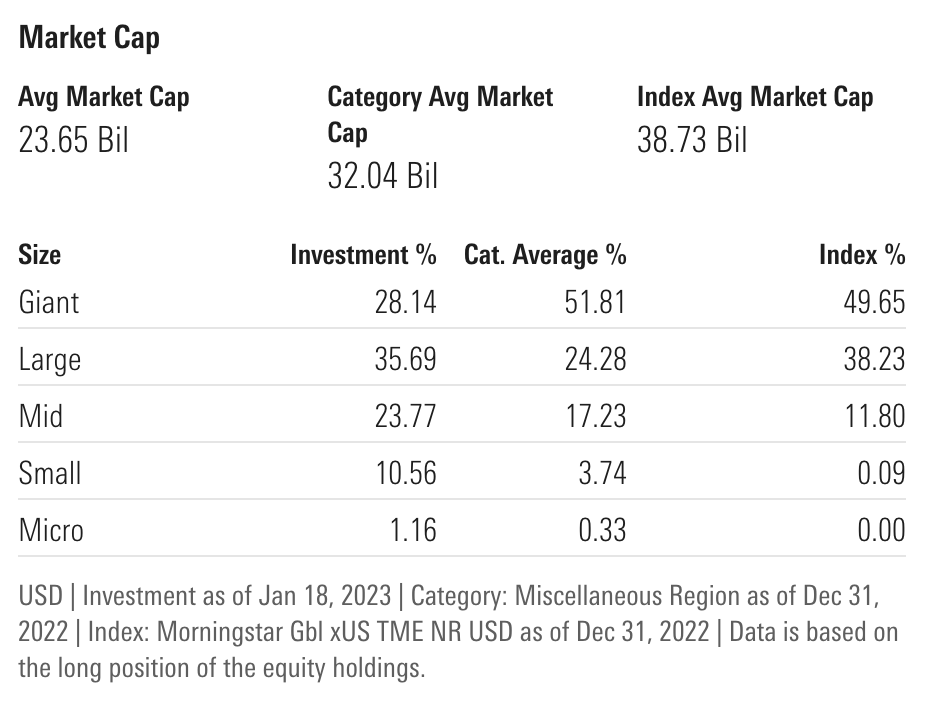

As of Jan. 18, 2023, KSA has 108 holdings and an average market cap of $23.65B. As such it broadly fits in the large-cap bucket, but contains a sizable allocation to small-cap companies, making up over 10% of the fund.

Morningstar.com

ESG

KSA does not seek to follow an environmental, social, or governance investment strategy. Morningstar has assigned KSA a single globe, their lowest possible sustainability rating. MSCI rates KSA a 2.4 out of 10 for their ESG quality score. Sustainability conscious investors should look elsewhere.

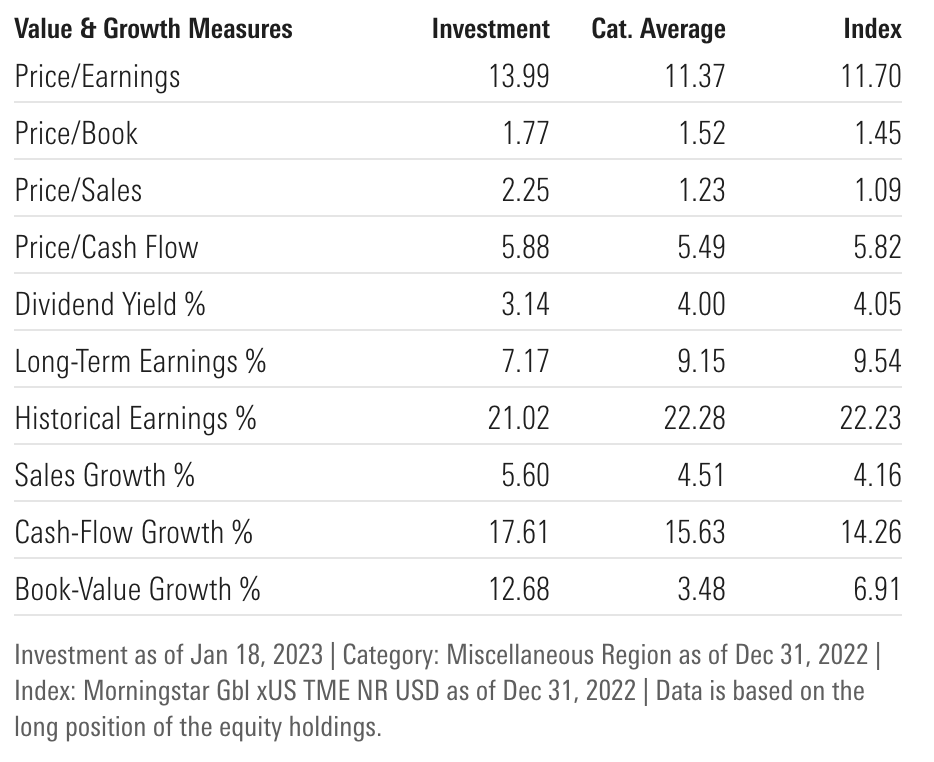

Growth and Valuation Metrics

Relative to the category and index, KSA boasts a higher sales growth percentage, cash flow growth percentage, and book/value growth percentage. This is at the cost of higher valuation multiples, but with a modest P/E of 13.99 there is still plenty of room for future expansion.

morningstar.com

Just Another Oil Proxy?

Many investors view an investment in Saudi Arabia as a proxy for oil. They wouldn’t be completely wrong, as oil production is still the dominant driver for the Saudi Arabian economy. However, with Saudi Arabia planning their 2023 budget for a sub-$80 barrel, and the country posting their first budget surplus in over a decade, there is less concern (relative to previous years) of Saudi Arabia having significant issues balancing its budget in 2023.

A strategic framework to reduce the country’s dependence on oil and diversify into other sectors was initiated in 2016. This program, called Vision 2030, created a handful of new government entities that have been developing businesses in service sectors unrelated to oil. This is why the time is right: The conservative oil price expectation and major efforts underway to create new businesses and diversify the economy away from oil could catapult the Saudi businesses to new all-time highs in 2023.

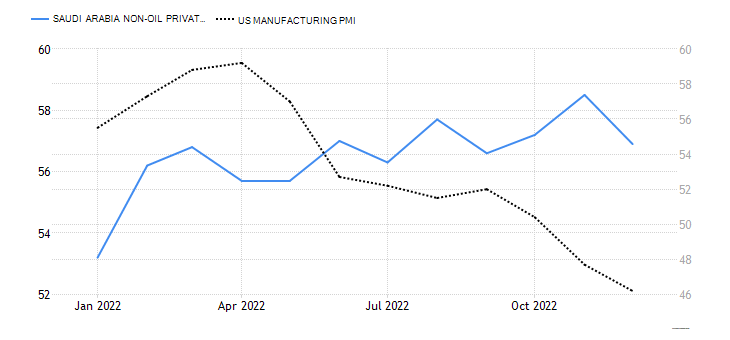

The Purchasing Managers’ Index (PMI) shows the direction of economic conditions for businesses (primarily manufacturing) within a country. Comparing the Saudi Arabian non-oil private sector PMI to the U.S. manufacturing PMI, we see opposite trends throughout 2022.

TradingEconomics.com

The Technicals

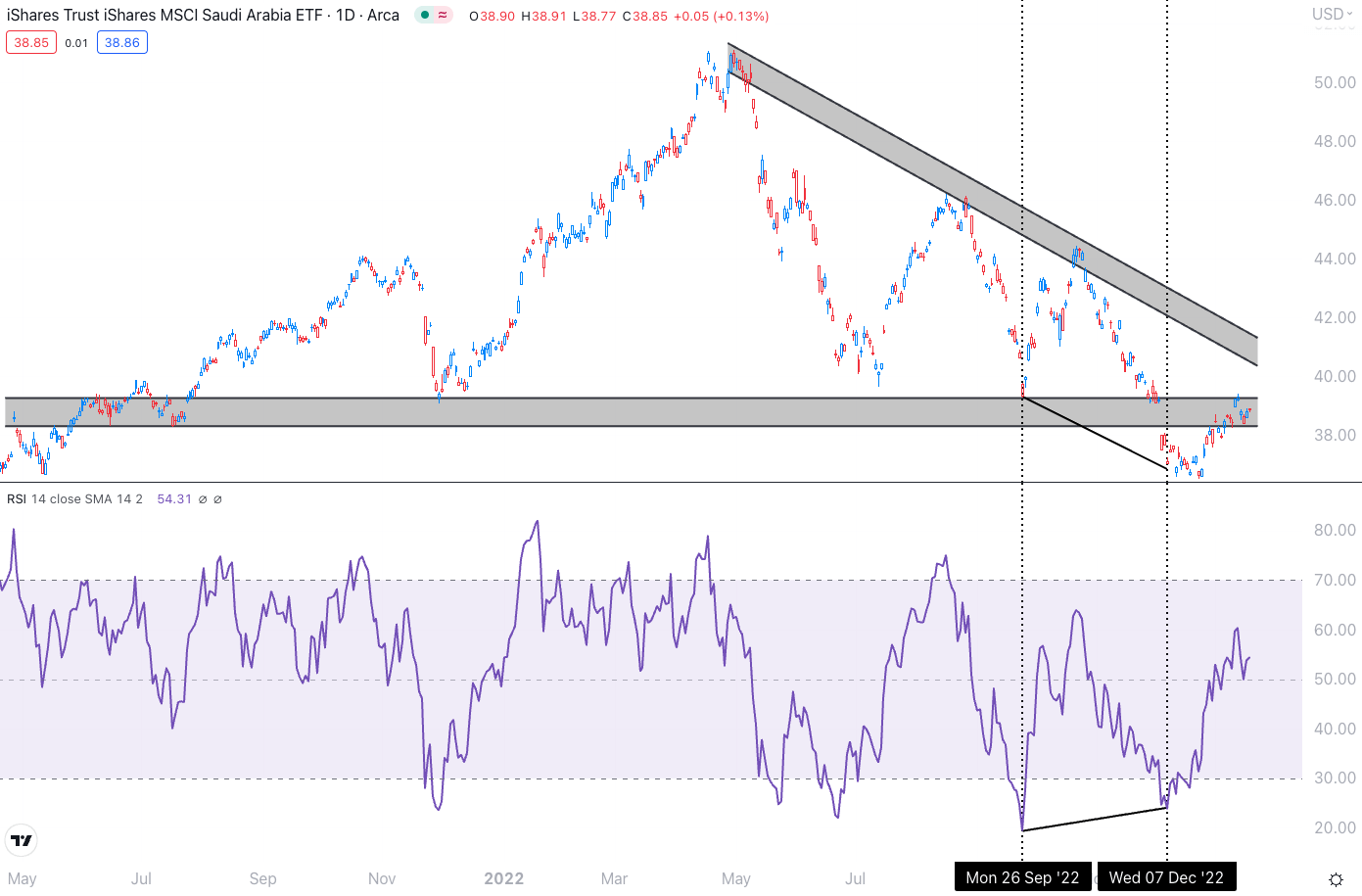

Viewing KSA through the lens of a technical analyst, there are reasons to be excited about shifting momentum. The relative strength index (RSI) is a popular oscillator used to indicate momentum. Divergence between the RSI and the direction of price action is generally seen as a critical signal that a reversal could be imminent. In the chart below, we can see that during the period between September and December, the price fell to a lower low while the RSI created a higher low. This was a sign that the strength of the downward momentum was waning – further confirmed by rising price action as we entered 2023.

TradingView.com

With price gapping below the horizontal support level in early December and subsequently filling the gap in recent trading days, a current short-term trading opportunity could exist from $39 to $41 per share, where price would encounter the declining resistance. If the downward trend is indeed weakening and possibly reversing, a price breakout above the declining resistance could be a great reason to enter a longer-term position.

Key Risks

There are a few key risks potential investors should consider with respect to KSA. The first is oil dependency, as a collapse in oil prices would likely be detrimental to many underlying holdings. Despite efforts to diversify away from the country’s dependency on oil, Saudi Arabia still relies on oil exports for a majority of its government funding. Falling oil prices would lead to a decrease in public spending, which would lead to higher unemployment. Oil exportation is also a major source of foreign currency for the country. Declining oil prices could result in an increase in import costs and lead to inflation.

Second, there are geopolitical risks as tensions with neighboring countries are difficult to predict, could escalate quickly, and are unique to the region. Saudi Arabia and Iran have a long-standing rivalry, mostly due to political and religious differences. And in the ongoing Yemen conflict, Saudi Arabia is leading a coalition opposing the Houthi rebels, who are aligned with Iran. Also, Saudi Arabia has had numerous disputes with Iraq and Kuwait involving oil production and borders.

Lastly, there’s cyclicality – the sector exposure is overweighted in sectors that tend to be more cyclical in nature. With more than 66% of the portfolio invested in financials and materials, KSA’s performance will heavily rely on the economy. KSA is positioned to perform very well during periods of economic growth, but will likely perform poorly if there were to be a recession.

Portfolio Construction Considerations

Through Dec. 31, 2022, KSA has generated three-year annualized returns of 9.01% with a three-year standard deviation of 20.92%. These are not particularly attractive historical risk-adjusted returns, and the volatility makes this strategy most useful for a small satellite allocation to most portfolios, not a core holding.

Investors are always making decisions on where to spend their risk budget, which depends on many factors such as overall risk tolerance, time horizon, and investment objectives. A small sleeve of KSA in a traditional investment portfolio brings unique return potentials via this novel investment. The offensive, cyclical nature of the strategy would pair well with defensive holdings.

Final Thoughts

The current investment environment has made it challenging to find opportunities to generate meaningful alpha. The potential macro tailwinds, strengthening technicals, and government initiatives significantly outweigh the risks, making KSA an attractive investment worth a strong consideration.

Be the first to comment